Amazon AMZN AWS good but retail sector not so much. (The stock is "over-owned" after many confidently professed the stock would blow thru $200 on improving fundamentals). Here.

Apple AAPL was fine but market won't like the comment that it is hard to quantify the AI contribution — and in the meantime they will continue to spend.

Apple Third Quarter Earnings Preview (224.09 +1.97)

Apple AAPL will report its third quarter earnings tonight after the close. There is a conference call scheduled for 17:00 ET.

Q3 FactSet consensus calls for EPS of $1.34 (versus $1.26 last year) on revenue of $84.43 bln (+3.2% yr/yr).

On the most recent conference call, the company said it sees Q3 total revenues up low single digits yr/yr. Co expects F/X headwind of 2.5%. The company also sees gross margin of 45.5-46.5% and expects iPad and services revenues to grow double digits.

Since the start of the pandemic, the company has switched from providing exact guidance in the press release to providing more vague guidance for the next quarter on the conference call. Q4 FactSet consensus calls for EPS of $1.55 and $93.36 bln.

Also, during the conference call, look for any update on rollout of Apple Intelligence and if it is having any impact on iPhone upgrades. Apple recently released developer beta for initial Apple Intelligence features.

The Street is expecting Q3 iPhone revenue to be $38.8 bln vs. $39.7 bln last year and services revenue of $24.1 bln vs. $21.2 bln last year.

AAPL has a $3.43 trillion valuation and currently trades at 35 times FY24 earnings.

Based on the weekly AAPL Weekly Aug02 $224.00 straddle, the options market is currently pricing in a move of ~5% in either direction by weekly expiration (Friday).

Suppliers to keep on note include: SWKS, CRUS, AVGO, QRVO, TSM, and QCOM.

More Tales From Nvidia: Mega-Cap Tech Accounting and Wild Market Moves

I am not sure investors realize how expensive stocks are.

There is a fair bit of interesting accounting these days, which makes the comparison to Y2K valuations not apples-apples. If you look on an FCF basis, which is ultimately what should matter, many are much more expensive now versus then:

There are probably a litany of accounting and use-of-cash issues making the comparison challenging.

One is all the stock options and cash required to buy them back to hold share count flat, especially at these prices.

Another interesting one is what is being done with depreciation schedules for AI CAPEX. They seem incredibly stretched, especially for a very immature technology, where much of it may be garbage. Even for mature technologies, much of this stuff still depreciates at a very rapid rate, especially the silicon. I would love to know the rate at which the hyperscalers are effectively depreciating the Nvidia NVDA GPUs, the same ones Nvidia is basically telling us will be obsolete when their new GPU comes out shortly. I would start watching the actual cash flow (and balance sheets) for the hyperscalers very closely.

Scroll through the above thread, there are some interesting observations. Here are two of them:

The related point is one of the reasons mega-cap tech is valued where it is, is because of the stock buybacks. But now we are at the point where they cannot shrink their share counts because they are valued so highly. Even prior to all of the AI spending, some have decimated their balance sheets playing this game, and borrowing low just to buy back stock. Apple now has about $100 billion of debt, and their net cash position seemingly drops every quarter. I suspect it will get harder and harder for companies to keep plowing cash into AI CAPEX and to keep buying back stock at the same rate.

Market Structure Concerns

Then a side point. The market is really broken. The degree of moves are just stunning. Nvidia added $550 billion of market-cap yesterday on no company-specific news. A 10% move used to be considered a very good year — now it can happen daily, on vapors, even for huge companies that are liquid, which blows my mind. Today NVDA is giving a lot of it back on no company-specific news. To put $550 billion in perspective, Exxon’s XOM total market cap is $461 billion. Goldman Sachs' GS market cap is $160 billion.

Something tells me the algos basically all trade on the same factors. The pods are all running the same risk models. Then all of the short-term options and other crap. There is way too much auto-correlation built into the markets.

The U.S. debtload hit $35 trillion three days ago.

The U.S. is adding $196 billion of new debt every month and $6.4 billion of new debt every day. That equates to $268 million in new debt every hour, $4.5 million in new debt every minute and $75,000 in new debt every second.

There are only three ways we can deal with our burgeoning debt load — higher inflation, the erosion in the value of our currency or default.

We desperately need to gain control of our deficit.

To do so, we must reduce spending and implement tax reform.

Unfortunately the political will does not exist so the outcome of the November election won't change things. Neither party is addressing this significant problem and neither party is securing our financial future — as they would likely face political extinction if they told the voters the truth of what has to be done.

By not addressing our future and continuing with a policy of self-destruction our leaders are compromising our ability to solve other problems at home and abroad.

With Procter & Gamble PG (+$4.40) benefiting from a rotation out of technology, I have reduced my position at $165.17/share back to small sized (after picking stock up on weakness after the disappointing EPS report).

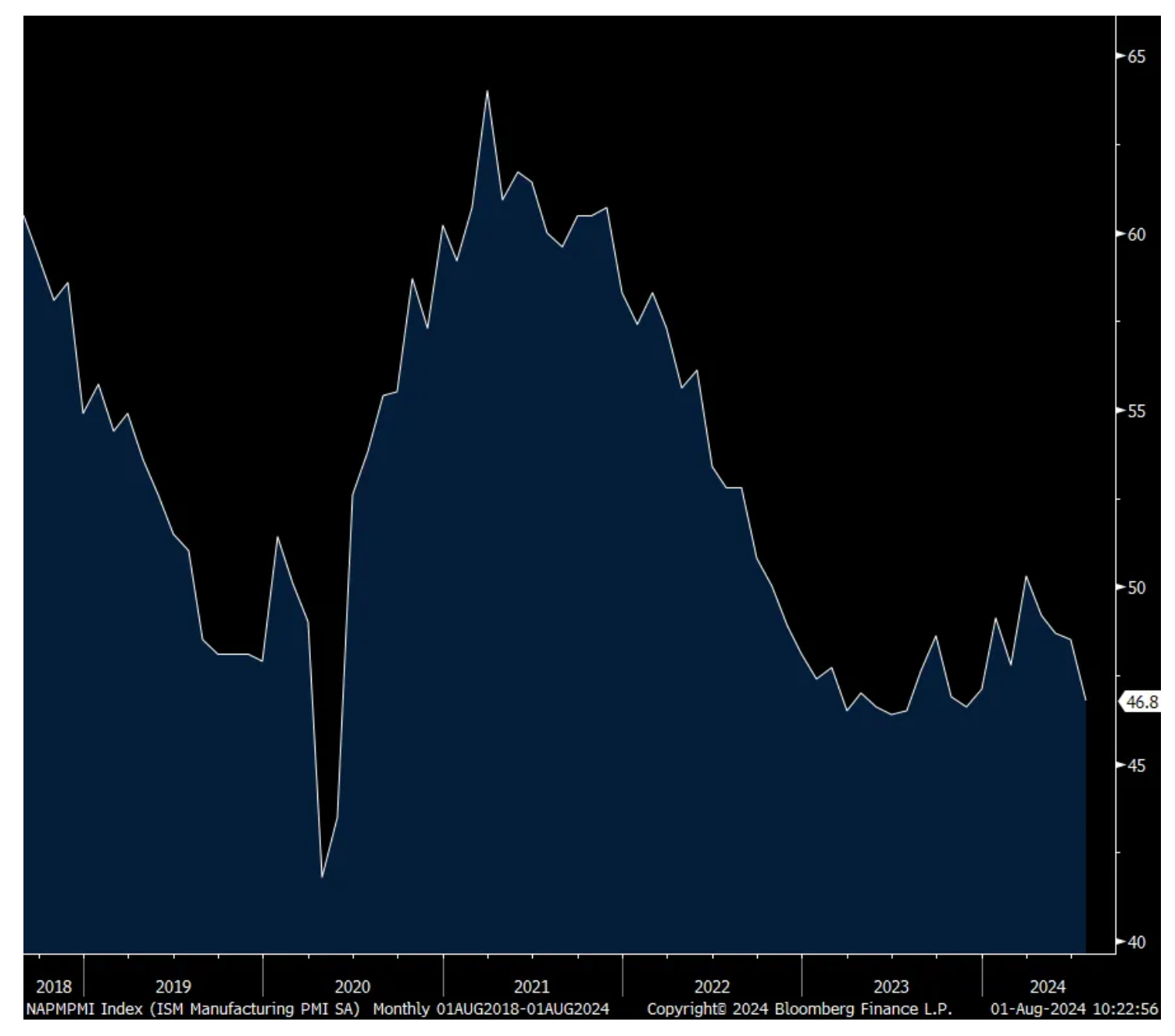

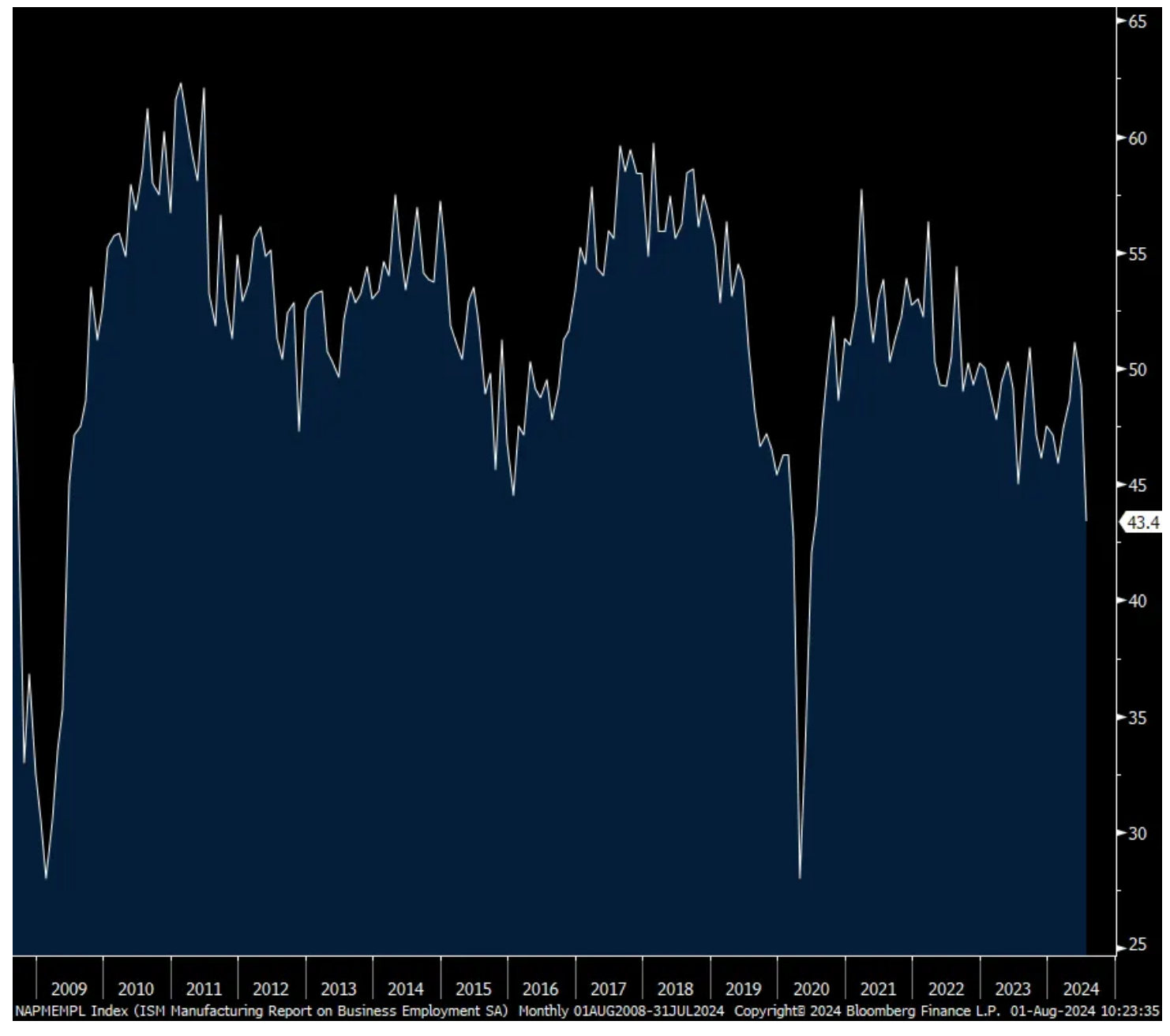

ISM mfr'g still soft and now the employment component is buckling

The July ISM manufacturing index continued its string of below 50 prints as it fell to 46.8 from 48.5. That’s the lowest since November. New orders too as they fell almost 2 pts to 47.4 while backlogs were unchanged at well below 50 at 41.7. No inventory build just yet even though things remain lean at 44.5 and with the customer inventory figure at 45.8. Ahead of tomorrow’s jobs data, the employment component fell to just 43.4, the lowest since May 2009 not including the Covid plunge. Supplier deliveries jumped back above 50 at 52.6 and I wonder if some of that is related to the container shipping issues. Prices paid rose .8 pts to 52.9 but after falling by about 5 pts last month. Export orders were little changed but still below 50 at 49.

Specifically on the employment component, the ISM said “Respondents’ companies are continuing to reduce head counts through layoffs, attrition and hiring freezes. Panelists’ comments in July indicated a notable increase in staff reductions compared to June, supported by the approximately 1 to 1.8 ratio of hiring vs head count reduction comments.” Just 2 of 18 industries saw a rise in employment.

On inventories, “None of the six big industries reported increased manufacturing inventories in July. Continuing demand uncertainty is causing panelists’ companies to reduce investment in inventory and remain reliant on suppliers to carry ‘on demand’ inventory.”

On exports, “As was experienced in June, new export orders remain sluggish as international trading partners continue to struggle with weak economies.”

On pricing, “Commodity prices continue to be volatile, especially oil, natural gas, aluminum and plastic resins. Steel prices have reached long term historical lows, supported by declining scrap prices. 23% of companies reported higher prices in July, compared to 20% in June.”

Breadth weakened as just 5 industries saw growth vs 8 last month while 11 said their business is contracting vs 9 in June.

ISM said “US manufacturing activity entered deeper into contraction. Demand was weak again, output declined, and inputs stayed generally accommodative…Demand remains subdued, as companies show an unwillingness to invest in capital and inventory due to current federal monetary policy and other conditions. Production execution was down compared to June, likely adding to revenue declines, putting additional pressure on profitability.”

The anecdotal comments from companies in a variety of industries reflect the weakness seen in the survey.

“Business is relatively flat — the same volume, but smaller orders.” [Chemical Products]

“Demand continued to soften into the second half of the year. Supply chain pipelines and inventories remain full, reducing the need for overtime. Geopolitical issues between China and Taiwan as well as the election in November remain weighing concerns.” [Transportation Equipment]

“Even though we are used to a seasonal reduction in business over the summer, consumer behavior is changing more than normal. Sales are lighter, and customer orders are coming in under forecasts. It seems consumers are starting to pull back on spending.” [Food, Beverage & Tobacco Products]

“Availability of parts is good, with small exceptions of missing materials here and there. Ordering is still well below typical levels as we continue to burn down inventory of raw goods, with ‘normal’ ordering trends expected to return sometime in the second half of 2024.” [Computer & Electronic Products]

“It seems that the economy is slowing down significantly. The number of sales calls received from new suppliers is increasing significantly. Our own order backlog is also diminishing. We are hoping for an increase in customer demand, or we will possibly need to make organizational changes.” [Machinery]

“Unfortunately, our business is experiencing the sharpest decline in order levels in a year. We were well below our budget target in June; as a result, it was the first month this year that we had negative net income.” [Fabricated Metal Products]

“Business is slowing, and we are taking cost actions.” [Electrical Equipment, Appliances & Components]

“Some markets that are usually unwavering are showing weakness. Weather is the common factor, but only so much.” [Nonmetallic Mineral Products]

“Our sales forecast for July and August are slow, but we’re making every attempt to remedy that situation. Our medical end-user customers continue to meet their forecasts, which is promising.” [Textile Mills]

“Elevated financing costs have dampened demand for residential investment. This has reduced our need for component products and inventory.” [Wood Products]

My bottom line, just as I thought we were seeing signs of manufacturing bottoming with hoped for inventory restocking, it seems to have taken a leg down and now we’re seeing a further deterioration in the labor market within manufacturing.

Treasury yields are at the lows of the morning with the 10 yr below 4.00%. I see around the 3.85% level as the key spot as that was the starting point to 5% last summer when the BoJ widened yield curve control.

Doesn’t work…but boy the brinksmanship between all of these CEOs on the conference calls.

Eventually it hits the P&L and they will feel pressure too, especially as investors are starting to recognize this stuff really doesn’t work and the economics are terrible:

* With S&P cash -43 handles I have covered all my short caIls on the Indices

* I will reshort strength

Doug Kass

With S and P cash now -44 handles (or about 85 handles below the day's high) I have taken off all of my short Index calls.I now have no position in the Indices....

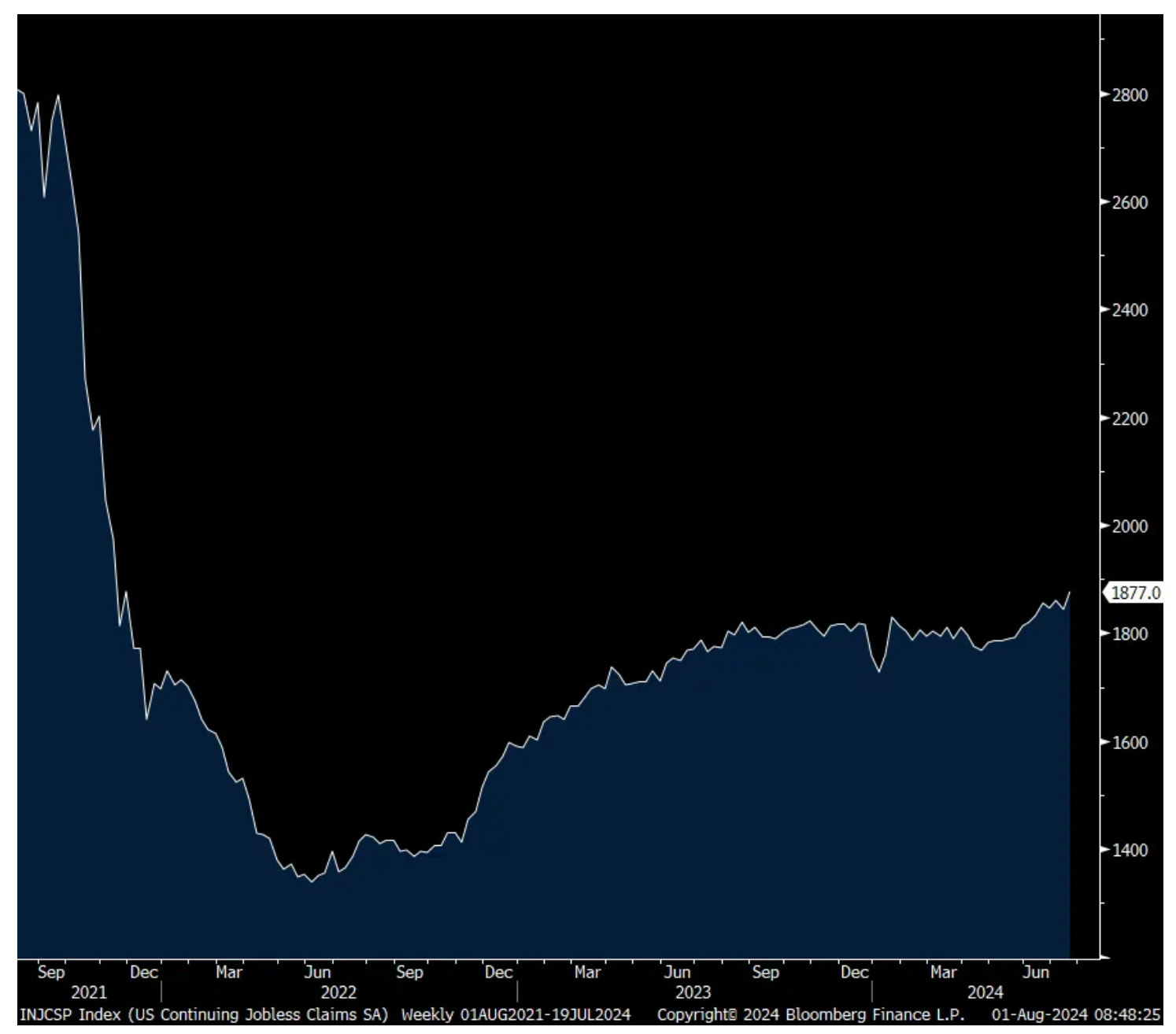

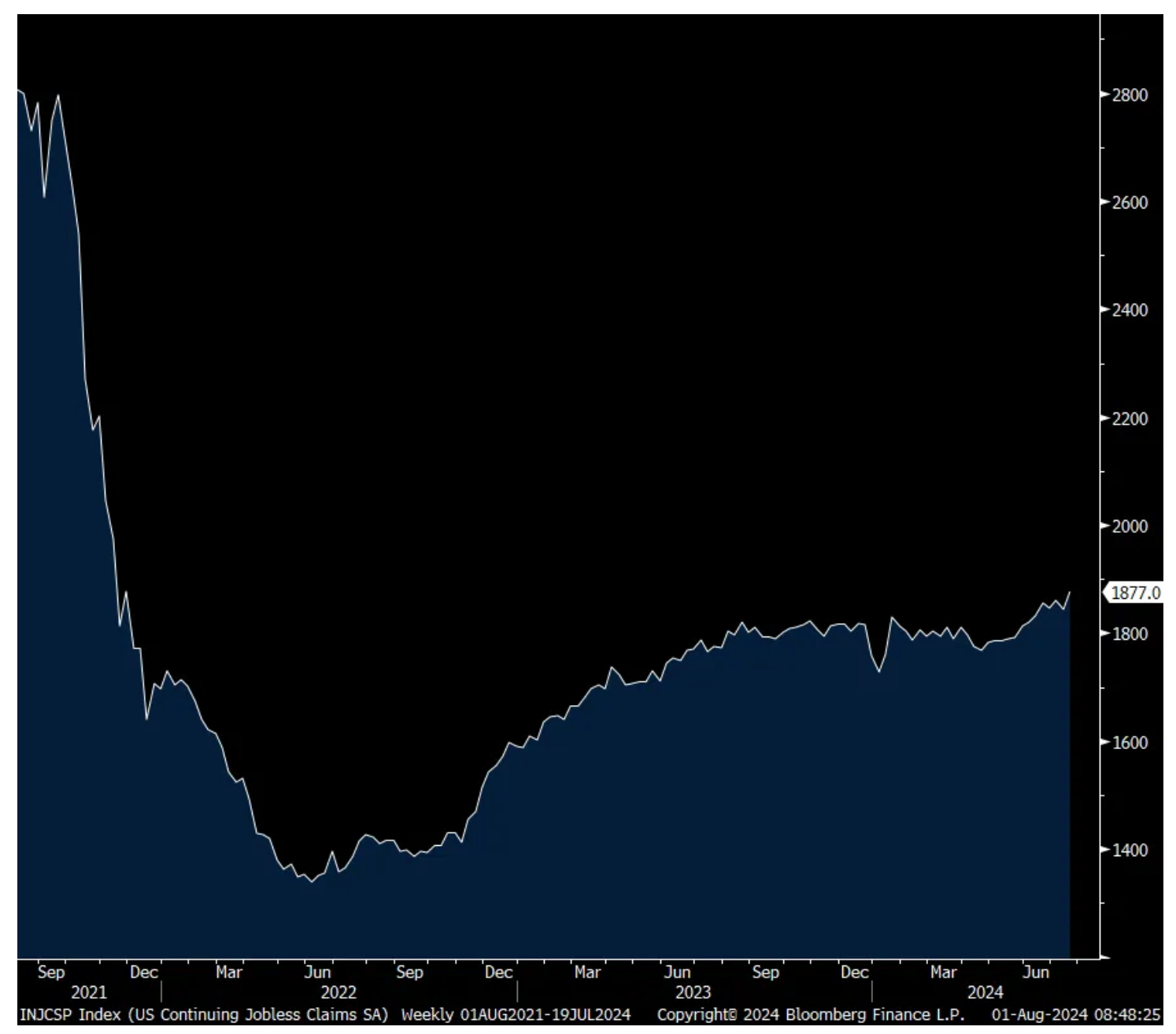

Initial jobless claims rose to 249k from 235k, the highest one week print since August 2023 and that was 13k more than expected. This brings the 4 week average to 238k from 236k and that is just below the highest since last summer. Continuing claims rose to 1.877mm, the most since November 2021 and up from 1.844mm in the week before.

Bottom line, the US labor market continues to soften.

Also out and confirming this, the Challenger report saw a drop in job cuts m/o/m but a rise by 9% y/o/y. Also, the announced hiring’s fell to the lowest monthly total since December 2023 and it is the slowest July since they started calculating hiring’s in 2009. They said, “The job market is indeed cooling, with hiring at the lowest point in over a decade. While we are seeing increased cuts in manufacturing sectors, both consumer and industrial, most industries are cutting below last year’s levels.” Tech continues to lead the pace of job cuts but has slowed by half from what was seen in 2023. So while there has been a rise in initial jobless claims, there still seems to be a desire to stick with ones employees as much as they can.

‘Why are Companies Cutting?’ asks Challenger, “Cost cutting is the leading cause for job cuts in July.” Don’t blame AI, “Companies have not cited technology, with AI directly or due to ‘technological’ update for any job cuts since April.”

4 Week Avg Initial Claims

Continuing Claims

Q2 productivity rose more than expected, by 2.3% q/o/q annualized. The estimate was 1.8% and follows a .4% increase in Q1. Versus last year, productivity was up 2.7% y/o/y and is the 4th quarter in a row with a 2 handle after a multi year stretch of subpar growth as we managed thru Covid.

After a 3.8% jump in Q1, unit labor costs were up .9% and are up .5% y/o/y.

Bottom line, coincident with the slowing labor market and reduced hours as seen with the monthly hours worked, while output is still pretty good, mathematically we’re seeing good productivity numbers and lower unit labor costs.

Treasuries are little changed in response to both data points but of course after a big late rally yesterday.

The Market Fallacy: Do You Really Believe in Goldilocks?

* A few interest rate cuts will likely fail to stabilize/improve the US economy

* Just as the lag of monetary tightening was longer than expected (it was different that time (2022-24)!), so may the easing have a lengthier impact (and be different this time (2024-26)!)

* The Fed may be ultimately forced to more aggressively ease next year, raising fears of a resurgence of inflation "down the road"

* The herd/consensus - acting like Pavlov's dogs- may again be wrong in its bullish thesis

a mistaken belief, especially one based on unsound argument.

"the notion that the camera never lies is a fallacy"

Open market interest rates have slipped over the last two weeks - coincident with market participants' expectations that the Federal Reserve might lower the Fed Funds rate twice this year.

As a direct result, equities have rallied from the July lows as optimism that rate cuts will spur economic growth.

We think that economic (and stock market) optimism is overdone for some of the following reasons:

* The U.S. economy is far less interest-rate sensitive than previously assumed.

* It took the Fed undertaking the most rapid increase in interest rates in decades to slowly dull domestic economic growth - it follows that it will likely take a rapid decline in interest rates to stabilize/improve economic growth in the U.S.

* It has taken more and more debt and money creation to generate a unit of production over the last decade.

* The stacked inflation (since 2020) is unique to the last few decades and remains a headwind to the consumer - and no rate cut changes its cumulative impact.

* Also unique is the U.S. deficit and burgeoning debt load which acts, increasingly, as a governor to economic growth.

* A large swath of disadvantaged U.S. consumers ("the have nots") may not have access to lower cost credit. Underwriting standards will tighten further as the economy moves lower. Moreover, it is unlikely that credit card rates will be lowered commensurate with reduced open market rates.

One vivid example of a changing rate/economy relationship can be seen in the housing market, which was misforecast by the Federal Reserve and by economists. After 15 years of zero interest rates, consumers had materially reduced their mortgage rates (through new mortgages and refinancings) - rendering a reluctance to substitute a 3% mortgage rate with a 7% mortgage rate. As a result the supply of homes for sale contracted and home prices remained firm.

Lower interest rates may have the opposite intended effect (especially when it coincides with higher unemployment) - by finally increasing the supply of homes for sale, serving to pressure home prices.

Bottom line

Goldilocks is still a well-embedded narrative - reinforced by the economic cheer leading by Chairman Powell (and his feckless Federal Reserve) yesterday.

The bullish cabal is likely to be disappointed in the next six to 12 months.

Finally, a reminder: Buying stocks in October 2007 when the Fed first cut rates was a poor idea - as it was when the Fed (under Greenspan) cut rates in 2000.

More on this theme of reduced economic rate sensitivity in the next few days...

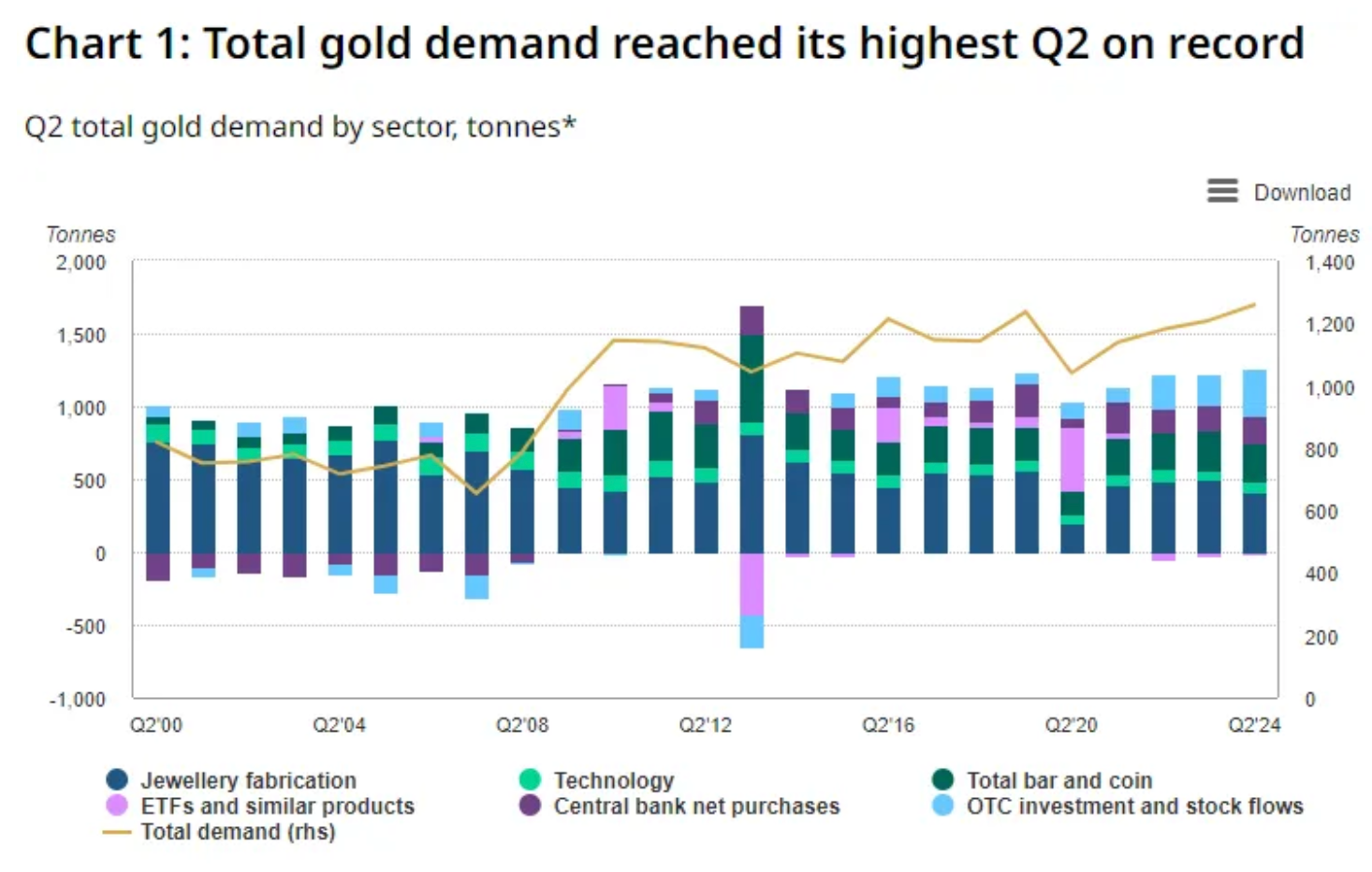

I'm going to start today with gold as the World Gold Council came out with its Q2 data on Tuesday. Including over the counter transactions "to total gold demand yields a 4% y/o/y increase to 1,258 tons - the highest Q2 in our data series back to 2000." OTC buying totaled 329 tons and the biggest buyer in the quarter and assume that these are investment flows. The other big buyer, the central banks, bought 184 tons, up 6% y/o/y, "driven by the need for portfolio protection and diversification." Interesting was this, "Gold used in technology jumped 11% y/o/y, as the AI trend continued to drive demand in the sector." Gold is rarely used in industrial uses as opposed to silver that is. Supply did keep up with demand in Q2 as it rose 4% y/o/y due to record mine production for a 2nd quarter along with higher recycling. We remain bullish and long both gold and silver, and some miners too.

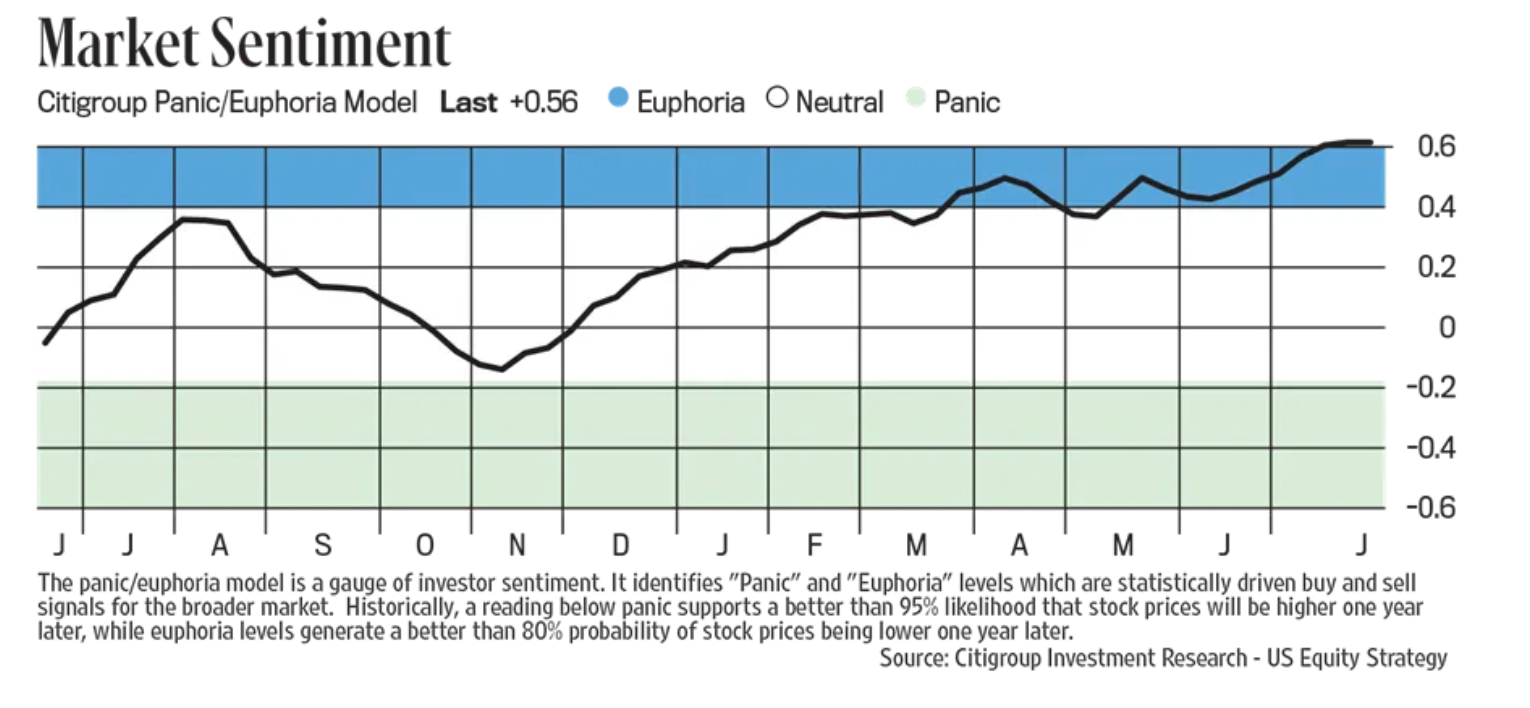

A major factor in the set up for the pullback in stocks over the past few weeks was excessively bullish sentiment. The Citi Panic/Euphoria index as of last weekend remained well into Euphoria territory. Bulls fell to 59.4 from 64.2 last week but still remains well above Bears which came in at 15.6 vs 14.9 in the week before. As stated before, a spread above 40 is extreme. The more fickle and volatile AAII today said Bulls rose 1.7 pts w/o/w to 44.9 after falling by 9.5 pts last week. Bears quickly disappeared, falling 6.5 pts to 25.2 after rising by 8.3 pts in the week before. A widespread remains here.

Bottom line, just looking at still optimistic sentiment tells me that this correction is not over. We need to ring out this giddiness.

Rather than waiting for inflation to sustainably trend around 2%, the Bank of England is doing what the ECB and BoC are doing and catching that falling inflation knife by cutting rates by 25 bps to 5.00% and I'd say it was about 50/50 on whether they would move. The vote was very tight, 5-4 with the 4 wanting to stay put. In the statement, they said while they are currently at 2% in headline CPI, they expect it to rise to 2 3/4% in the back half of the year "as declines in energy prices last year fall out of the annual comparison, revealing more clearly the prevailing persistence of domestic inflationary pressure." But they still cut rates nonetheless and even with services inflation running at 5.7% and wages by a similar amount.

Why did they cut in the face of this? As they expect inflation pressures to further recede (they have fingers crossed), "It is now appropriate to reduce slightly the degree of policy restrictiveness." And they followed this up by saying "Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further."

Bottom line, this was clearly a 'tweak' cut and nothing more, as of now. The 2 yr gilt yield is down 6 bps after falling by 5 yesterday. The 10 yr is lower by 3 bps. Inflation breakevens are little changed and the pound is lower by .5% vs the USD. The FTSE 100 is flattish, not benefiting much from the cut.

With the earnings calls, let's start with Meta and whose revenue grew by 22% y/o/y:

"We estimate that there are now more than 3.2 billion people using at least one or our apps each day." There are about 8 billion people in the world by the way. Zuckerberg then went quickly into AI and what it "means for our family of apps and core business." The CFO later said, "Looking forward, we believe generative AI will play a growing role in how businesses market and engage with customers at scale."

"Within ad revenue, the online commerce vertical was the largest contributor to y/o/y growth, followed by gaming and entertainment and media. On a user geography basis, ad revenue growth was strongest in Rest of World and Europe at 33% and 26%, respectively. Asia Pacific grew 20% and North America grew 17%."

Their cap ex outlook is $37b to $40b for the full year from their previous range of $35b to $40b. "While we continue to refine our plans for next year, we currently expect significant cap ex growth in 2025, as we invest to support our AI research and our product development efforts." And as a result, "we expect infrastructure costs will be a significant driver of expense growth next year as we recognize depreciation and operating costs associated with our expanded infrastructure."

On the digital ad market, "We're continuing to see healthy global advertising demand...We do expect y/o/y growth to slow in Q3 as we are lapping strong growth from China based advertisers as well as strong reels impression growth from a year ago, and we also expect modestly larger FX headwinds in Q3 based on current rates." Assume those Chinese companies are mostly Temu and Shein.

CDW is a very important company many have not heard of as they are a major distributor of everything tech including hardware, software, computers, cloud computing mobile devices, security, and network communication. It's stock fell 6% yesterday.

"2nd quarter market dynamics played out roughly as we expected. Cautious customer behavior once again elongated sales cycles and drove prioritization of needs over wants and cost savings over expansion. Capital investment in complex solutions, particularly those tied to data center and network modernization, continued to be downsized or put on hold and there was growing refresh activity in client devices. What was not expected were two end market specific dynamics, a worsening in the UK environment, and further federal funding challenges (in the US)."

Also, "Conversion remains challenging with uncertainty weighing on our customers' appetite to spend."

"Small business did not see significant refresh activity and while increasing mid-single digits sequentially, client devices declined slightly y/o/y in the quarter."

"Given these market conditions, our updated full year 2024 expectation is for flat to low single digit gross profit growth, a view that incorporates both our slower start to the year and our view that the mild recovery we anticipated in the 2nd half is not likely to materialize."

EBAY grew revenues by 2% y/o/y and gross merchandise volume by 1% and mentioned delivering this "amid continued macroeconomic headwinds, ongoing geopolitical uncertainty, and an evolving regulatory landscape."

"as we've said over the past few quarters, we've seen some shifts in consumer spend driven by the macro environment as cost-conscious consumers are increasingly searching for value." EBAY definitely delivers on that.

"our luxury category is still positive and has been for six straight quarters, so I think there's more pressure on the less affluent customers in the consumer market."

Mastercard is not just a play on consumer spending but the secular shift away from using cash so we need to remember that when they talk about their business:

"The macroeconomic environment remains mixed, and we continue to monitor the positives and negatives.

From Marriott:

They had a good quarter but not good enough and said "As we look ahead to the full year, we are narrowing our global RevPAR range to 3% to 4% growth, largely due to anticipated continued weakness in Greater China...We expect a continuation of current weak demand and pricing trends in the region, with a 3rd quarter anticipated to see the most meaningful RevPAR decline, as outbound travel accelerates during summer holidays." China makes up around 7% of RevPAR related fees for them and 10% of open rooms.

In addition, "we also expect marginally lower full year RevPAR in the US and Canada than we had previously anticipated, in part due to less Group business the first two weeks of November, given the intense focus on the US presidential election. Overall RevPAR trends in the US and Canada in the back half of the year are expected to remain relatively steady with the first six months of the year."

"On customer segment, worldwide RevPAR growth is well anticipated to be driven by another year of strong growth in Group revenue, continued improvement in business transient revenues, and slower, but still growing, leisure revenues."

Cheesecake Factory saw 1.4% comps for Q2 "meaningfully outperforming the casual dining industry resulting in record high Cheesecake Factory restaurant average weekly sales as well as total consolidated revenues." They did though see 2% negative traffic by the end of the quarter vs being positive by July 4th holiday weekend.

"We view the environment as being relatively tough and transitory, notwithstanding the outperformance in some of our concepts. I think we've seen a little bit of alcohol trade down."

On inflation, "We currently estimate total inflation across our commodity baskets, labor, and other operating expenses to be in the low to mid single digit range, and fairly consistent across the quarters."

From Autonation:

"the CDK outage masked what was developing into a very positive quarter...April and May, new unit sales were up about 5%" but ended up down 3% because of the outage. Used vehicle sales were tracking flat thru May but ended lower by 8% y/o/y also due to the outage.

"Average used vehicle selling prices moderated y/o/y by 5% reflecting the shift to lower priced used vehicles. Demand for those lower priced used vehicles remains resilient."

To a question on the consumer and the affordability challenges many have, "I think there's no doubt that affordability is top of mind for many of the consumers that come into this marketplace, whether it's on new or used vehicles. I mentioned the fact that if you look at our CFS (consumer financial services) performance, it's moderated very slightly. That was about product detachment rates, and that is all about not desire for the product per se, but it's all about managing to a monthly budget."

Also, "So I think that there are impacts in the marketplace. You're also beginning to see increases, I think, in delinquency rates that I think are manageable and not where they were a year ago, but I do think there are signs in the marketplace that consumers continue to feel pressure from the current environment."

Here were the manufacturing PMI's seen in Asia and they're mixed:

From The Street of Dreams: What a Difference a Day Makes

From JPMorgan:

· US: Futs are higher with Tech outperforming in RTY futs in the red, following the same trend seen late day yesterday; futs have given back gains potentially on geopolitical headlines. Pre-mkt, META +7% following earnings and AAPL +60bps, AMZN +1.1% ahead of earnings later. Semis are up small with NVDA +20bps. Bond yields are higher by 2-3bps which is boosting the USD to potentially its best day in 2 weeks. Cmdtys are bid with Energy and base metals leading. Today’s macro data focus is on ISM-Mfg, and mkt likely ignores jobs data ahead of tmrw’s NFP. AMZN/AAPL headline today’s earnings schedule.

and...

EQUITY AND MACRO NARRATIVE: What a difference a day makes. A combination of dovish macro data, reassurance from MSFT and Semis to support he AI/Tech trade, and dovish Powell led to an “Everything Rally”. Post-market, META and QCOM earnings are additive to those playing the rebound in the Tech trade. NDX futures are sitting on their 50dma, so a move through that could bring back the outflows seen over the last two weeks. Regarding AI, META’s earnings are another supportive point for the market as Paige Hanson tells us, “…capex message quite bullish as the co raises FY24 capex to $38.5bn at midpoint (consensus $37.5bn) and importantly, expects “significant capex growth in 2025” off that higher FY24 guide. META +4.5% after hours.”

These were my initial thoughts on the Fed statement:

“Nothing notable in the statement and press conference is likely the same. If the bond market takes this as hawkish and Equities decline, would consider buying that dip. The economy remains in good shape. Inflation is solved. The Fed’s next action is a cut. That formula is bullish. While much of July has been a somewhat perplexing trading environment the stage is set for a broad-based rally to ensue. I still like the barbell trade of Tech (Mag7 and Semis) and Cyclicals/Value (Banks, Credit Cards, Homebuilders, and Autos). Recent conversation point to some investors preparing to re-short, small-caps and weaker balance sheet types of names including RTY, Spicier parts of Tech, and Regional Banks, among others.”

· Our Chief US Economist Mike Feroli reinforces the view that September cuts have been cemented, “The conclusion is that rate cuts are imminent as policy may soon be too restrictive. Widespread expectations (including ours) for a cut in September are intact following today’s statement.”

The press conference cemented views of a September cut with hawks/Bears pointing to Jackson Hole for a possible pivot or for opening the door to a 50bps cut as some investors feel the Fed is already behind the curve, evidenced by comments from former Fed members. The bond market increased its view that the Fed will cut three times this year. Interestingly, bonds barely moved yesterday, and my colleague Marissa Gitler tells us, “Market was/is looking for a dovish angle here.. UST curves have re-steepened a bit, the totality of the move on the day is actually fairly minimal in the treasury complex. Belly of the curve witnessing a stronger bid on the margin … Equity market on the other hand is ripping.. (small caps especially) ; something to keep in mind.. Is where the mkt started head into the print.. this is a majority of the reason the px moves on the day are so standout... Equities were already extremely elevated pre-Powell (due to re-grossing in tech/earnings-related buying) ; the presser is giving no reason to shed these positions.”

What should we do? My friends in Equity Derivatives mention that it is prudent to have some downside hedges in case we see a snapback in markets given the Equity vs. Treasuries moves (and USD, too); the team have mentioned IWM and OQQ puts/put spreads as well as VIX upside as being particularly compelling. This is illustrated by the move seen in RTY which moved higher ~2% during the press conference before reversing lower and erasing almost 100% of that move.

Separately, Mastercard (MA) earnings pointed to a still resilient consumer. Their management noted that consumer spending strength is supported by a solid labor market and wage growth, although there are signs of labor market loosening. The company flags its AI usage as being used in fraud prevention measures and corporate decision-making, though it has being using ML tech over the last decade.

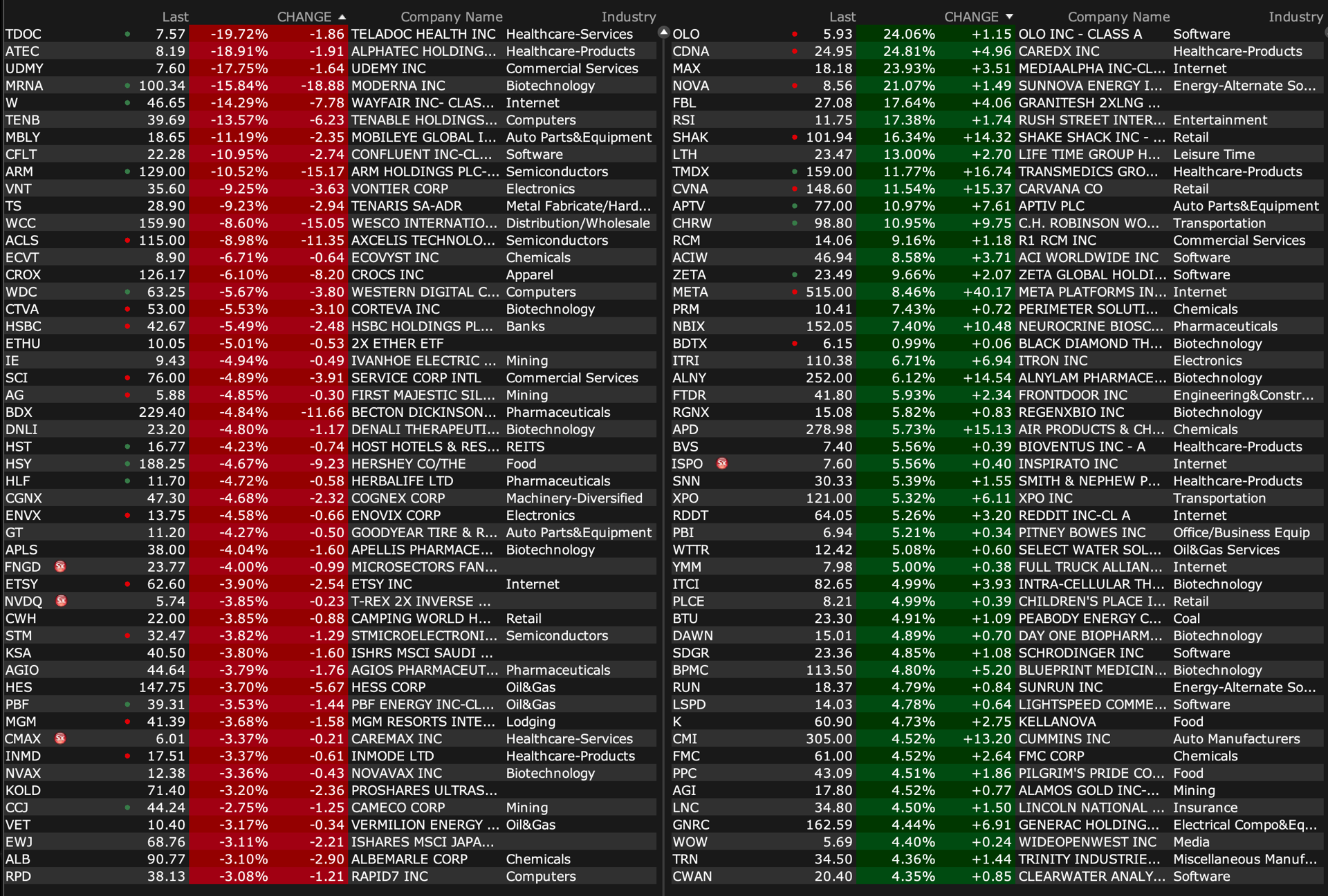

The U.S. select premarket movers as of 8:49 a.m. ET:

Upside:

-IMRX +30% (granted FDA Fast Track Designation for IMM-1-104 in First-line Pancreatic Cancer)

-MAX +24% (earnings, guidance)

-OLO +21% (earnings, guidance)

-NOVA +20% (earnings, guidance)

-RSI +19% (earnings, guidance)

-EOLS +17% (earnings, guidance)

-SHAK +15% (earnings, guidance)

-EXAS +13% (earnings, guidance)

-TMDX +12% (earnings, guidance)

-CVNA +11% (earnings, guidance)

-CHRW +10% (earnings, guidance)

-RCM +9.1% (to be acquired by TowerBrook and CD&R for $14.30/shr in cash)

-META +8.9% (earnings, guidance)

-ZETA +8.5% (earnings, guidance)

-SABR +7.6% (earnings, guidance)

-IDCC +6.7% (earnings, guidance)

-ITRI +6.7% (earnings, guidance)

-MX +5.9% (earnings, guidance)

-RDDT +5.3% (acquires Memorable AI, a startup that uses generative AI to help marketers create better ads)

-CMI +4.5% (earnings, guidance)

-FMC +4.5% (earnings, guidance)

-CRVS +4.3% (granted FDA Fast Track Designation for Soquelitinib for Treatment of Patients with Relapsed or Refractory Peripheral T-cell Lymphoma)

-K +4.0% (earnings, guidance)

-LLY +3.7% (Tirzepatide successful in phase 3 study showing benefit in adults with heart failure with preserved ejection fraction and obesity)

-RELY +3.5% (earnings, guidance)

Downside:

-ALXO -32% (reports topline data from ASPEN-06 Phase 2 trial)

-ATEC -19% (earnings, guidance)

-TDOC -18% (earnings)

-UDMY -16% (earnings, guidance)

-MRNA -14% (earnings, guidance)

-TENB -14% (earnings, guidance)

-W -14% (earnings, guidance)

-MDXG -13% (earnings, guidance)

-CFLT -12% (earnings, guidance)

-LAB -11% (earnings, guidance)

-AUR -10% (earnings)

-MBLY -9.3% (earnings, guidance)

-ARM -9.1% (earnings, guidance)

-OCGN -8.9% (prices 30.4M shares at $1.15/share)

-ACLS -7.9% (earnings, guidance)

-HTZ -7.1% (earnings)

-MYRG -7.6% (earnings)

-CTVA -5.5% (earnings, guidance)

-HSY -5.3% (earnings, guidance)

-ENVX -4.9% (earnings)

-WDC -4.6% (earnings, guidance)

-ETSY -4.0% (earnings, guidance)

-CGNX -2.7% (earnings, guidance)

-HLVX -2.2% (announces 40% reduction in workforce; explores the potential for continued development of its HIL-214 and HIL-216 norovirus vaccine candidates)