A Rally Out of Left Field

Let's take a technical look at what just whizzed by Wall Street Monday, and pay tribute to the Pride of the Mets.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Oh, somewhere in this favored land the sun is shining bright;

the band is playing somewhere and somewhere hearts are light,

and somewhere men are laughing, and somewhere children shout;

but little boys buried deep inside of old men cried last night,

for our favorite shining light has flamed out.

RIP, Ed Kranepool (1944-2024) ... Pride of the Mets.

- adapted from "Casey at the Bat" by Ernest Thayer

A Rally?

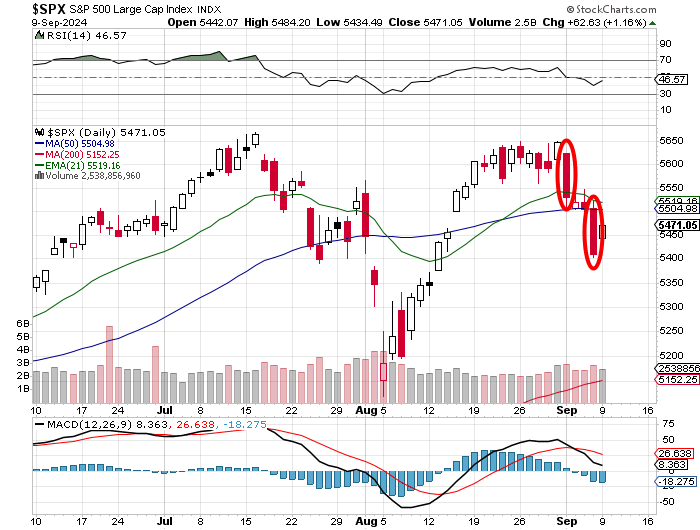

For real? After that double-top pattern had formed? After last week, the S&P 500 had presented chart-watchers with both a day-one selloff and a follow-through day? After the daily Moving Average Convergence Divergence indicator for that same S&P 500 had displayed the "cross-under" of the 26-day exponential moving average by the 12-day exponential moving average with the histogram of the 9-day exponential moving average in negative territory? Those would be quite bearish conditions. Yes, they would.

Still, there was a rally. A strong rally. Does it count? Was it meaningful? Take another look at the daily chart:

While the reading for Relative Strength is neutral and has been neutral for almost two months, that daily MACD is postured quite bearishly. The "day one" and the "follow-through" day are both circled in red. The double-top reversal is as clear as a bell, with the Aug. 5 low of 5,119 serving not as a downside target, but quite possibly as the pivot. Should that play out, this scenario would put the April lows of 4,953 in play. (But I am by no means certain it will play out, as the traditional rally season of late October / early November into the year's end lies ahead and this is an election year.)

Put bluntly, there is good reason to keep one's head on a swivel right now and behave more defensively and less aggressively than if conditions were normal. On the bright side, Monday was an "inside day," which means that the entire daily candle fits inside of the candle from the prior day. That is usually taken as a sign of cooling volatility.

Disappointingly, despite the rally, the S&P 500 lost contact with its own 50-day simple moving average on Monday. The index might not have a lot of time to re-engage with that level before the algorithms that game price discovery and often force overshoot (note both Friday and Monday as evidence) decide to target the 200-day simple moving average. Keep your eyes on the 21-day exponential moving average, should that line cross below the 50-day simple moving average (baby death cross), the swing crowd will indeed swing.

Marketplace Gains

On Monday, the S&P 500 gained back 1.16% as did the Nasdaq Composite. How algorithmic, I mean odd, is that? The Philadelphia Semiconductors (+2.15%) who were absolutely roasted last week, led the session, with the KBW Banks (+1.81%) close behind. Small caps did not really participate on Monday. The small-cap Russell 2000 gained 0.3% for the day, but the S&P 600 gave up 0.25%.

All 11 S&P sector SPDR exchange-traded funds closed out the Monday session in the green, led by Technology XLK and the Industrials XLI as Communication Services XLC posted the best last place finish (+0.43%) we've seen in quite a bit. Arm Holdings ARM led tech and the semis, gaining 7.03% as Apple AAPL revealed ARM's involvement in the release of the iPhone 16 series.

Winners beat losers by almost 2 to 1 at the New York Stock Exchange, and by a rough 3 to 2 at the Nasdaq on Monday. Advancing volume took a 70.6% share of composite NYSE-listed trade and a 67.3% share of composite Nasdaq-listed activity, so breadth was certainly minty fresh. Unfortunately, overall trading volume was not really there. Aggregate trade across NYSE-listed securities was really flat (up very small, a smidgen), but aggregate trade across Nasdaq-listed securities was down 7.5% day over day.

So, was Monday's price discovery meaningful? Without being sure, I have my doubts. The presidential debate is tonight. I am not sure how much of an impact that might have upon financial markets, but with one candidate suggesting higher corporate taxes and one candidate suggesting lower corporate taxes, I don't think it too difficult to figure out which candidate equity markets, in the very short-term, would be rooting for.

Probably even more important, at least to the algos that run everything, will be the August CPI data, scheduled for release on Wednesday morning. Basically, I see good reason for Monday's "inside day" and a little more sideways movement would not surprise if this weeks' events lend little in the way of clarity moving forward.

On That 'Note' ...

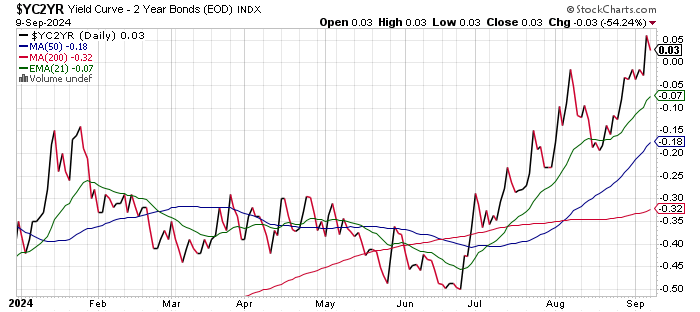

The spread between the yields of the U.S. Ten-Year and Two-Year Notes did narrow, but also did hold onto that newly created state of normalization through the Monday trading session....

The Ten-Year Note / Three-Month T-Bill spread, which is significantly more important, still shows no sign of giving a darn.

Interestingly

On Monday, the Census Bureau revised July Wholesale Inventories from growth of 0.3% down to growth of 0.2%. In response to that report, as well as having taken another look at last week's ISM surveys and labor market surveys, the Atlanta Fed tweaked higher its inputs for personal consumption expenditures and gross private domestic investment. This took that district's GDPNow model for the third quarter back up to growth of 2.5% (quarter-over-quarter, seasonally adjusted annual rate) from 2.1%. The model will not likely be revised again until next Tuesday after August retail sale and industrial production reports hit the tape.

SoFi's Noto Speaks

On Monday, with the Fed in its eight-times a year hibernation period, SoFi Technologies SOFI CEO Anthony Noto appeared at the Goldman Sachs Communacopia & Technology Conference, and sort of urged the Fed to get aggressive next week. Noto said: "You're much better off cutting 50 basis points now because you'll spur more economic activity next year because corporations are making decisions about next year now. If they know they have 50 basis points on a huge balance sheet of debt, they could do more hiring, they could do more investing, even having that information."

Fed funds futures trading in Chicago are currently pricing in a 73% probability for a quarter-point rate cut next week and a 27% likelihood for a half-percentage point rate cut. By year's end, these markets are pricing in an 87% probability for at least 100-basis points worth of rate cuts with a 46% chance for more than that.

Apple's Launch Event

By all accounts, the event itself was rather boring and the launch of Apple Intelligence inside of the new iPhones was a little vague. What caught my attention was the possible new use for Apple AirPods as hearing aids. As someone who lost most of his ability to hear in the military, I think this might be a welcome advance. I had hearing aids before, but I hated them. I chose to just be semi-deaf. Being that I wear these headphones often enough just so I can make out what is being said half of the time when on the phone or listening to news and podcasts, this is something I would be willing to try.

Anyone Else Notice...

... That China remains in a deflationary/disinflationary environment. On Monday, China's National Bureau of Statistics posted an August consumer price index that was up 0.6% year-over-year, which was below expectations for 0.7% and an August producer price index that was down 1.8% year over year, vs. expectations for -1.5%. China has now posted a negative year-over-year PPI for 23 consecutive months. Chinese GDP growth has been trending lower for about a year as well.

Our good friend Keith McCullough and his crew at Hedgeye Risk Management (my macro go-to, as they are that good) currently estimate third-quarter Chinese gross domestic product at y/y growth of 3.81%, down from 4.7% for Q2 and 5.3% for Q1. Put bluntly, the Chinese economy will not be the engine driving global economic growth anytime soon. That said, the Indian economy just might be.

Trading Notes

Palantir Technologies PLTR, on news for the upcoming addition to the S&P 500 and the five-year strategic collaboration with BP PLC BP popped for a gain of 14.08% on Monday, closing at $34.60, after peaking at $34.70. I have been asked by readers if I have taken any profits. The answer is no, I have not. As stated in yesterday's piece, my target price remains unchanged, at $36.

Should we get a $36 tick ahead of the Sept. 20 add, I will likely sell some token amount and head higher with my balance. This stock is too valuable in my opinion going forward to take off any amount that diminishes its weighting upon my book. After Monday, Palantir is now my fifth heaviest-weighted long position. This is the stock's first appearance in my top five.

Economics (All Times Eastern)

07:00 a.m. - NFIB Small Biz Optimism Index (Dec): Expecting 93.6, Last 93.7.

08:55 - Redbook (Weekly): Last 6.3% y/y.

4:30 p.m. - API Oil Inventories (Weekly): Last -7.4M.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

After the Close: PLAY (.86), GME (-.09)

At the time of publication, Guilfoyle was long SOFI, PLTR equity.