Tracking Buffett and Druckenmiller Trades, CPI Oddities, Hot Financials, Cisco

It's 13F day, so let's review the latest filings from two of the greatest investors/traders. Plus, checking out a key line on the S&P 500 chart, rate-cut expectations fade and more!

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We really don't pay all that much attention to the news that floods across our screens on 13F Day every quarter, but in a way, we do. We know the information is dated, coming 45 days after the quarter being reported ends. We know that short positions and cash positions are not included. What if a long position listed on a 13F is merely a hedge against a larger short position in a somehow adjacent security? We'll never know.

Many of the 13Fs released, come from very accomplished funds run or managed by very accomplished managers. I look at many of them. I don't really take away any feelings of conviction or concern about my own book based on the positions taken by these accomplished individuals in names that I do or do not trade — except maybe for two.

I won't change my book necessarily based on what these two have done, but I will read through what they have done a little more thoroughly than the rest and try to put their head in mine, or rather mine in theirs...knowing that the information is both dated and incomplete.

In my opinion, and it's just an opinion, the two greatest investors/traders of my long career on Wall Street have been Warren Buffett and Stanley Druckenmiller. I revere Buffett so, to the point that I have been and remain an investor myself in Berkshire Hathaway, the "B" stock BRK.B. I choose the B over the "A" stock BRK.A as the Southern Oak in my backyard does not grow gold bars on its branches. Druckenmiller became a star manager for Quantum Fund (George Soros) and Duquesne Capital, which he shut down in 2010. He has since managed the Duquesne Family Office.

We already knew that Buffett had cut his long position in Apple AAPL in half. It appears that Druckenmiller has also reduced his long position in Apple, along with reducing his long side exposure to Nvidia NVDA, and Microsoft MSFT, while completely exiting Meta Platforms META. His sizable bet on small caps in a broad way, is missing, as perhaps he feels that trade has come and gone.

Buffett exited long positions in Paramount Global PARA, and Snowflake SNOW, while reducing long-side exposure to Chevron CVX and Louisiana-Pacific LPX. Notably, Buffett increased long-side exposure to Occidental Petroleum. OXY.

Conviction or Not?

Like Druckenmiller, I had reduced Nvidia, not during the quarter, but upon its completing the second peak of its summertime double top. I added some back on during last Monday's market meltdown. No idea if Druckenmiller did the same as these forms are not close to real-time documents.

Buffett reduced Chevron during the quarter. I got completely out of that name during the quarter. Buffett is investing very heavily in OXY, my Energy sector eggs have been almost solely in Exxon Mobil's XOM basket for months now.

Microsoft remains my most heavily weighted long position though I did reduce small once the stock lost the 50-day simple moving average (SMA) back in July and added that tranche back on as the stock tested its 200-day SMA in early August.

Consumer Prices Print on Consensus

On Wednesday morning, the Bureau of Labor Statistics posted their July data for consumer prices. For that month, headline CPI printed at growth of 0.2%, up from June's -0.1% contraction. At the core, CPI crossed the tape also at growth of 0.2%, accelerating from June's 0.1%. These numbers, though up from June, were projected.

On a year-over-year basis, headline CPI slowed from growth of 3.0% to 2.9%, while Core CPI printed at 3.2%, down from 3.3%. Again, both of these numbers landed precisely on consensus. What was hot in July? Fuel oil, shelter, and transportation services. What was cool? Utility gas, new and used vehicles, as well as medical care services and commodities.

What was odd in the report? Health insurance prices were down 0.4% month over month and down 0.6% year over year. This, I don't think is even remotely believable. I don't think my insurer is even thinking of playing this tune. Prices for men's suits are down 12% year over year. Blame "work from home" or blame the fact that a lot less men are working full time.

Apples were down 1.2% m/m and down 14.5% year over year. I wrote about this yesterday. I eat more apples than anyone I know. Really. I live out on Long Island and in central Florida. Apples are definitely up in price noticeably month over month and year over year in both of those locales.

Smooth Sailing?

One might have thought. Though July producer prices hit the tape on the cool side and July consumer prices printed in line with expectations, markets seemed less pleased than what some expected. There was a significant rally on Tuesday in response to that PPI print. so maybe just meeting expectations for CPI on Wednesday, was in a mild way, disappointing.

This morning, expectations for a 50-basis point rate cut on September 18 have faded a bit. Fed Funds futures trading in Chicago are now pricing in just a 38% likelihood for a cut of 50-basis points to be made to the target for the Fed Funds Rate at that time. This is down from a majority probability. There is now a 62% likelihood for a 25-basis point rate cut that day.

The extra 25-basis points have been pushed out by these markets to November 7. Futures now show a 58% chance for 75-basis points worth of rate cuts by that date and a 75% probability for 100-basis points worth of rate cuts by December 18.

Melba Toast Wednesday

Bland. Traders seemed frozen in time on Wednesday, for the most part, remaining inactive.

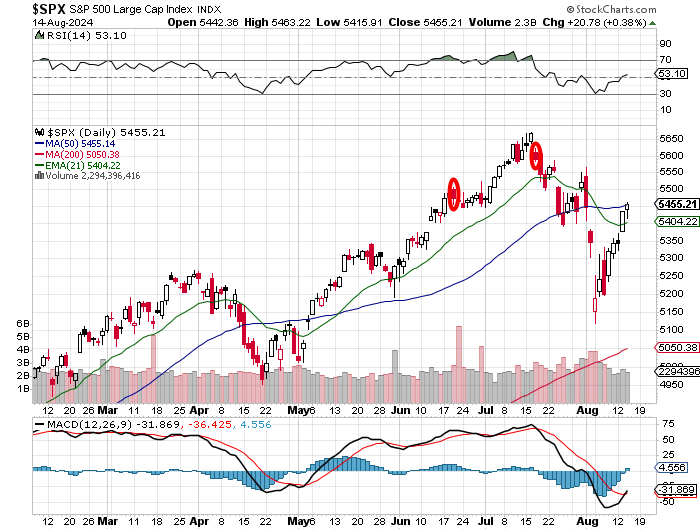

The S&P 500 traded up 0.38% to the 5455 level, which just happens to be for that index, the 50-day simple moving average (SMA).

Look at this:

I wouldn't really call that a rejection. The index just kind of coasted to the level and decided to put that fight off, at least for a day. On the bright side, look at the daily Moving Average Convergence Divergence (MACD) below the chart. This is bullish. The 12-day exponential moving average (EMA) line (black) has crossed above the line representing the 26-day EMA (red), while the histogram of the 9-day EMA (blue filed) has snuck above the "zero bound" for the first time since mid-July.

Away from the S&P 500, the Nasdaq Composite gained just 0.03% on some awful breadth. The Nasdaq Composite is not close to taking on its 50-day line but could have a date with its 21-day EMA. That could at least engage the swing crowd.

The Financials were hot, with the KBW Bank Index up 0.9%, but the small-caps were cool. The Russell 2000 gave up 0.52%.

Breadth

Eight of the 11 S&P sector-select ETFs ended Wednesday in the green. That's somewhat misleading though. Two sector funds closed so close to unchanged we should really consider them flat for the day. So outside of those two flats that closed "unch" on Wednesday, seven of these SPDRs closed higher, easily led by those Financials XLF, while two SPDRs closed lower, led by Communication Services XLC.

It was a tale of two exchanges. Winners beat losers at the NYSE by roughly 4 to 3 margin while losers beat winners by about 4 to 3 at the Nasdaq. Advancing volume took a 56.3% share of composite NYSE-listed trade, but just a 45.6% share of the composite action for Nasdaq listings.

Making everything even less meaningful, aggregate trading volumes cooled from Tuesday's increased levels. Activity was down 7.3% for NYSE listings, down 8.8% for Nasdaq listings and down 7.4% across the membership of the S&P 500. Does that mean that traders got fired up at the PPI, shrugged their collective shoulders at the CPI and eagerly await this morning's data for July Retail Sales? Quite possibly, or even probably.

The Band Played On

Is Cisco Systems CSCO trading higher overnight because the firm beat Wall Street's fiscal fourth-quarter expectations for both top and bottom-line performance? Is the stock trading higher because fiscal Q1 and fiscal 2025 guidance didn't really stink?

Or is Cisco up 6% several hours ahead of Thursday's opening bell because the firm announced plans to reduce its payroll by 6,300 employees or 7% of its global headcount? Investors do love to hear about payroll reduction.

Remember the Great Financial Crisis? Hey, why is XYZ up a whole bunch of percentage points? Oh, they're laying off entire departments. Gotcha. Let's hope that as far as large-scale job reductions go, this is not the tip of the iceberg.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 232K, Last 233K.

08:30 - Continuing Claims (Weekly): Last 1.875M.

08:30 - Retail Sales (July): Expecting 0.3% m/m, Last 0.0% m/m.

08:30 - Core Retail Sales (July): Expecting 0.1% m/m, Last 0.4% m/m.

08:30 - Empire State Manufacturing Index (Aug): Expecting -6.0, Last -6.6.

08:30 - Philadelphia Fed Manufacturing Index (Aug): Expecting 6.5, Last 13.9.

09:15 - Industrial Production (February): Expecting 0.0% m/m, Last 0.6% m/m.

09:15 - Capacity Utilization (February): Expecting 78.6%, Last 78.8%.

10:00 - Business Inventories (June): Expecting 0.3% m/m, Last 0.5% m/m.

10:00 - NAHB Housing Market Index (Aug): Expecting 43, Last 42.

10:30 - Natural Gas Inventories (Weekly): Last +21B cf.

16:00 - Net Long-Term TIC Flows (June): Last $-54.6B.

The Fed (All Times Eastern)

09:10 - Speaker: St. Louis Fed Pres. Alberto Musalem.

13:10 - Speaker: Philadelphia Fed Pres. Patrick Harker.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: DE (5.85), NICE (2.54), TPR (0.88), WMT (0.65),

After the Close: AMAT (2.02)

At the time of publication, Guilfoyle was long WMT, BRK.B, NVDA and MSFT equity.