The Witches' Brew, Santa and Palantir Too

Are the markets set up for a Santa Claus rally? Here's how things are shaping up after last week. Plus, the 'GDP game,' and how I'm trading Palantir after its addition to the Nasdaq 100.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It's the holiday season (the holiday season)

So hoop-dee-doo and dickory dock

And don't forget to hang up your sock

"Cause just exactly at twelve o'clock

He'll be coming down the chimney

Coming down the chimney

Coming down the chimney, down

Happy Holiday

(Happy Holiday) Happy Holiday

While the merry bells keep ringing

Happy holiday to you

- "The Holiday Season" Irving Berlin (Andy Williams), 1963

Who's Ready for a Holiday?

Well, whether you or I are ready or not, here we are. On Mondays I usually label this section "The Week Ahead" and place it near the end of this column. Not today. Honestly, there's not a lot to speak of or write about for the week ahead, so instead I ask who's ready? Everyone asks for gift cards around us this year. Young people just want the dough. Fine by me. Easy peasy.

As for how the dough is kneaded... weeks bearing holidays are always tough on those who support themselves and their families through either their ability to trade a P/L or through commission. No, I don't think too many of us traders can complain this year. This has been another good year. By good, I mean that opportunities were plenty, were identifiable and most of us probably aren't trying to save the entire year right up to the wire.

That said, this is still a two-week period where there are only eight days of trade, really seven and a half spread over a time frame that usually provides 10 full trading sessions. Hence, the pressure on those who run revenue and pay bills on a monthly basis who might be behind for December, will feel some pressure.

In a week where markets are open only 80% of the days, the level (because every trader knows his or her level in terms of revenue that must be averaged on a daily basis to pay those bills) for those performing with no safety net (base salary) moves up a gnarly 25%. Sometimes all it takes is one good trade. Sometimes, it takes all week. Let that game begin.

As far as the week ahead, even those parasitic algorithms that feed off of momentum and news flows will have to be patient. The macroeconomic calendar is light. We do get November Durable Goods Orders on Tuesday, but not much else. There are no Fed speakers on the docket. Pretty sure that crew is not chock full of hard-charging, fire-eating go-getters. Doubt there's much work being done this time of year.

There aren't even any significant quarterly earnings due to be reported this week. Not one. Of course, Tuesday is Christmas Eve. Stock markets will close at 13:00 ET tomorrow, bond markets will close an hour later. Wednesday is Christmas Day and a federal holiday. All financial markets are closed. The eight-day festival of Chanukah kicks off on Wednesday night. The seven-day observation of Kwanzaa will start on Thursday.

Last Week

Markets got ugly last week, that is until Friday anyway. This leads us to a question that I'll have to ask a little further down. A lot of news hit the tape last week and most of what happened put upward pressure on the U.S. dollar, upward pressure on Treasury yields, and downward pressure on risk assets.

First November Retail Sales were better than expected, at least at the headline level. Core Retail Sales were rather weak, but the market paid that no mind.

On Wednesday, the FOMC cut their target range for the Fed Funds Rate by 25 basis points to 4.25%-4.5%. The cut was expected, but what roiled markets was the FOMC's outlook for 2025, which showed increased economic growth, and higher inflation than the Fed had previously projected. This of course, forced the FOMC to take higher their median idea for where the Fed Funds Rate might be in 12 months by 50 basis points.

Bitcoin was the star of the week, trading near $107,000 per token at one point, prior to going out on Friday below $95,000 per token. Gold, while not running with Bitcoin into those December highs, has held up well on dollar strength and in the face of a more normalized yield curve.

Then came Friday and cooler-than-expected numbers for November PCE Prices. PCE data rarely surprises and these cool-to-the touch inflation numbers had a positive impact on stocks on what was also a "triple-witching expirations event.

Keyword reading algorithms loved it when Chicago Fed President Austan Goolsbee said that he sees lower rates ahead if the economy can do over the next 18 months or so what it has done over the past 18 months or so. Obviously, that's, for the most part, economic drivel meant for consumption by simpletons, but Wall Street needed a rally and bought what Goolsbee was selling. Check this out...

Marketplace

Among the major to mid-major U.S. equity indexes last week....

- The S&P 500 gained 1.09% on Friday but still closed the week down 1.99%.

- The Nasdaq Composite gained 1.03% on Friday but still closed the week down 1.78%.

- The Nasdaq 100 gained 0.85% on Friday, still closing the week down 2.25%.

- The Russell 2000 gained 0.94% on Friday, still closing the week down 4.45%.

- The S&P SmallCap 600 gained 0.6% on Friday but still closed the week down 4.82%.

- The S&P MidCap 400 gained 0.6% on Friday, still closing the week down 4.67%.

- The Dow Transports gained 0.21% on Friday but closed the week down 4.9%.

- The Philly Semiconductors gained 1.46% on Friday, still closing the week down

3.59%.

- The KBW Bank Index gained 2.01% on Friday, only to close the week down 3.45%.

On Friday, all 11 S&P sector SPDR ETFs closed in the green, with the REITs XLRE leading seven of these funds that gained at least 1% for the session. Consumer Discretionaries XLY closed out the day in last place, but still up 0.25%.

For the week, all 11 S&P sector SPDR ETFs closed in the red, led by Energy XLE at a very ugly -5.69%. The funds gave up at least 4%, while nine of these funds gave up at least 2% for the week. It was so rough out there, that Technology XLK was the top-performing fund among the 11 at -1.29%.

The Witches' Brew and Santa Too

Markets amid their extremely high-volume, triple-witching run to glory on Friday, may have set up a Santa Claus rally. I'm serious. That said, I am not sure.

Winners beat losers decisively at both the NYSE and the Nasdaq on Friday, as advancing volume took a commanding share of the action as aggregate trade soared. Is that meaningful? Dead-cat bounce? It is difficult to refer to the elevated level of trade as having real conviction behind it given that so much of it was tied to expirations. Still, the tape was green, and the volume was red.

We told you last week when the Day One of the downward change in trend was confirmed. It may have been quick, but markets did trade lower. No, I am not sure that the selloff is over. As a matter of fact, I am not all that bullish on early 2025, but I do listen to the market more than I listen to my spider sense, which is probably a good thing. Friday may have been a Day One of an upward change in trend, still in need of confirmation, ahead of the traditional Santa Claus rally.

Take a look at this:

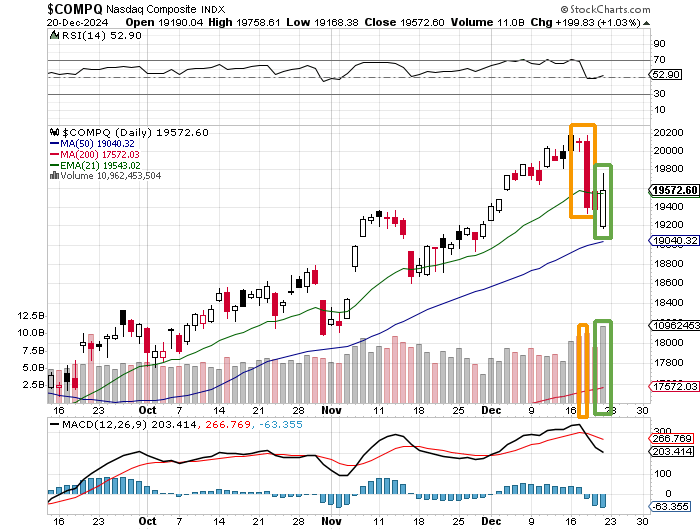

For the Nasdaq Composite, above, the daily MACD (moving average convergence/divergence) is still ugly, but the index did find help above its 50-day SMA (simple moving average) and retake its 21-day EMA (exponential moving average) on Friday.

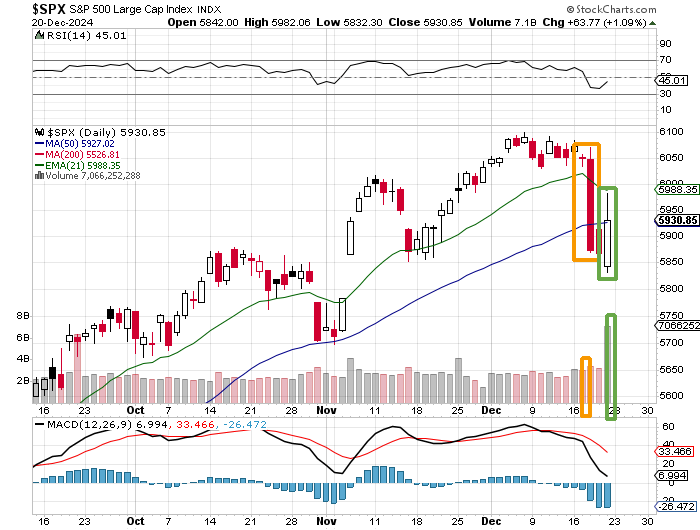

In the chart above, readers will see that the S&P 500 is also not set up well by its own daily MACD, but did manage to retake its 50-day SMA after losing it. That's potentially huge. Now, I don't make promises, but I will tell you this. The traditional Santa Claus rally period encompasses the final five trading days of the outgoing year and the first two trading days of the upcoming year. That's December 24 through January 3 for those of you without a calendar.

Just off the top of my head, for the S&P 500, the period runs positive a little better than 75% of the time, and that gain over several decades has averaged about 1.5%. I'll take 1.5% over seven trading days every time if I can. How about you?

The GDP Game

This past Thursday, the BEA revised their estimate for third-quarter GDP to growth of 3.1% (q/q, SAAR), from 2.8%. What's interesting, but no one in the financial media even brought up, is that while GDP was revised higher, Q3 GDI, which measures the same economic activity and in theory should equal GDP, was revised down to growth of 2.1% from 2.2%.

How one measure of national economic growth is revised higher while the other was revised lower is beyond me. The average of the two is 2.6%, which is what an honest economist would say Q3 growth amounted to. As I have told readers many times, when the two numbers are not in concert with one another, they are to be averaged. That's the Fed's own instructions.

Last week, the Atlanta Fed revised their GDPNow model for the fourth quarter down to growth of 3.1 (q/q, SAAR) from 3.3%. Among other central banks running close to real-time GDP models for the current quarter, the New York Fed raised its estimate for Q4 growth to 1.9% from 1.85%, while the Cleveland Fed still nudged its view for Q4 growth up to 1.85% from 1.84%. The St. Louis Fed revised their model for Q4 GDP growth up to 1.48% from growth of 1.33%.

The Atlanta Fed is still the upside outlier right now, but the highest and lowest estimates among the four are starting to work their way towards each other. Atlanta will revise their model just once this week, on Tuesday. The other three models are revised once a week, on weekends.

Palantir News and Trading

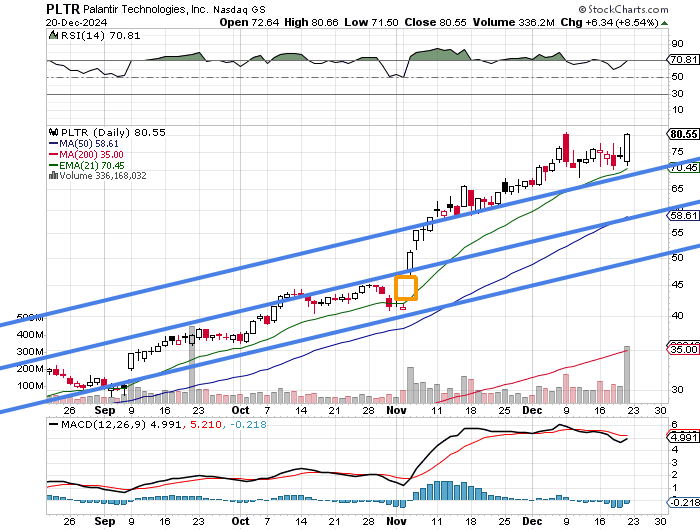

Ahead of being added to the Nasdaq 100 over the weekend, last Wednesday, Palantir Technologies PLTR announced the extension of a long-standing partnership with the U.S. Army to deliver the Army Vantage capability in support of the Army Data Platform. The total value of the agreement was for $400 million over four years with a ceiling of almost $619 million.

Over the weekend, the Financial Times reported that Palantir and Anduril Industries, a defense contractor largely dealing in robotics and AI technology for unmanned drones, as well as autonomous surveillance, are in talks with possibly a dozen rivals to potentially create a consortium that would jointly bid for federal contracts in what would be a challenge to the large legacy defense contractors such as Lockheed Martin LMT, RTX Corp. RTX, and Boeing BA.

Don't get me wrong. In terms of weighting, Palantir is still a top-five holding for me. In fact, it's number two on my pad. Readers should just be fully cognizant that coming off of the addition to the Nasdaq 100, and peaking on Friday afternoon for that reason, the stock is at the moment, at risk for a double-top reversal.

That does not mean that this has to happen. It does mean that with the stock up further overnight, that if I were not long the shares, this would not be a day that I would consider initiating a new long position in this name. I would let the dust settle if I were considering something like that.

Economics (All Times Eastern)

10:00 - CB Consumer Confidence (Dec): Expecting 113, Last 111.7.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle was long PLTR, LMT and RTX equity.