The Market's Delicate 'Balance of Risks'

Before really finishing the job on inflation, the Fed swerves toward the economy, big earnings like Nvidia await and many questions linger.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

"The time has come for policy to adjust."

- Fed Chair Jerome Powell (August 23rd, 2024)

Can we expect higher for longer? No, I'm not talking about rates. I'm talking about equities.

The answer: Possibly.

Friday has come and gone. The speech we had waited all summer for was rather short, and really not specific. What Chair Powell did, though, was provide clarity on one main item -- the one item that had already for the most part been assumed and I had thought priced into markets. The trajectory of forward-looking monetary policy has indeed, at last changed. Though there still has not been a change made to the target range for the Fed Funds Rate, and still will not be, until Sept. 18, Powell left no doubt.

That trajectory just mentioned, has changed. There will not be a next rate hike to tamp down on consumer-level inflation, despite that inflation remains well above the Fed's stated 2% target. There will not be a furthering of the "higher for longer" period of elevated short-term rates. The Federal Open Market Committee has not changed that target since a quarter-point increase on June 26, 2023, about 14 months ago. Powell told us where his current concern is.

The Fed chair stated that the slowdown in U.S. labor markets was "unmistakable," and that, "We do not seek or welcome further cooling in labor market conditions." On this slowing in demand for labor, Powell commented, "The current level of our policy rate gives us ample room to respond to any risks we may face, including the risk of unwelcome further weakening in labor market conditions."

On short-term rates, the Chair was direct. But on where Powell sees a terminal rate, or how much easier policy will need to get, he does not and cannot know. ..."

The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook and the balance of risks."

What Now?

It's that "balance of risks" comment that really sticks, when I ponder what the Fed will now try to accomplish. We know that the Federal Reserve Bank operates at least officially, with a dual mandate. The central bank seeks to pursue full employment while facilitating price stability. It feels suddenly, as if the committee and its leader have moved quite definitively away from their group focus on containing consumer- level inflation, as employment appeared to be taking care of itself.

Now that demand for labor has weakened, and we know with certainty that the nation's employment situation was never that close to being as strong as it was presented to the public, the Fed is quite obviously preparing to fend off a prolonged economic slowdown or outright recession. In short, the balance of risk has shifted for our central bankers to where labor market health is, at the moment, the greater threat to the U.S. economy than is consumer level inflation. To nip eroding demand for labor in the bud, the Fed must abandon its war on inflation before that battle has been fully won. Remember, for most middle- to below-middle-income American households, it's not the 3% inflation in 2024 that's wrecking their standards of living, it's the 20%-plus aggregate inflation over three-plus years.

... About Prices ...

Before ending his address on Friday, Powell added: "Our objective has been to restore price stability while maintaining a strong labor market, avoiding the sharp increase in unemployment that characterized earlier disinflationary episodes when inflation expectations were less well anchored. While the task is not complete, we have made a good deal of progress toward that outcome."

Quote of the ... Decade?

Central banks have worked out, although they try to keep it a secret, that the natural state of the economy is to generate deflation. This is better known as productivity growth. As companies become more efficient and workers more productive, they produce the same amount of goods for less effort (or more goods for the same effort). In other words, the natural tendency of the economy is for the production cost of goods to fall.

That should be good news for everyone and result in a falling tendency in consumer prices which, when combined with stable wages, should result in an increase in real wages and worker purchasing power (it also leads to an increase in overall demand for goods and services). So why try to counteract this beneficial, natural tendency?

Simple: it makes it more difficult to pay back debt. More accurately, it makes it more difficult for governments to pay back their debt (individuals and companies find it easier to pay back debt when their real incomes are rising). The generation of inflation by central banks is an effort to provide governments (their bosses) with an easy way out of their debt problems: through inflation rather than fiscal prudence.

- Dr. Jim Walker, Chief Economist at Aletheia Capital (March 2019)

The GDP Game

There was not a whole heck of a lot of macroeconomic data released last week. The Atlanta Fed's GDPNow model for the third quarter, which will be revised later this morning after the Census Bureau releases its July numbers for Durable Goods Orders, still stands at growth of 2.0%, quarter over quarter, seasonally adjusted annual rate.

Among other central banks running close to real-time gross domestic product models for the current quarter, the New York Fed has the third-quarter humming along at 1.94%, the Cleveland Fed shows growth of 1.6%, and the St. Louis Fed shows growth of 1.65%. The St. Louis Fed was the most accurate among the four for the first quarter, while Atlanta was the most accurate for the second quarter.

Marketplace

What did you expect? It was a light week for macro, a light week for earnings and outside of the clambake in Jackson Hole that was dominated by Powell, a light week for the Fed, at least publicly. Powell, like it or not, was the axe, last week.

- The S&P 500 gained 1.15% on Friday to close the week up 1.45%.

- The Nasdaq Composite gained 1.47% on Friday to close the week up 1.4%.

- The Nasdaq 100 gained 1.18% on Friday to close the week up 1.09%.

- The Russell 2000 gained 3.19% on Friday to close the week up 3.58%.

- The S&P Small Cap 600 gained 3% on Friday to close the week up 3.04%.

- The S&P Mid Cap 400 gained 2.18% on Friday to close the week up 2.82%.

- The Dow Transports gained 1.61% on Friday to close the week up 1.9%.

- The Philly Semiconductor Index gained 2.79% on Friday to close the week up 1.13%.

- The KBW Bank Index gained 3.37% on Friday to close the week up 2.7%.

All 11 S&P sector-select SPDR exchange-traded funds closed out Friday in the green, with the real estate investment trust XLRE) out in front. Breadth was overwhelmingly positive for the day with winners beating losers by an 8-to-1 count at the New York Stock Exchange and by about 7-to-2 at the Nasdaq. Advancing volume took an almost incredible 91.1% share of Friday's composite NYSE-listed trade and a 78.9% share of composite Nasdaq-listed trade.

Aggregate trading volume increased on a day-over-day basis for names listed at both exchanges as well as across the S&P 500. But this aggregate trade activity still failed to reach those respective trading volume 50-day simple moving averages. That makes the rally meaningful, but perhaps less so than it could have been.

For the week, 10 of the 11 S&P sector SPDRs closed in the green, still led by the REITs, which were up 3.61%. Both Discretionaries XLY and Materials XLB gained more than 2% a piece as the U.S. dollar stumbled and Treasury yields fell. Among the 11 funds, only Energy XLE closed in the red for the week and just barely.

Up and to the Right

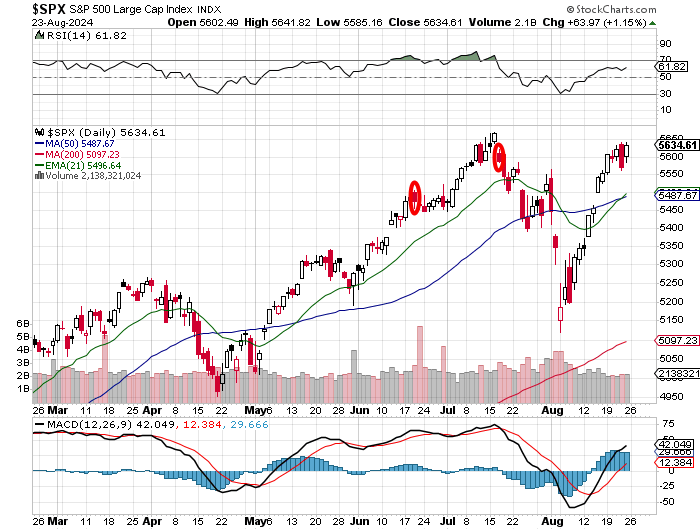

Readers will see that the S&P 500 last week solidified gains made the week prior and has not yet come close to retesting its 50-day simple moving average from above. Instead, the 21-day exponential moving average crossed bullishly above that 50-day line creating a mini or swing traders' golden cross. Relative strength had improved nicely and has held those gains as the daily moving average convergence divergence indicator went from being cheap horror movie material to looking more bullish to now looking very bullish in just three weeks' time.

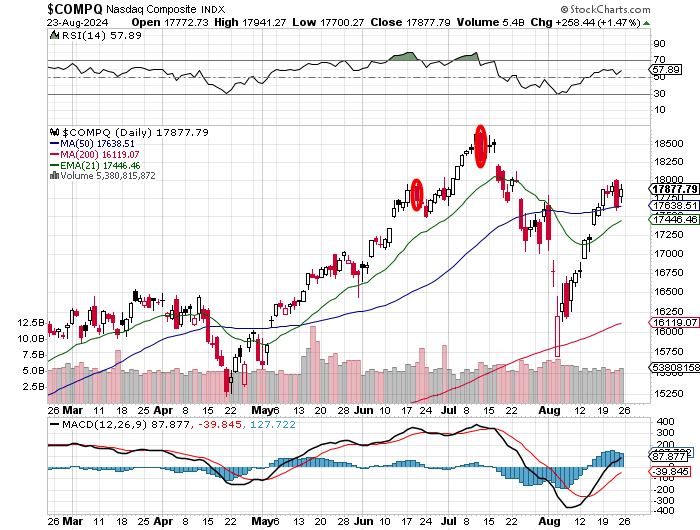

The Nasdaq Composite not only retook its own 50-day simple moving average, but survived a midweek test of the level from above, which might just be more impressive than what the S&P 500 has done.

Here, too, both the Relative Strength Index and daily MACD are looking stronger. That said, I'd really like to see the 26-day EMA within that daily MACD rise above the zero-bound before declaring any victories.

The Week Ahead

Honestly, only one item and one item alone will matter most this week. The macroeconomic calendar heats back up. Besides July Durable Goods Orders on Monday, and July PCE data due this Friday, the BEA will update its original estimate for second-quarter GDP on Thursday. None of that matters all that much, though. With a couple of exceptions, the Fed will be somewhat quiet this week. Guess it must have some jet lag from last week. That brings us to earnings. Does it ever. The season, long as it is, nears an end, but the calendar has some heavyweights headed our way this week. In fact, it has the heavyweight headed our way. Traders and investors will hold their collective breath this Wednesday evening. Sure, we'll hear from Chewy CHWY and Foot Locker FL on Wednesday morning. Sure, we'll hear from Best Buy BBY, Lululemon Athletica LULU, Marvell Technology MRVL and Ulta Beauty ULTA on Thursday. On Wednesday evening, however, CrowdStrike CRWD, and Salesforce CRM will report alongside the one name that will stop everyone in their tracks: Nvidia NVDA. How is demand for the company's most elite chips? Are we in the seventh inning of the surge for these chips or are we still pulling up our stirrups and tying out cleats with nine full innings still ahead? How is the delay in the Blackwell architecture progressing?

Economics (All Times Eastern)

8:30 a.m. - Durable Goods Orders (July): Expecting 4.0% m/m, Last -6.6% m/m.

8:30 - ex-Transportation (July): Expecting 0.0% m/m, Last 0.5% m/m.

8:30 - ex-Defense (July): Expecting 2.2% m/m, Last -7.0% m/m.

8:30 - Core Capital Goods Orders (July): Expecting 0.7% m/m, Last 1.0% m/m.

10:30 - Dallas Fed Manufacturing Index (Aug): Expecting -14, Last -17.5.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

After the Close: HEI (0.92)

At the time of publication, Guilfoyle was long CRWD, NVDA equity.