The Crazy Irony for Costco Shareholders

Costco is one of the most widely held and recommended stocks. However, here's why smart investors should be ringing the register or avoiding new commitments.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

People love Costco Wholesale COST for its bargain prices if you are willing to buy huge quantities all at once.

Investors love COST shares right now for the opposite reason. They are enamored of the stock price momentum, which rocketed the shares to an all-time intraday high of $850.30 last week.

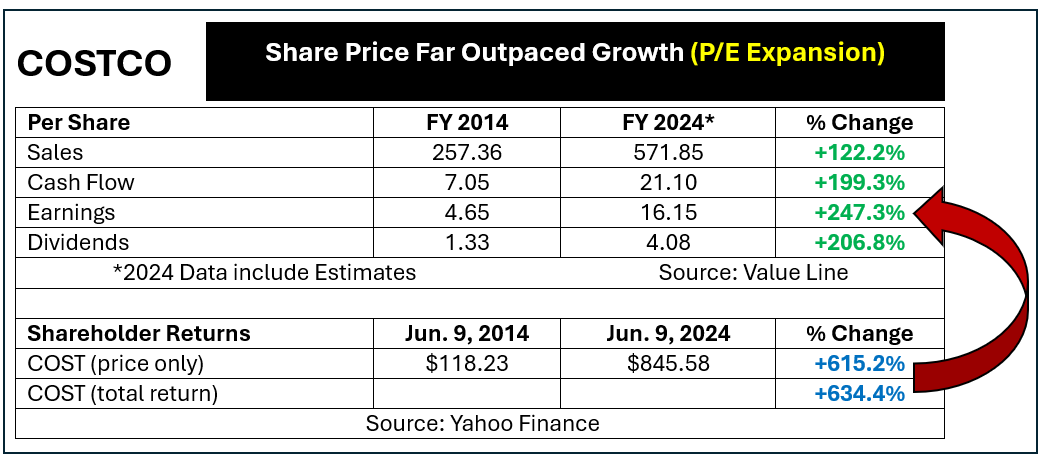

Here is graphic evidence of the crazy run Costco has just completed.

Over the last decade per-share sales grew by about 122%. Cash flow expanded by almost 200%. Both dividends and EPS more than tripled.

That is great news and a major corporate accomplishment. The stock’s rise, though, far outran the change in fundamentals. Total return surged by greater than 156% more than the increase in EPS due to P/E expansion to levels never seen before.

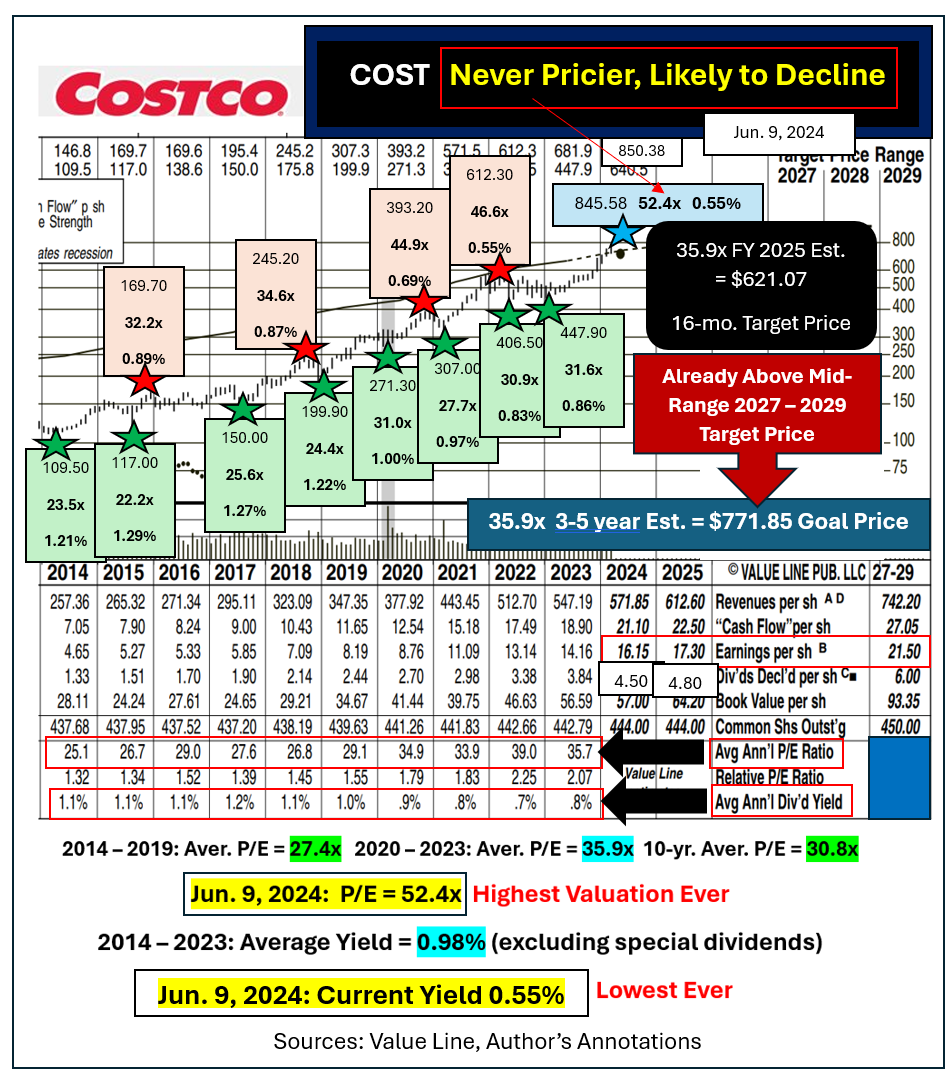

From a 2014 P/E of 23.5x and a 10-year median multiple of 30.8x, Costco weighed in on June 9, 2024 at 52.4x.

In retailing terms that is a huge “mark-up” in price, equivalent to 123% inflation over those 10-years.

Costco’s yield at 2014’s low was 1.21%. As of June 9, 2024 it was only 0.55%, even after a recent quarterly payout increase.

In short, COST has never been more expensively priced.

That said, Costco remains one of the most widely held and recommended stocks right now, defying all logic.

What Is COST Worth?

Take an optimistic view of what the stock’s multiple should be by assuming a return to its post-Covid average P/E of 35.9x. Apply that to the firm’s FY 2025 (ends Aug. 31, 2025) estimate and the 16-month target price becomes about $621. That implies around 26.5% of downside from its current quote even if next year’s earnings hit another new record.

Reverse engineering the current $4.64 annual dividend rate to a more normalized 0.97% suggests $464 as a rational target price by the fall of 2025.

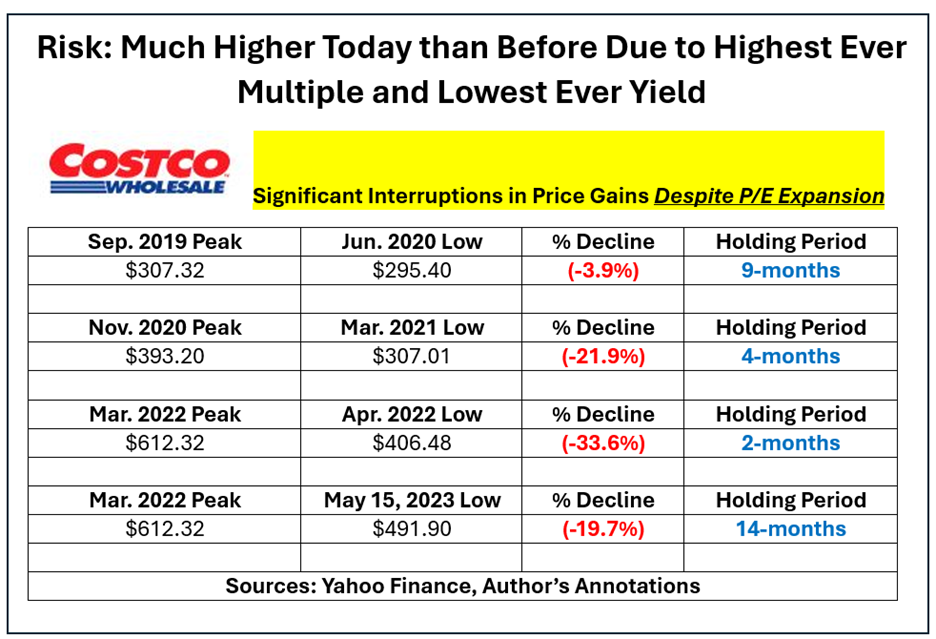

Even during COST’s euphoric period since 2019 there have been significant interruptions in share-price gains along the way.

From today’s crazy high valuation the risk of poor future stock price performance is much higher.

More Paul Price:

- Forget Meme Players… What Is GameStop Really Worth?

- Is Value Investing Dead? You Make the Call

- Buying Income Is Hazardous to Your Wealth

Those who own COST and fail to lock in profits are likely to see worse selloffs than those detailed above. Traders who are buying in for the first time are tempting fate, hoping to geta final, momentum-based run-ups before reality sets in.

I am not alone is seeing this.

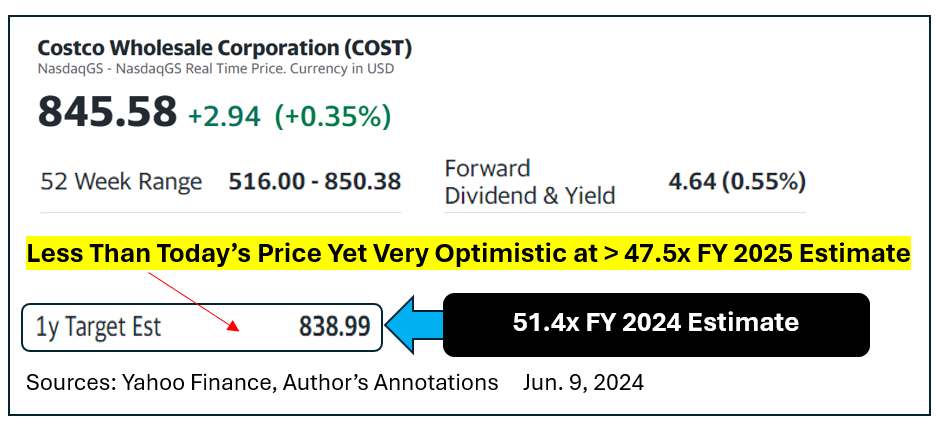

Yahoo Finance sees COST slightly lower than its current quote by this time next year. I am calling that forecast way too optimistic. It assumes Costco will still command a 51.4x multiple something that is statistically unlikely.

Even so, there is no discernible upside over the coming year.

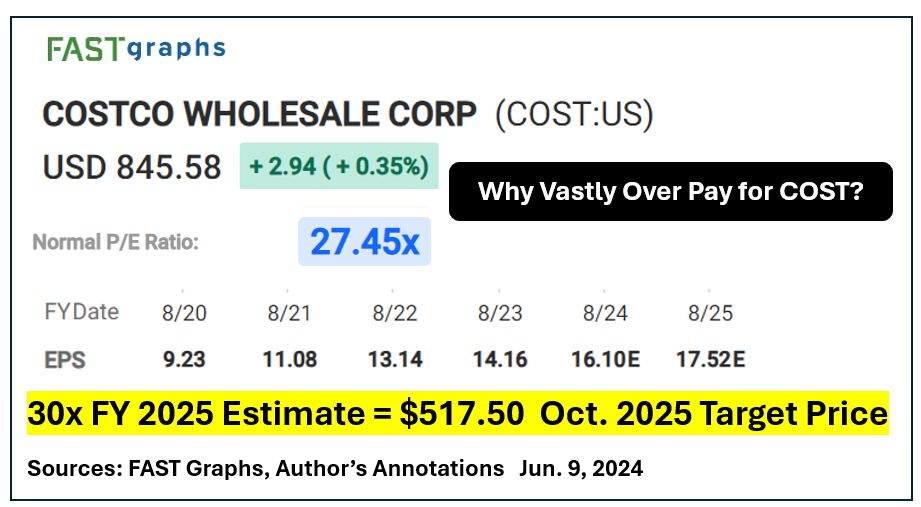

Research from FAST Graphs calls Costco’s normalized P/E as about 27.5x. That appears a bit conservative based on the past five years’ actual trading history. Assuming a 30 P/E on projected FY 2025 EPS estimates only generates a $517.50 goal price by October 2025.

That implies downside risk of about 39%.

Once again crunching the numbers suggests horrible intermediate-term performance while significant upside potential is totally lacking.

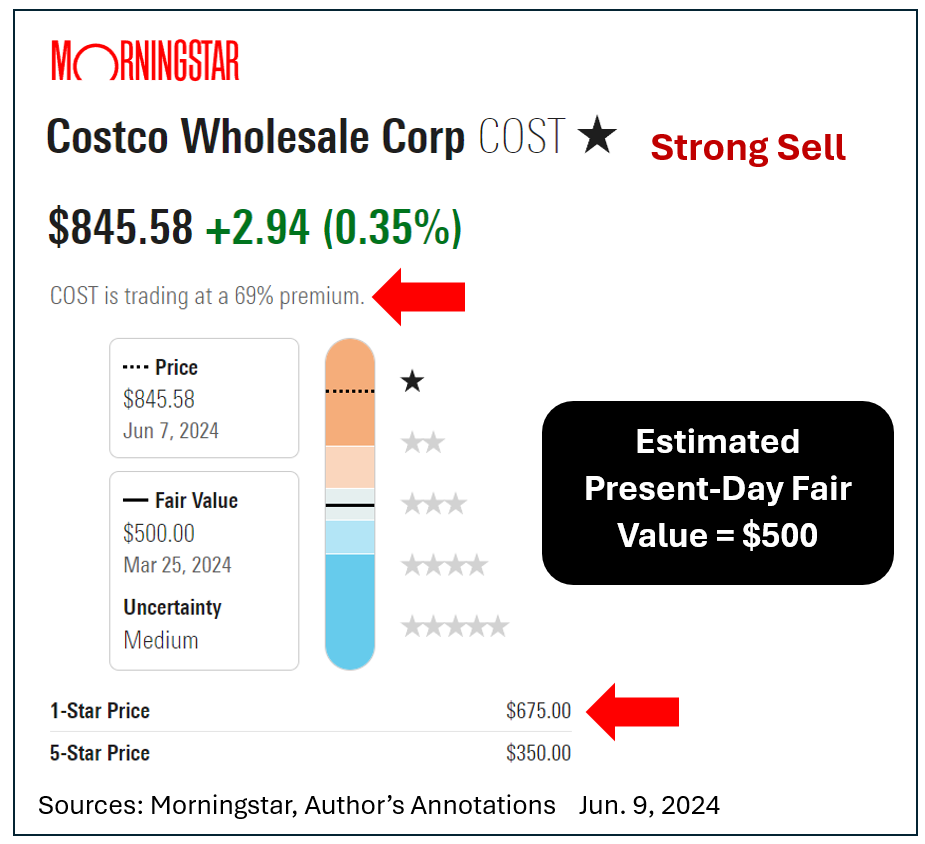

Independent research from Morningstar comes to a similar conclusion on COST. Morningstar assigns the shares its lowest 1-star (out of 5) "strong sell" rating. It calls present-day fair value for COST as just $500.

That implies the share fetch a more normalized 31x P/E. Costco’s 10-year average P/E (2014–2023) has been 30.8x.

Television talking heads continue to be falling all over themselves touting COST as it ran up to a new all-time peak.

Smart investors will be ringing the register or avoiding new commitments.

Don’t say you weren’t warned.

At the time of publication, Price had no positions in Costco shares or options.