The Calm Before the Fed Storm

Expect things stabilize a bit ... before 2 p.m. today. Also, a look at tariffs, Treasuries, the S&P and more.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

You thought that things might calm down a little? The fact is that things will, at least for several hours. Trading volumes tend to come close to a screeching halt on "Fed Days" until at least 2 p.m. ET. At that point, the official policy statement is released, and the activity starts to pick up. Only four times a year are the Federal Open Market Committee's economic projections released, along with that policy statement. Today is not one of those four, so the statement will be released in isolation. Keyword reading algorithms will read the document in microseconds and lead whatever knee-jerk reaction in price discovery that will become visible immediately.

A half hour later, the Fed Chair, currently Jerome Powell, whose term to serve on the Fed Board of Governors expires in 2026 in case you were going to ask, will take the podium as both human and algorithmic traders calm back down. Often, the action remains quiet until the Fed Chair says something that either fires up the risk taking or forces those seeking shelter to crawl back into their caves.

Will this week's electoral results impact monetary policy? The answer is "no," at least not today. For this afternoon, Fed Funds Futures markets trading in Chicago are still pricing in a 99% probability for a quarter-point cut made to the target range for that overnight rate. That would take the range down to 4.5% to 4.75%. Interestingly these markets are now also pricing in a higher terminal rate and reduced chances for aggressive cuts in the near-term future.

The likelihood, according to these markets, for another quarter-percentage point rate cut on Dec. 18 is down to 71%. A terminal rate range of 3.75% to 4% is now expected to be reached by June (54% probability), and at least the way futures traders see it, that's where it will stay for some time.

Rates in Real Time

Treasury debt securities may be trading lower, but Wednesday's auction of $25 billion worth of new 30 Year Long Bonds went quite well. The high yield awarded printed at 4.608%, stopping though the "when issued" at the time by 2.2 basis points. That was the largest "stop through" since late 2020. Bid to cover showed nice demand at 2.642, well above the recent norm of about 2.4 for this series.

After that, it gets a little messy. Foreign demand was not overly impressive with Indirect Bidders taking down 62.7% of the issuance. In October, foreign accounts took down an 80.5% slice of this pie. But domestic accounts showed unusual interest in grabbing some 30-year sovereign debt. Direct bidders took down a 27.1% allocation of this auction, up from a paltry 7.4% last month. This was the third largest take down by direct bidders for this series on record. This left dealers with just 10.2% of the sale, the smallest slice of the 30-Year pie dealers have been "stuck with" since the June 2023 auction.

For the session on Wednesday, the yield for the U.S. Thirty Year Bond ran up 18 basis points to 4.66%, while the yields for the U.S. Ten- and Two-Year Notes popped 15 basis points and 9 basis points respectively to go out at 4.44% and 4.29% in that order. U.S. Treasuries have found a bid overnight. As I work my way through the zero-dark hours, I see 30-Year, 10-Year and 2-Year U.S. sovereigns paying 4.62%, 4.43%, and 4.26% respectively.

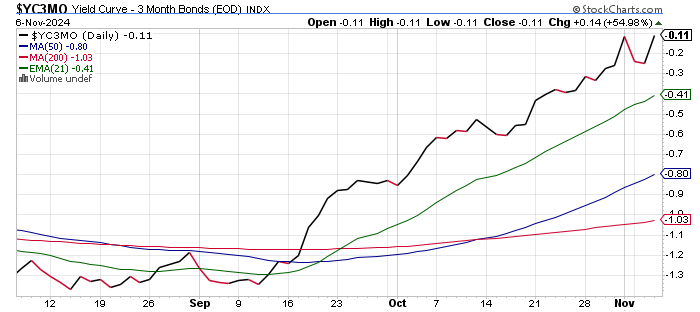

Check Out This Little Cutie

Just check out the spread between the yield between the U.S. Three Month Note and the U.S. Ten Year Note. Remember, this spread has been in the past, the most accurate predictor of economic contraction that we have at our disposal. This spread is finally nearing an "un-inversion" or normalization. We never came close to an outright contraction, some might say. In nominal terms, after some magical revisions that much is true.

In real terms, however, many industries have been in and out of a rolling recession, while the manufacturing sector has been mired in a deep state of recession for two years, without coming up for air. At the household level, real wages are negative over the past three years relative to inflation. Hence, the average American family unit has been in its own state of recession since 2021.

Keep In Mind

While many fret that reduced tax rates and increased tariffs will weaken an already porous federal budget, that will force increased Treasury security issuance. While increased issuance is a given at this time, regardless of electoral outcome, remember that tariffs are a weapon in negotiation. One cannot gain leverage unless his or her adversaries believe they will "go there" and they have to be willing to indeed "go there."

Globalism has in my opinion done as much as anything else to expand the ranks of the U.S. poor, while hollowing out what used to be the middle class.

On the bright side, tariffs can be an aid to U.S. businesses that source from home or from allies and can force others to do so as well. This not only improves conditions for U.S. suppliers, but more often than not, puts upward pressure on low- to middle-income wage levels. This must be considered in making "big picture" projections.

Simply scoffing at tariffs, because someone does not like the one willing to use them, is political in itself. Globalism has in my opinion done as much as anything else to expand the ranks of the U.S. poor, while hollowing out what used to be the middle class.

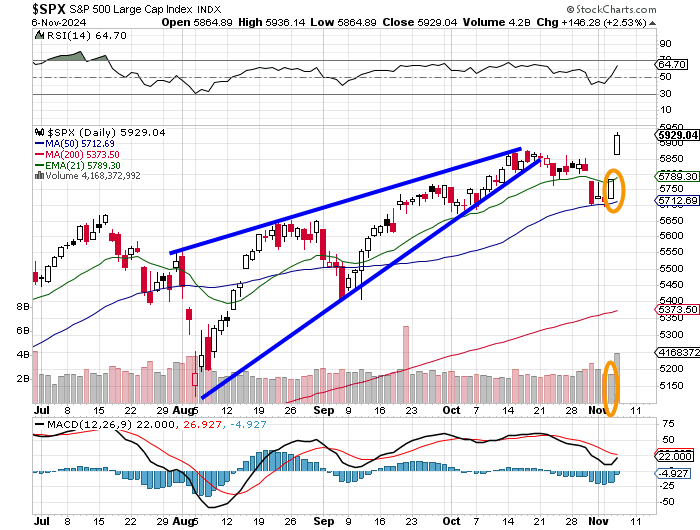

Wednesday's Romp

Equity markets broadly celebrated the likelihood for reduced regulation that a re-election of Pres. Donald Trump probably brings with it. The S&P 500 ran 2.53% on Wednesday as the Nasdaq Composite gained an impressive 2.95%. Both of our major equity indices closed at all-time highs. That does not mean that the two were not outperformed by several of the mid-majors.

If you did something other than trade the markets on Wednesday, some of these numbers will knock your socks off. The Dow Industrials and Philadelphia Semiconductors gained 3.57% and 3.12% in that order. Smaller caps? The S&P 400 gained 4.15% as the Russell 2000 popped for a gain of 5.84% and the S&P 600 soared 6.09%. We're not done. The KBW Bank Index ... drum roll please ... ran a stunning 10.69% higher for the day.

Eight of the 11 S&P sector SPDR exchange-traded funds closed out Wednesday in the green. Financials XLF obviously led, gaining 6.08%, followed by three other cyclical-type sector funds that gained more than 3%. The bottom four rungs on the daily performance tables were clearly reserved for defensive-type sectors as risk was "on" for the day, in a "bigly" kind of way. The Staples XLP and the REITs XLRE both gave up more than 1%.

Trump Trade Trading Volumes

On Wednesday, at the NYSE, winners beat losers by roughly 5 to 3 after beating losers 9 to 2 on Tuesday. Advancing volume took a 65.9% share of composite Wednesday NYSE-listed trade after taking an 80% share on Tuesday. Aggregate trading volume for NYSE-listings was up a jaw dropping 68% on a day over day basis after Tuesday's aggregate was up just 4.6% day over day.

At the Nasdaq, on Wednesday, winners beat losers by a 7 to 4 margin after beating losers 5 to 2 on Tuesday. Advancing volume took a 64.2% share of composite Nasdaq-listed activity on Wednesday after taking a 77.6% share on Tuesday. Aggregate trading volume for Nasdaq-listings was up 15.3% on a day over day basis after Tuesday's aggregate was up 22.5% day over day.

The trading volumes over the past two days have been enormous. On Wednesday, the S&P 500 had its busiest regular trading session since September Triple Witch. As far as I can tell, Wednesday was the busiest day for stocks on a non-expirations event, and non-rebalancing event type of day in years.

Remember Tuesday's 'Day One'?

Readers have seen a lot of this chart lately. That's because it is evolving daily. The Nasdaq Composite chart has behaved similarly with the exception of not having tested its 50-day simple moving average. We see here that the S&P, after having tested that thin blue line, put together a day of upward reversal on increased trading volume on Tuesday (Election Day). That was our "day one." After "day one", we look for a day of confirmation. That would be a second day in support of the upward move, again on increased trading volume.

The catch? Yes, there is a catch. Technically, Wednesday, despite gapping higher on humongous trading volume, is considered part of the same move as Tuesday. For confirmation, we need to see some daylight between the day of reversal and the confirmation day. Unfortunately, as wonderful as Wednesday was for shareholders, it did not constitute a confirmation of an upward change in trend. Not that this confirmation won't still happen. Just understand that we do not have it just yet.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 221K, Last 216K.

08:30 - Continuing Claims (Weekly): Last 1.862M.

08:30 - Non-Farm Productivity (Q3-adv): Expecting 2.3% q/q, Last 2.5% q/q SAAR.

08:30 - Unit Labor Costs (Q3-adv): Expecting 0.7% q/q, Last 0.4% q/q SAAR.

08:30 - Wholesale Inventories (Sep-rev): Flashed 0.1% m/m.

10:30 - Natural Gas Inventories (Weekly): Last +78B cf.

4:00 p.m. - Consumer Credit (Sep): Last $8.93B.

The Fed (All Times Eastern)

2:00 p.m. - FOMC Policy Decision. 2:30 - FOMC Press Conference.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: BDX (3.77), DDOG (.40), DUK (1.73), HAL (.75), MRNA (-1.94), RL (2.38)

After the Close: ABNB (2.13), SQ (.88), TTD (.39), U (.14), UPST (-.15)

At the time of publication, Guilfoyle had no position in any security mentioned.