My Stock Pick for 2024 Might Surprise You, but Not When You Learn Why

I narrowed down my choice from a bunch of big tech winners like Nvidia and Amazon, and several military contractors.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Some of you might be surprised when I reveal my stock pick for 2024. But before I name names, let me explain a few things.

I don't feel as good about the economy as everyone else seems to feel, but I do believe that further strength in equity markets will have been driven by purpose, as I think inflation will flare up at least once or twice if not more, and I do believe that the economy will slow to the point where we will wonder whether or not we are in recession.

Once we are in that position, the rest is up to the human response. I hear other pundits talk about a shallow or moderate recession. Granted, the Fed may reverse course completely on monetary policy, but that would also mean that things are moving along at a much worse clip than projected. Once managers freeze wages, other managers freeze wages. Once managers cut overhead, other managers cut overhead. Less capital goods are purchased, less business-to-business services are purchased and more payrolls are cut. Once Johnny loses his job, Jimmy becomes more grateful for his.

That's how humans respond to conditions of surplus and scarcity and emotions such as fear and anger are involved. These are impossible to predict. This is why we must identify drivers that are more impervious to human response than others. This is why we must be as emotionless as we can be.

The drivers that I see as sustainable are those likely to benefit from the emergence and expansion of generative artificial intelligence, aerospace and defense, and cybersecurity. You all know that I am long Nvidia NVDA and Advanced Micro Devices AMD , Palo Alto Networks PANW , CrowdStrike CRWD , Lockheed Martin LMT , General Dynamics GD and Northrop Grumman NOC . Though I do not expect to sell any of those names anytime soon, they did not make the final four. I then excluded another long position that I like, Amazon AMZN .

My final three were Alphabet GOOGL , Microsoft MSFT and the name that is my 2024 stock of the year ... Palantir Technologies PLTR .

Pealing Back Palantir

Palantir, as former "Stocks Under $10 Portfolio" subscribers well know, was one of the great wins at the portfolio. This stock was never a true small-cap at least while it was in that portfolio, but it sure did trade below $10. The company currently runs with a market cap of more than $38 billion, since coming in a bit over the past month. That said, the shares traded as low as $7.28 as recently as this past May. The stock is still up 140% from those May lows despite standing almost 20% below the November highs.

About a week ago, Palantir won a long-rumored contract with the U.K.'s National Health Service to modernize the national system and create a more efficient, more clearly defined road toward improving the patient experience. There was a bit of a "sell the news" response that followed that news as it came to light that not only was Palantir to lead a handful of companies in the effort, thus sharing the payout, but the contract itself (seven years, 330 million British pounds, including 25.6 million British pounds the first year) was considerably less lucrative that were the rumors that preceded it. Investors were mildly disappointed. There was some profit taking.

Since then, Palantir's deal with the U.S. Army has been extended for one year to run the Vantage program for a contract valued at $115 million. This is the extension of the 2019 four-year deal for $458 million that was up for renewal that had some analysts doubting. The deal was extended for a year (a win for the bears?) at almost the same fee (a win for the bulls?).

Additionally, a number of Palantir insiders had made planned sales of some of their shares. Since the firm's most recent earnings release on Nov. 2, CEO Alex Karp, CTO Shyam Sankar, CFO David Glazer and President Stephen Cohen have all made sales as did Peter Thiel who serves on the board of directors. Thiel, Cohen, and Karp are all Palantir cofounders. This rattled some investors further. You don't see any of those insiders taking leave of the firm, do you?

Earnings Beat

Palantir on Nov. 2 released third-quarter earnings results, revealing an adjusted earnings per share of $0.07 (unadjusted EPS: $0.03) on revenue of $558.159 million. These results topped consensus expectations across all three of those metrics, as the sales number grew 16.8% year over year.

The lion's share of the adjustments made were made primarily for the purpose of stock-based compensation. That quarter was the fourth consecutive quarter of unadjusted profitability, which is technically now eligible for membership in the S&P 500.

As revenue grew 16.8%, the cost of that revenue increased just a bit to $107.922 million. This left gross profit of $450.237 million (+21.6%) as gross margin improved from 77.5% all the way to 80.7%. Total operating expenses actually decreased (not a misprint) 5.1% to $410.254 million, leaving an operating income of $39.983 million (up from the year ago comp of $5.54 million). This took operating margin up to 6.6% from a mere 1.6%. After accounting for interest and taxes, net income / loss attributable to shareholders improved from -$123.875 million to $71.505 million -- that's an almost a $200 million swing. That's how we get to a unadjusted EPS of $0.03

Looking forward, Palantir is set to report the current quarter in mid-February. Wall Street is looking for an adjusted EPS of $0.08 (up from $0.04) or an unadjusted EPS of $0.03 on revenue of roughly $603 million. That would be good enough for year over year growth of 19%.

Getting Down to the Basics

For that most recent quarter, Palantir generated operating cash flow of $133.443 million. Out of that, the company spent only $1.565 million on capital expenditures, and added a credit of $8.969 million for cash paid related to employer payroll taxes tied to stock-based compensation. This put free cash flow at $140.847 million. (Larger than operating cash flow. You don't see that very often.) Year to date, free cash flow comes to $425.772 million. The company does not return and has not returned capital to shareholders. That means that this free cash is truly free and has migrated to the balance sheet.

Looking at that balance sheet, Palantir ended the most recent period with a cash position of $3.283 billion and current assets of $3.809 billion. Current liabilities added up to $688.925 million, including deferred revenue of $223.507 million. That puts Palantir's current ratio at an super-hero strong 5.53. If we adjust for deferred revenue, which as we know is not a financial obligation, this current ratio then rises to an awe-inspiring 8.19.

Total assets amount to $4.193 billion. The company claims no value for intangible assets, which we like to see. Total liabilities less equity came to $921.52 million, which included an additional $34.88 million in deferred revenue. There is absolutely no debt on this balance sheet. None. Zero.

Think this through: Cash position of $3.283 billion, no debt whatsoever, current ratio of 5.53, and an adjusted current ratio of 8.19. This balance sheet is as clean as a whistle and you would have to search high and far to find another mid-cap company with a fortress like this behind the business.

A Light Ahead

At the time of that earnings release, for the current quarter to be reported in February, Palantir expected to generate revenue of $599 million to $603 million. That leaves the midpoint above the $599 million that Wall Street was looking for at the time. Consensus is now for $603 million. The company also expected to drive adjusted operating income of $184 million to $188 million and a positive unadjusted net income.

For the full year, Palantir has raised its revenue guidance to $2.216 billion - $2.22 billion, bringing the lower end of the range above the $2.21 billion that Wall Street was looking for at that time. Wall Street is now at $2.22 billion. Full-year adjusted operating income is expected to land between $607 million and $611 million, as the company still expects to achieve unadjusted profitability for each quarter of the year. Current Wall Street expectations for adjusted EPS are for $0.08 (Q4) and for $0.29 (full year). Nine of nine sell-side analysts who cover PLTR have increased their earnings expectations for this firm over the past 90 days.

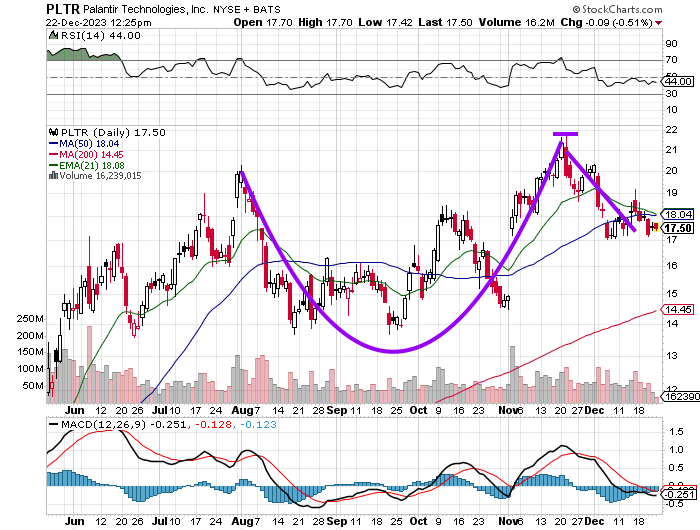

The Technicals

Readers can see that the cup pattern developed that stretched from late July into mid-November. It appears a handle has been added to that cup on the November into December pull back that took the shares down below their 21-day EMA and 50-day SMA. That places the pivot on the right side peak, which here is $22.

This puts our target price for PLTR at $27. I believe the opportunity to initiate or add to this name is now as the handle feels around for support. Relative strength is neutral and the daily Moving Average Divergence Convergence is actually bearish looking as that cup pattern has just (maybe completed) adding the handle. The stock did just surrender its 50-day simple moving average, which would be a sign of caution for a shorter-term trader.

How to Handle Palantir

Target Price: $27

Pivot: $22

Add: down to 200-day SMA ($14)

Panic: Break of 200-day SMA.

(AMZN, GOOGL, and MSFT are among the holdings in the Action Alerts PLUS portfolio. Want to known when AAP buys or sells stocks? Click here now.)

At the time of publication, Guilfoyle was long NVDA, AMD, PANW, CRWD, LMT, GD, NOC, AMZN, GOOGL, MSFT, PLTR equity.