Meta's Quarter Looks Just Fine Without Augmented Reality

And here's how I'd trade the name.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Meta Platforms META reports, and did they ever?

Social media and, I guess, future metaverse giant Meta Platforms released second- quarter financial results after the close on Wednesday evening -- and the numbers were hot. Meta posted an unadjusted earnings per share of $5.16 on revenue of $39.071 billion. These top and bottom-line numbers both easily beat Wall Street's expectations, while that revenue print reflected year-over-year growth of 22.1%.

Family of Apps daily active people (DAP) was 3.27 billion on average for the month of June 2024, which was up from June 2023. Ad impressions delivered across the firm's family of apps increased 10% over the comparable period last year. Average price per ad increased 10% year over year as well. Headcount decreased 1% to 70,799 as of the quarter's end.

Operations

As revenue generated increased 22,1% to $39.071 billion for the quarter, the cost of that revenue plus operating expenses increased 7.2% to $24.224 billion, leaving operating income of $14.847 billion, which was up a whopping 58.1%. After accounting for interest and taxes, net income printed at $13.465 billion, which was a stunning year-over-year increase of 72.9% over last year's comp. This works out to $5.16 per diluted share versus last year's $3.03. No doubt, expenses are rising as was Wall Street's fear going in. Obviously though, revenue generation is accelerating at a far greater pace than are costs.

Segment Performance

- Family of Apps... generated revenue of $38.718 billion (+22.1%), producing an operating income of $19.335 billion (+47.2%). This unit includes Facebook, Instagram, Messenger, Threads, and WhatsApp.

- Reality Labs... generated revenue of $353 million (+27.9%), producing an operating loss of $4.488 bilion (compared with a loss of $3.739 billion). This is the unit that contains the Oculus VR, and augmented reality hardware and software, Ray-Ban Meta glasses and Quest 3. This is the home of the Metaverse.

Guidance

For the current quarter, Meta sees revenue generation at $38.5 billion to $41 billion, assuming a 2% foreign exchange headwind. This brings the midpoint of that range above the $39.1 billion expected by Wall Street. Meta also sees full year capital spending as potentially higher than previously provided guidance. The company sees 2024 capital expenditures at $37 billion to $40 billion, bringing the lower end of that range up from $35 billion. But full-year total expenses are in a range spanning from $96 billion to $99 billion. That is unchanged from guidance previously given.

On Generative AI...

"We had a strong quarter, and Meta AI is on track to be the most used AI assistant in the world by the end of the year," said CEO Mark Zuckerberg in the press release. "We've released the first frontier-level open-source AI model, we continue to see good traction with our Ray-Ban Meta AI glasses, and we're driving good growth across our apps."

During the call, Zuckerberg added that, "At the end of the day, we are in the fortunate position where the strong results that we're seeing in our core products and business give us the opportunity to make deep investments for the future. And I plan to fully seize that opportunity to build some amazing things that will pay off for our community and our investors for decades to come. The progress we're making on both the foundational technology and product experiences suggests that we're on the right track."

Fundamentals: Strong Balance Sheet

For the period reported, Meta generated operating cash flow of $19.37 billion. Out of that number, came capital expenditures of $8.173 billion and principal payments on finance leases of $299 million, leaving free cash flow of $10.898 billion, which was in line with the year-ago quarter. Out of that number, Meta repurchased $6.299 billion worth of common stock and paid out $1.266 billion in cash dividend payments.

Turning to the balance sheet, Meta ended the period with a cash position of $58.08 billion and current assets of $76.431 billion. Current liabilities add up to $27.004 billion that includes no debt and no unearned revenue. This leaves the firm with a very strong current ratio of 2.83.

Total assets amount to $230.238 billion, including just $20.654 billion in goodwill. At less than 9% of total assets, this is hardly worth mentioning. Total liabilities less equity comes to $73.475 billion. this does include $17.685 billion in long-term debt, which is something that Meta could pay out of pocket more than three times over. This is a rock-solid balance sheet.

Wall Street's Take

When it comes to Meta Platforms, there's more opinion on Wall Street than one could shake a stick at. So far, I have come across 29 highly rated (four-plus stars at TipRanks) who have opined on META since these earnings were released last night. After allowing for changes, there are 26 "Buy" or buy-equivalent ratings and three "hold" or hold-equivalent ratings among them. Three "Buys" and one "Hold" chose not to set a target price, so we are working with 25 targets.

The average target price across those 25 analysts is $576.80 with a high of $647 (Ken Gawrelski of Wells Fargo) and a low of $$470 (Brian Pitz of BMO Capital). Once omitting those two as potential outliers, the average target across the other 23 rises to $578.17.

My Take

These were much better-than-expected earnings. We also heard from a sharp sounding Zuckerberg who sounds like he knows exactly what he's trying to do and understands how to go about it. And we got muscular cash flows, a superb balance sheet, and robust returns to shareholders. There really is no glaring problem spot at this time. Zuckerberg even expressed during the call that the "Family of Apps" is making significant strides in attracting young adults who a few years ago, had appeared to have moved on. I am not long these shares. Last night, Zuckerberg left me wishing I was.

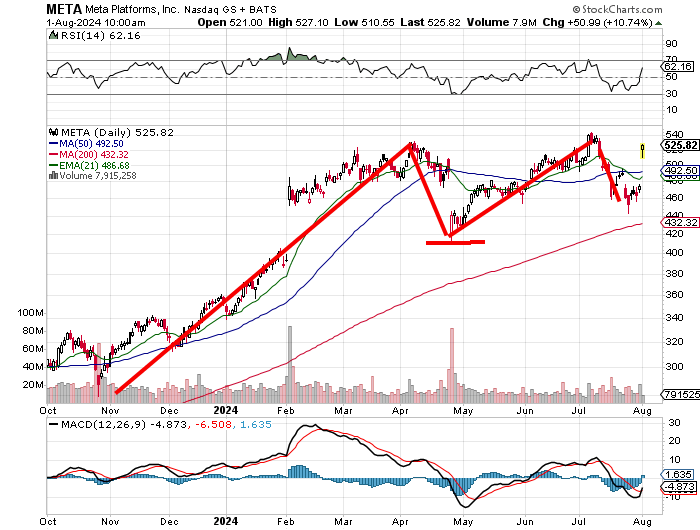

I'm not going to blow smoke up your tailpipe. The chart is not all that optimistic. Relative Strength has suddenly turned sharply in a northerly direction as the daily moving average convergence divergence indicator has just experienced a bullish crossover of the 26-day exponential moving average by the 12-day EMA. But both remain in negative territory.

The biggest problem with this chart is that despite this morning's 11% pop, the prevailing technical pattern is still a double-top reversal, which is a bearish pattern. The double top has a pivot of $414, that almost seems out of comprehension at this point. Still the pattern is not broken until either a third peak is created or the 50-day simple moving average is held long enough to start making everything from June on start looking like consolidation. Remember, triple tops do exist. They are less common than double tops, but they are just as bearish.

This morning's action has created a huge gap unfilled between $476 and $510. I would be real slow to initiate or add any unhedged equity between the 50-day SMA ($492) and the apex of the second top ($542). It's not that this is not a good company, or that it did anything wrong. It's that I missed the good prices, and these prices are not necessarily good, know what I mean?

Trade Idea

I would feel more comfortable, at these prices, getting long an Aug. 23 $525 / $545 bull call spread for a rough net of $8 than I would shelling out the dough for the equity. That same trader, if unafraid to expose him or herself to discounted equity risk, could also sell a like amount of Aug. 23 $500 puts for just under $8 nearly wiping out the net debit on the spread. Just an idea.

At the time of publication, Guilfoyle had no position in any security mentioned.