With Increased Dividend and Lower Rates on the Way, it's Time to Consider This REIT

This small-cap real estate investment trust is outperforming XLRE and presents a compelling opportunity to investors.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Lower rates on the way? The REITs have been hot. The Real Estate Sector SPDR ETF XLRE is now up 20% from its springtime lows. The XLRE yields 3.15%. What if I found you a small-cap REIT that's been profitable, been growing revenue and, after increasing the dividend last week, now yields 6%? Oh, and it's outperforming the XLRE.

You'd listen, right? Check this one out...

Alpine Income Property Trust (PINE)

Who? Alpine Income Property Trust PINE is a Florida-based REIT that seeks to deliver risk-adjusted returns and cash dividends by investing in, owning and operating a portfolio of single-tenant properties predominantly leased to publicly-traded and credit-rated tenants.

The primary objective of the business is to maximize cash flow and value by generating stable, risk-adjusted returns. The firm operates through two segments: income properties and commercial loans and investments. There are 138 properties in the corporate portfolio that represent 3.8 million gross rentable square feet with leases that run with a weighted average term of seven years.

Results and Expectations

For the second quarter, Alpine posted funds from operations (FFO) of $0.43 on revenue of $12.49 million. Both numbers beat Wall Street, while the revenue print was good for year-over-year growth of 10%. For the current quarter, Alpine is expected by Wall Street to generate FFO of $0.40 on revenue of $12.16 million. The four analysts that I know of that follow this stock have all increased their estimate for this quarter's revenue since the quarter started.

Balance Sheet and Fundamentals

Alpine ended the June quarter with total assets of $565.8 million, including real estate assets valued at $446.4 million. The firm does have long-term debt of $268.3 million, but none of it is current (maturing within 12 months). As of the end of that period, the firm had a tangible book value of $198.3 million, which works out to $14.55 per share. That's not too bad.

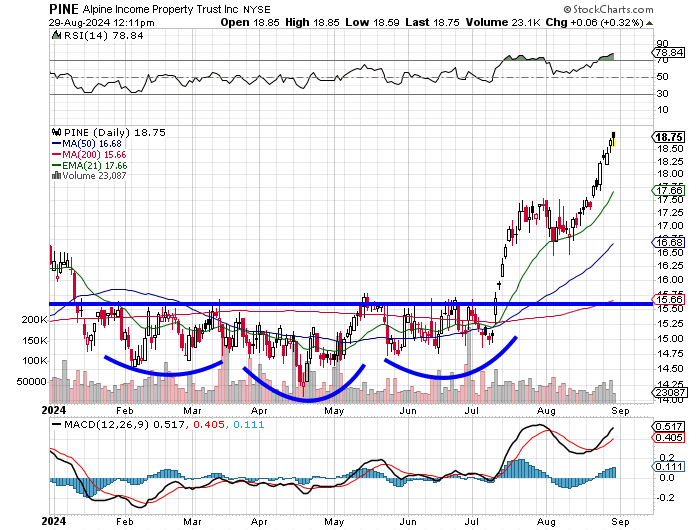

The Chart

Just look at this chart.

A 30% rise off of springtime's lows. Both the daily MACD and RSI appear to be technically overbought. I see a very subtle inverse head and shoulders with a neckline at $15.65. That's the pivot. In my book, this creates a target of roughly $19.50.

However, I am not sure that this stock is trading on technicals. Since early July, it's gone parabolic in slow motion, outperforming the REITs more broadly. That 6% yield though. I just locked in 4.5% on a CD at my bank going into next year, which is something because they know rates are about to come in. $1.12 a year. Might be worth it, if you can catch this one on a down day.

At the time of publication, Guilfoyle had no positions in any securities mentioned.