This Natural Foods Company Is Definitely Investible

The CEO seems focused on cleaning up some issues and a trade opportunity has emerged.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Tuesday morning, The Hain Celestial Group Inc HAIN released the firm's fiscal fourth quarter results. For the three-month period ended June 30, HAIN posted an adjusted EPS of $0.13 (GAAP EPS: $-0.03) on revenue of $418.799 million. The top-line number fell just short of Wall Street's expectations while reflecting a year-over-year contraction of 6%. The adjusted EPS print beat the street by a nickel. Adjustments were made for long-lived asset impairments and certain litigation expenses.

Just Who the Heck Is Hain Celestial?

This Hoboken, New Jersey based firm describes itself as a global health and wellness company. The firm operated through two segments: North America, that includes the U.S. and Canada, and International, that includes the U.K. and Europe.

Hain's products are sold through a number of brand names that some readers have definitely heard of. These would be Garden Veggies Snacks, Terra Chips, Garden of Eatin, Celestial Seasonings, Joya, Yorkshire Provender, Covent Garden, Alba Botanica and Live Clean. These products are sold through specialty stores, natural food distributors, supermarkets, natural food stores, convenience stores and through e-commerce retailers as well.

Quarterly Sales Performance

- North America generated $260 million in sales (-8%) on organic growth of -5%

- International generated $159 million in sales (-4%), all organic

- Snacks generated $121 million in sales (-6%) on organic growth of 0%

- Baby & Kids generated $64 million in sales (-10%) on organic growth of -10%

- Beverages generated $56 million is sales (+3%) on organic growth of 3%

- Meal Prep generated $149 million in sales (-5%) on organic growth of -5%

- Personal Care generated $29 million in sales (-21%) on organic growth of -17%

CEO on Struggles

Wendy Davidson, the still newish (her term started on January 2023) president and CEO of the firm, commented in the press release: “Fiscal 2024 was the foundational year of our Hain Reimagined strategy, during which we made substantial progress in simplifying our business and generating fuel. We transitioned to a global operating model, reducing geographic complexity and driving scale, and developed a performance-driven, values-based culture. Our fuel initiatives exceeded our targets for fiscal 2024, allowing us to pay down debt, invest in capabilities, and to deliver on our updated full-year guidance.”

Operations

As net sales contracted by 6%, the cost of those sales decreased 7.6% to $320.79 million. This left a gross profit of $98.003 million (-2.7%) on a gross margin of 23.4%, up from 22.5%. After accounting for operating expenses, transformation costs and the amortization of acquired assets, GAAP operating income dropped 0.7% to $12.012 on a GAAP operating margin of 2.9%, up from 2.7%.

Adjusted EBITDA landed at $40 million, down from $44 million a year ago as adjusted EBITDA margin dropped from 9.7% to 9.4%. After accounting for interest, other expenses and income and taxes, net income/loss came to $-2.937 million, which works out to a GAAP EPS of $-0.03, which was up from the year-ago comparison of $-0.21.

Guidance

For the full fiscal year just started, Hain sees organic net sales growth that is flat at worst. Adjusted EBITDA is seen growing by mid-single-digits. Gross margin is projected to grow by 125 basis points. Free cash flow is seen at a minimum of $60 million.

Fundamentals

For the fiscal fourth quarter, despite having its problems, Hain generated operating cash flow of $39.396 million. Out of that number came capex spending of $8.692 million. This left free cash flow of $30.704 million. The firm used this free cash and then some to pay down a net $33.575 million worth of debt between term loans and a revolving credit facility.

Turning to the balance sheet, at quarter's end Hain had a cash position of $54.307 million and inventories of $274.128 million. This puts current assets at $557.059 million. Current liabilities add up to $281.503 million including shorter-term debt of just $7.569 million. The firm's current and quick ratios stand at a more than adequate 1.97 and 1.01, respectively.

Total assets amount to $2.118 billion. This includes $1.174 billion in goodwill, trademarks and other intangibles. At 55.4% of total assets, I will admit to being uncomfortable with that number. I'd rather the majority of assets by a wide margin be tangible. Total liabilities less equity comes to $1.175 billion, including long-term debt of $736,523 million. Yes, that can be a problem for a firm with a cash position that comes to about one-thirteenth of that number. The current situation is fine. Longer term, this balance sheet is a work in progress. At least the CEO does seem to be on top of it.

My Thoughts

HAIN is, in my opinion, certainly investible. At least with this CEO, Wendy Davidson, at the helm. She seems to be getting a handle on margins and on cash flows. She is also serious about paying down debt. This may be when one invests in a name that has been through heck but is finally getting its footing.

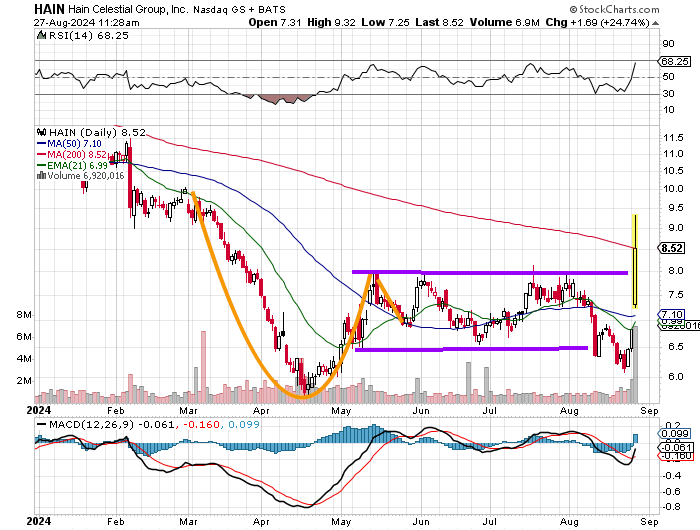

This stock traded at a high of $48.88 late in 2021. In less than three years, the share price has been decimated. Readers will see that coming out of the long sell-off, as the stock price stabilized, a cup with handle pattern formed that failed to develop a breakout.

The stock then based for about three months, broke out to the downside, and then on Tuesday, on this news, broke out to the upside. It's easy to see why. The guidance is better than feared and the CEO is serious about improving the fundamentals.

This morning, as both the stock's RSI and daily MACD showed improvement, the shares took back their 21-day EMA and 50-day SMA. The stock had taken at one point, its 200-day SMA, but has had trouble holding that level.

Plan...

- Don't chase

- Initiate a long equity position on any ensuing dip within a week or two that retests the 50-day SMA from above

- Go out to October 18, 2024, expiration and purchase $8 calls for about $1.00. Sell a like amount of Oct 18, 2024, $7 puts for about $0.10 to reduce the expense. The options trade will cost the trader a net $0.90. Should the investor end up long the stock after expiration, it would either be at a net basis of $8.90 with the stock trading above $9 or at a net basis of $7.50 with the shares trading below $7.

At the time of publication, Guilfoyle had no positions in any securities mentioned.