Fix Portfolio Drift Now and You Might Save Your Retirement

Your future self is begging you to check up on your portfolio holdings.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Say you’re 35, and you’ve been investing in your 401(k) for the past decade. For the most part, markets have been strong, with the S&P 500 up about 15%.

Your account balance looks great, and you haven’t touched your allocation in years.

And why would you?

Things may look super duper now, but this is exactly how people end up in trouble 20 years down the road. Bull markets gradually push portfolios into equity-heavy territory and nobody notices until a volatile quarter hits just when you’re thinking, “Hey I might like to retire sometime.”

Why Timing Matters More Than You Think

I’ve written a lot here about sequence of returns risk, which rears its ugly head in a down market in the early years of retirement.

But the problem I’m focusing on today isn’t losing money. It’s the problem of making too much money.

I hear you loud and clear.

How in the world is that a problem?

Well, if you get used to good markets, you might be reluctant to rebalance your account, or implement a glide path that would dial down the risk as you approach retirement.

What Portfolio Drift Actually Looks Like

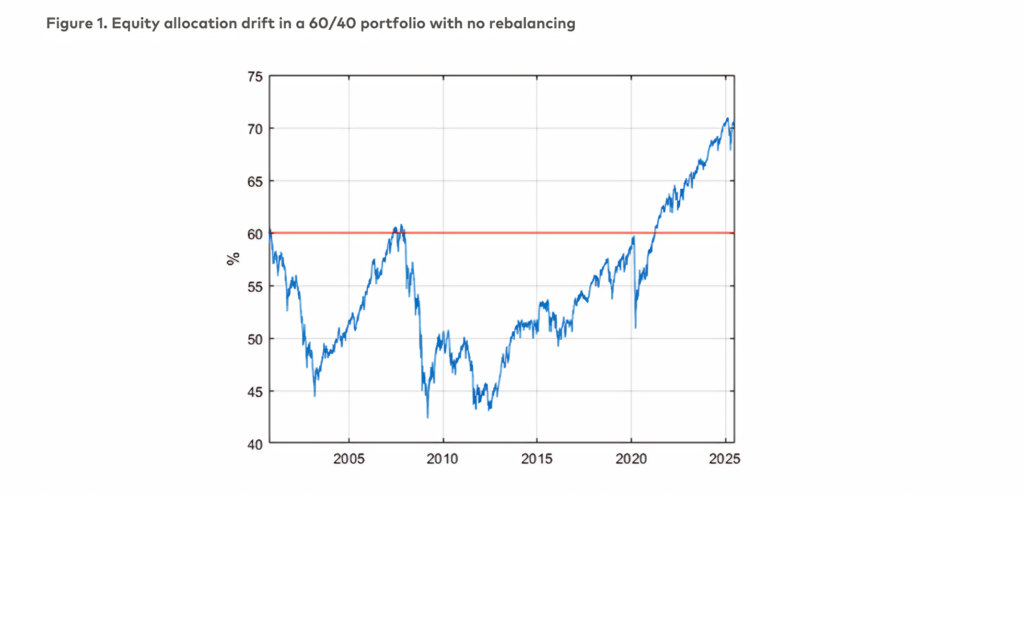

Below are a couple of charts from Vanguard that show what account complacence can look like.

The first image shows an initial 60/40 portfolio left untouched between 2000 and 2025. It drifts all over the place, eventually consisting of about 70% equities by 2025. That’s significantly overweight its original risk target.

Nobody here made an active decision to take on more risk. It just kinda… happened. The market ran lower, then higher, then ultimately much higher, and the ignored allocation followed along.

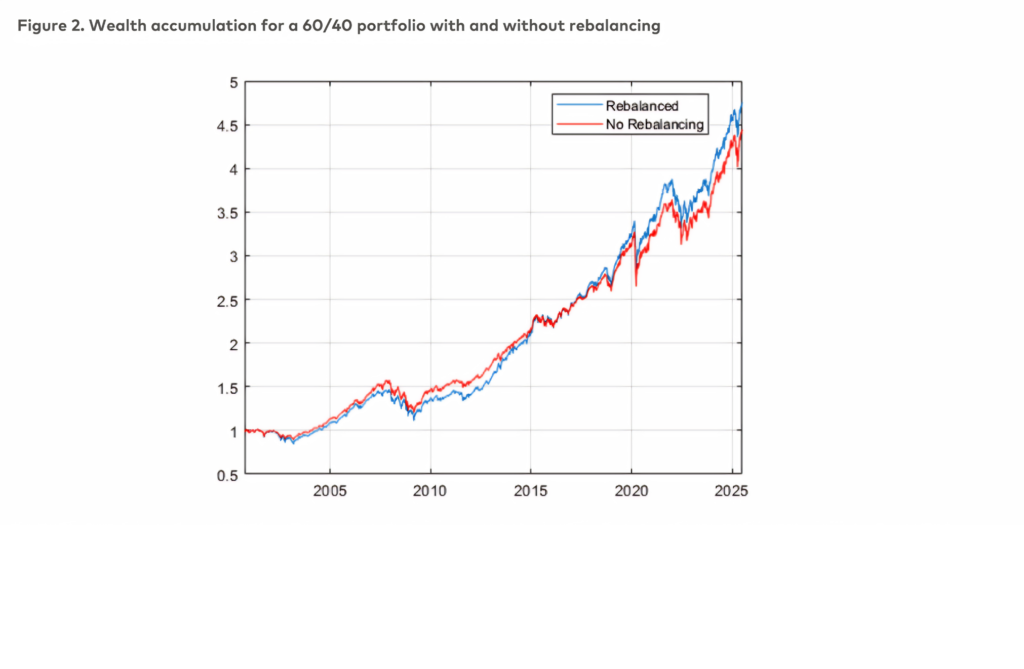

This second image from Vanguard shows the results of that inattention. One dollar invested in 2000 grew to around $4.50 by 2025. The rebalanced portfolio edged ahead slightly and held up better during downturns like 2022.

But the most important benefit of rebalancing wasn’t higher returns. It was avoiding the extra volatility that comes from letting stocks drift above their target allocation.

A 60/40 portfolio drifting to 70/30 isn’t just a minor imbalance. It means you’re carrying significantly more equity risk than you intended. During a market crash, that extra exposure translates directly into deeper losses. No “may” or “could” type of qualifiers needed here.

And that kind of drift can happen fast: Even small portfolios can swing eight to 12 percentage points in just 18 months during strong markets.

“Over time, the performance of different asset classes will vary. This can cause your asset allocation to drift away from your target allocation. To keep your portfolio aligned with your financial goals, you’ll need to rebalance it regularly. This can mean selling some of the investments that have performed well and investing the proceeds in other asset classes, or adding money to any asset class that’s below its target allocation.”

-Vanguard Group, “Investment portfolios: asset allocation models”

When This All Matters

That 60/40 portfolio drifting to 70/30 isn’t such a big deal if you’re in your mid-30s or early 40s, with no thought of retirement lurking in the back of your mind.

But give yourself a few years.

A decade out from retirement, you’ve entered the window where sequence of returns risk finally becomes real.

A sharp downturn in your final working years can do some real damage to an overweighted equity portfolio. It can permanently reduce what you’re able to withdraw in retirement, even if markets eventually recover.

We tend to think of that risk popping up early in retirement, but it can wreak havoc if you’re still working. That’s why people delayed retirement after the great financial crisis. Back then, I had clients who hadn’t paid any attention to their portfolios before we met; several decided to work a few extra years as their investments stabilized.

This is exactly why financial planners treat the decade before retirement as a distinct planning phase.

“As retirement approaches, complexity increases. Decisions become more nuanced as savers navigate how to draw income; when to claim Social Security; how to sequence withdrawals; and how to balance longevity, market risk, and health care costs.”

-T. Rowe Price, “Retirement Market Outlook”

Letting drift go unchecked means you may arrive at that window with far more equity exposure than your plan ever assumed, and far less margin for error than you realize. Bull markets are great, but the old advice, “let your winners run” doesn’t apply in this case the way it might with your higher risk single-stock account that’s not earmarked for future spending.