Eli Lilly: The One That (Kind of) Got Away

The stock's march higher has been relentless. But now that Lilly's obesity and other drugs are actually producing revenue, is it all priced in? Here's my bearish trade idea.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I can't complain.

Eli Lilly LLY was one of my great trades of 2022-2023. I got out of the shares at an average of $771.39 by May of this year. My average on the way in was $313.35. Like I said, I cannot complain.

My execution on the way out might not be anything to brag about, but it is far better than not making money. The stock ran up to $966 within two months of my sale, then ran back down to where I got out by early August. Thursday morning, LLY shares are soaring yet again in response to the company's second-quarter numbers.

For the second quarter ended June 30, Lilly posted adjusted EPS of $3.92 (GAAP EPS: $3.28) on revenue of $11.303 billion. These top and bottom-line results both beat Wall Street's expectations, while the revenue print reflected year-over-year growth of 36%.

The adjustments were made for restructuring costs, net losses on equity investments, and the amortization of intangible assets.

The sister drugs Mounjaro for diabetes and Zepbound for obesity drove the sales growth along with Verzenio, which is indicated for breast cancer therapy. The growth was offset somewhat by declining sales of Trulicity, which is also a diabetes drug.

The shares are trading up around 8% with an $835 handle Thursday morning. This is interesting because key competitor Novo Nordisk NVO had a tough day on Wednesday after reporting sales that missed the mark for its Wegovy weight-loss drug.

The CEO

David Ricks, Chair and CEO of Eli Lilly, commented in the press release:

"Mounjaro, Zepbound and Verzenio led our strong financial performance in the second quarter as we advanced our manufacturing expansion agenda, and it is equally exciting to see the growth around the world of our medicines for cancer, neurological disorders and autoimmune diseases. We also recently received approval of Kisunla to help people with Alzheimer's disease, a moment that was decades in the making."

Key Drug Revenue Performance

-- Mounjaro generated revenue of $3.091 billion (up from $979.7 million).

-- Verzenio generated revenue of $1.2466 billion (+42%).

-- Trulicity generated revenue of $3.091 billion (-31%).

-- Zepbound generated revenue of $1.243 billion (up from zero).

-- Taltz generated revenue of $824.7 million (+17%).

-- Jardiance generated revenue of $769.9 million (+15%).

-- Humalog generated revenue of $631.6 billion (+43%).

Guidance

For the full year, Eli Lilly is raising guidance.

Revenue is now seen at $45.4 billion to $46.6 billion, up from prior guidance of $42.4 billion to $43.6 billion. GAAP gross margin is seen at 36% to 38%, up from 32% to 34%, while adjusted gross margin is seen at 37% to 39% from 33% to 35%.

On a GAAP basis, the company is projecting EPS of $15.10 to $15.60, up from prior guidance of $13.05 to $13.55. Adjusted, the EPS print is now seen at $16.10 to $16.60, up from prior guidance of $13.50 to $14.00.

These improved numbers are on an expected effective tax rate of 15%, up from a previous expectation for 14%.

My Thoughts

The march higher has been relentless for almost two years. Now, these drugs that we were all betting on, are actually producing revenue and are the drivers of growth.

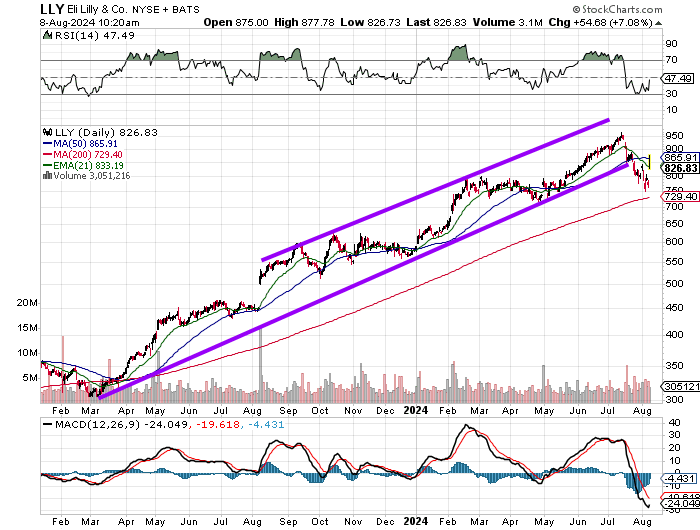

Readers will note that the stock had broken the support of the lower trend line of this ascending price channel and had to test its 200-day simple moving aaverage (SMA) as both its Relative Strength and daily Moving Average Convergence (MACD) exhibited weakness.

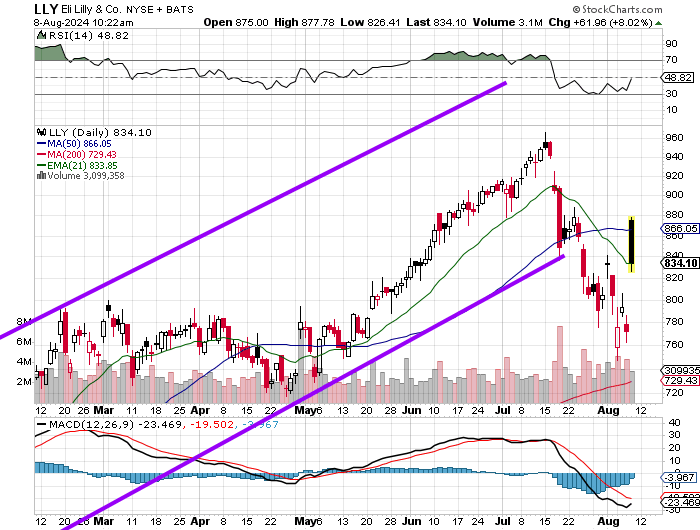

Let's zoom in a bit:

It would appear that LLY has been rejected at its 50-day SMA just after the U.S. open Thursday. Holding the 21-day expoential moving average (EMA) would at least keep some swing traders online. Failure to do so will result in a lower share price, not for the day, but one that puts the shares back where they were or close to it.

The stock trades at 56 times forward-looking earnings, so it's clear that Wall Street is looking for a lot going forward for this obesity drug maker. There is almost no short interest, so none of Thursday morning's action was the result of a squeeze.

My feeling is that for the short-term, the shares may be shortable in between the 21-day EMA and the 50-day SMA as it is probably necessary for this name to develop a base of consolidation. It may go much higher over the long run, but competition is only going to intensify.

A bearish trader not willing to short the equity could purchase an August 23 $825 put for about $20 and sell an $810 put with the same expiration for about $12. The net debit would come to roughly $8 in an attempt to win back $15.

Better than a sharp stick in the eye if it works. Controlled risk if it fails.

At the time of publication, Guilfoyle had no positions in any securities mentioned.