Complacency Kills

Risk comes fast and hard with very little warning. Almost two decades after the financial crisis, I have yet to forget what true despair felt like, and I hope I never do.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The reward for holding an asset is often slow, but risk comes fast. There could be many reasons for it, but my take is that investors become more comfortable buying as the market moves higher. The result is slow and consistent buy orders hitting the market. Yet, when traders liquidate, it is often done under duress and all at once. This is why they say markets climb the stairs but take the elevator down.

This pattern repeats itself over and over because humans are creatures of habit. But the irony is, if we could train ourselves to do what is uncomfortable rather than comfortable, we would probably be better traders and investors.

One of the biggest mistakes I've witnessed over the years is complacency. Market participants have short-term memories when things are going their way. For instance, stock market investors were scrambling to take on tech stock and cryptocurrency risk in hopes of outsized gains in late 2021. The buying frenzy was aggressive, illogical, and devoid of risk considerations. It was a mirror image of what transpired just a year and a half earlier when the S&P shaved off 35% of its value in a few weeks.

Unfortunately, the human tendency to panic when things feel bad and downplay risks when things feel good causes investors to sell their holdings at the worst time and load the boat at the most dangerous time. It isn't difficult to imagine someone ruining their retirement by selling into a 35% drawdown, then missing a 100% rally, only to start getting back in before the next 35% correction. Unfortunately, this experience happens more than one would expect.

Tough Lessons and Gaining Experience

I am a futures and options broker who, for a living, assists market participants in short-term speculation. I am not licensed or qualified to offer advice on long-term investment strategies. Nevertheless, I have learned some tough lessons and gained experience in market cycles, sentiment, and risk management. It has been my experience that when things seem too good to be true, they are.

As a young adult who had just broken into the middle class in 2005/2006, I was euphoric about my net worth. The financial crisis quickly made me aware that wealth on paper is merely a mirage unless you do something about it. In 2007, monitoring my home value on Zillow Z (yes, I know their "Zestimates" are not necessarily accurate estimates, but they are convenient) and hitting the browser refresh on my investment portfolio was like a drug. The higher the numbers, the wealthier I felt, and the more bullish everything appeared.

Looking back, it was both euphoric and complacent. The years following were a reality check; stocks lost over half of their value, and my home in Las Vegas was among the worst-hit zip codes in the nation, with losses close to 80%.

Risk came fast and hard with very little warning. Almost two decades after the financial crisis, I have yet to forget what true despair felt like, and I hope I never do because it is my mechanism for tapping the brakes on risk when things are going too well.

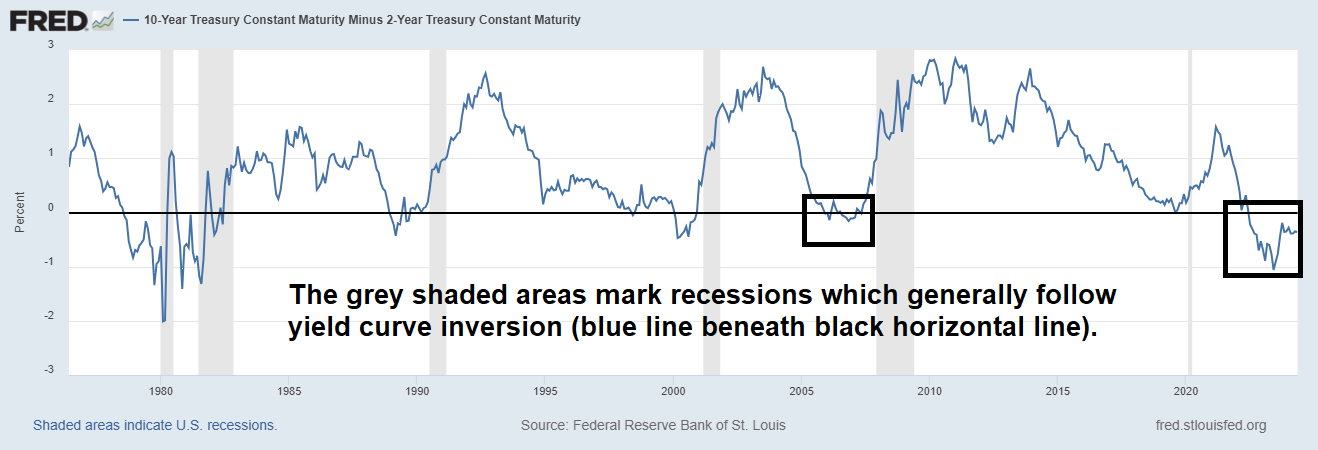

I hope I am wrong, but it feels like things are going too well at the moment. Further, I see signs of dysfunction similar to those that were present prior to the Financial Crisis, such as overleverage (think yen carry trade), complacency (think Dow 14,000 caps in 2007), and yield-curve inversion (inversion started in early 2006 and recession officially arrived in late 2008).

If everything is going unusually well for you regarding asset valuation or even your speculative trading, it might be time to focus on protecting accumulated wealth. Unless you hit the sell button or hedge your price risk, it doesn't count; complacency kills.

Portfolio Hedging

If you have stock market exposure to hedge, the futures and options markets offer efficient opportunities. The primary benefit of hedging vs. liquidating is retaining dividend income and avoiding a taxable event (i.e., locking in capital gains).

One way to do this is with risk reversals, often called market collars. In this strategy, a portfolio hedger can sell a call option above the market and use the proceeds to buy a put option. In other words, the investor can use the market's money to pay for downside protection.

Anyone who has purchased puts repeatedly to hedge a portfolio knows doing so is expensive and drags the performance of a portfolio considerably. For demonstrative purposes, an example would be to sell a June E-mini S&P 500 5400 call for about 20.00 points and then buy the June 5000 put for about 20.00 points. The result is free insurance under 5000, but the opportunity cost is to give up portfolio gains above 5400 and there is a margin requirement to hold the position.

Reach out to us at www.DeCarleyTrading.com if you are interested in participating in such hedging strategies.

More Trading Basics