If These Are the Best, I Would Hate to See the Rest

Considering annuities for a portion of your lifetime nest-egg? Read this first.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

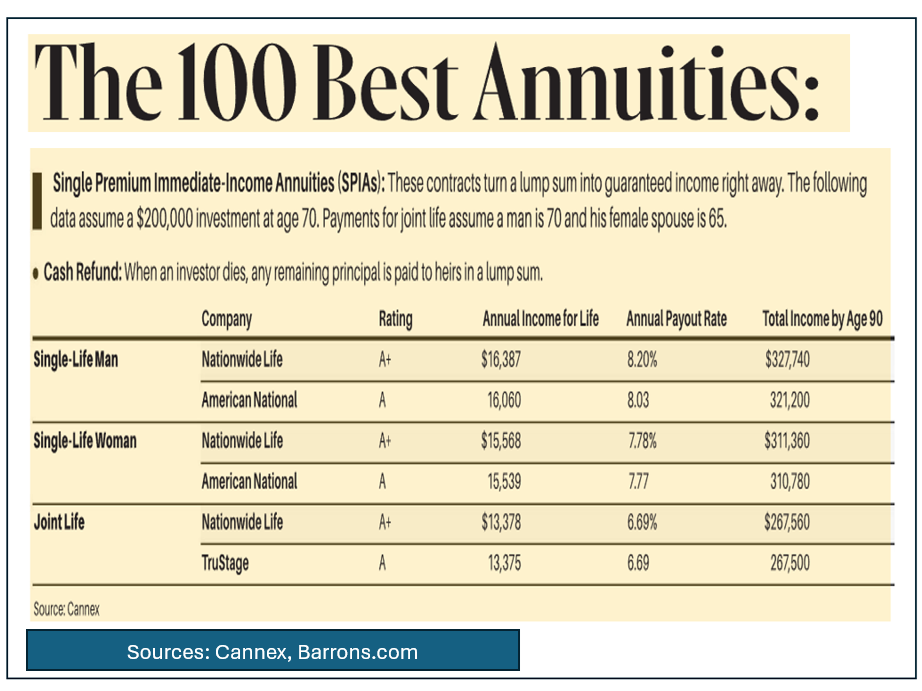

Once each year Barron’s runs a cover story titled, “The 100 Best Annuities.“

Financial advisors love to sell annuities. They pocket among the highest percentage commissions of any product they offer and often generate huge dollar payouts to the broker and firm right up front.

Better still, from the advisor’s standpoint, the buyer does not see that “hidden” commission as it is theoretically paid by the insurance company issuing the plan, rather than the customer.

Multi-year early termination fees and high annual expense ratios ensure, though, that the issuers will more than recoup the generous commissions one way or the other over time.

I am going to limit my discussion today to only the basic Single-Premium Immediate-Income product as it is the most transparent type. Deferred annuities are impossible to gauge accurately in advance due to the long lead time between purchase and the beginnings of monthly payments.

There were listed as the best single-premium immediate annuities in this issue.

All three statements are true, yet they fail to make an “apples to apples” comparison regarding the favorable income rates versus traditional income-producing vehicles.

Why do I say that?

Certificates of deposit, Treasury bills and bonds all pay coupon interest rates while promising the return of your principal upon reaching maturity.

Annuity issuers, though, will not return your principal in full. You, and your heirs, forfeit that forever as payment for the “income stream” you cannot outlive.

The one exception to that would be from the “cash refund” clause. It states that if you die before receiving back your original lump sum payment, your heirs will be made whole for any difference between cumulative benefits paid and your original purchase price.

If that occurs your start-to-finish actual net gain from inception date through your death would equal exactly 0.00%. The issuing insurance company would have had an interest-free loan of your total annuity value while you earned absolutely nothing.

Risk of not getting paid is low when dealing with highly rated issuers but can never be called zero. All annuities are only as secure as the companies standing behind them.

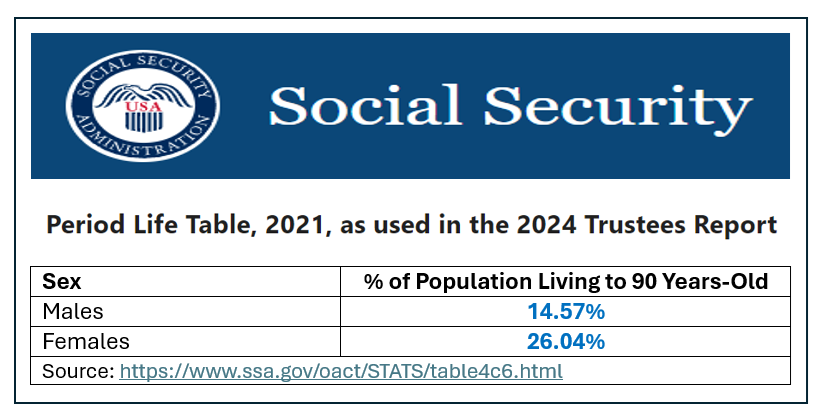

Understanding how much an annuity might pay you over time requires knowing how long the average person is likely to live.

Our Social Security department says that once you have reached 65, an average male is likely to live to about 84.3 years of age. That figure rises to 86.6 years for females.

Some people will outlive those projections, but many others will pass away before reaching those average-life expectancies.

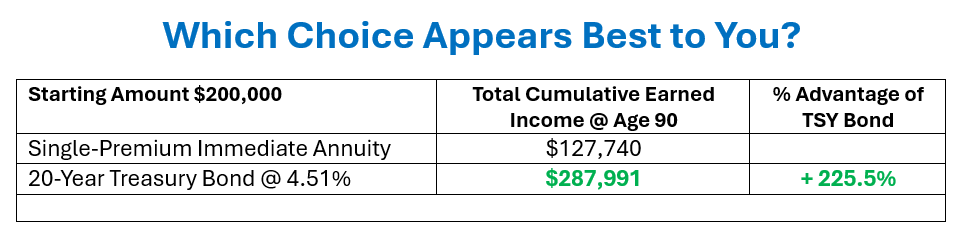

That makes the “total income by age 90” totals shown in the best annuities chart a bit disingenuous. Only a small percentage of annuity owners are likely to reach that age.

Even using that optimistic assumption, the actual percentage returns shown in that opening graphic are terrible.

A single, 70-year-old man who ponied up $200,000 to get $327,740 back would have only earned $127,740 on his original $200,000 over a full 20 years.

That translates into a puny cumulative 63.87% 20-year total return or 3.1935% annually in simple interest. That is a fraction of the 8.20% “monthly income” shown in the chart.

The low annual earnings number considers the forfeiture of the principal over the annuity example’s two-decade period.

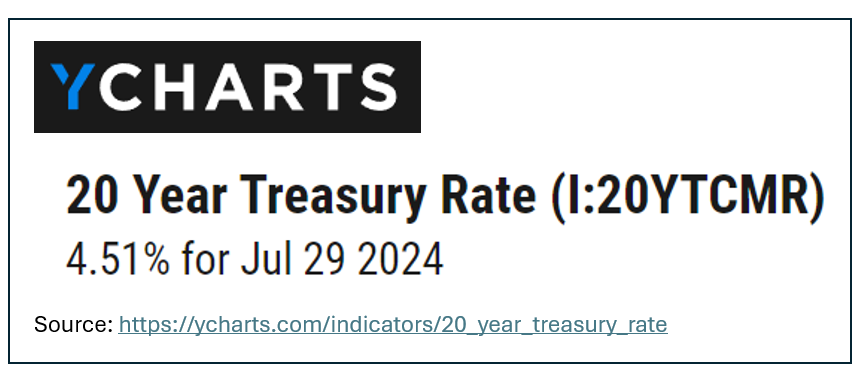

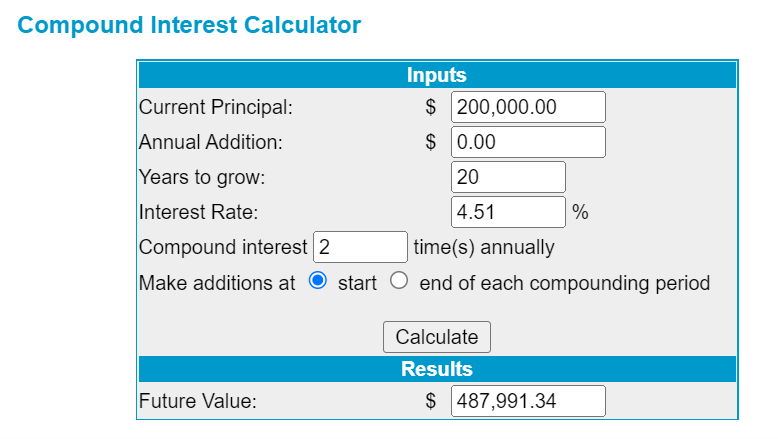

Simply putting the same $200,000 in a 20-year U.S. Treasury Bond (from age 70 to 90) would have generated $287,991 in interest plus the return of your $200,000 principal [$487,991 in total] over the same period.

Here are the two 20-year total returns side by side:

Is it any wonder that issuers are willing to pay 6% commissions to agents for selling annuities?

Our consumer protection bureau still “blesses” annuities as suitable investments for almost anybody. It even changed the rules to allow for annuities to be purchased within tax-sheltered retirement accounts.

One of the first “rules” of common-sense investing is to never put an already tax-sheltered vehicle inside another tax-shelter.

If you have already reached about 65 years of age you are probably inundated with offers for educational seminars offering fine free meals for simply listening to advice on retirement planning.

Almost every one of those will eventually be recommending purchase of annuities for at least a portion of your lifetime nest-egg.

If you go along with that advice your “free” steak or lobster dinner may become the priciest meal you ever had.

Caveat emptor.

More Paul Price:

- Short-Term Variations Make Us Crazy. They Also Create Opportunities.

- Investing Is a Marathon. Trading Is a Sprint.

- Fun Facts That Help Investors Make Money

Disclosure: I was insurance licensed in the 1980s. I never sold any annuity products.