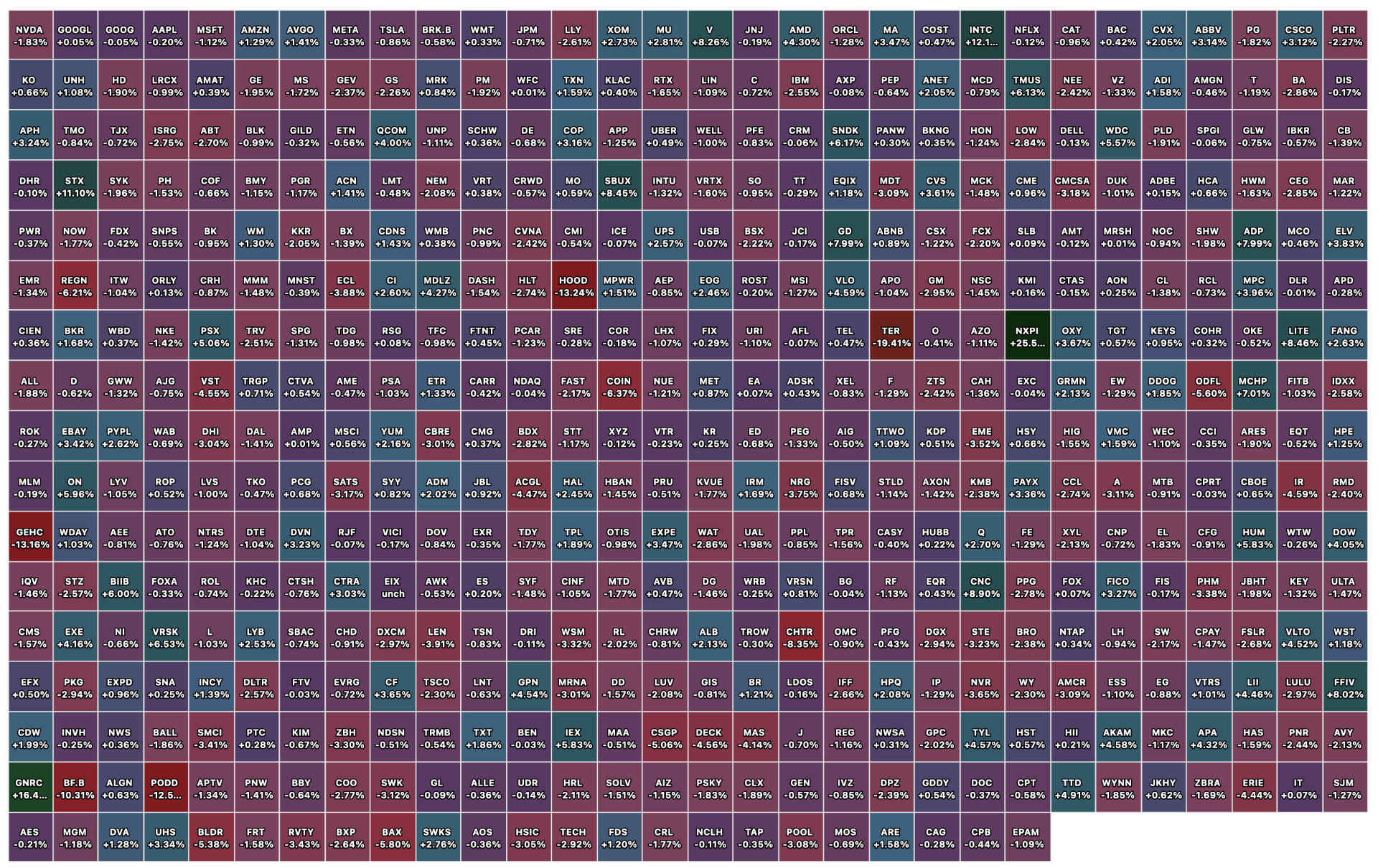

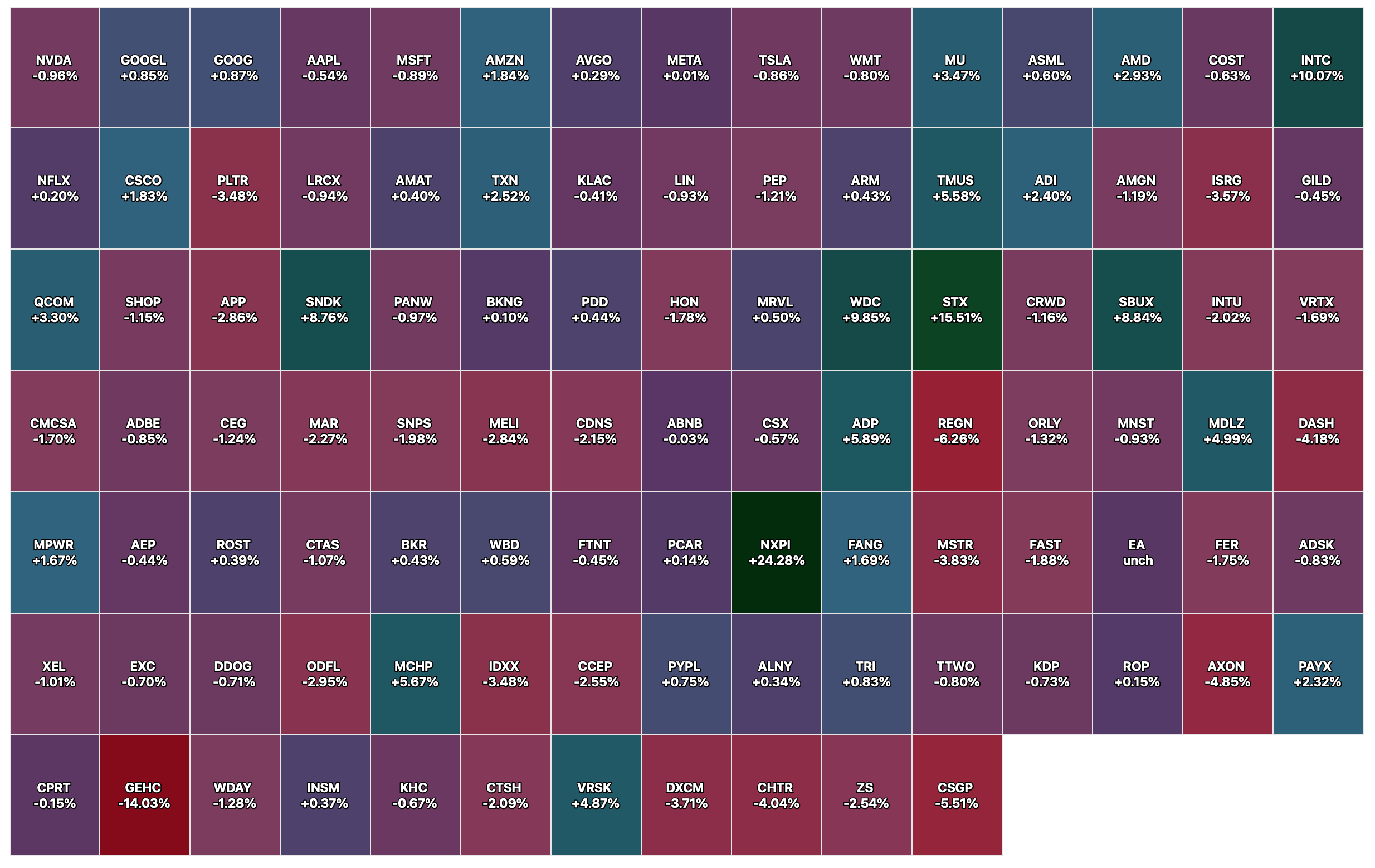

Closing S&P 500 Heat Map

BY Doug Kass · Apr 29, 2026, 4:45 PM EDT

BY Doug Kass · Apr 29, 2026, 4:45 PM EDT

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Apr 29, 2026, 4:35 PM EDT

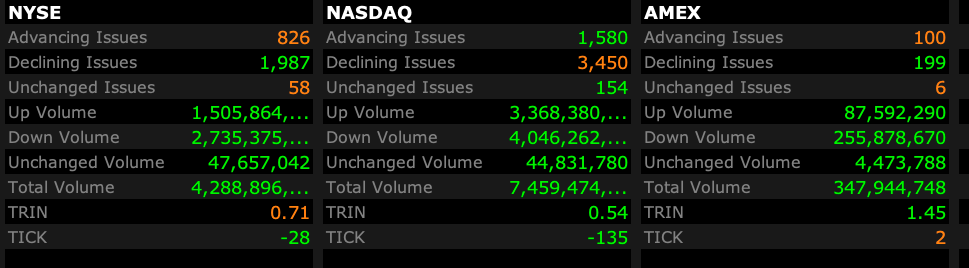

Closing Volume

- NYSE volume 4% below its one-month average;

- NASDAQ volume 11% below its one-month average;

- VIX index: up 2.58% to 18.29

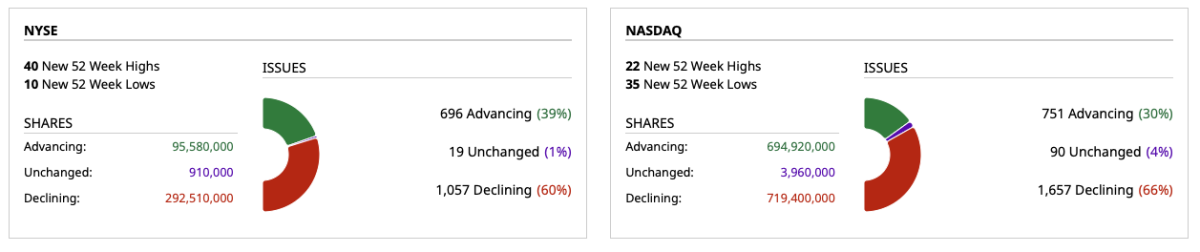

Breadth

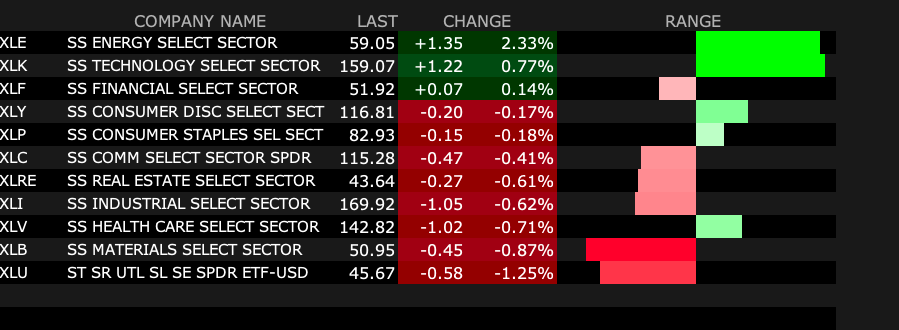

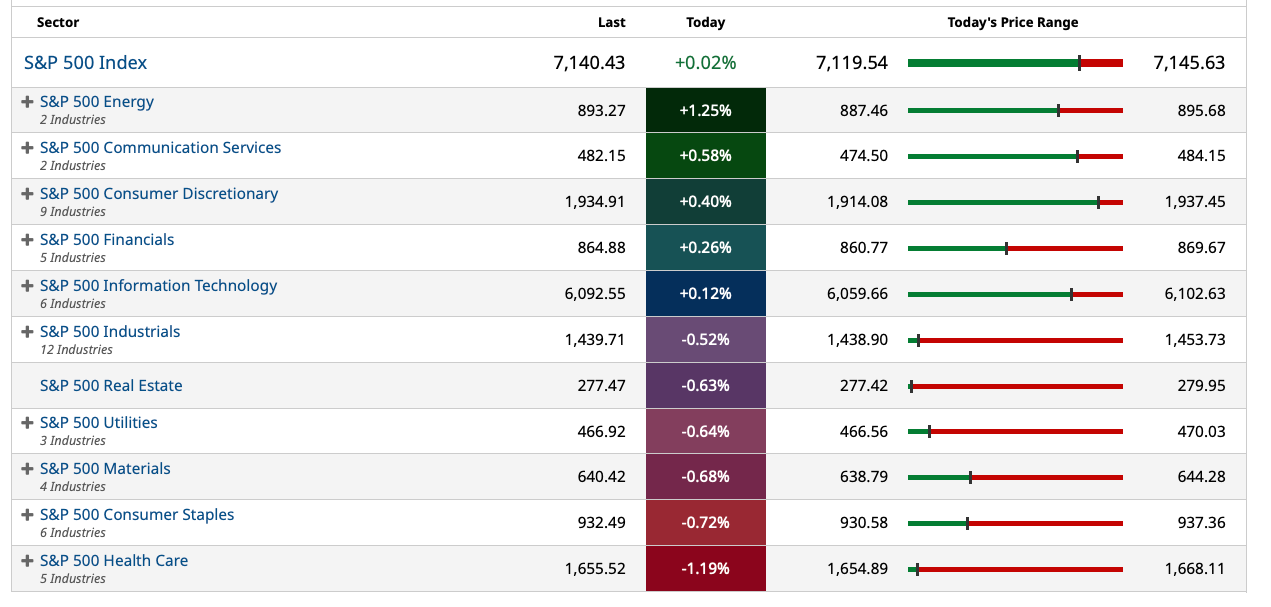

S&P 500 Sector ETFs

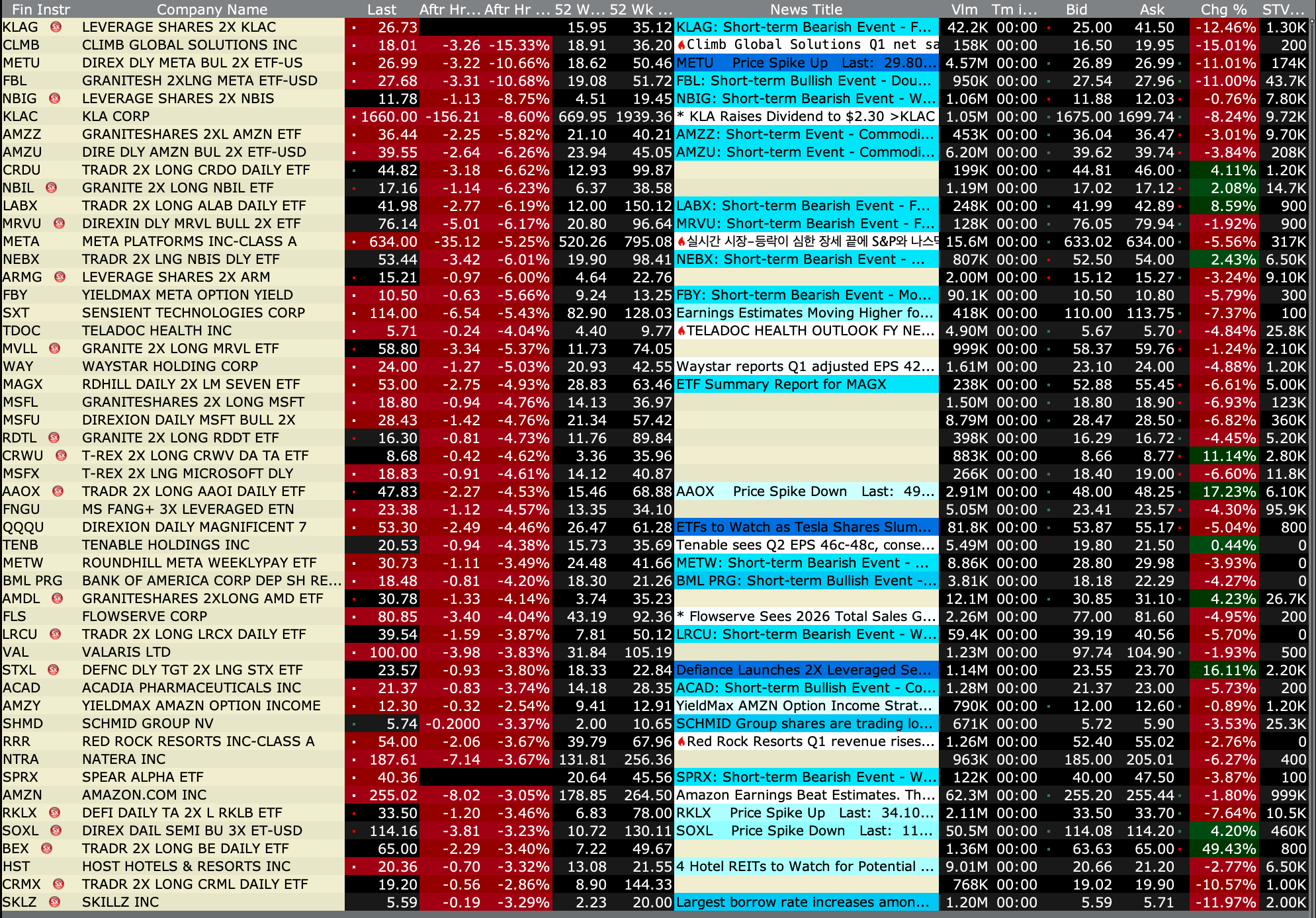

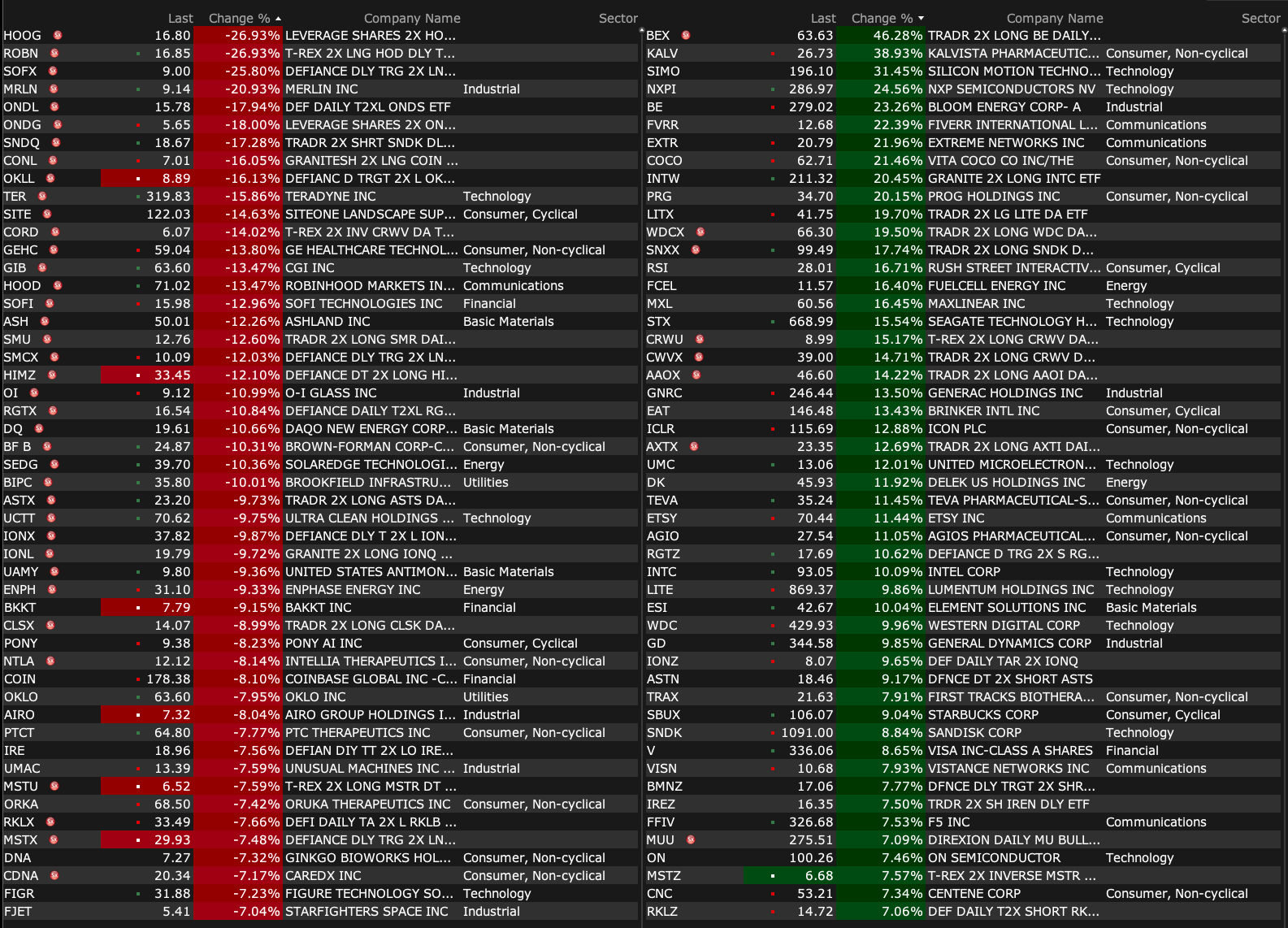

% Movers

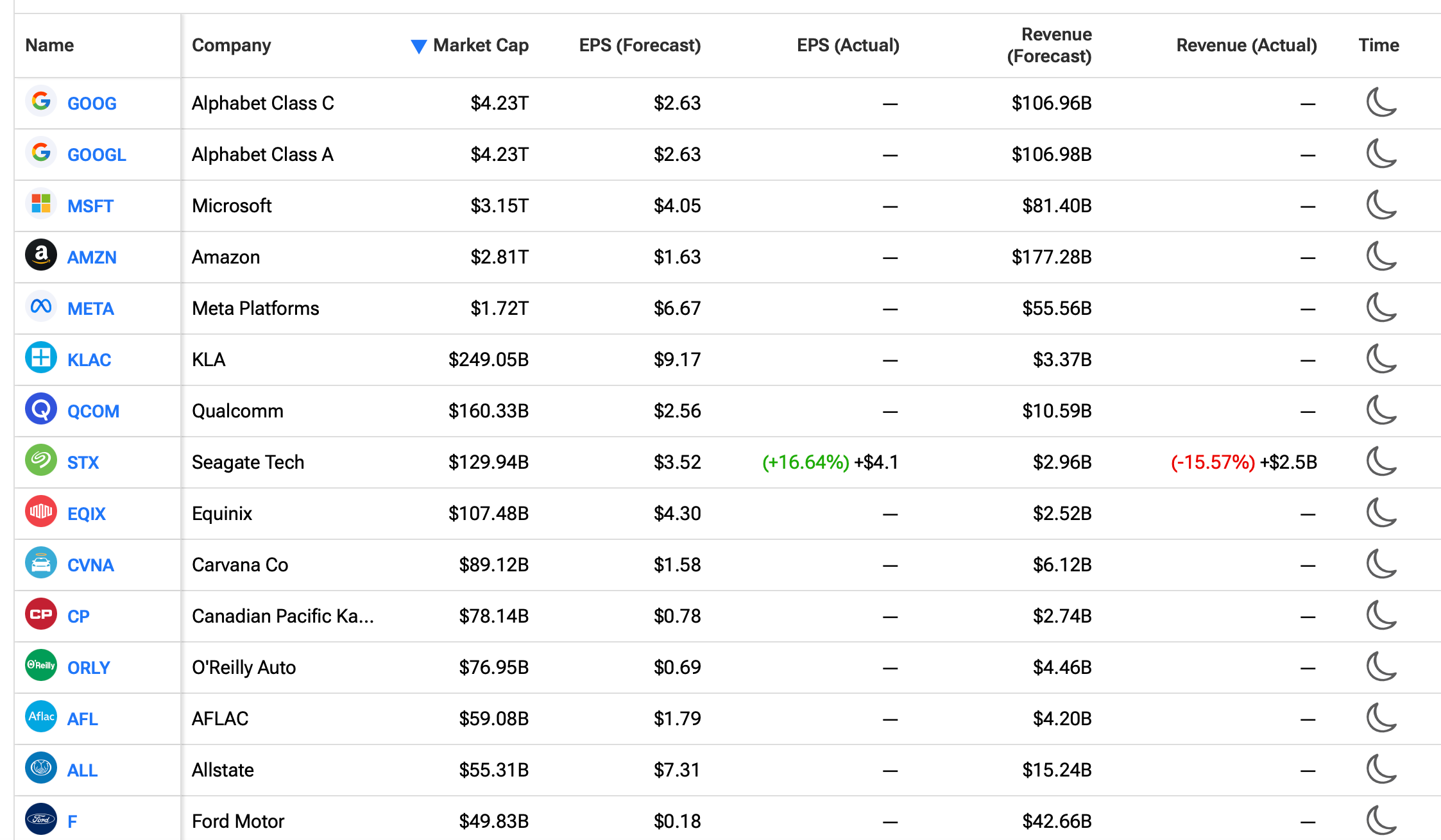

BY Doug Kass · Apr 29, 2026, 4:11 PM EDT

Please don't listen to the panelists who immediately opine on big tech EPS releases after the close without thoroughly reviewing the reports and waiting for guidance from the conference calls.

Moreover:

How can Fin TV panelists (who generally don't speak to hyperscaler managements, their competition and/or customers) be so confident about this afternoon's EPS releases?

— Dougie Kass (@DougKass)

Oh, stupid me, I know... they follow the share price action leading up to the releases.

Easy peasey. @cnbc…

BY Doug Kass · Apr 29, 2026, 4:04 PM EDT

BY Doug Kass · Apr 29, 2026, 3:15 PM EDT

Wolf Street howls about the Fed meeting.

BY Doug Kass · Apr 29, 2026, 3:05 PM EDT

From Charlie:

BY Doug Kass · Apr 29, 2026, 2:55 PM EDT

From Peter Boockvar:

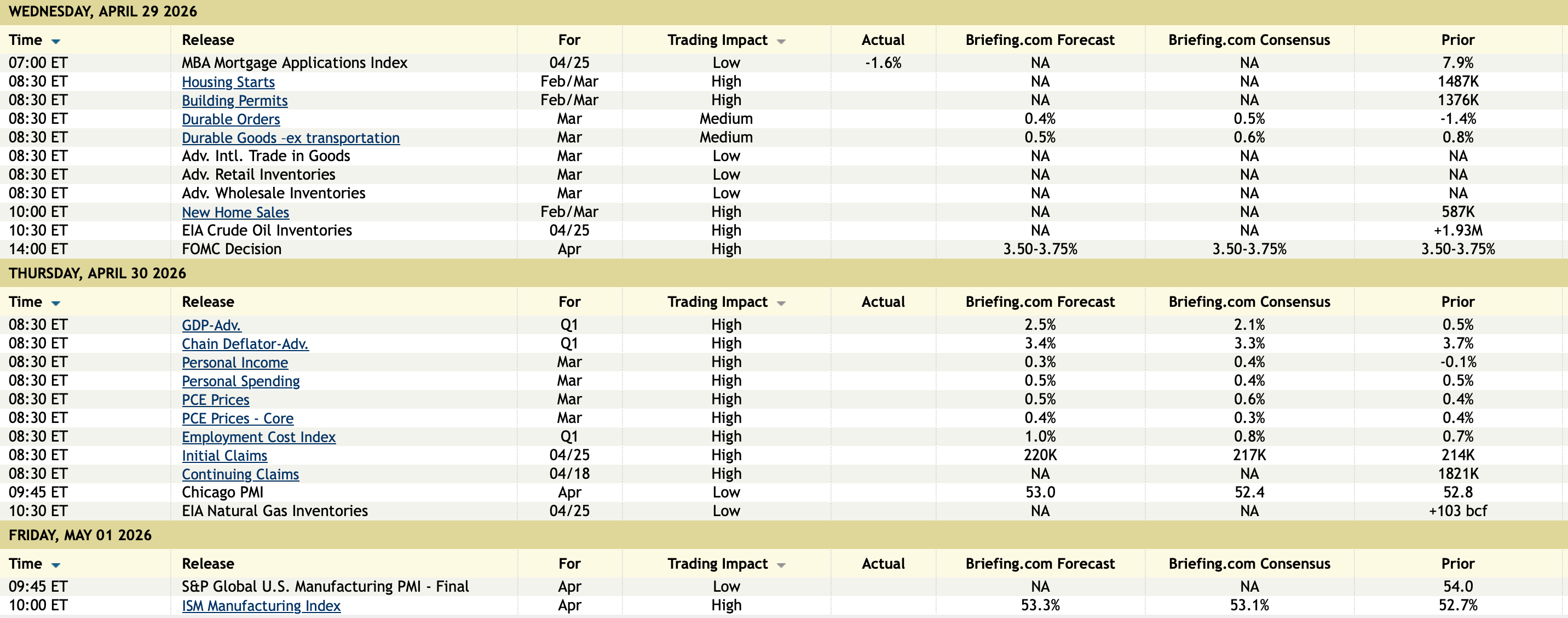

The FOMC statement was about identical to the March release but that was an issue for some members. After saying the fed funds range was left intact, this line was repeated, “In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks” and that bothered three of the members.

This sentence implies the committee is still leaning to cutting rates again but Beth Hammack, Neel Kashkari and Lorie Logan “did not support inclusion of an easing bias in the statement at this time.” Stephen Miran again wanted to cut rates, quite the look thru on higher energy prices and rising prices of other things that use it as a raw material.

The only other thing with the statement of note was a slight tweak to the inflation comment. In March they said “Inflation remains somewhat elevated.” Today they took out ‘somewhat’ and added color, “Inflation is elevated, in part reflecting the recent increase in global energy prices.”

Bottom line, we know there has been quite an internal debate on how to manage monetary policy in the current environment and the dissenters today outside of Miran, want the committee to be more neutral in its outlook with rates and not be leaning to cutting rates. I would have voted for the same thing. The world has changed over the past two months and maybe when the Strait fully reopens things go back quickly to where we stood prior to the war. Or maybe not. Why not just sit on the 50 yard line and wait to see how this concludes rather than lean in one direction?

The fed funds futures December contract is now pricing in ZERO chance of a rate cut this year.

BY Doug Kass · Apr 29, 2026, 2:40 PM EDT

If someone told me crude would be +$7.20 and bond yields would hit a new multi-month high (the long bond is closing in on 5%), I would have thought equities would be considerably lower.

And, well they might be, in the fullness of time.

BY Doug Kass · Apr 29, 2026, 2:30 PM EDT

Slugflation likely lies ahead:

The most important takeaway from the Fed decision:

— The Kobeissi Letter (@KobeissiLetter)

For months, the Fed has characterized inflation as "somewhat elevated" in their policy statements.

Today, that changed.

Amid surging energy prices, the Fed now says inflation "is elevated."

The Fed says inflation is back. pic.twitter.com/NuBI0fiLAJ

BY Doug Kass · Apr 29, 2026, 2:19 PM EDT

I was long Pershing Square (PSUS) at $40.70. Then I sold PSUS at $42.46.

Position: None

BY Doug Kass · Apr 29, 2026, 2:12 PM EDT

I have added to the following shorts: (BXMT) , (CHGG) , (CZR) , (GRNY) , (JOET) , (MGM) , (MPTI) , (RICK) , (SNBR) , (WGO) and (WYNN) .

New shorts: (FIGS) , (CAT) , (COST) , (CVNA) and (WMT) .

Position: Short all the above

BY Doug Kass · Apr 29, 2026, 2:07 PM EDT

BY Doug Kass · Apr 29, 2026, 1:55 PM EDT

Here are today's things:

* Shorted (AMD) at $332.02, (INTC) at $92.84, and (MU) at $521.59.

*Added to longs (KMB) at $96.77, (PEP) at $153.59 and (PG) at $146.37.

Position: Long KMB (VS), PEP (VS), PG (VS); Short AMD (VS), INTC (VS), MU (VS)

BY Doug Kass · Apr 29, 2026, 1:45 PM EDT

I am short Intel (INTC) :

Intel is such a horse. I have NO bear case

— Jim Cramer (@jimcramer)

Position: Short INTC (S)

BY Doug Kass · Apr 29, 2026, 1:35 PM EDT

PAUL TUDOR JONES ON BUYING THE S&P 500 RIGHT NOW:

— Sam Badawi (@Sam_Badawi)

"If you buy the S&P at this current valuation, the 10-year forward returns are negative when you buy with the S&P P/E of 22. That's what history shows."

Jones called the 1987 crash before it happened. He's not predicting a… pic.twitter.com/Sz7awktBny

BY Doug Kass · Apr 29, 2026, 1:30 PM EDT

How can Fin TV panelists (who generally don't speak to hyperscaler managements, their competition and/or customers) be so confident about this afternoon's EPS releases?

— Dougie Kass (@DougKass)

Oh, stupid me, I know... they follow the share price action leading up to the releases.

Easy peasey. @cnbc…

BY Doug Kass · Apr 29, 2026, 1:18 PM EDT

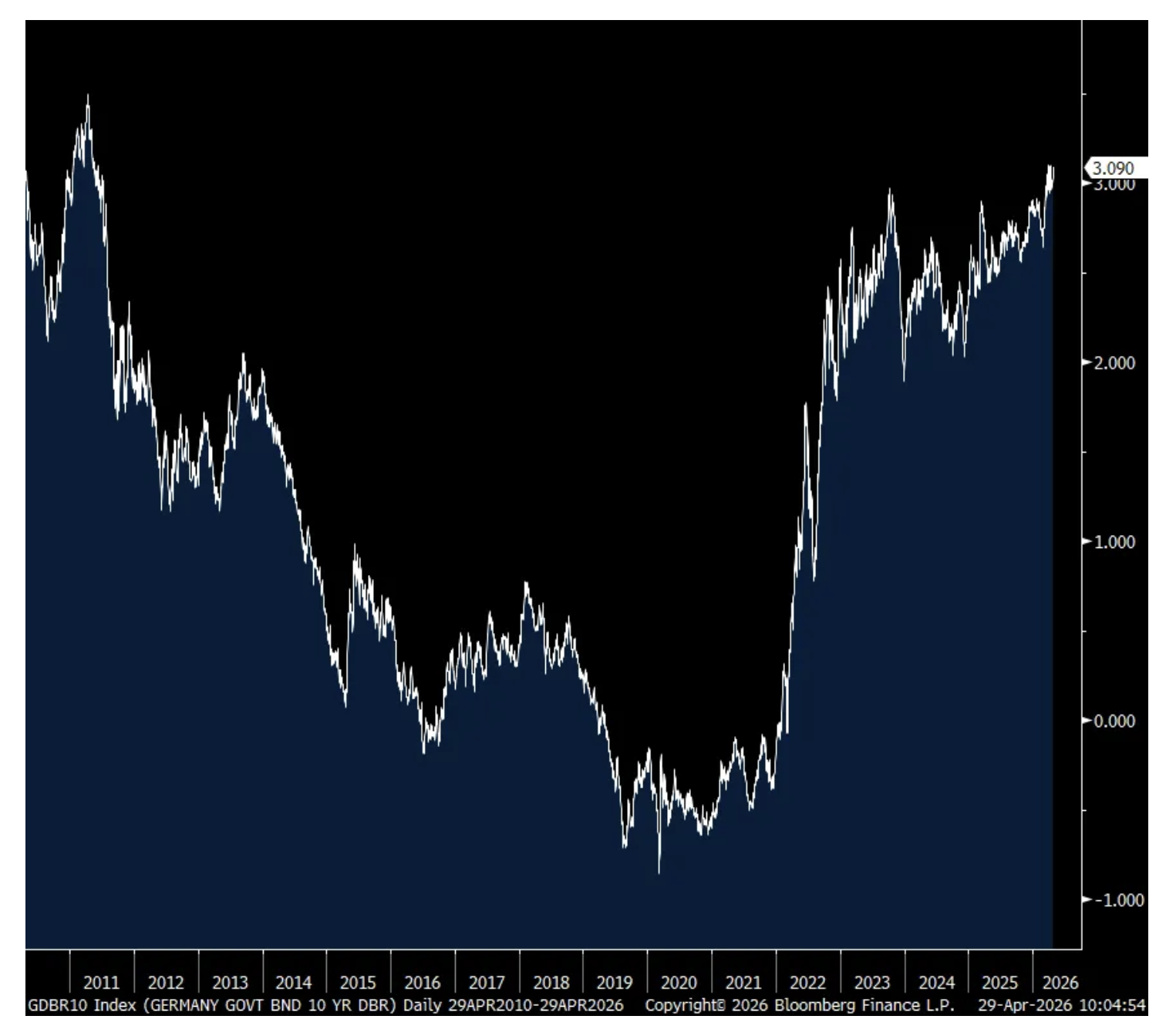

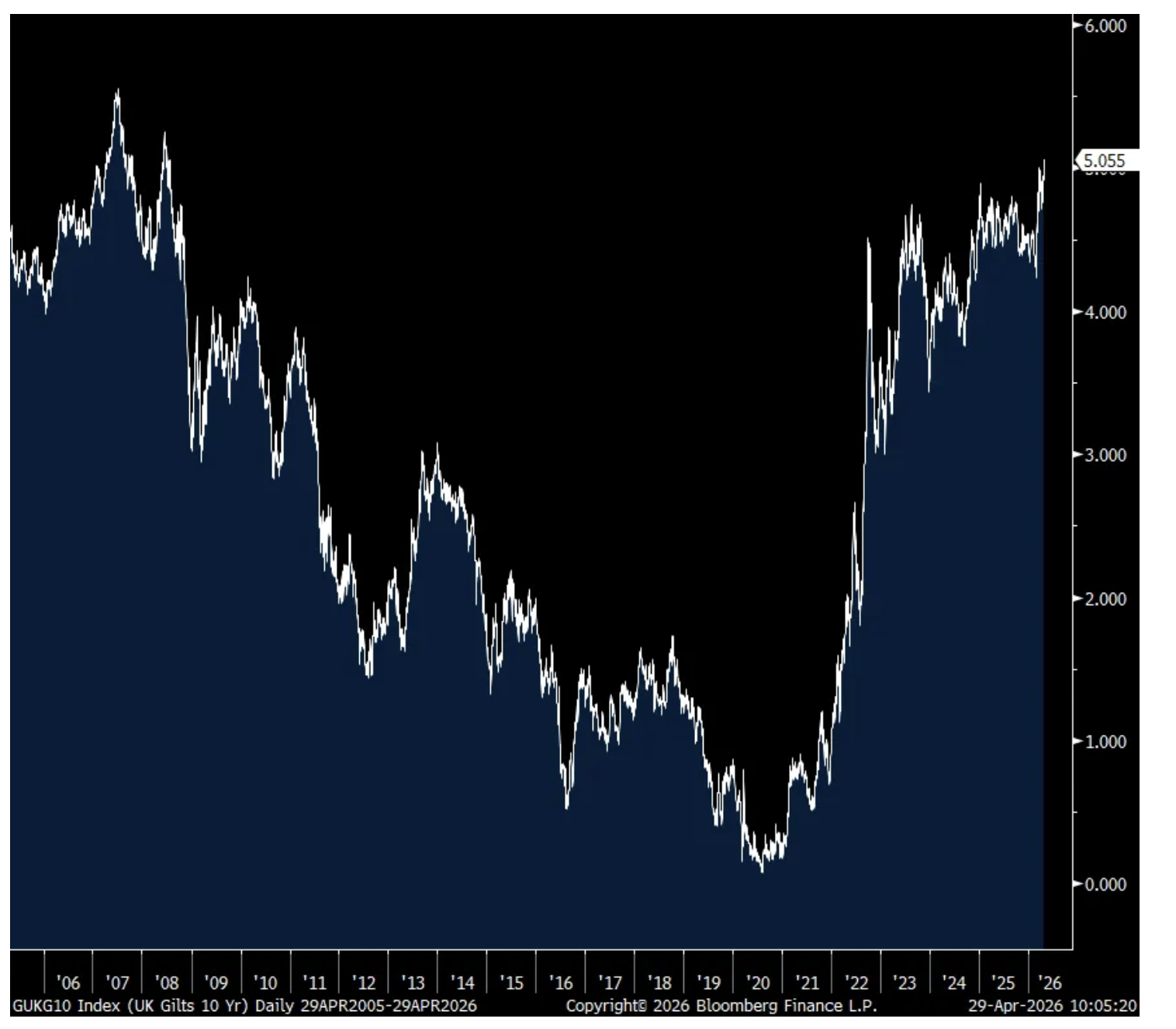

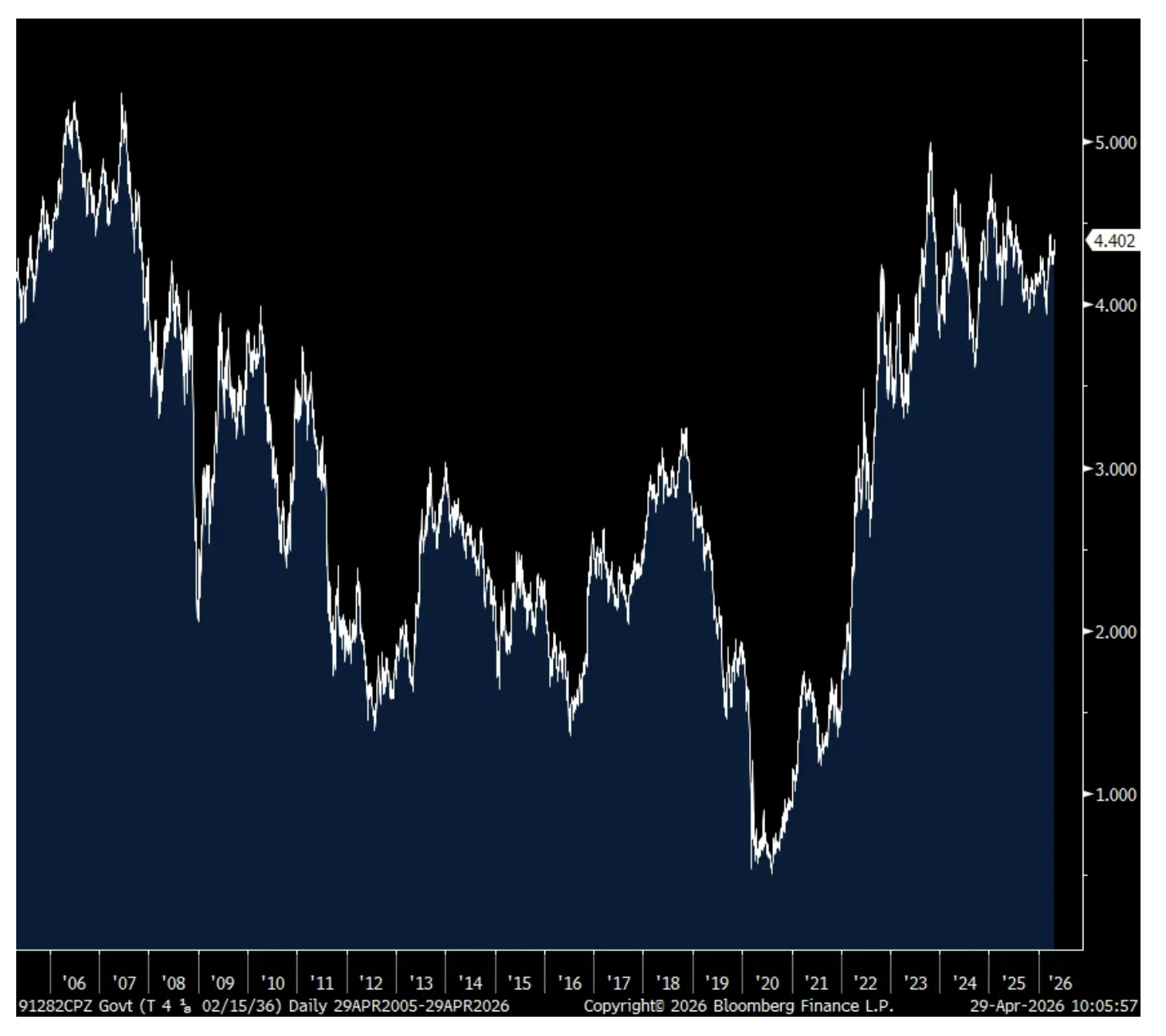

From Peter Boockvar:

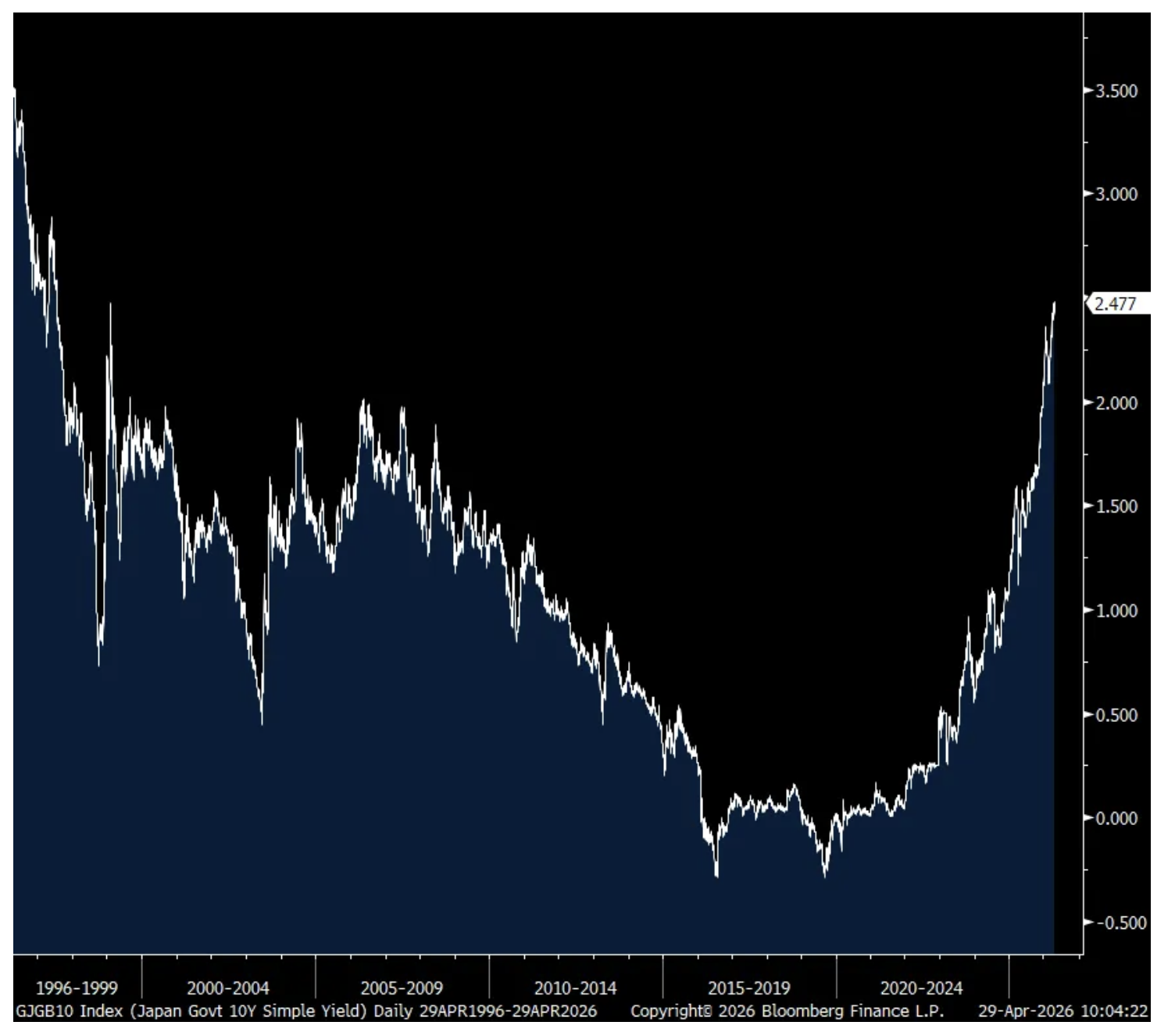

As the US 10 yr yield is now touching 4.40%, the 10 yr JGB yield closed overnight at a 29 yr high, the German 10 yr yield is at a 15 yr high, and the 10 yr UK yield is at an 18 yr high. Debts and deficits matter and inflation still does too.

JGB 10 yr yield

Bund 10 yr yield

Gilt 10 yr yield

US 10 yr yield

BY Doug Kass · Apr 29, 2026, 11:55 AM EDT

- NYSE volume 4% below its one-month average;

- Nasdaq volume 8% below its one-month average;

- VIX index: up 1.35% to 18.07

Positions: None

BY Doug Kass · Apr 29, 2026, 11:31 AM EDT

From Peter Boockvar:

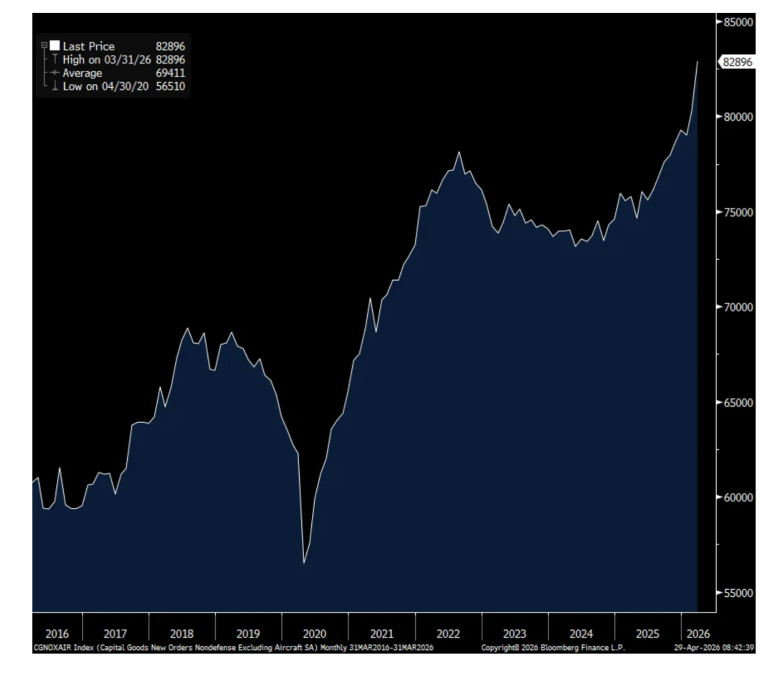

Non defense capital goods orders ex aircraft in March blew away expectations with a 3.3% m/o/m increase after a 1.6% gain in February (revised up from .7%).

I believe we can ascribe two reasons for the strength, data center construction and the reaction on the part of procurement officers to front load ordering with the new reality of the closure of the Hormuz Strait.

To the former specifically, orders for computers/electronics jumped by 3.7% in the month after a 1.3% rise in February and they are now up 14% y/o/y with particular strength in communications equipment. Orders for electrical equipment were higher by .7% m/o/m and 7.3% y/o/y and with machinery, orders increased by .8% m/o/m and 12.3% y/o/y. Metals, needed for the data center buildout, saw orders rise for both primary and fabricated. Outside of the core read, orders for vehicles/parts were up by 1.2% m/o/m.

Bottom line, thanks to the building of data centers, as said, durable goods orders have finally broken out of a multi year period of consolidation. Also as said, we are definitely seeing a pull forward of ordering and a restocking of inventories because no company is going to want to be caught short of anything.

Core Durable Goods Orders in absolute, nominal dollars

Positions: None.

BY Doug Kass · Apr 29, 2026, 11:20 AM EDT

Back shorting the overbought (absurdly high RSI) in large cap tech (with a tight stop):

* (INTC) $92.84

Positions: Short INTC VS MU VS AMD VS

BY Doug Kass · Apr 29, 2026, 11:13 AM EDT

Adding to consumer staples longs (on weakness):

* (PG) $146.37

* (PEP) $153.59

* (KMB) $96.77

Positions: Long PG S PEP S KMB S

BY Doug Kass · Apr 29, 2026, 11:05 AM EDT

In the current period when "nothing really matters" to equities, I strongly suggest tuning into MRKT CALL with Carter, Guy and Dan at 11 a.m. ET daily.

On MRKT CALL you will find uncensored (and even sometimes humorous) discussions and strategy and how to make money in a market when, arguably, others are losing their minds!

You might even get a discussion and debate on some of the observations I am making on TheStreetPro.

Chair Powell's Final Fed Meeting + Big Tech Earnings On Deck | Wednesday, April 29th

Positions: None.

BY Doug Kass · Apr 29, 2026, 10:55 AM EDT

From Peter Boockvar:

Outside of this being Jay Powell’s encore performance before he exits stage left, most likely, I expect today’s FOMC statement and presser to be as boring as possible as Powell & Co are left with no choice but to play spectator right now to global events.

Before I get to some earnings info, companies are passing on price increases to mitigate their own cost pressures. On Monday I read on Bloomberg News that “BASF is raising prices on plastic protecting chemicals, commonly used in the car and consumer goods industries, for a second time since the start of the Iran conflict in February. The German manufacturer’s customers will see prices go up by an additional 25% on products in its antioxidant, process stabilizer and light stabilizer portfolio for plastic applications, BASF said on Monday. The increase comes on top of a 20% hike announced on March 4 and is effective immediately.”

Paper stocks rallied yesterday after Citi said Smurfit Westrock was raising prices of containerboard by $50 per ton starting June 1. Prices currently run between $900 and $1000. This follows already a previous $50 per ton rise year to date.

So many earnings calls to go through.

From Kimberly Clark, a stock little changed yesterday, one of the consumer staples stocks we own with the group being one of my favorites right now and I stand very much alone on that:

“We aren’t really seeing any large scale shifts in consumer buying behavior. And we are still seeing consumers under pressure, but that’s not a new dynamic.”

“In terms of the good, better, best question, I would say the premium side of the business remains healthy and is continuing to grow and it’s the key to category growth. The consumers with higher incomes have remained resilient. And then on the good and the better, we’re not seeing any specific patterns. I think what it comes down to is the strength of the value proposition within the tiers. And that really is what’s winning. I think consumers are getting more choiceful for their money.”

As to how much higher oil prices are impacting their COGS, “If oil prices were to persist at the $100 per barrel level for the duration of the second half, we could see additional gross input cost inflation in the range of $150-$170 million. While this is not built into the outlook we’re providing today, we’re proactively evaluating levers available to mitigate any potential impact.”

This was interesting on South Korea, a country that has the worst birth rate in the developed world but improving and where Kimberly Clark benefits from their diaper business, “in developed Asian markets like Korea, we’re seeing a baby boom. And so I think births were up 6.5% last year in 2025. And so the category was up 20% in Korea, where we have over 60% share.”

Hilton fell 3% yesterday and said this of note:

“For the first quarter, system wide RevPAR increased 3.6% y/o/y, driven by broad based growth across all chain scales, brands and segments, as well as sequential monthly improvement throughout the quarter in the US.”

Business transient RevPAR was up 2.7%, “representing a four point step up in demand from the fourth quarter when adjusting for day of week and holiday shifts, driven by improving midweek demand across all chain scales.”

Leisure transient RevvPAR was higher by 3.5%, “driven by concentrated spring break demand that enabled strong rate growth.”

Group RevPAR was up 4.3%, “driven by growth in company meeting and convention demand. We continue to see healthy underlying momentum for group, supported by strong growth in corporate lead volumes.”

“As we look ahead to the second quarter, we remain encouraged by a continuation of demand trends that we’ve been observing since late 2025 and now through April, but we do expect some headwinds related to the Middle East.”

“For the full year, we expect improving performance in the lower and mid-chain scales with RevPAR strength continuing to move downstream from luxury and upper upscale toward a more balanced convergence demand shape, or what I have been calling a C-shaped economy.”

More on travel from Booking Holdings which is trading down pre-market:

“In the first quarter, our business was impacted by the ongoing situation in the Middle East, which led to elevated cancellations and a moderation in new bookings in March. The impact of the conflict was also felt outside the Middle East region as we saw changes in broader travel patterns, particularly in transit corridors such as the one between Europe and Asia.”

“I am pleased to report that our US room night growth accelerated for the fourth consecutive quarter to the low teens, driven primarily by strong domestic demand...Furthermore, we saw strength in the US, not only in accommodations, but across flights, cars and packages.”

“In Asia, we continue to see one of the most compelling structural growth opportunities in the global travel industry.” I’ll add, the growing middle class in Asia is a very exciting growth story.

From Coca Cola, another consumer staple stock we own and which rose by 4% yesterday:

“During the quarter, the external environment differed greatly across our markets. While many consumers remain resilient, others are under pressure due to persistent inflation, greater macroeconomic uncertainty, and volatility driven by the conflict in the Middle East.”

Specifically in North America, “While we benefited from slightly an easier comparison versus the prior year, we delivered solid performance. We gained both volume and value share, and grew volume, revenue and profit.”

“In Europe, despite a cautious consumer environment, we gained value share.”

“In Eurasia and the Middle East, we gained better share. While we grew volume for the quarter, our volume declined in March after the onset of the conflict.”

“In Asia-Pacific, we grew volume across all operating units despite cycling a strong comparison versus the prior year. We also grew revenue, but profit declined, driven by commodities headwinds in tea and coffee, and phasing of inventory costs.”

From Starbucks and whose stock is up pre-market:

Global comps rose 6%, “driven by terrific performance across the business, especially in the US.”

“Positive comp trends have continued through April, and this gives us the confidence to take up our fiscal 2026 guidance for global comp growth to 5% or better...We believe this quarter reflects the turn in our turnaround.”

“Our US company operated business grew transactions across all day parts, with mornings now roughly back to fiscal 2022 levels, and we saw broad based spend growth across all income levels and age demographics. Our delivery business also contributed both comp ticket and transaction growth in the quarter.”

“International comp sales grew 2.6%, once again led by transactions, which were up over 2% in the quarter...all 10 of our largest international markets, including China, Japan, South Korea, and Mexico, delivered positive comps for the first time in 9 quarters.”

With respect to the outlook, “Customer demand trends in our business remain strong today, and while history demonstrates the resilience of our brand through periods of high gas prices, the current macro environment brings heightened uncertainty to our operating landscape and consumer behavior more broadly. Our comp guidance accounts for these considerations.”

Also on the food side, Sysco the distributor fell 2.6% yesterday and said this of note:

“Overall foot traffic to restaurants remains challenged, and Sysco is improving our performance due to selling initiatives within our direct control...Per Black Box, traffic to restaurants was down approximately 1.9% in the quarter.”

Visa is popping pre-market and they certainly benefit from inflation as they live in a nominal world and also from the shift to digital payments from cash. They said this:

“US payments volume grew 8% y/o/y, up almost 1.5 from Q1, reflecting resilience in consumer spending, e-commerce spend outpaced face-to-face spend. Both US credit and debit demonstrated broad based spend improvement, and we believe both were helped, in part, by higher tax refunds.”

“Growth across consumer spend bands saw incremental improvement from Q1, with the highest spend band continuing to grow the fastest. Across our volume, both discretionary and non-discretionary spend remained strong. We do not see signs of the lower spend consumer weakening in our volumes.”

“our cross border business is very resilient. It’s well distributed. And while there is some impact in the Middle East, as we saw in Q2, and we do expect to see in Q3, we’ve seen that there’s offsetting factors, strength in other regions, other parts of the business. For example, we’re expecting an increase in inbound volumes in the US and Latin America, given the enthusiasm for the upcoming World Cup.”

On the big ticket spend of an automobile, Asbury Auto Group, a dealership company, said this:

“Our results reflect the expected decrease in volumes as consumer demand moderated from last year’s tariff driven spike in sales. More challenging weather was also a factor.”

“Parts and service had a more challenging quarter, driven by a variety of factors including weather and a more cautious consumer.”

Any customer buying changes in light of higher gasoline prices? “From a mix, typically when you see gas prices hit the levels where we are right now, it usually takes 5 to 6 months for consumers to start really changing their buying habits. We have not seen that. And what I mean by that is a consumer that is going to trade in a Chevy Tahoe for a Honda Civic or what have you, we have not seen that, but the longer the war goes, I think the closer we’re going to be getting to see a shift in consumer behavior, but we’re not there yet.”

“And from a used car standpoint, the demand for used cars is there, especially with the difference in the cost of sale between a new and used car. When you factor in all the items that have gone up, insurance rates, the average cost of maintaining a car, when you look at all that, the demand is definitely there for used cars.”

Lastly from UPS whose stock fell 4% yesterday and they said this:

“As we look to the balance of the year, there are a few external factors that we are watching that could impact demand, especially higher fuel costs stemming from the conflict in the Middle East and US consumer confidence, which is at historic lows.”

“For the quarter, total US average daily volume was down 8% versus the first quarter of last year. Nearly two-thirds of the decline came from the glide down of Amazon volume and our deliberate actions to remove lower yielding e-commerce volume from our network.”

“Moving to the customer mix, SMB average daily volume increased 1.6% y/o/y, driven by high-tech, healthcare, and automotive customers.”

With respect to higher fuel costs, they recapture it via fuel surcharges to the customers. Also, “If you look at our exposure in the Middle East, it’s pretty small.”

To some economic data, mortgage applications were little changed w/o/w, down 1.6% weighed down by a 4.4% drop in refi’s while purchases rose 1.2%. Mortgage rates were little changed on the week but likely higher next week with this move up in the 10 yr yield.

Australian bond yields are falling after an in line March CPI report as the trimmed mean rose 3.3% y/o/y, the same pace seen in February.

In Europe, Spanish CPI in April rose 3.5% y/o/y, one tenth more than expected and Spanish yields are up slightly in response.

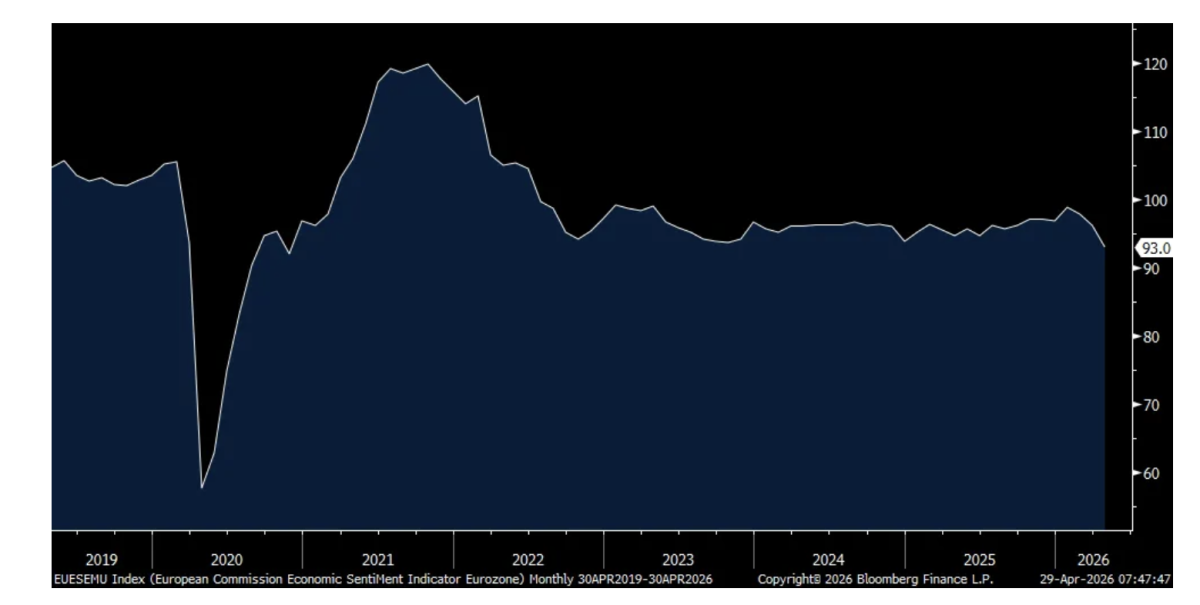

Finally, the April European Economic Confidence index fell to 93 from 96.2, the weakest since November 2020. Declines were across the board m/o/m, in manufacturing, services, consumer, retail and construction. I guess not a surprise.

Europe Economic Confidence

Positions: None.

BY Doug Kass · Apr 29, 2026, 10:25 AM EDT

I am not sure what surprises me more -- that crude is +$5/barrel or that equities are non plussed by the climb in the price of oil.

The argument being made is that the consumers' exposure to higher gasoline prices is far below what it has been historically.

That, however, neglects to discuss the impact of materials and goods that are influenced meaningfully by higher energy costs.

Positions: None.

BY Doug Kass · Apr 29, 2026, 10:15 AM EDT

(SOFI) and (HOOD) results should place a pall over money center banks and brokerage stocks today.

I am not sure, but I should be (as I recently observed a possible double top in BKX).

Positions: None.

BY Doug Kass · Apr 29, 2026, 9:59 AM EDT

No trades (yet) today...

Positions: None.

BY Doug Kass · Apr 29, 2026, 9:50 AM EDT

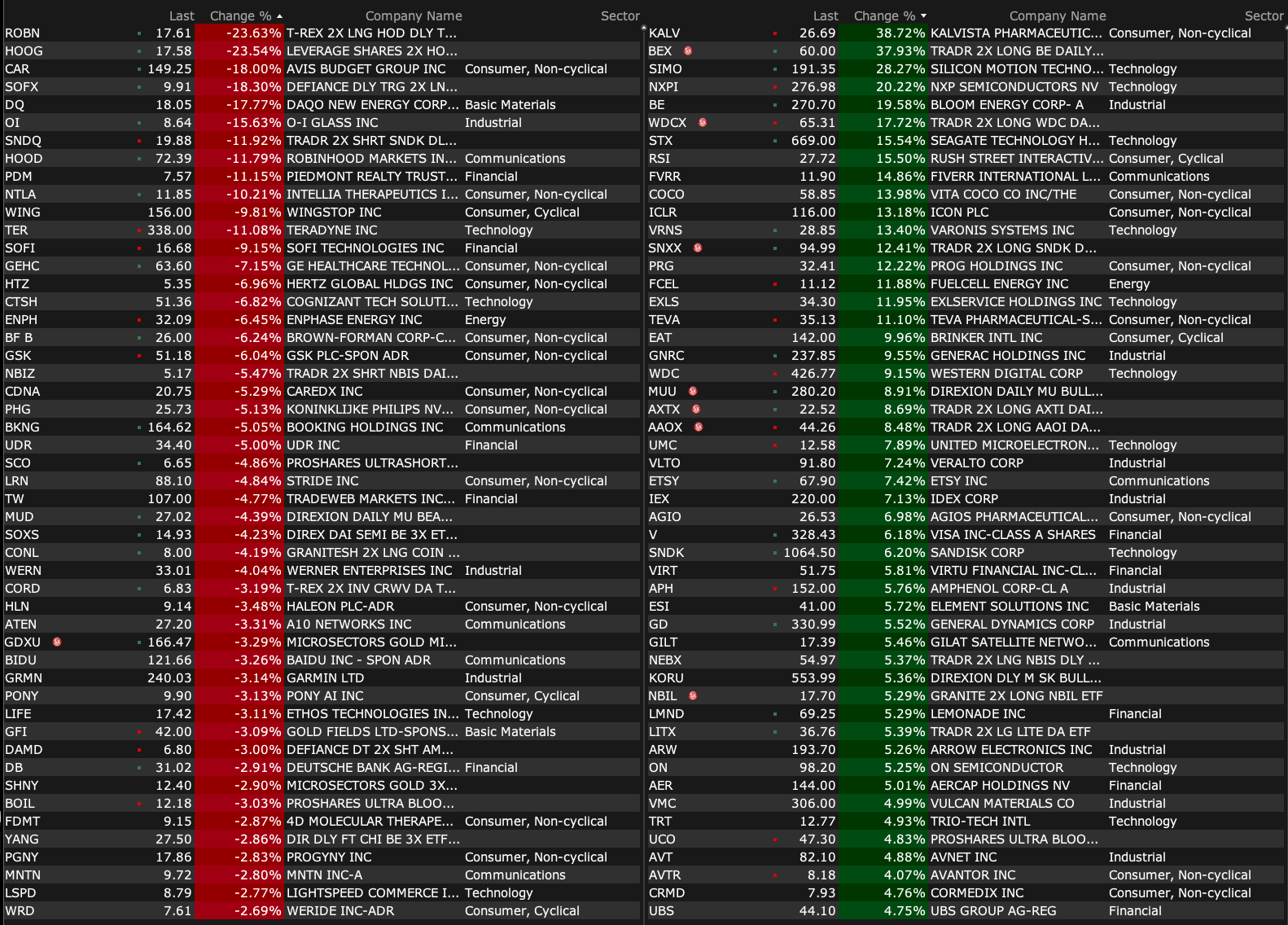

-KALV +39% (to be acquired by Chiesi Farmaceutici SpA at $27.00/shr in cash in ~$1.9B deal)

-PRCH +20% (earnings, guidance)

-BE +17% (earnings, guidance)

-COCO +16% (earnings, guidance)

-ICLR +15% (audit committee completes accounting investigation; to restate 2023,2024, part of 2025 results)

-RSI +15% (earnings, guidance)

-STX +15% (earnings, guidance)

-FSS +13% (earnings, guidance)

-VRNS +13% (earnings, guidance)

-TEVA +9.3% (earnings, guidance)

-GNRC +8.6% (earnings, guidance)

-FICO +8.4% (earnings, guidance)

-APH +7.8% (earnings, guidance)

-GD +7.4% (earnings, color)

-ETSY +7.0% (earnings, guidance)

-VIRT +5.8% (earnings, color)

-V +5.6% (earnings, color)

-GILT +5.1% (awarded order for over $7M through prime contractor to support U.S. Department of War for Wavestream EnduroStream SSPA solution)

-VMC +5.0% (earnings, guidance)

-LMND +4.7% (earnings, guidance)

-SBUX +4.5% (earnings, guidance)

-ADP +4.1% (earnings, guidance)

-SMG +3.2% (earnings, guidance)

-MDLZ +2.3% (earnings, guidance)

-CAR -19% (earnings, color)

-HOOD -12% (earnings, color)

-TER -9.5% (earnings, guidance)

-WING -8.7% (earnings, guidance)

-SOFI -8.2% (earnings, guidance)

-ENPH -8.0% (earnings, guidance)

-GEHC -6.6% (earnings, guidance)

-BF.B -6.3% (Pernod Ricard ends merger talks with Brown-Forman)

-BKNG -4.2% (earnings, guidance)

-HUM -2.1% (earnings, guidance)

Positions: None.

BY Doug Kass · Apr 29, 2026, 9:25 AM EDT

Positions: None.

BY Doug Kass · Apr 29, 2026, 9:09 AM EDT

Positions: None.

BY Doug Kass · Apr 29, 2026, 8:55 AM EDT

11:30 a.m.: Treasury hosts a $69B 17-Week Bill Auction

Positions: None.

BY Doug Kass · Apr 29, 2026, 8:41 AM EDT

BY Doug Kass · Apr 29, 2026, 8:25 AM EDT

BY Doug Kass · Apr 29, 2026, 8:00 AM EDT

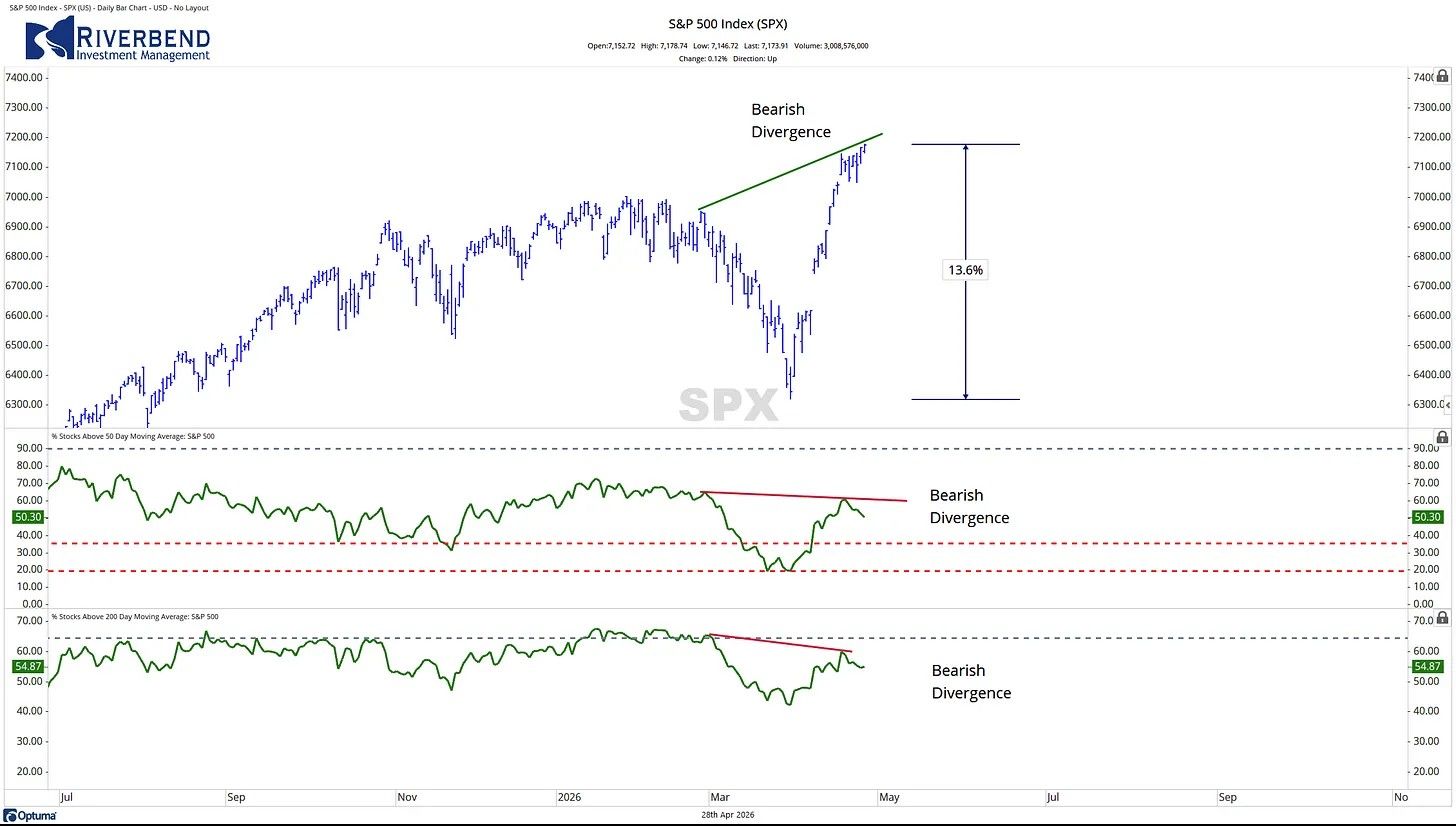

While investors/machines cheer the multi-week rally — and ignore higher inflation/interest rates/price of oil, plummeting confidence reads, the lack of fiscal discipline (manifested in a continued rise in the deficit and the aggregate U.S. debt load), still elevated valuations, improvisational policy in Washington D.C., bonafide questions regarding AI capital spending (and their anticipated returns etc.) — there are some signs of internal market weakness.

Specifically, fewer stocks are providing leadership. Here are three examples of the narrowing:

* The number of stocks above their respective 50-day and 200-day moving averages is declining while the index continues to rise.

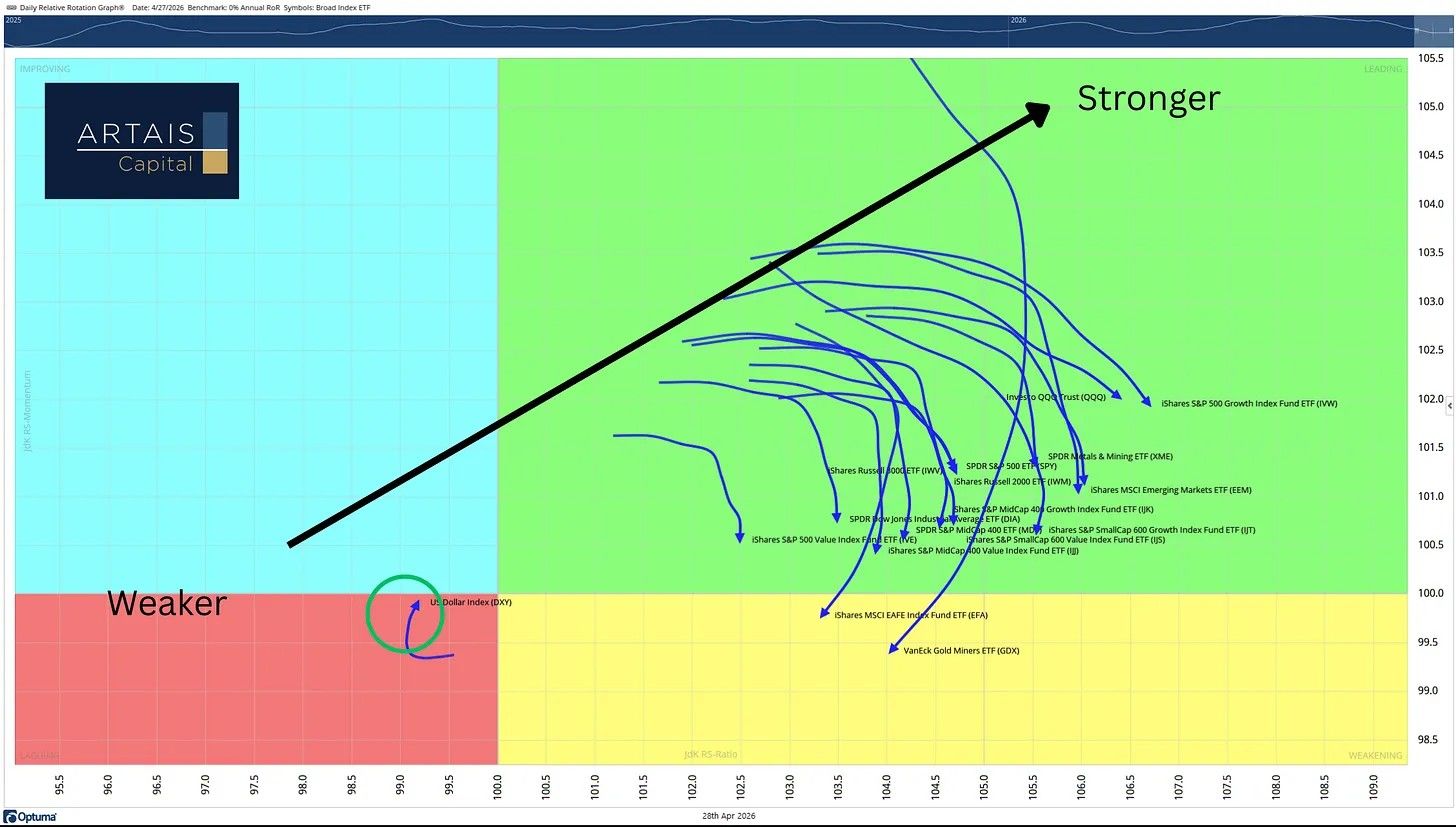

*Large-cap, mid-cap, and small-cap stocks are all rotating towards the “weakening” quadrant, indicating a loss of upside momentum:

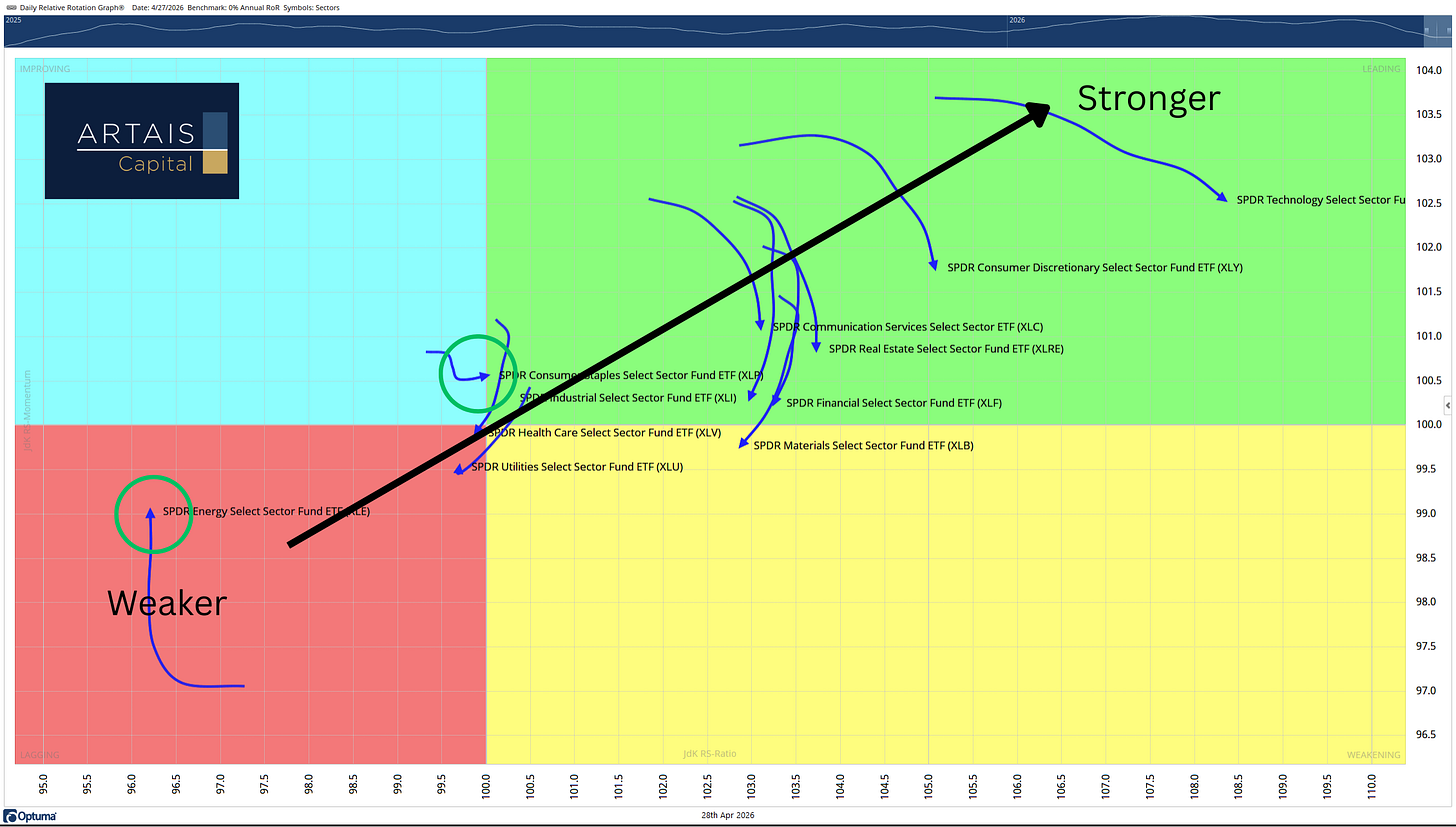

* Nine of the 11 sectors that make up the S&P 500 are also showing signs of weakness, with only the Energy and Consumer Staples sectors showing improvement:

BY Doug Kass · Apr 29, 2026, 7:10 AM EDT

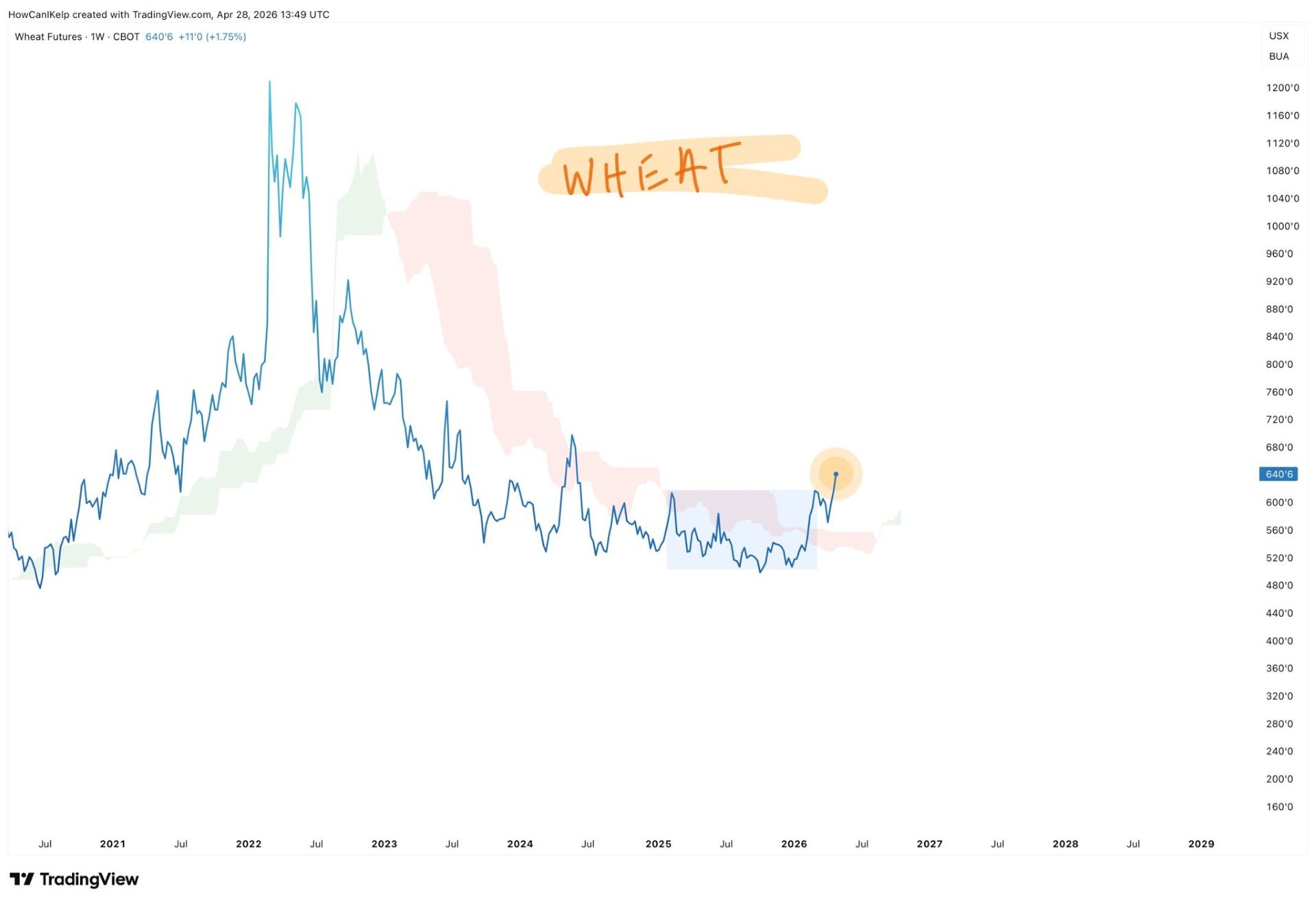

Chart of the Day: Wheat

For yesterday's chart of the day, we highlighted the natural progression of a commodity cycle, with one of the last phases being a run into Energy.

Agricultural commodities tend to move alongside Energy due to shared input costs and inflation dynamics, and today, Wheat futures pushed to fresh 52-week highs.

Grains are now on pace for one of their strongest three-week advances of the decade, with the Invesco Agriculture Fund (DBA) looking primed to push higher out of a multi-year range.

The Takeaway: Commodity strength continues to broaden, with agriculture joining Energy in the leadership rotation.

- (18) Analogics (@HowCanIKelp) / X

The market has been undergoing a stealth correction over the past week, with the equal-weight S&P 500 on pace for its sixth consecutive down day.

— Sam Gatlin (@sam_gatlin)

This is the longest losing streak since December of 2024. pic.twitter.com/IaMMhMG8XQ

El ratio NASDAQ 100 / S&P 500 ( $QQQ / $SPY ) esta en máximos históricos mientras que el ratio entre sus proxy "equalweight" $QQQE / $RSP sigue lateral

— Daniel Puleo, CMT, CFTe, €FA (@dpuleo19)

Esto confirma que el outperformance actual está concentrado en las mega caps tech pic.twitter.com/9JlSmvMx99

$Energy sector back above the 20 & 50-DMAs with this move. It held the 50% retracement of the entire upward move this year...more upside from here?@SchwabTrading @SchwabNetwork #SchwabCoaching

— Kevin Horner (@KevinHornerCS)

*not a recommendation pic.twitter.com/3z3bWVr4J9

Yo, Charts — pic.twitter.com/qxKG3GIynk

— da Chart Life (@daChartLife)

WHAT IF the biggest bubble of our lifetime isn't crypto?

— Thierry from arvy 🇨🇭 (@ThierryBorgeat)

Not AI stocks.

Not real estate.

What if it's the one asset every pension fund, every retiree, every "safe" portfolio is loaded with?

Bonds.

200 years of rate cycles say the same thing:

Every peak lasts 56–67 years.

The… pic.twitter.com/eVCL5YzKkj

Bonus — Here are some great links:

BY Doug Kass · Apr 29, 2026, 6:35 AM EDT

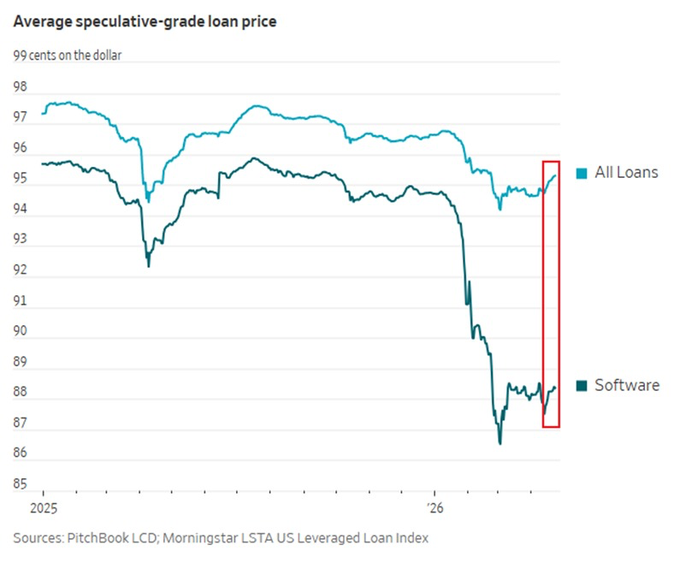

The US software sector is struggling:

— The Kobeissi Letter (@KobeissiLetter)

Average software company loan prices are down to ~88 cents, near the lowest in at least 2 years.

This marks a 6-cent, or -7% decline since the start of the year.

As a result, software is the most affected sector in the US leveraged loan… pic.twitter.com/4Hg7g0iKpz

BY Doug Kass · Apr 29, 2026, 6:25 AM EDT

I will be operating outside of my office (on a laptop) this morning for the second fumigation (for fleas from my dogs) stage (two weeks after the first event)!

BY Doug Kass · Apr 29, 2026, 6:15 AM EDT

BREAKING: Hedge fund repo borrowing is now up to a record $3.4 trillion.

— The Kobeissi Letter (@KobeissiLetter)

Repo borrowing is a form of short-term financing where hedge funds pledge Treasuries as collateral to borrow cash, allowing them to make levered bets.

Repo borrowing has more than TRIPLED since 2019.… pic.twitter.com/YCWTcEDHcp

BY Doug Kass · Apr 29, 2026, 6:05 AM EDT

My guest today is Paul Tudor Jones (@ptj_official), one of the greatest macro traders of all time.

— Patrick OShaughnessy (@patrick_oshag)

He correctly predicted the 1987 stock market crash and shorted the Japanese bubble in 1990. For over 40 years, his flagship fund has had a negative correlation to the S&P 500. 100%… pic.twitter.com/pLu1u1BIBL

BY Doug Kass · Apr 29, 2026, 5:55 AM EDT

The S&P Short Range Oscillator stands at 2.60% vs. 3.85%.

Moderately overbought.

Position: Short SPY (VS), QQQ (VS)

BY Doug Kass · Apr 29, 2026, 5:45 AM EDT

WHAT IF the biggest bubble of our lifetime isn't crypto? Not AI stocks. Not real estate. What if it's the one asset every pension fund, every retiree, every "safe" portfolio is loaded with? Bonds. 200 years of rate cycles say the same thing: Every peak lasts 56–67 years. The Show more

BREAKING: Hedge fund repo borrowing is now up to a record $3.4 trillion. Repo borrowing is a form of short-term financing where hedge funds pledge Treasuries as collateral to borrow cash, allowing them to make levered bets. Repo borrowing has more than TRIPLED since 2019. Show more

The US software sector is struggling: Average software company loan prices are down to ~88 cents, near the lowest in at least 2 years. This marks a 6-cent, or -7% decline since the start of the year. As a result, software is the most affected sector in the US leveraged loan Show more

$Energy sector back above the 20 & 50-DMAs with this move. It held the 50% retracement of the entire upward move this year...more upside from here? @SchwabTrading @SchwabNetwork #SchwabCoaching *not a recommendation

My guest today is Paul Tudor Jones (@ptj_official), one of the greatest macro traders of all time. He correctly predicted the 1987 stock market crash and shorted the Japanese bubble in 1990. For over 40 years, his flagship fund has had a negative correlation to the S&P 500. 100%

PAUL TUDOR JONES ON BUYING THE S&P 500 RIGHT NOW: "If you buy the S&P at this current valuation, the 10-year forward returns are negative when you buy with the S&P P/E of 22. That's what history shows." Jones called the 1987 crash before it happened. He's not predicting aShow more

The most important takeaway from the Fed decision: For months, the Fed has characterized inflation as "somewhat elevated" in their policy statements. Today, that changed. Amid surging energy prices, the Fed now says inflation "is elevated." The Fed says inflation is back.

The market has been undergoing a stealth correction over the past week, with the equal-weight S&P 500 on pace for its sixth consecutive down day. This is the longest losing streak since December of 2024.

Yo, Charts —