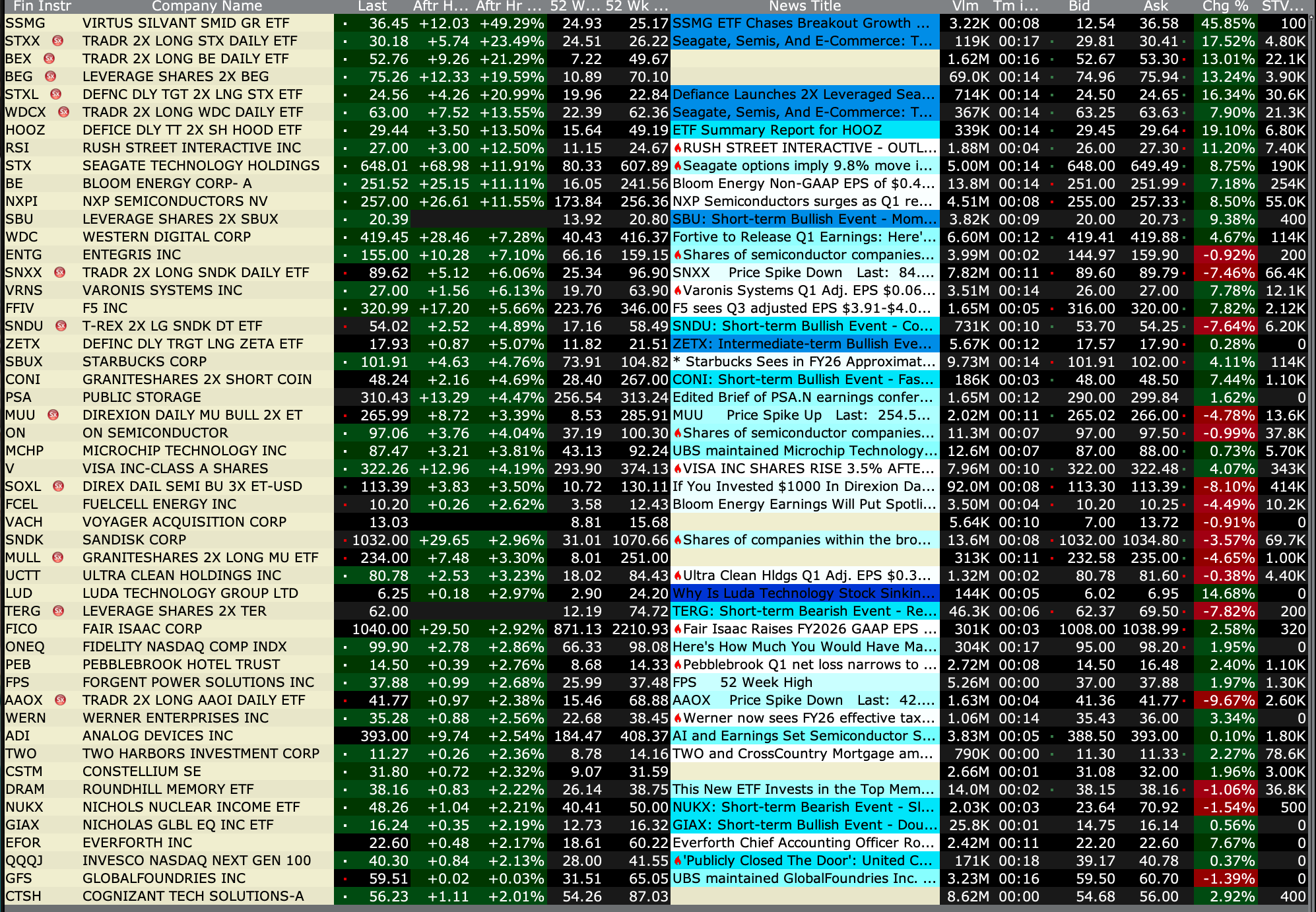

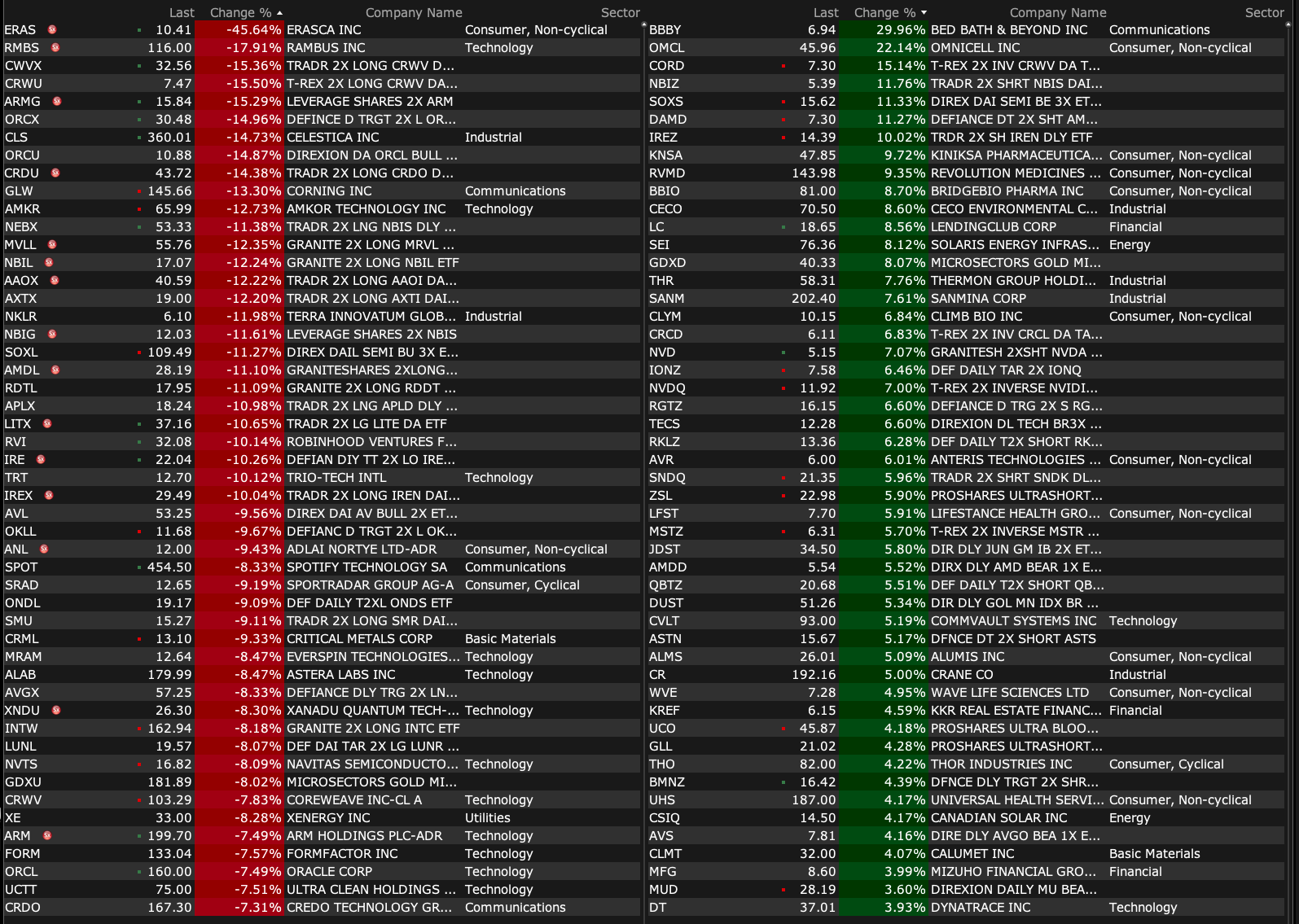

Tuesday's After-Hours Advancers and Decliners

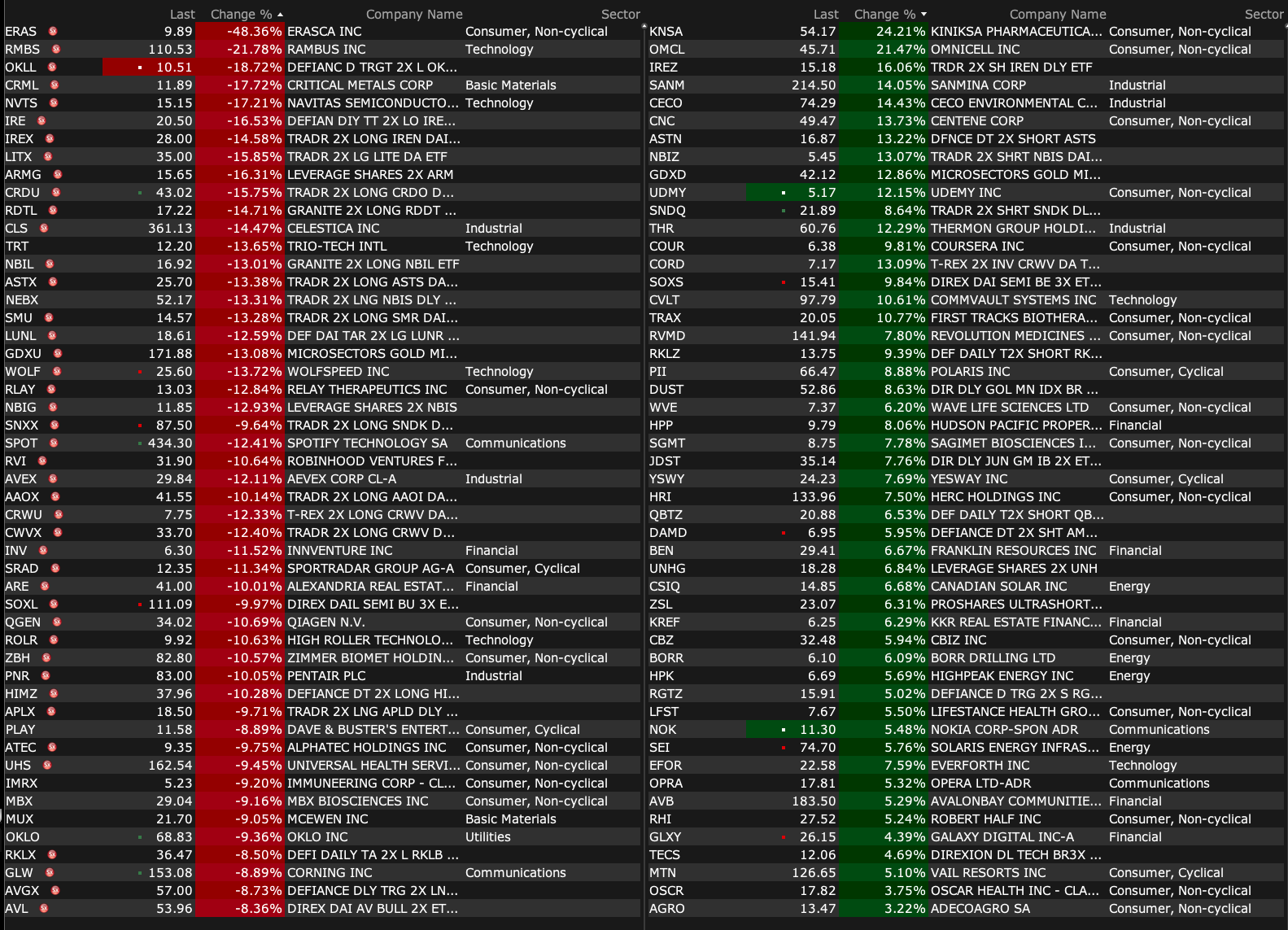

After-Hours % Advancers

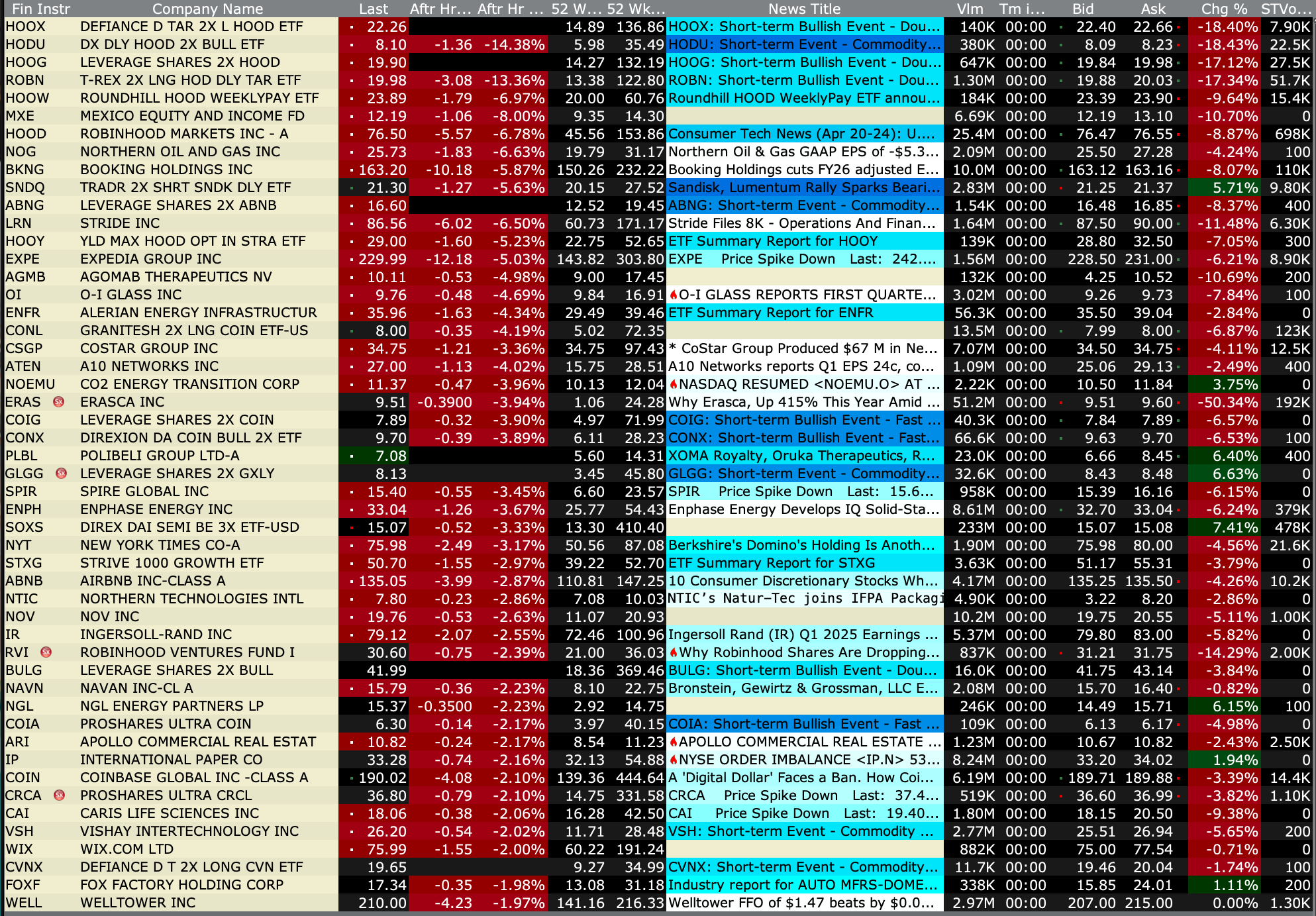

After-Hours % Decliners

BY Doug Kass · Apr 28, 2026, 4:40 PM EDT

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Apr 28, 2026, 4:40 PM EDT

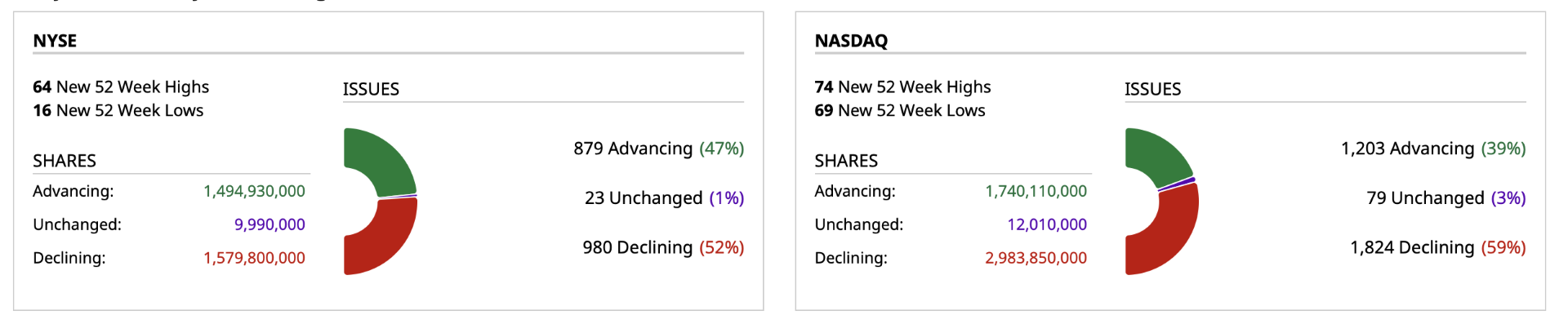

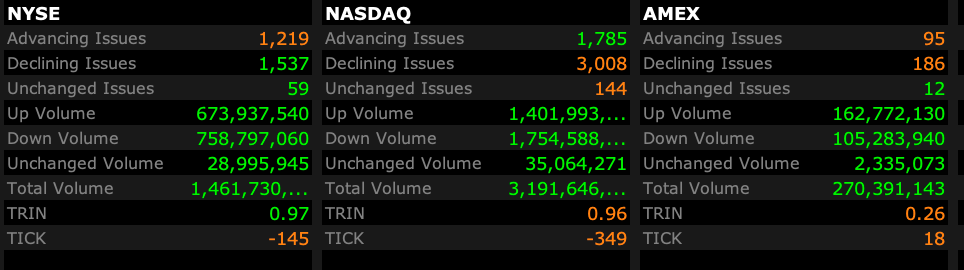

Closing Volume

- NYSE volume 7% below its one-month average

- NASDAQ volume 20% below its one-month average

- VIX index: down 1.17% to 17.81

Breadth

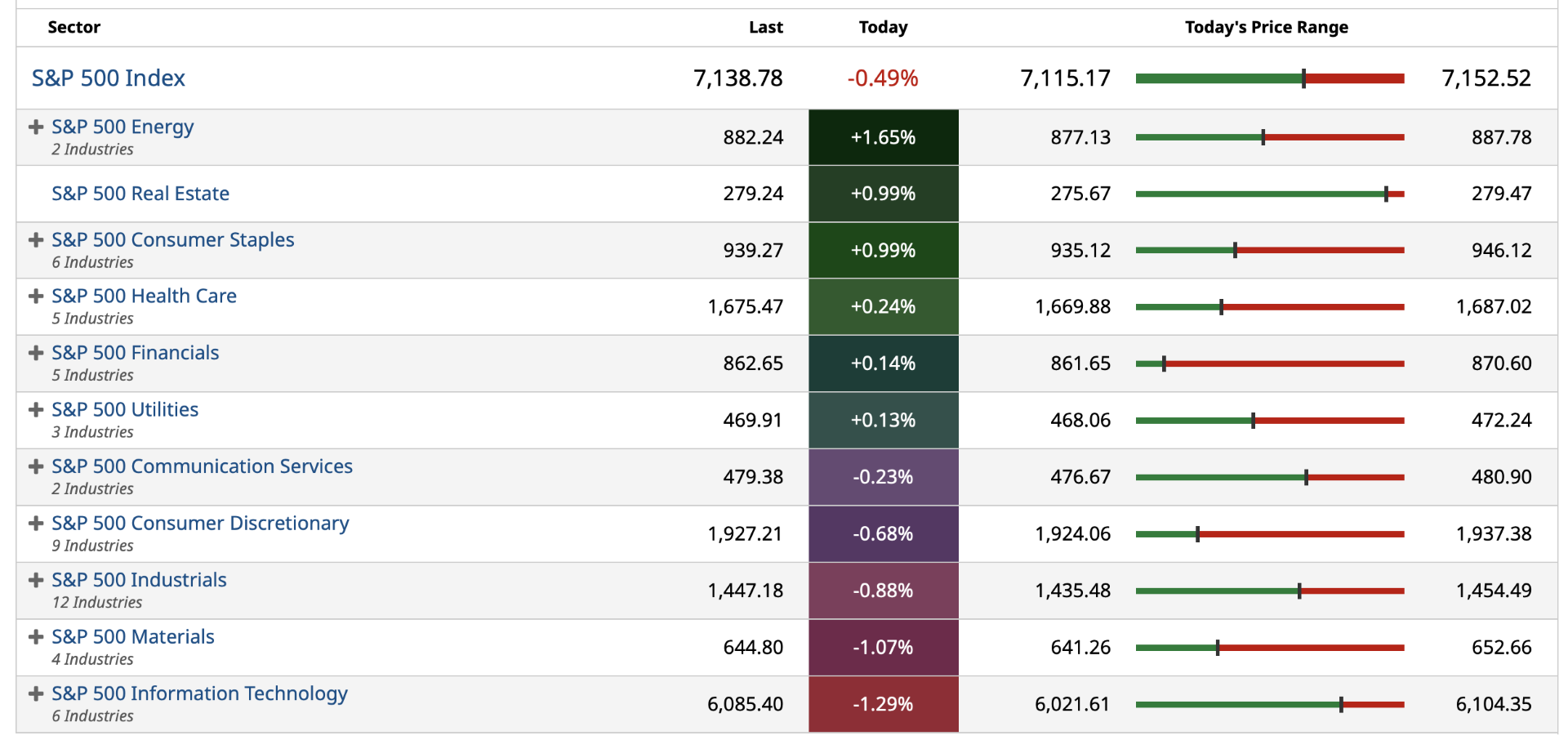

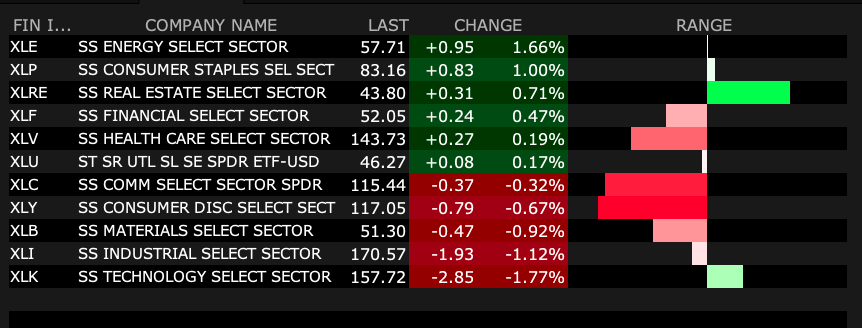

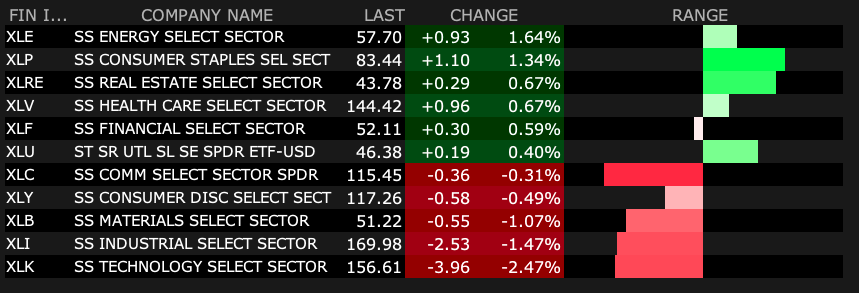

S&P 500 Sectors

% Movers

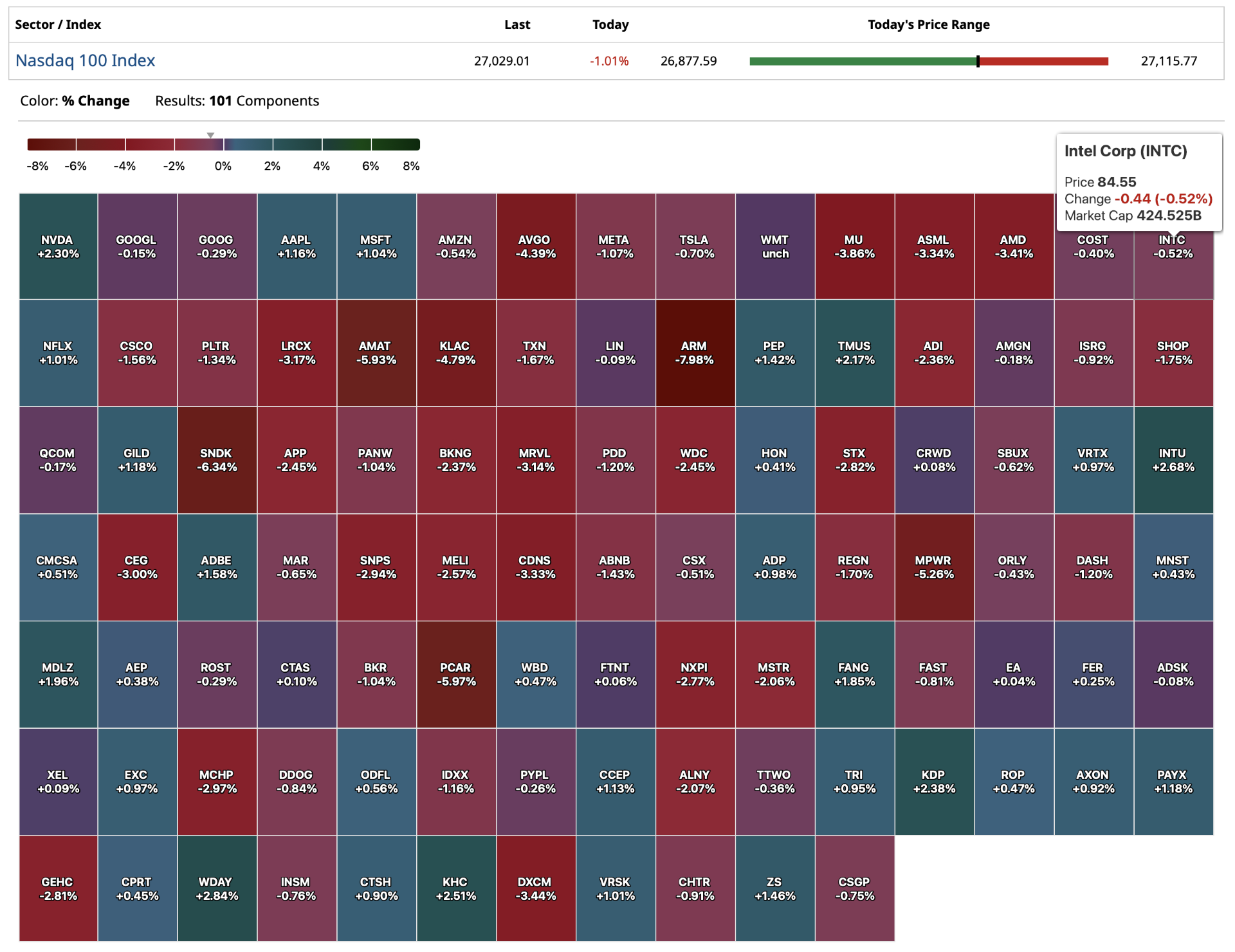

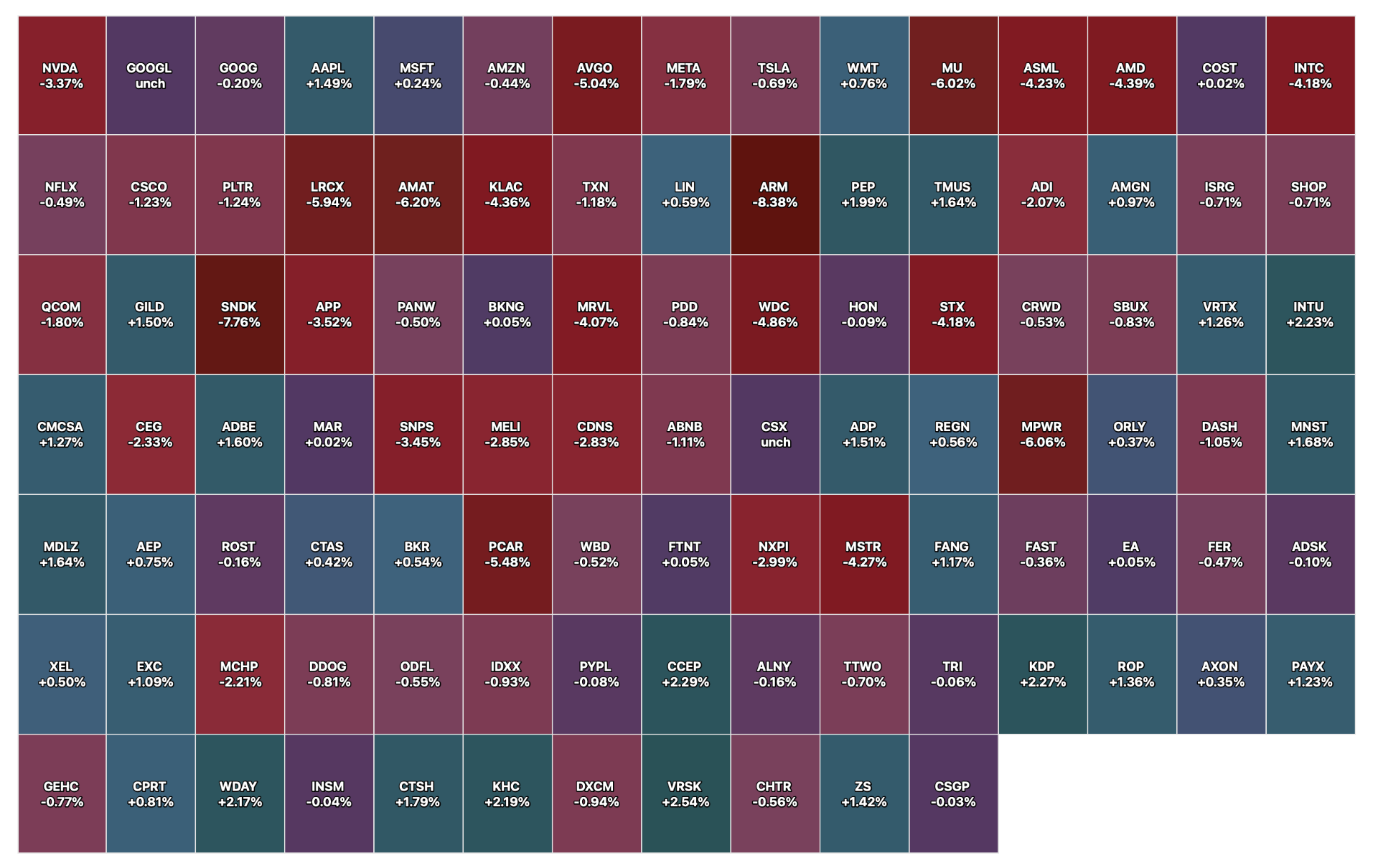

Nasdaq 100 Heat Map

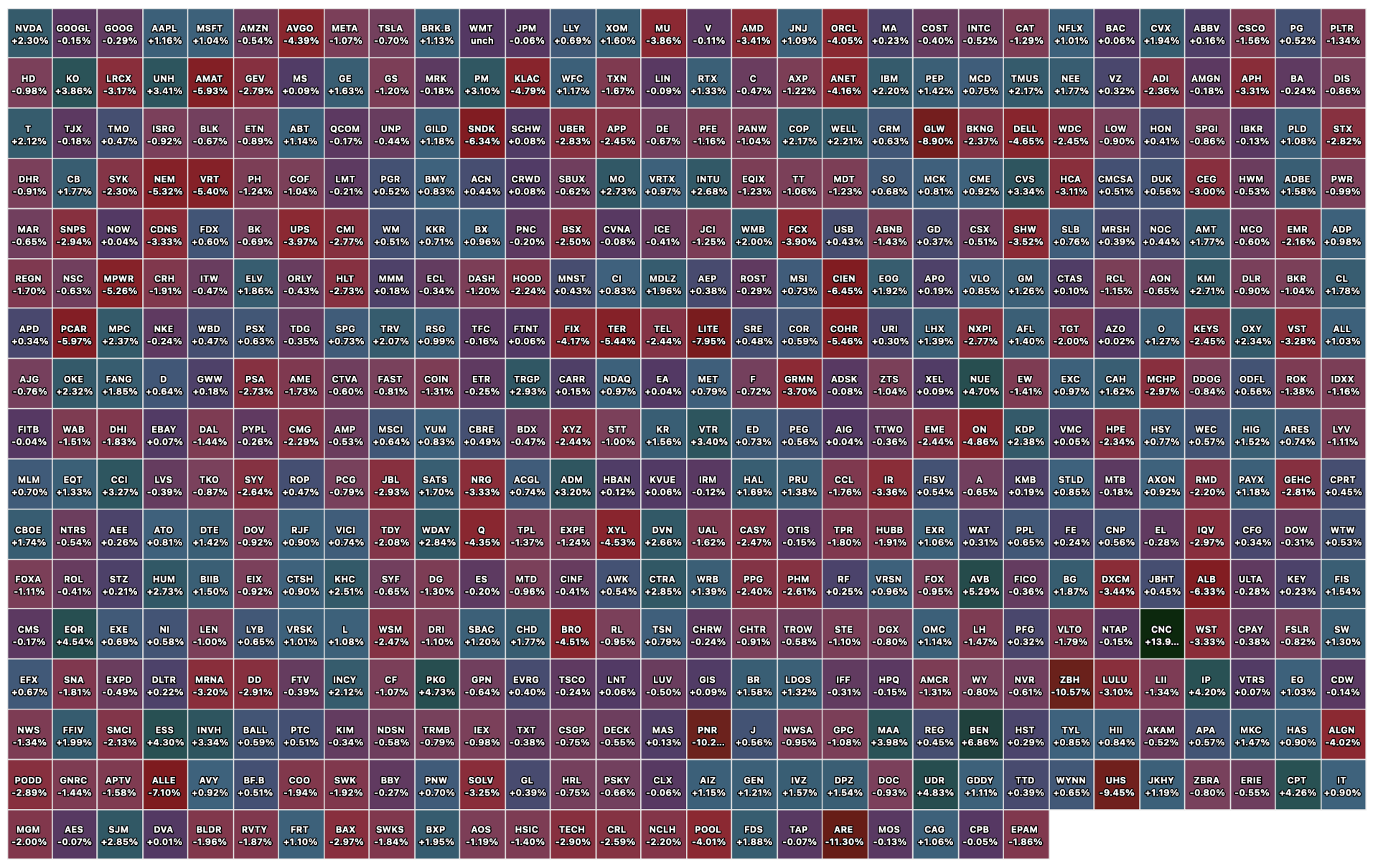

Closing S&P 500 Heat Map

BY Doug Kass · Apr 28, 2026, 4:31 PM EDT

Here are today's things:

* I took in my index shorts:

(SPY) $711.02

(QQQ) $656.68

*I re-established -ndex shorts:

SPY $711.60

QQQ $658.15

* I covered my tech trading short rentals: (MU) $507.88, (AMD) $317.97 and (INTC) $81.84

* I covered my (TSLA) short at $375.78.

Position: Short SPY (VS), QQQ (VS)

BY Doug Kass · Apr 28, 2026, 3:28 PM EDT

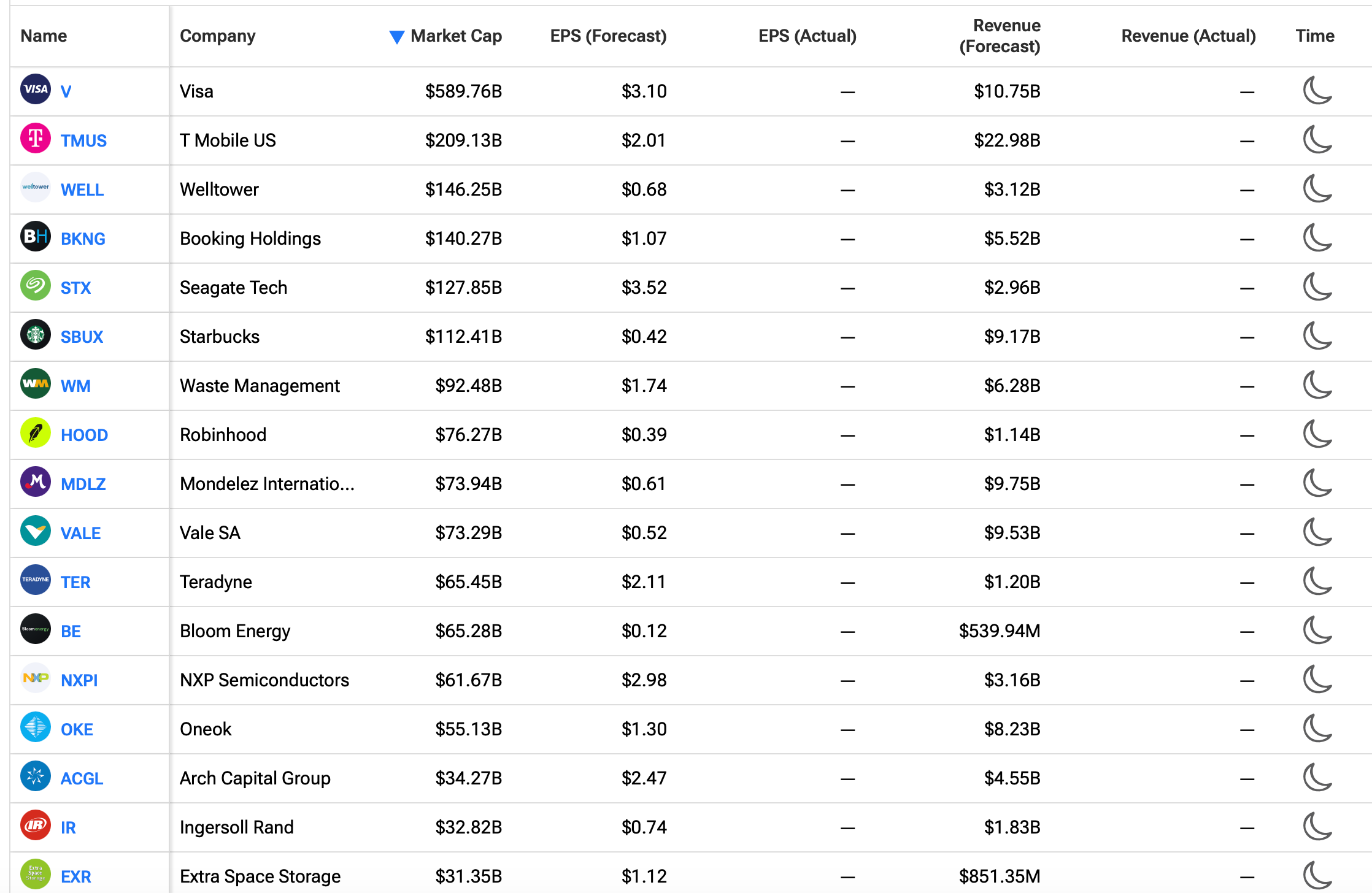

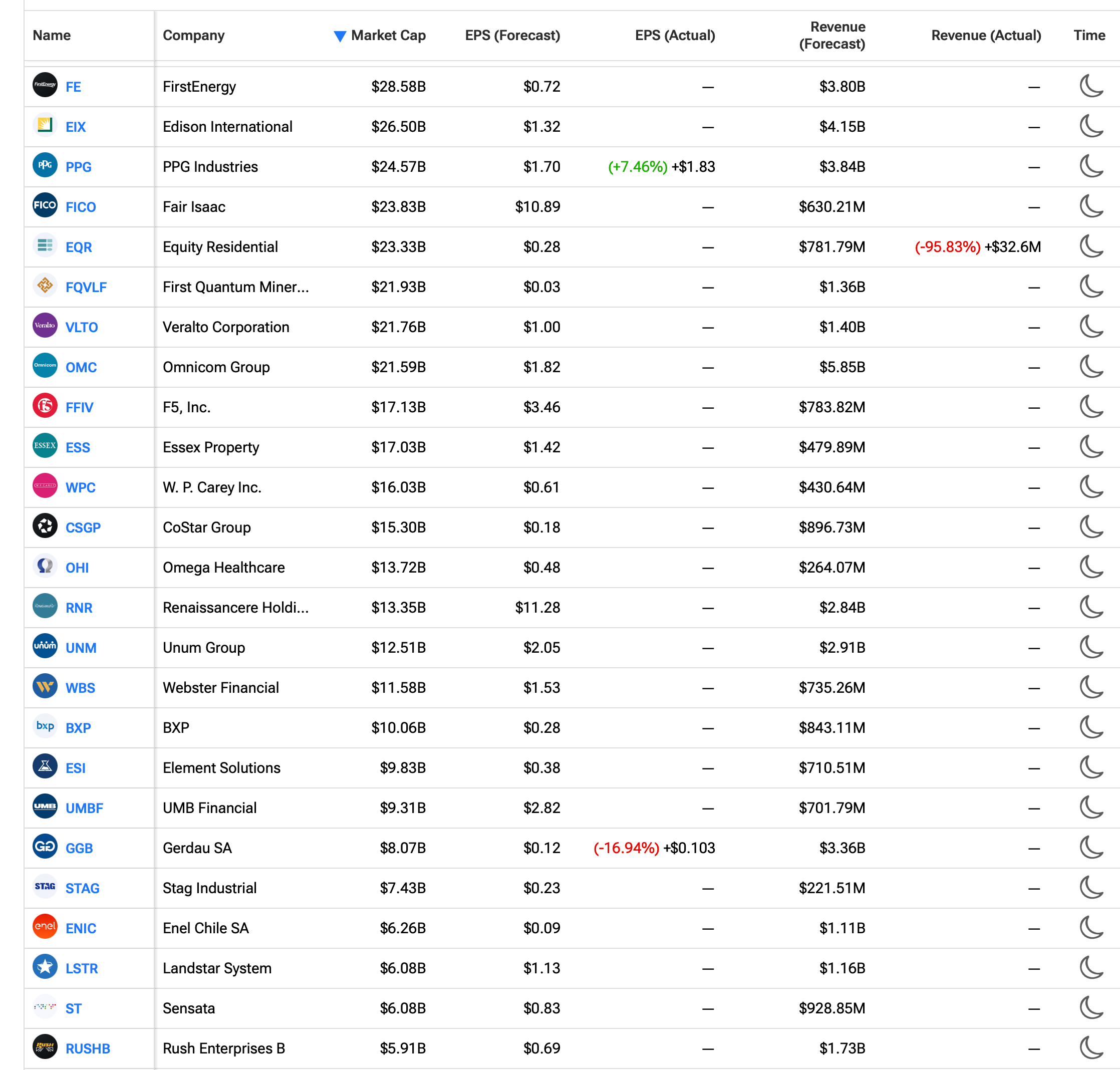

Earnings Calendar After-Hours Tuesday

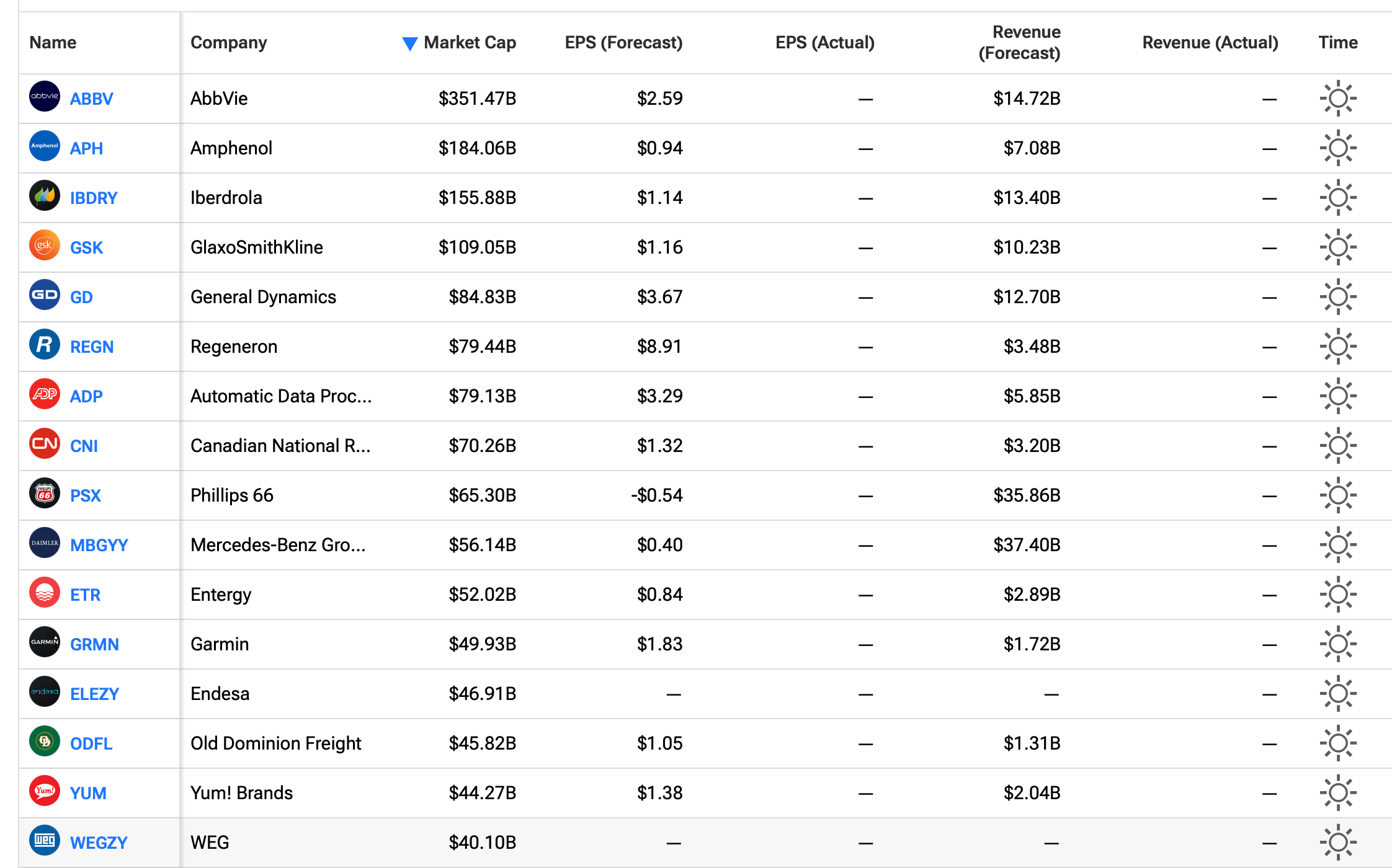

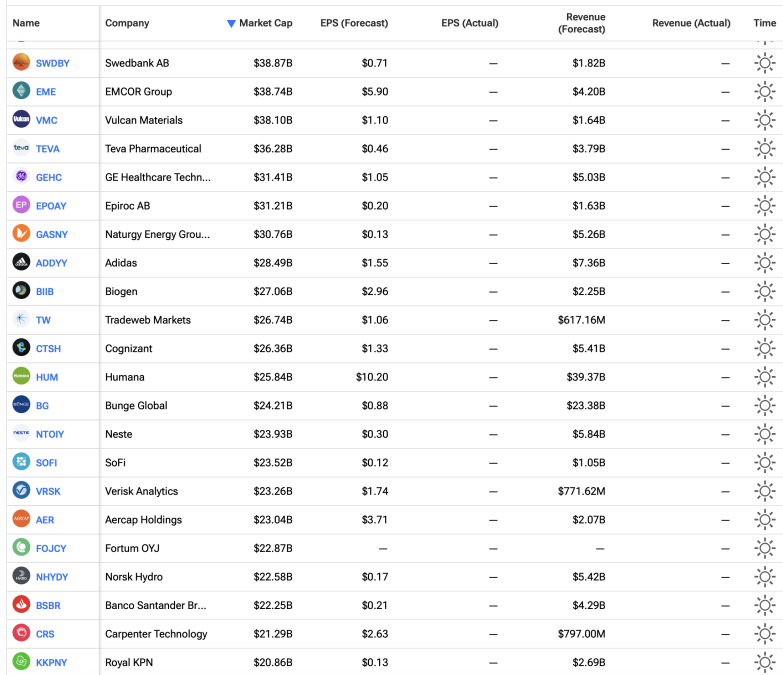

Earnings Calendar Pre-Open Wednesday

BY Doug Kass · Apr 28, 2026, 3:15 PM EDT

With S&P cash -34 handles, I am back shorting the indices:

* (SPY) $711.60

* (QQQ) $658.15

Position: Short SPY (VS), QQQ (VS)

BY Doug Kass · Apr 28, 2026, 2:58 PM EDT

I'm back in the saddle.

BY Doug Kass · Apr 28, 2026, 2:53 PM EDT

At 1:49 PM:

BY Doug Kass · Apr 28, 2026, 2:12 PM EDT

From Peter Boockvar:

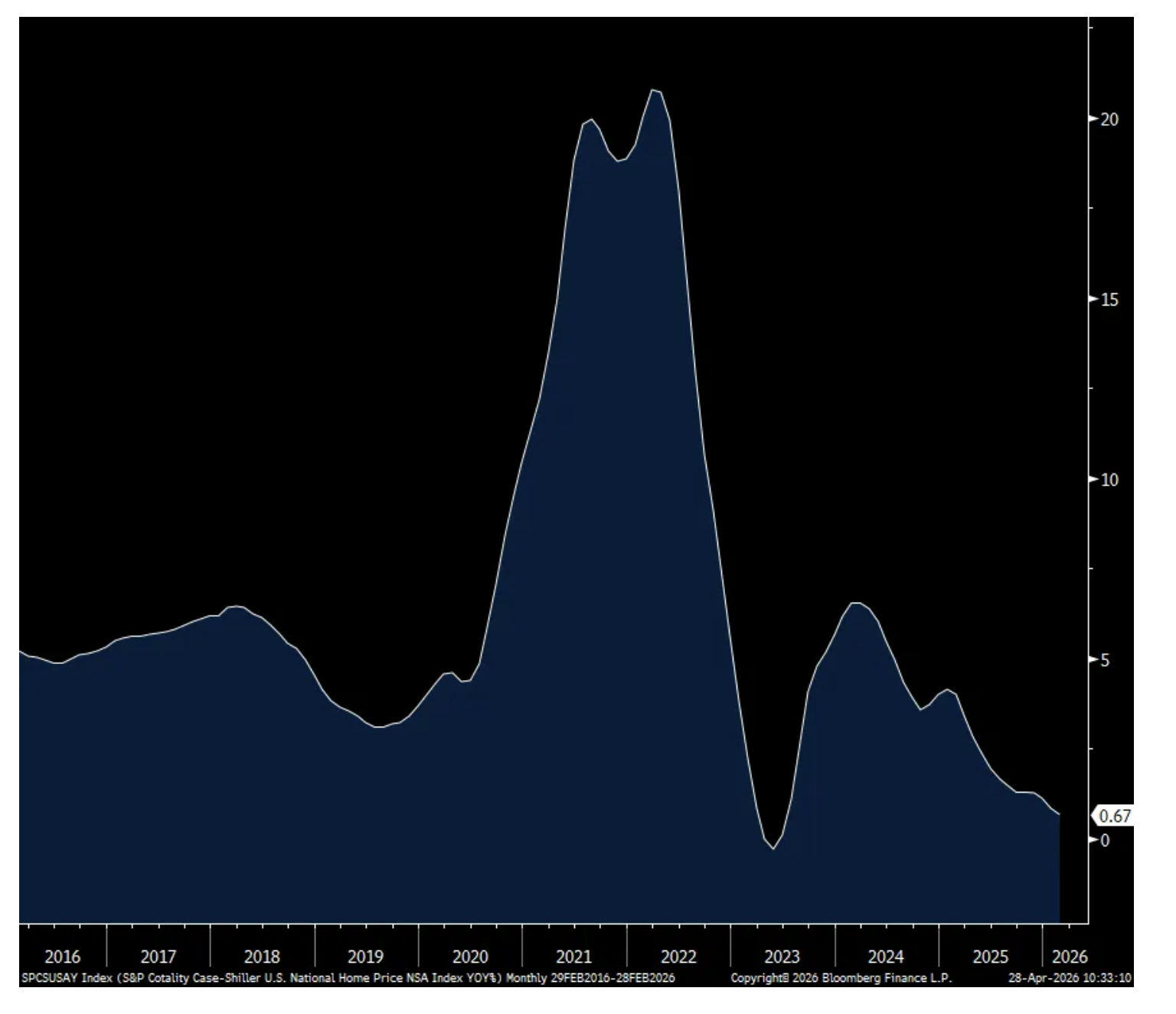

The pace of home price gains in February continued to slow, rising just .7% y/o/y, something that I continue to say should be welcomed in terms of inviting more first time buyers into the market from an affordability perspective which would increase the pace of transactions and mobility.

The softest markets are where they were the hottest in the past few years as more supply has come online. Examples include Denver, Tampa, Dallas, Phoenix and Las Vegas. The best markets are still supply constrained such as New York, Chicago, Cleveland and Minneapolis. S&P Global said “Leadership remains concentrated in Midwest and Northeast markets.”

S&P Global said “More than half of major US metropolitan markets posted y/o/y price declines in February, signaling that the housing slowdown has broadened well beyond its Sun Belt origins.”

Home Price Change y/o/y

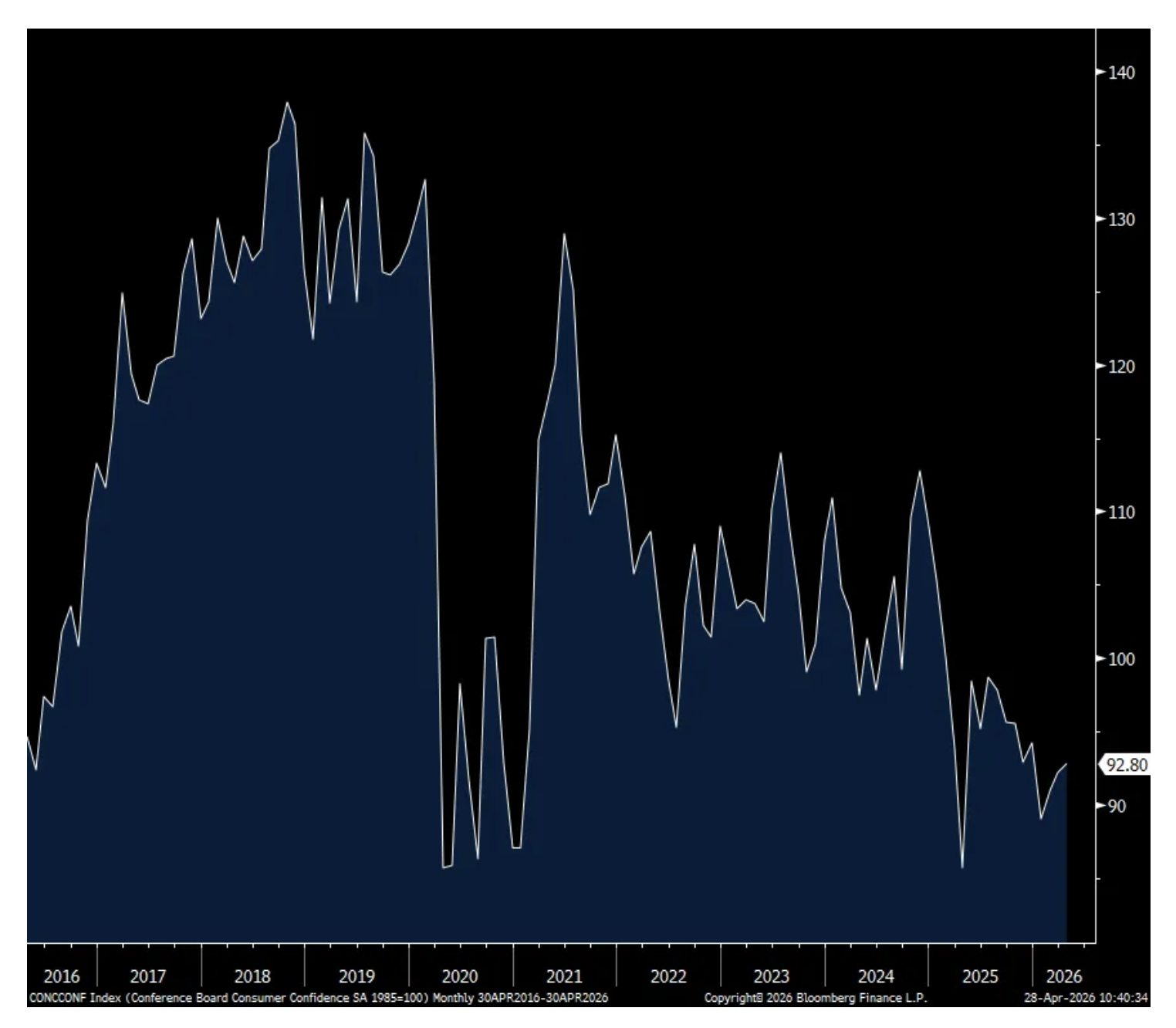

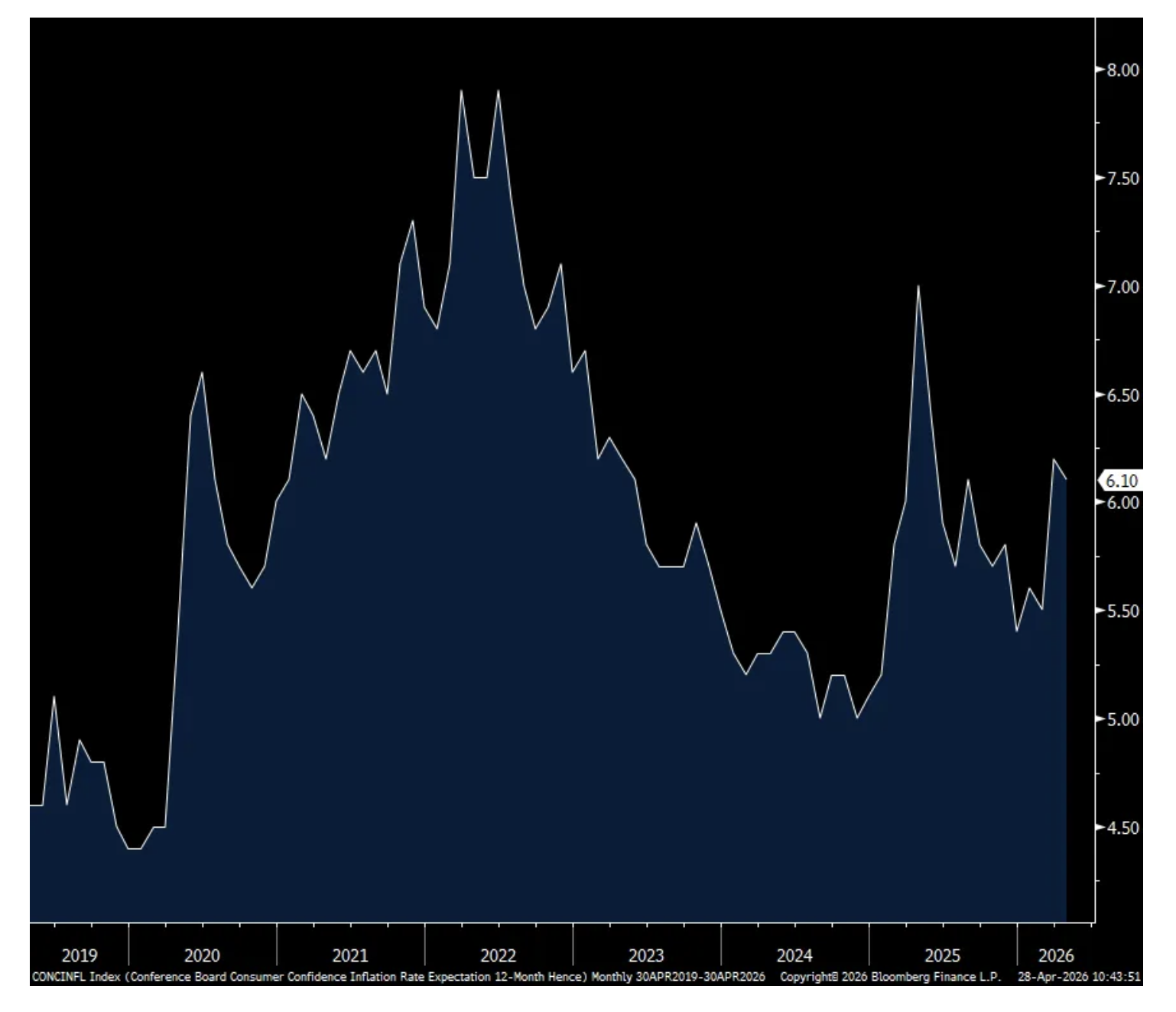

The April Consumer Confidence index from the Conference Board was little changed m/o/m at 92.8 vs 92.2 in March and the best of the year, though still well below the February 2020 print of 132.6 and more just bouncing along a multi year bottom. One yr inflation expectations were 6.1% vs 6.2% in March and 5.5% in February.

The answers to the labor market questions were mixed. Those that said jobs were Plentiful were little changed but there was a 1.5 pt drop in those saying jobs were Hard to Get. Also, there was a .7 pt rise in those expecting ‘more jobs’ over the coming six months after dropping by .6 pts last month. Income expectations slipped but after rising in March.

Spending intentions improved for both vehicles and homes and were mixed for major appliances. With respect to other big ticket items though, the Conference Board said “Consumers’ plans to buy big-ticket items over the next six months continued to shift from “yes” and “maybe” in February, to “no” in April. Nonetheless, the proportion saying “yes” remained well above the other responses. Used cars, furniture, TVs, and smartphones remained the most popular items within their respective categories for future purchases. Among pricy items, furniture remains the top expected purchase.”

With respect to the purchase of travel within the services sector, “Overall expected spending on airfare/trains for personal travel fell again in April.”

A few other noted things from the Conference Board commentary, “Consumers’ write-in responses on factors affecting the economy continued to skew towards pessimism in April. Comments about prices, oil and gas, and war increased in frequency compared to March—a likely signal of consumers’ underlying worries about how the war in the Middle East will impact their pockets.”

“A two-week ceasefire and a rebound in stock market indices within the survey-sample period (April 1–22) likely helped ease concerns about financial indicators somewhat in April after spiking in March. Still, consumers remained warry.”

Nothing market moving in response to the data but we know the very uneven financial situation and mood of the US consumer, especially after the jump in energy prices and it’s always better to see how they actually spend rather than how they feel.

Consumer Confidence

One yr Inflation Expectations

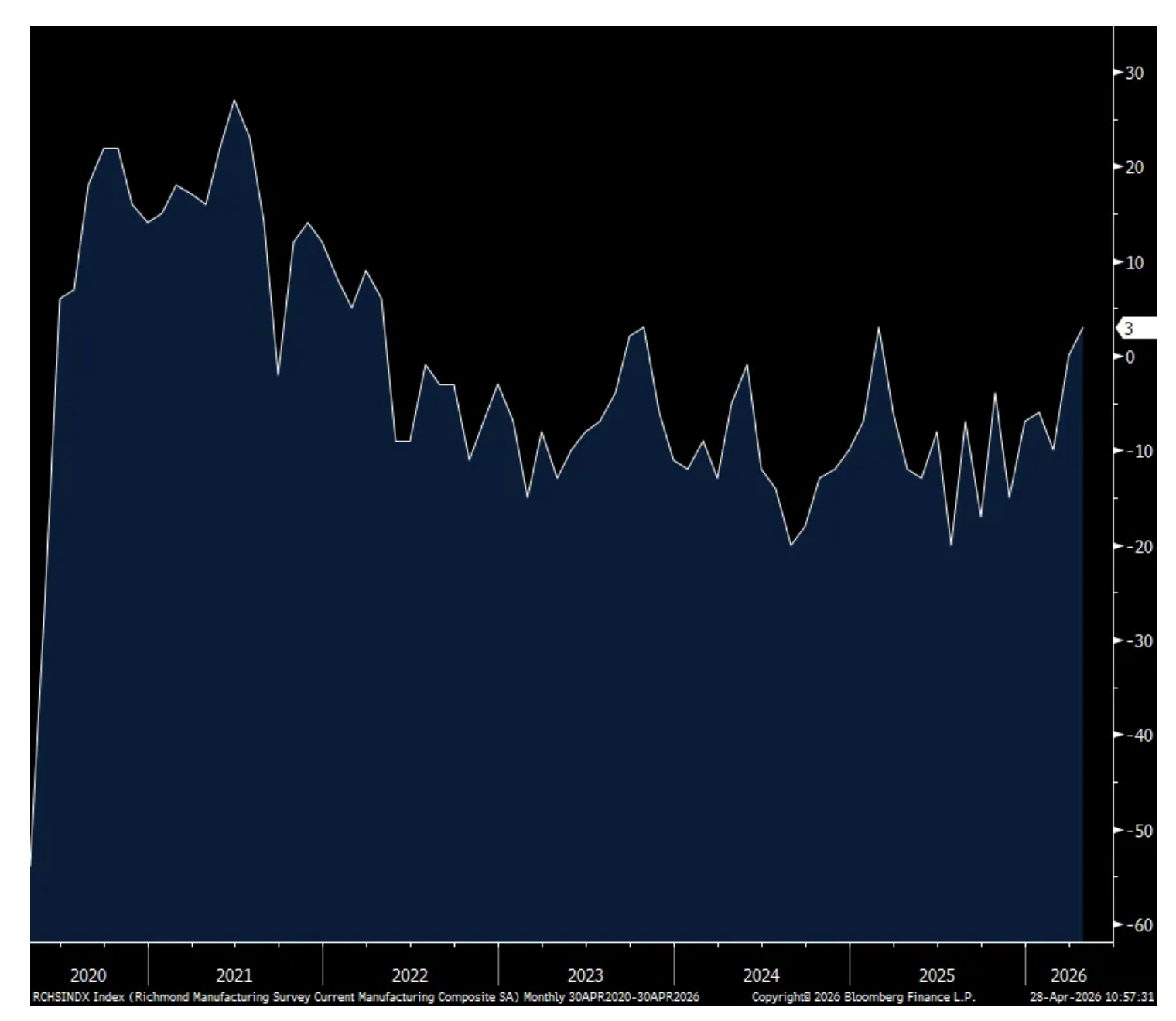

Lastly today, the April Richmond manufacturing index rose to +3 from zero. As seen with other manufacturing surveys, new orders continued to improve and I’ll argue again that it seems to be the front loading of ordering post war ahead of any price increases/supply issues.

Capital spending plans remained negative. With respect to cost inflation and pass through, prices paid rose after slipping in March while those received dipped after rising last month. Of note, six month expectations for prices paid rose to the highest since last September and went to a 3 month high for prices received.

Bottom line, global manufacturing is recovering but seems to be more due to inventory restocking rather than due to a natural improvement in end demand.

Richmond Mfr’g index

BY Doug Kass · Apr 28, 2026, 12:55 PM EDT

🚨 China's Real Estate Market has erased all gains from the last 20 years pic.twitter.com/ZIGemn0dPs

— Hedgeye (@Hedgeye)

BY Doug Kass · Apr 28, 2026, 12:25 PM EDT

Semiconductor are now 14% of the market, nearly double the dot-com peak. pic.twitter.com/TLBPAQFGJ4

— Hedgeye (@Hedgeye)

BY Doug Kass · Apr 28, 2026, 12:10 PM EDT

* Pre eye surgery chatter..

Yesterday a child came out to wonder

Caught a dragonfly inside a jar

Fearful when the sky was full of thunder

And tearful at the falling of a star

And the seasons they go round and round

And the painted ponies go up and down

We're captive on the carousel of time

We can't return we can only look behind

From where we came

And go round and round and round

In the circle game

- Joni Mitchell, The Circle Game

I have been thinking about all the circular deals in AI and "Ponzi- like" characteristic where everything continuing depends first on pump priming cash flows or funding (all the private deals funding the AI data centers and the core AI creator companies — the promised payoff lure being the 10x plus multiples private unicorns can payout if successful) being the pump priming, followed by the sort of fake returns — lend me the money and I'll buy your chips/I'll buy your computing power — that allow and support a next round of incoming $$ financing... "I'll buy more of those chips and computing power and btw...the next round of buying into MY unicorn will be at a higher price, and so on..."

"Ponzis" breakdown when there is suddenly no further incoming money.

OpenAI's admission that their customer count/usage and revenues are falling short of projections — which if not met are going to make it harder to keep raising the funding round valuations — looks to me a lot like the money may be about to stop coming in.

To my knowledge, there have been no slow, orderly unwinds of any major "Ponzi-like" schemes.

Position: None

BY Doug Kass · Apr 28, 2026, 11:45 AM EDT

Breadth

S&P 500 Sectors

% Movers

Nasdaq 100 Heat Map

BY Doug Kass · Apr 28, 2026, 11:25 AM EDT

From Peter Boockvar:

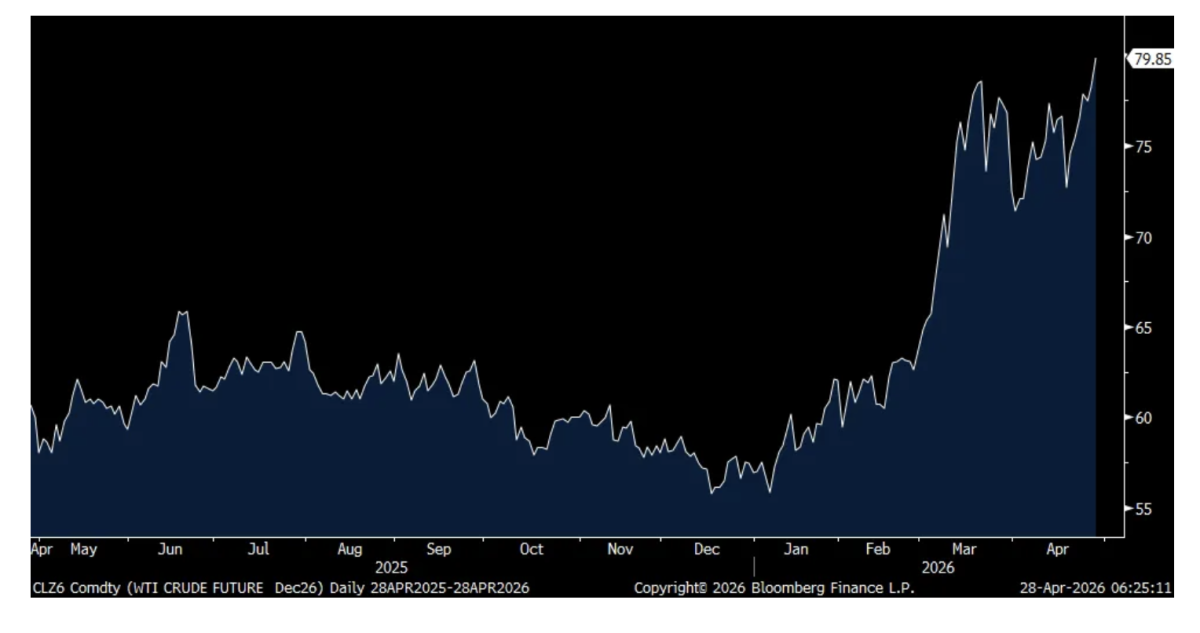

I know most of us wake up and look at the front month crude oil contract and today see it’s back to about $100 due to the unhappiness with the latest Iranian proposal. But, I encourage you to also look further out on the curve because the December contract in particular at around $80 is at a new high post war.

December WTI Crude Oil Contract

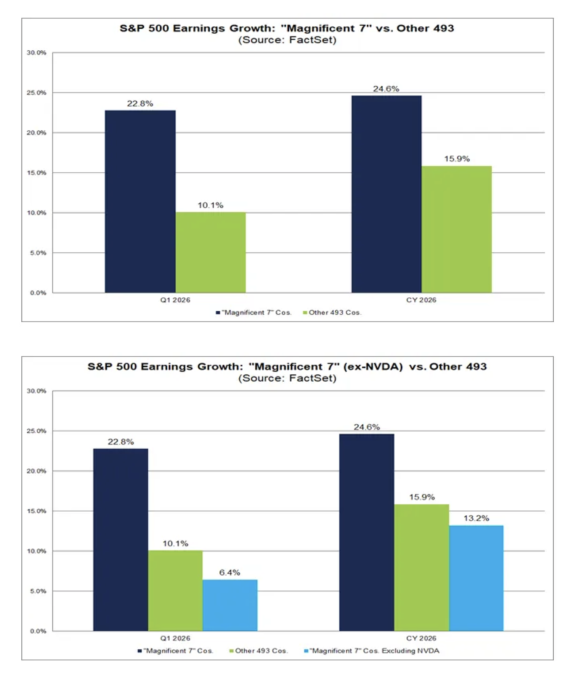

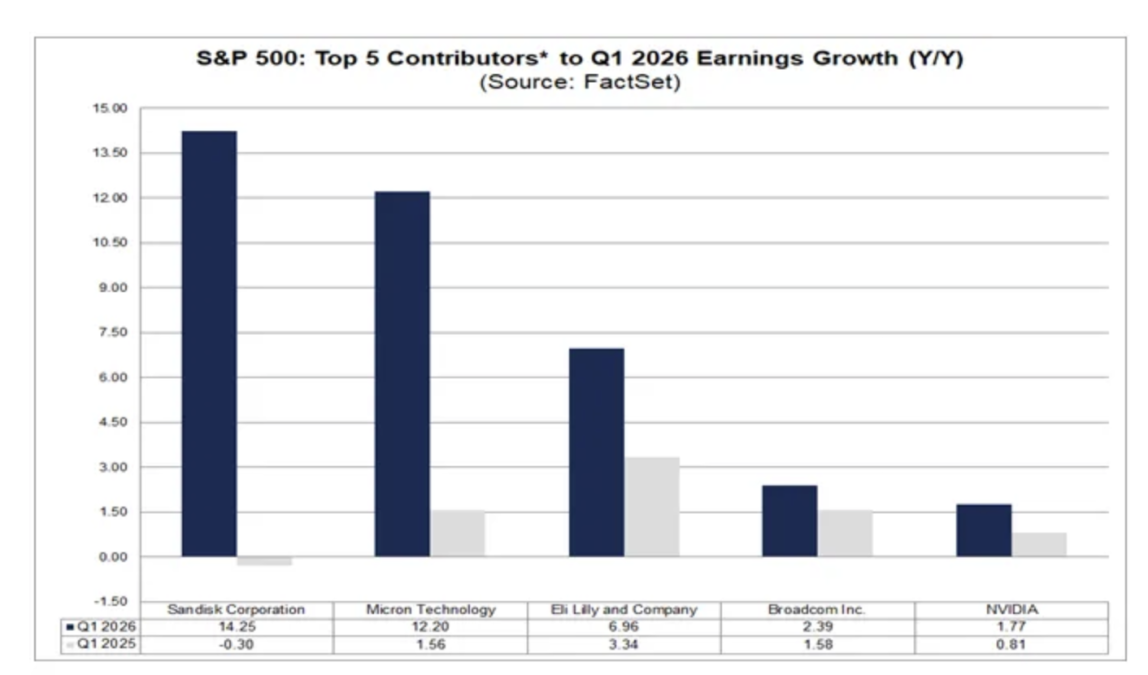

FactSet always has great stats on the earnings picture and I post three of their charts below to highlight the dependency the strong earnings story in the aggregate is dependent on the AI buildout, particularly from Nvidia, Micron and other semis.

Last year I referred to OpenAI as too big to fail. Not from the perspective of a government backstop but because their tentacles have reached so wide in the data center ecosystem buildout. So, it will be real interesting on how this plays out from here, wsj.com/

The April Dallas manufacturing index seen yesterday was -2.3 vs -.2 in March so call it around the flat line. Lost in the news with the focus now on the Strait closure and war but the issue with tariffs hasn’t gone away and talk about them was littered throughout the industry comments seen below. I bolded the word each time it was mentioned.

Chemical manufacturing

Computer and electronic product manufacturing

Fabricated metal product manufacturing

Food manufacturing

Machinery manufacturing

Miscellaneous manufacturing

Nonmetallic mineral product manufacturing

Paper manufacturing

Plastics and rubber products manufacturing

Primary metal manufacturing

Printing and related support activities

Textile product mills

Transportation equipment manufacturing

The Bank of Japan left rates unchanged overnight as expected but interestingly three members wanted to raise rates. Here were some of things Governor Ueda said of note:

“If I were to sum up the main reason for stand-pat in one sentence, it’s that the certainty of meeting our baseline outlook has declined quite significantly this time.”

“If inflationary risks could materialize or if they heighten significantly, we could raise interest rates on condition that downside economic risks or the risk of a sharp economic worsening are limited.”

“Our decision today is based on the view that central banks should look through temporary supply shock driven inflation. But if such shock brings about second round effects on underlying inflation, we must raise interest rates.”

“Prices may rise mainly for energy and energy related goods, but it’s not clear whether that could affect underlying inflation. As for supply chain disruptions, that will likely affect the economy in a fairly short period of time.”

“We don’t see a strong chance of Japan experiencing a repeat of the 1970’s style oil shock. But one thing in common is that our policy interest rate is below levels deemed neutral to the economy. We will take that into account in guiding policy.”

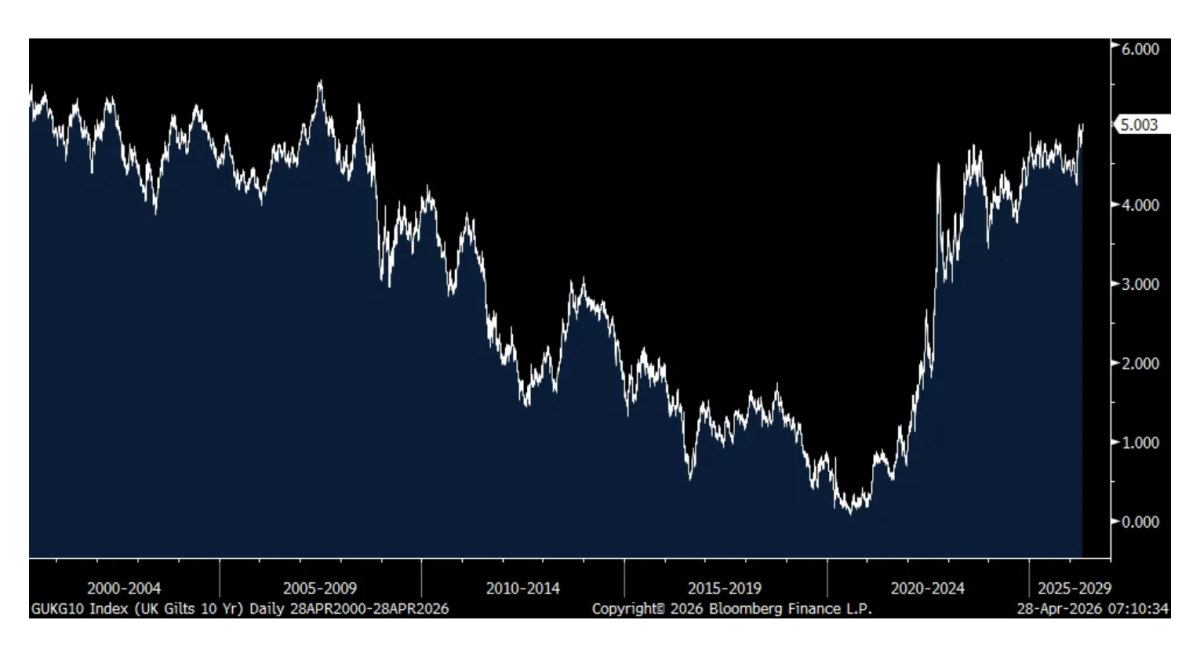

The policy split now puts the June meeting in focus for a possible hike. The 2 yr JGB yield was up by 1.3 bps to 1.38% but just back to where it was a few weeks ago. The 10 yr yield was unchanged at its 29 yr high of 2.48%. With the oil price rise, European yields are higher again as are US Treasury yields. The UK 10 yr gilt yield in particular is back to 5%, the highest since 2008. The yen is slightly weaker, just under 160 as the committee continues to drag their feet when it comes to normalizing rates. Of course though it’s been about 30 yrs since rates were normal in Japan.

10 yr Gilt Yield

To some earnings calls.

From Domino’s Pizza and whose stock fell about 9% yesterday:

“While I was pleased with our start to the year, performance for the rest of the quarter did not meet our expectations, resulting in same store sales of .9%.”

“Looking back at Q1, pressure intensified throughout the quarter, in particular in March, because of growing consumer uncertainty. Consumer sentiment hit Covid level lows, and ongoing inflation continued to impact purchase decisions. Weather also affected our business in the quarter, including the beginning of our carryout special boost week. Competition within the QSR pizza space also increased in Q1, as the national pizza players offered deals comparable, if not identical to the renowned value Domino’s has made famous.”

Rambus (semi company) and Celestica (contract manufacturer), two tech stocks are down sharply pre market and I await their earnings calls.

Nucor is up pre-market after better than expected top and bottom line numbers. From their earnings release:

“All three of our operating segments reported sequential earnings growth, driven by strong demand across key end markets, growing contributions from recent capital investments, and federal trade policies that continue to reduce the flood of unfairly traded imports into the United States.”

Positions: None.

BY Doug Kass · Apr 28, 2026, 10:21 AM EDT

I have retina surgery between 1:15 and 3 p.m. today.

Radio and vision silence during that time frame!

Positions: None

BY Doug Kass · Apr 28, 2026, 10:00 AM EDT

Following covers (for good profits):

* (MU) $507.88

* (AMD) $317.97

* (INTC) $81.84

I plan to reshort on strength.

BY Doug Kass · Apr 28, 2026, 9:45 AM EDT

-BBBY +28% (earnings, guidance)

-OMCL +22% (earnings, guidance)

-AXGN +12% (earnings, guidance)

-RVMD +8.7% (momentum following allegations that Erasca ERAS-0015 infringes on RVMD patent; TD Cowen reiterates RVMD with Buy)

-LC +8.6% (earnings, guidance)

-LGIH +8.6% (earnings, guidance)

-SANM +8.1% (earnings, guidance)

-SEI +7.3% (earnings, guidance)

-DT +5.1% (Activist Starboard Value takes stake in Dynatrace)

-CRDL +5.0% (expands U.S. MAVERIC Phase 3 Trial Network; Target recruitment anticipated by end of 2Q26, with potential to extend into Q3 to accommodate patient enrollment from the additional clinical sites)

-UHS +4.3% (earnings, guidance)

-KO +3.1% (earnings, guidance)

-SHW +2.0% (earnings, guidance)

-VISN -50% (downside momentum)

-ERAS -42% (Revolution Medicines alleges Erasca ERAS-0015 infringes patent, misuses trade secrets)

-GLND -38% (files to sell $70M public offering with warrants)

-RMBS -19% (earnings, guidance)

-CLS -15% (earnings, guidance)

-GLW -12% (earnings, guidance)

-SPOT -10% (earnings, guidance)

-ARM -7.7% (downside momentum)

-ORCL -7.3% (broad AI weakness following report of OpenAI missing targets)

-CRWV -7.1% (broad AI weakness following report of OpenAI missing targets)

-LITE -5.4% (lower in sympathy with GLW)

-AAOI -5.3% (lower in sympathy with GLW)

-UPS -5.0% (earnings, guidance)

-GLXY -4.4% (earnings)

Positions: None.

BY Doug Kass · Apr 28, 2026, 9:26 AM EDT

Positions: None

BY Doug Kass · Apr 28, 2026, 8:51 AM EDT

What this really tells you is that LLMs are commoditized products with no switching costs or any other meaningful moat

— Ross Hendricks (@Ross__Hendricks)

and if you know that, you know these companies will never turn a profit, which means the entire AI capex trade eventually goes up in smoke https://t.co/bKDxKaoyYU

BY Doug Kass · Apr 28, 2026, 8:15 AM EDT

Short people got no reason

Short people got no reason

Short people got no reason to live

They got little hands

Little eyes

They walk around tellin' great big lies

They got little noses

And tiny little teeth

They wear platform shoes on their nasty little feet

Well, I don't want no short people

Don't want no short people

Don't want no short people 'round here

- Randy Newman, Short People

Shorting is a dangerous game.

— Daniel (@danielisdizzy)

If you’re wrong on a long, you lose 100%.

If you’re wrong on a short, losses are unlimited.

Just listen to Stanley Druckenmiller:

“I’ve never had a down year, but I’ve never made money in shorts.

When I was at Soros, I shorted $200M of internet… pic.twitter.com/i6JWxUNuAo

BY Doug Kass · Apr 28, 2026, 8:05 AM EDT

The problem with "formulaic programming" on Fin TV is that they too often miss the most important news of the morning.

— Dougie Kass (@DougKass)

Case in point:

The OpenAI revenue miss (chatgpt) has not been mentioned once on @cnbc this morning. @gnoble79 @KeithMcCullough @SamofAmerica @HedgeyeDJ https://t.co/Po60oMvvvx

BY Doug Kass · Apr 28, 2026, 7:55 AM EDT

This is not Bitcoin, Ethereum, or even some memecoin. It’s the Japanese 10 year yield. pic.twitter.com/zwTfXUAQbO

— Hedgeye (@Hedgeye)

BY Doug Kass · Apr 28, 2026, 7:45 AM EDT

With S&P futures -40 handles and Nasdaq futures -302 handles, I have taken in my index shorts:

* (SPY) $711.02

* (QQQ) $656.88

I plan to re-short strength.

Position: None

BY Doug Kass · Apr 28, 2026, 7:35 AM EDT

The cracks inside OpenAI are deepening, and the numbers don’t lie.

— The Assembly (@InTheAssembly)

When your own CFO is sounding the alarm, something is seriously wrong.

Check this out:

1: OpenAI missed its target of 1 billion weekly active users, and missed multiple monthly revenue targets earlier this… pic.twitter.com/JC2IPGfVPr

BY Doug Kass · Apr 28, 2026, 7:25 AM EDT

* We are short INTC, AMD and MU

From Kakashii:

Compute Shortage, Overbooked Components: What’s Really Going On?

boy i hope all that GPU rental 'tightness' and insane semi backlog isn't a reflection of capacity chase and triple ordering like 2021. That would be tragic pic.twitter.com/umlKqmays3

— Paulo Macro (@PauloMacro)

Everyone is in shock of the recent run in semiconductors. Rightfully so.

— Mike (@MarketMike)

Take a look at just one way to measure how extended it's gotten.

The only other time $SOXX was this far from its 200 EMA was 2000.

Markets don't stay disconnected forever. They catch up through time, or… pic.twitter.com/CxOSkmdSsy

Position: Short INTC (S), AMD (S) MU (S)

BY Doug Kass · Apr 28, 2026, 7:15 AM EDT

I don’t think people realize the ramifications of OpenAI’s revenue growth slowing. Oracle is building about $348bn in data centers and needs OpenAI to pay it $75bn a year in revenue to keep up with the costs. Ellison has bet everything on this. https://t.co/kfIi6umbcS https://t.co/zPwwSUObpD pic.twitter.com/OHZ2PT0pw8

— Ed Zitron (@edzitron)

*OPENAI MISSED '25 REV TARGET FOR CHATGPT: WSJ

— zerohedge (@zerohedge)

*OPENAI MISSED GOAL OF REACHING 1B WEEKLY USERS BY 2025-END: WSJ

No worries, they only have $1.5 trillion in spending commitments

Per article that follows, the fascinating thing is that OpenAI's valuation keeps going up massively every round and these are massive and unheard of numbers to begin with.

The private investors/partners/bagholders with each round are effectively just kiting stock back and forth to keep goosing the valuation.

The whole industry is a giant Ponzi scheme from the revenue and circular deals to the valuations:

"OpenAI recently missed its own targets for new users and revenue, stumbles that have raised concern among some company leaders about whether it will be able to support its massive spending on data centers.

Chief Financial Officer Sarah Friar has told other company leaders that she is worried the company might not be able to pay for future computing contracts if revenue doesn’t grow fast enough, according to people familiar with the matter."

OpenAI Misses Key Revenue, User Targets in High-Stakes Sprint Toward IPO

Position: None

BY Doug Kass · Apr 28, 2026, 7:00 AM EDT

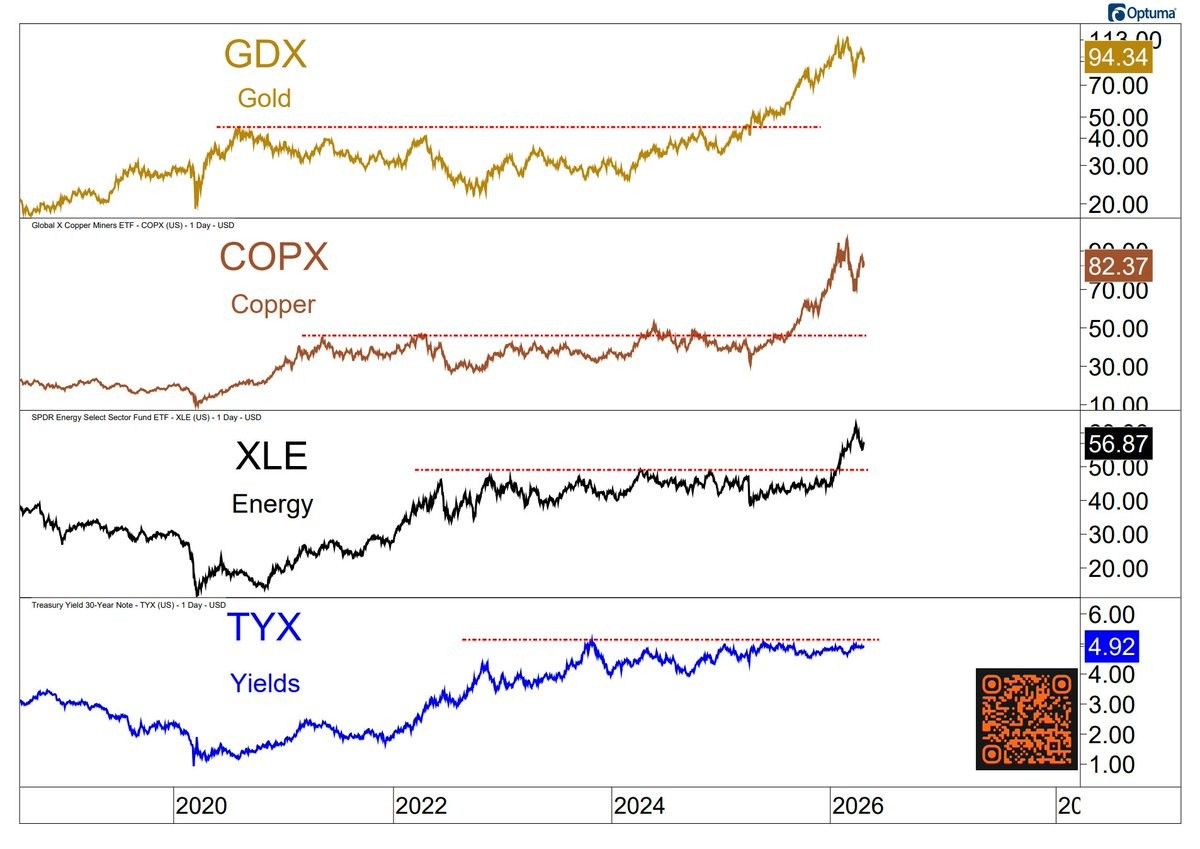

Chart of the Day

This commodity cycle has followed a classic script, with precious metals leading, followed by industrial metals, and then Energy.

That progression typically extends into rates, making long yields, or short bonds, the next logical phase as inflation pressures build beneath the surface.

With yields tightly coiled just under resistance and volatility near multi-year lows, conditions are in place for a move that should be anything but subtle.

The Takeaway: Rising yields may be the next phase of the commodity trade.

- (1) Ricardo Sarraf (@nullcharts) / X

Wednesday will be one of the most concentrated earnings sessions in history (% of market cap reporting) pic.twitter.com/VJNxGfMPRr

— Connor Bates (@ConnorJBates_)

MAG flag? pic.twitter.com/AqHQSsiDE4

— Mark Ungewitter (@mark_ungewitter)

I wrote the repost about the changing nature of war.

— Jim Bianco (@biancoresearch)

This chart is unusual ... war is now bad for defense stocks?

Maybe the stock market also sees that the defense procurement business model has to change, and that legacy defense contractors will struggle. https://t.co/QpgNhE97Ge pic.twitter.com/g1cKUbbzto

— Arun S. Chopra CFA CMT🧐 (@FusionptCapital)

Bonus — Here are some great links:

BY Doug Kass · Apr 28, 2026, 6:45 AM EDT

On Friday and Monday we @SeabreezeLP shorted $INTC, $MU and $AMD.

— Dougie Kass (@DougKass)

Go to @thestreetpro for an explanation why.... @dougkass

Global Markets Investor on X: "⚠️Semiconductor valuations have RARELY been this stretched: The Semiconductor Index, $SOX, now trades at a P/E ratio of 60…

BY Doug Kass · Apr 28, 2026, 6:35 AM EDT

Wolf Street howls about the implosion of real estate brokerage equities.

BY Doug Kass · Apr 28, 2026, 6:25 AM EDT

~90% of Wall Street analysts adjust their estimates so companies can beat (every time). Public companies not beating is (very) rare for this reason. Wall Street research, for the most part, is simply an extended "marketing arm" for publicly traded companies. If the mkt ever… https://t.co/dFBIqRnd1C

— Gordon Johnson (@GordonJohnson19)

BY Doug Kass · Apr 28, 2026, 6:15 AM EDT

BY Doug Kass · Apr 28, 2026, 6:05 AM EDT

WHAT IF the biggest bubble of our lifetime isn't crypto?

— Thierry from arvy 🇨🇭 (@ThierryBorgeat)

Not AI stocks.

Not real estate.

What if it's the one asset every pension fund, every retiree, every "safe" portfolio is loaded with?

Bonds.

200 years of rate cycles say the same thing:

Every peak lasts 56–67 years.

The… pic.twitter.com/eVCL5YzKkj

BY Doug Kass · Apr 28, 2026, 5:55 AM EDT

The S&P Short Range Oscillator remains (less) overbought at 3.85% vs. 4.89%.

Position: Short SPY (S), QQQ (S)

BY Doug Kass · Apr 28, 2026, 5:45 AM EDT

Semiconductor are now 14% of the market, nearly double the dot-com peak.

This is not Bitcoin, Ethereum, or even some memecoin. It’s the Japanese 10 year yield.

🚨 China's Real Estate Market has erased all gains from the last 20 years

Shorting is a dangerous game. If you’re wrong on a long, you lose 100%. If you’re wrong on a short, losses are unlimited. Just listen to Stanley Druckenmiller: “I’ve never had a down year, but I’ve never made money in shorts. When I was at Soros, I shorted $200M of internet Show more

What this really tells you is that LLMs are commoditized products with no switching costs or any other meaningful moat and if you know that, you know these companies will never turn a profit, which means the entire AI capex trade eventually goes up in smoke

Seeing this making the rounds today. This should not be a surprise to anyone that uses LLMs on a daily basis. Claude had clearly overtaken GPT for at least 2/3 months, a large number of people had switched over. This is a lagging indicator of OpenAI’s poor model progress prior

The problem with "formulaic programming" on Fin TV is that they too often miss the most important news of the morning. Case in point: The OpenAI revenue miss (chatgpt) has not been mentioned once on @cnbc this morning. @gnoble79 @KeithMcCullough @SamofAmerica @HedgeyeDJ

*OPENAI MISSED '25 REV TARGET FOR CHATGPT: WSJ *OPENAI MISSED GOAL OF REACHING 1B WEEKLY USERS BY 2025-END: WSJ No worries, they only have $1.5 trillion in spending commitments

MAG flag?

boy i hope all that GPU rental 'tightness' and insane semi backlog isn't a reflection of capacity chase and triple ordering like 2021. That would be tragic

~90% of Wall Street analysts adjust their estimates so companies can beat (every time). Public companies not beating is (very) rare for this reason. Wall Street research, for the most part, is simply an extended "marketing arm" for publicly traded companies. If the mkt ever Show more

For Q1 2026 (with 28% of S&P 500 companies reporting actual results), 84% of S&P 500 companies have reported a positive EPS surprise and 81% of S&P 500 companies has reported a positive revenue surprise.

The cracks inside OpenAI are deepening, and the numbers don’t lie. When your own CFO is sounding the alarm, something is seriously wrong. Check this out: 1: OpenAI missed its target of 1 billion weekly active users, and missed multiple monthly revenue targets earlier thisShow more

On Friday and Monday we @SeabreezeLP shorted $INTC, $MU

I wrote the repost about the changing nature of war. This chart is unusual ... war is now bad for defense stocks? Maybe the stock market also sees that the defense procurement business model has to change, and that legacy defense contractors will struggle.

I am not a military analyst. I'm a financial analyst focused on macroeconomic risk. That different lens might explain why I see something most military strategists and investors are missing. --- The New Rules of Warfare—And Why We Can't Opt Out For nearly a century, warfare

*OPENAI MISSED '25 REV TARGET FOR CHATGPT: WSJ *OPENAI MISSED GOAL OF REACHING 1B WEEKLY USERS BY 2025-END: WSJ No worries, they only have $1.5 trillion in spending commitments

I don’t think people realize the ramifications of OpenAI’s revenue growth slowing. Oracle is building about $348bn in data centers and needs OpenAI to pay it $75bn a year in revenue to keep up with the costs. Ellison has bet everything on this. wheresyoured.at/how-openai-kil…

One banger bit of reporting after another here by @berber_jin1 wsj.com/tech/ai/openai…

WHAT IF the biggest bubble of our lifetime isn't crypto? Not AI stocks. Not real estate. What if it's the one asset every pension fund, every retiree, every "safe" portfolio is loaded with? Bonds. 200 years of rate cycles say the same thing: Every peak lasts 56–67 years. The Show more