Boockvar on ChangXin Memory Technologies, Hynix, Oracle, Delta

From Peter Boockvar:

Maybe not yet/The most important IPO this month & it’s not SK Hynix/Oracle/Delta/Very euphoric

There doesn’t seem to be much follow through on that story Friday that the Japanese government was going to direct its pension funds to invest more at home. Reuters today is reporting that Japan has no immediate plans to change target asset allocations of its state pension funds but could work within existing allocation ranges to direct more investment to domestic assets, people with knowledge of government deliberations told Reuters. GPIF is the world’s biggest pension fund with about $1.8 trillion of assets as of March. Currently the fund has allocated about 25% in domestic equities, 25% in foreign equities, 25% in domestic bonds and 25% in foreign bonds.

This said by Reuters, there is leeway around the fixed income allocation so if JGB yields continue to rise, and thus making them more attractive, I’m pretty sure the GPIF and other Japanese domestic funds, will take advantage of that yield opportunity, bring money home and with not having to take FX risk.

After falling by a sharp 13 bps on Friday, the 10 yr JGB yield rebounded by 5 bps. The yen is weaker again and the Nikkei fell 2%, also weighed down in sympathy by the selloff in the Kospi. Keep your eye on this situation in many ways. The impact that the direction of JGB yields has on global rates, the carry trade implications if the yen continues to weaken, along with its inflationary influence and in turn JGB impact. And Japanese stocks have been big winners this year so far.

While the market got very excited about the SK Hynix US listing, I’m much more interested in this week’s CXMT (ChangXin Memory Technologies) listing (I believe on Thursday) in Hong Kong as SK has already been public for years. As I’ve mentioned a few times over the past few weeks this is China’s biggest DRAM producer and the 4th largest in the world. They are looking to raise about $4.3 billion and be sure that they are coming for Micron’s 85% gross margin, along with the earnings that Samsung and SK Hynix produce. Soon after will be a listing of China’s largest storage NAND company, Yangtze Memory Technologies, the 6th largest NAND maker in the world.

Just as China is now competing on the global stage and head-to-head with US AI frontier models, they want to do so on the hardware side as well and as Jeff Bezos once said, your gross margin is their opportunity.

With respect to Q2 US earnings season, a quick mention on Q1. Of the 28% y/o/y earnings growth, about 12 percentage points came from ‘other income’ from the big hyperscalers which happened to be their upside marks on their private equity holdings of SpaceX, Anthropic and OpenAI. About half of the earnings growth balance was from semiconductor companies. Thus, when hearing the headline earnings growth pace for both Q1 and now Q2, it’s important to look under the hood for a breakdown and the contributors.

Speaking of a hyperscaler, I went through the S&P downgrade of Oracle over the weekend to BBB- and these were the key points from them:

“Oracle’s growing AI infrastructure business is diluting its strong business risk profile. We assigned Oracle a negative outlook in July 2025 due to the pace of its AI infrastructure buildout and the potential financial impact. We now recognize that we underestimated the scale of the investments required to expand the AI business and its impact on our overall view of Oracle’s creditworthiness.”

“We project Oracle’s cloud infrastructure business, which accounted for 27% of revenues in fiscal 2026, will make up almost 60% of revenues by fiscal 2028. We view this to be much riskier than its legacy enterprise software and database businesses…This is because of the need for substantial upfront investment while returns are realized over the duration of multi-year contracts.”

“In addition, SpaceX’s recent decision to lease its compute capacity to Anthropic and Alphabet – and the potential for Meta to do the same – portend growing competition within the industry.”

Lastly of note, “OpenAI remains a key credit risk. We estimate that OpenAI makes up roughly half of the $638 billion in RPO (remaining performance obligations). OpenAI’s ability to meet its contractual obligations and raise external financing will be contingent upon AI tailwinds continuing and its models being market leaders. If OpenAI were unable to pay Oracle, we believe Oracle could be left with massive data center leases that it might be unable to exit or have to re-lease to new tenants under less favorable terms.”

I’ll argue again, OpenAI, because of their wide tentacles throughout the GenAI date center eco system, is too big to fail because it would bring down a lot with it.

This was from Delta’s earnings call Friday and whose stock has fallen in 6 out of the last 7 days:

“Our customers are prioritizing experiences and investing in the moments and connections that matter most to them, driving sustained strength and demand for air travel.”

With respect to their Delta/AmEx partnership, “Card spend has grown double-digits for the past 7 quarters with particular strength among our premium reserve cardholders.”

“structural change (in the industry) has accelerated, enabling the industry to recapture this year’s fuel cost inflation at the fastest pace of any recent cycle. Even after recent fare increases, airfares remain 10 points to 15 points below overall inflation since Covid. With continued fuel volatility and much of the industry still earning returns below its cost of capital, we believe current revenue momentum should remain sustainable even if fuel prices moderate.”

“main cabin trends improved through the quarter, with main cabin unit revenue growing mid-teens in the month of June.”

“We need to continue to make certain that we cover our costs, and one of our biggest costs is fuel, which is still up 50%. So I would not anticipate any decline in airfares.”

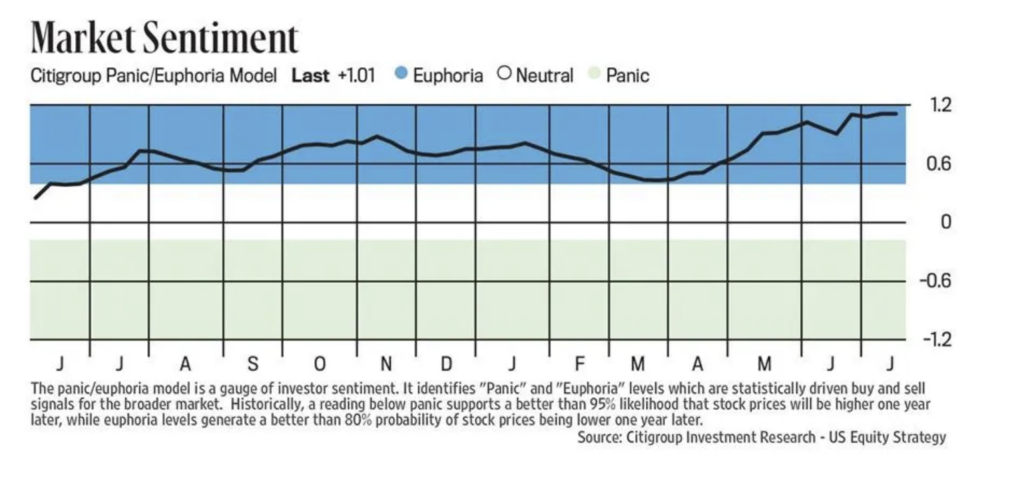

With respect to stock market sentiment, at least by the Citi Panic/Euphoria index, it is back to the recent highs of Euphoria and as a reminder, .41 is threshold so we are well above it.

Positions: None.

BY Doug Kass · Jul 13, 2026, 9:50 AM EDT