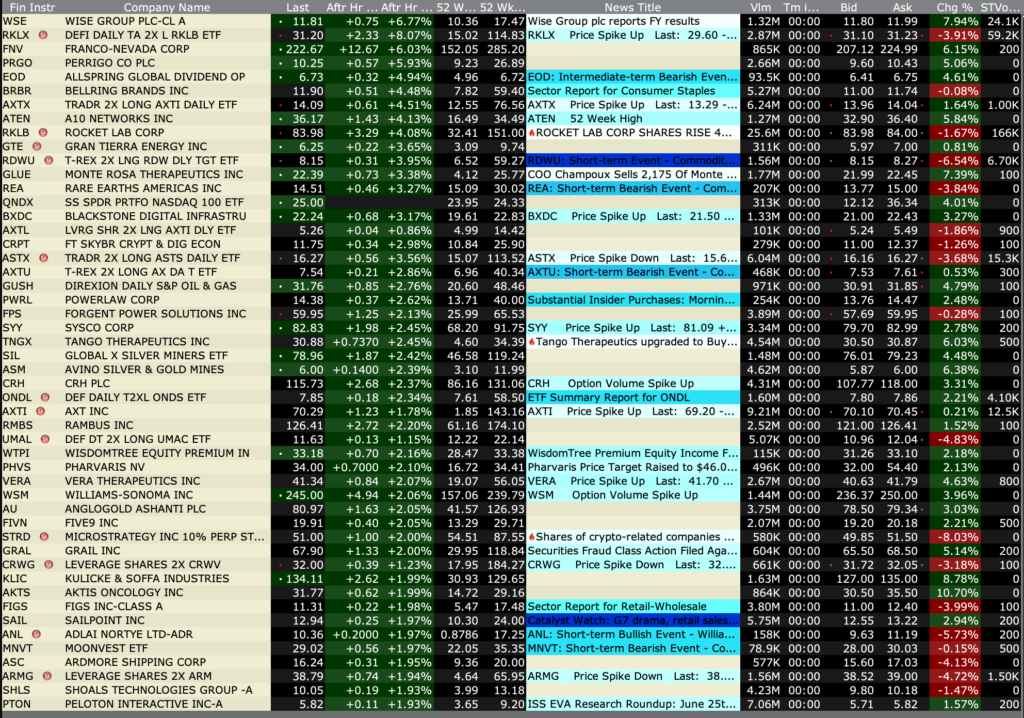

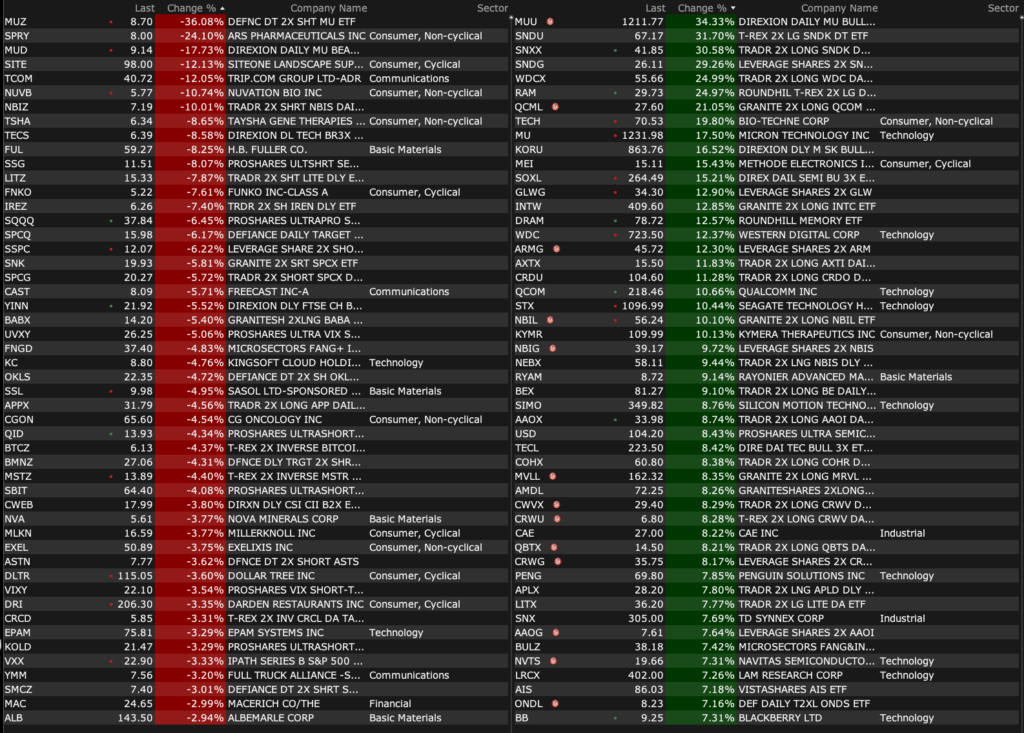

Thursday’s After-Hours Advancers and Decliners

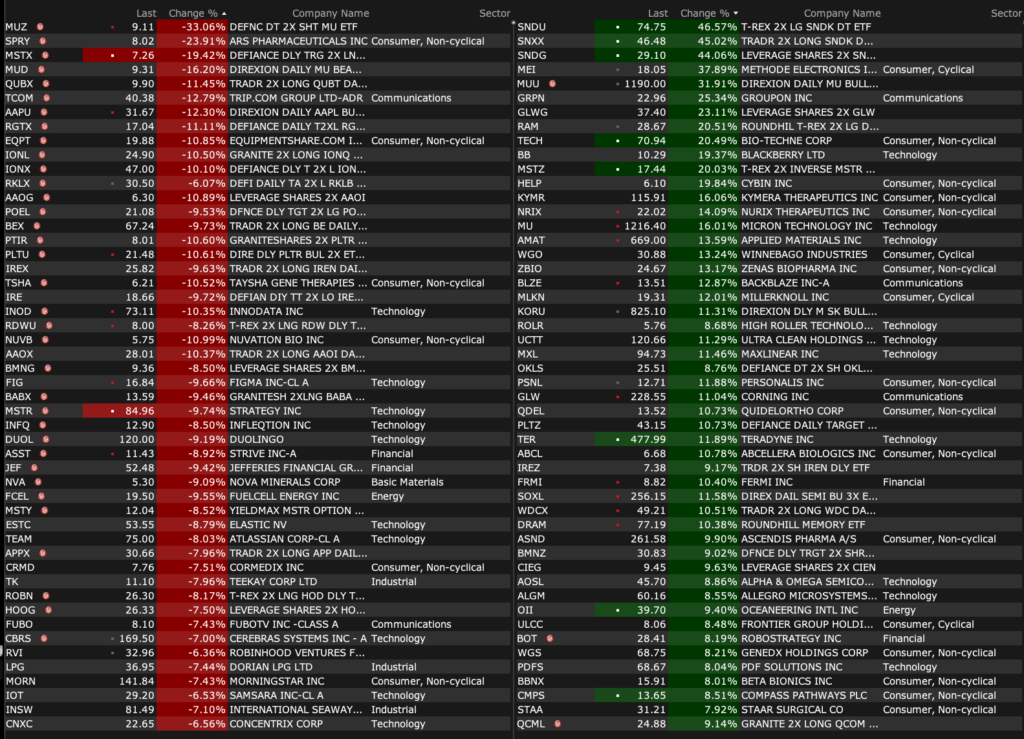

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · Jun 25, 2026, 4:40 PM EDT

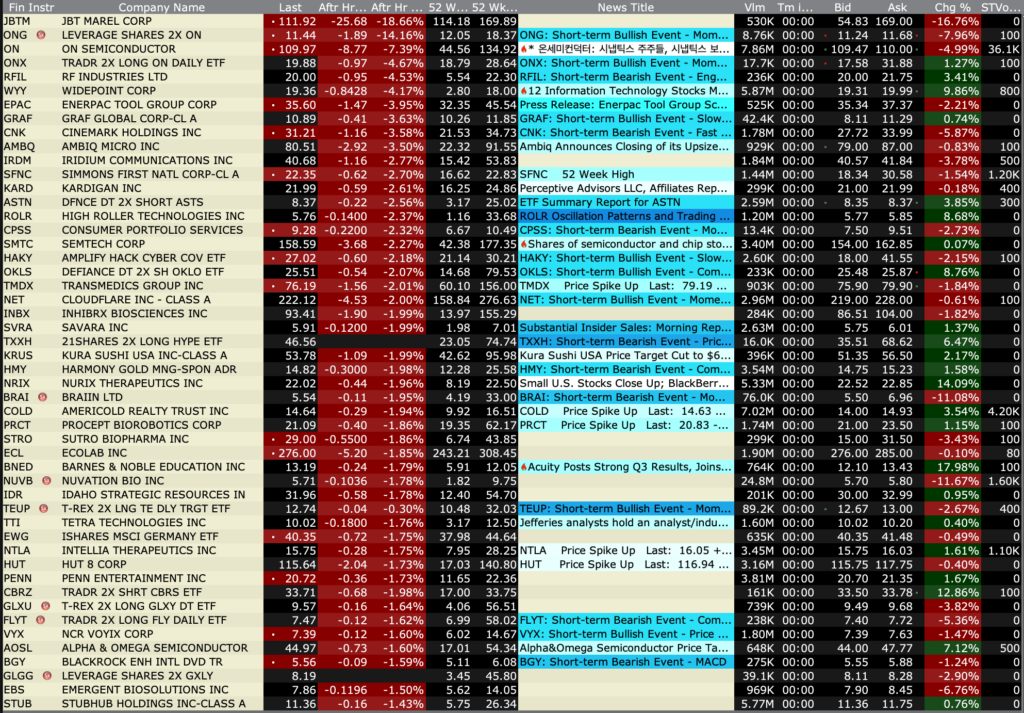

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · Jun 25, 2026, 4:40 PM EDT

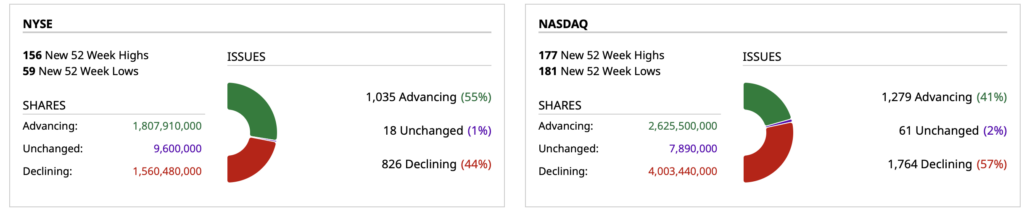

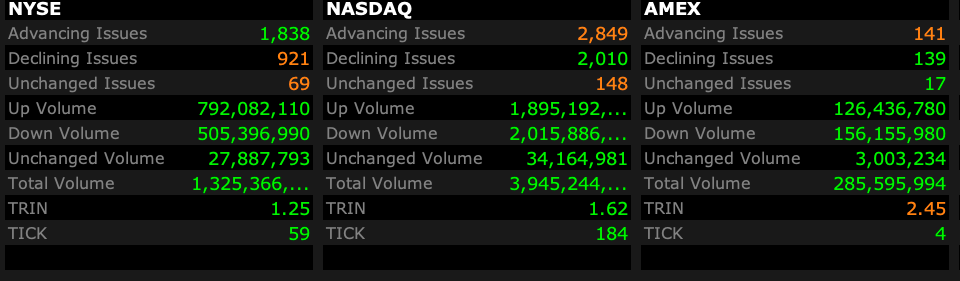

Closing Volume

– NYSE volume 9% below its one-month average

– NASDAQ volume 13% below its one-month average

– VIX Index: up 1.56% to 18.92

Breadth

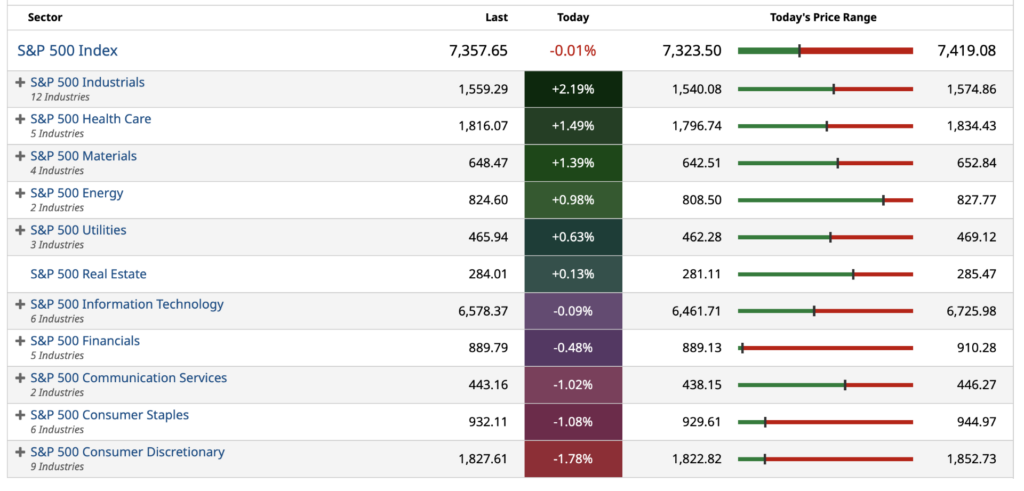

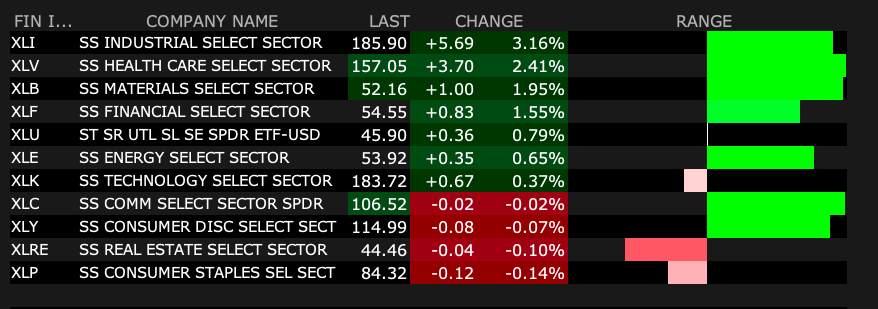

S&P 500 Sectors

% Movers

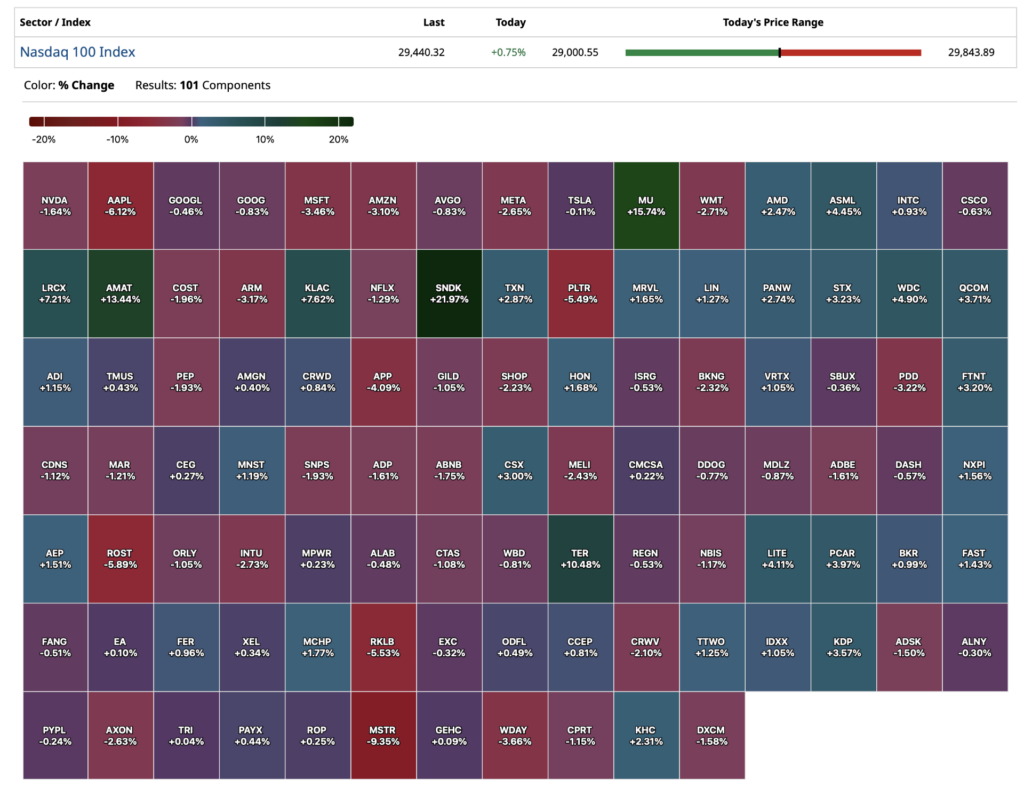

Nasdaq 100 Heat Map

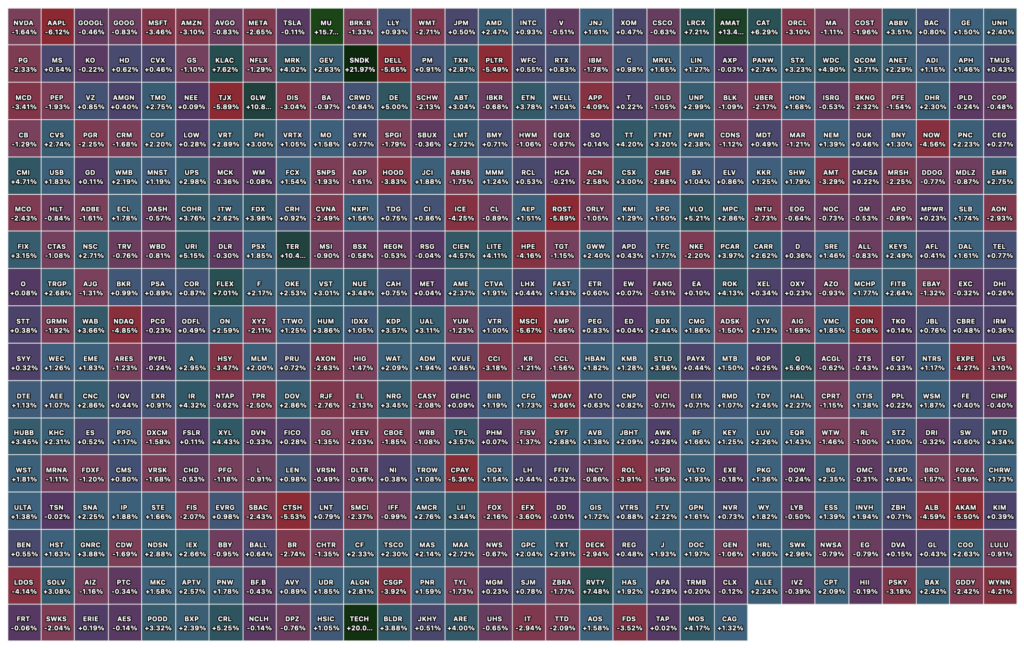

Closing S&P 500 Heat Map

Position: None

BY Doug Kass · Jun 25, 2026, 4:29 PM EDT

Disney continues to be a “dog with fleas.”

AI presents a threat to their movie business, high admission prices at theme parks and a large debt load remain my concerns.

Position: None

BY Doug Kass · Jun 25, 2026, 4:05 PM EDT

I truly think it is astonishing that, given the clear trend of Mag 7 from capital light to capital intensive (that I have been discussing ad nauseum for the last year), it is only now — with the stocks lagging so badly — that “talking heads” are becoming concerned.

Remember the battles in the Comments Section?

Crickets, now.

Position: None

BY Doug Kass · Jun 25, 2026, 3:35 PM EDT

Nvidia (NVDA) is trading -$5 to $194 today.

I wrote this yesterday when Nvidia was trading at $201:

I am not great on technicals.

But from a fractal standpoint, Nvidia (NVDA) broke an important technical line yesterday.

Position: None

BY Doug Kass · Jun 24, 2026, 9:27 AM EDT

Position: None

BY Doug Kass · Jun 25, 2026, 3:14 PM EDT

The bond market just went red.

And financials have reversed hard (e.g., Goldman Sachs)

Position: None

BY Doug Kass · Jun 25, 2026, 2:53 PM EDT

I have a 230 PM research meeting.

Back around 315 PM.

Til then, radio silence.

Position: None

BY Doug Kass · Jun 25, 2026, 2:25 PM EDT

Position: Long Cannabis

BY Doug Kass · Jun 25, 2026, 2:00 PM EDT

Position: None

BY Doug Kass · Jun 25, 2026, 1:50 PM EDT

Hyperscalers (“check writers”) vs. Chips (“check receivers”):

Position: None

BY Doug Kass · Jun 25, 2026, 1:40 PM EDT

At 12:52 PM:

Position: None

BY Doug Kass · Jun 25, 2026, 12:57 PM EDT

Position: Long Cannabis

BY Doug Kass · Jun 25, 2026, 12:45 PM EDT

Given the state of the average Joe (weakening), I disagree with Gene.

I am of the belief that demand elasticity will take hold after the large price increases in the Apple (AAPL) products:

Position: None

BY Doug Kass · Jun 25, 2026, 12:20 PM EDT

Positions: None.

BY Doug Kass · Jun 25, 2026, 11:45 AM EDT

Positions: None.

BY Doug Kass · Jun 25, 2026, 11:30 AM EDT

Market structure risks are mounting amid a casino-like backdrop.

Remember this column from earlier this month?

Dr Frankenstein: Now that brain that you gave me, was it Hans Del Brooks?

Igor: No.

Dr. Frankenstein: Would you mind telling me whose brain I did put in?

Igor: Abby someone.

Dr. Franksenstein: Abby, who?

Igor: Abby Normal – I am almost sure that was the name.

Dr. Frankenstein: Are you saying I put an abnormal brain into a 7 1/2 foot long, 54 inch wide gorilla?

– Young Frankenstein Abby normal scene

Consider the following price changes in today’s session:

* SNDK -$201

* MU -$101

* AMD -$51

* MRVL -$38

To me, this should make investors consider whether the market has been nothing more than a casino — in which the many momentum-based investors know everything about price but nothing about value.

And that, as I have observed, the concepts of risk vs. reward and “margin of safety” have been generally ignored.

Position: None

Position: None.

BY Doug Kass · Jun 25, 2026, 11:00 AM EDT

Adding to Mag7 on weakness and super sizing cannabis.

Positions: Long MSFT S AMZN S GOOGL S Cannabis

BY Doug Kass · Jun 25, 2026, 10:34 AM EDT

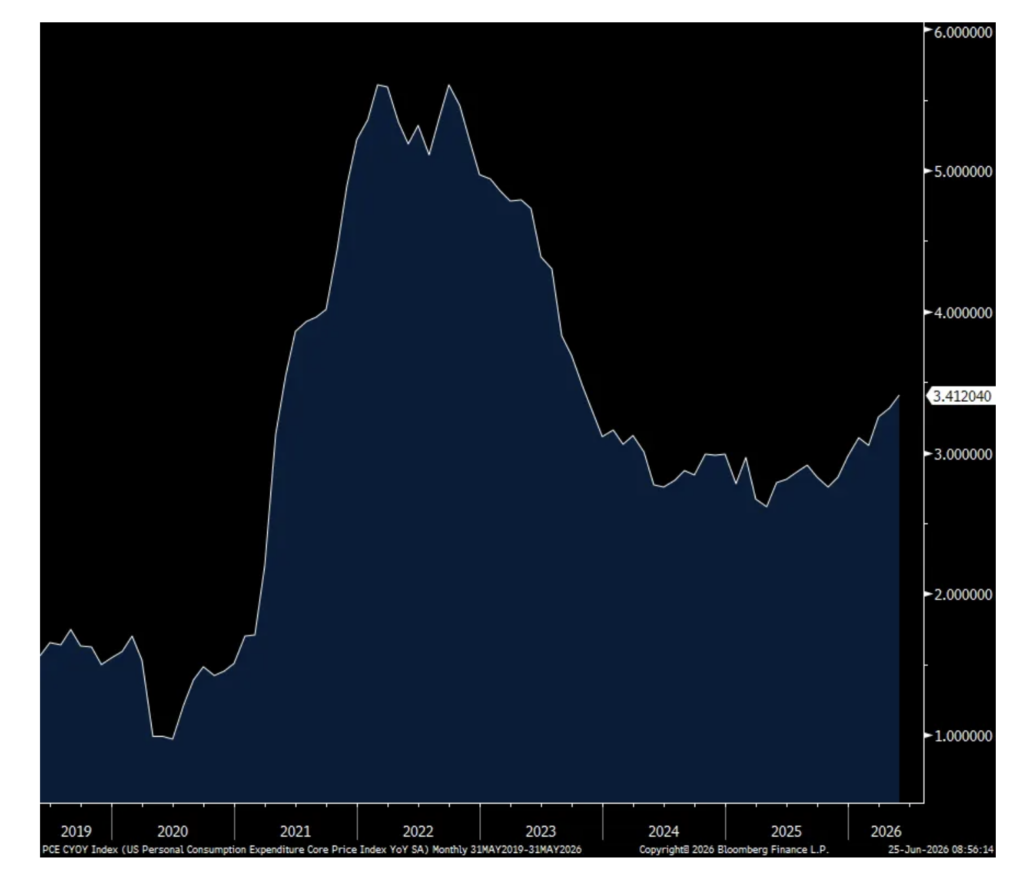

From Peter Boockvar:

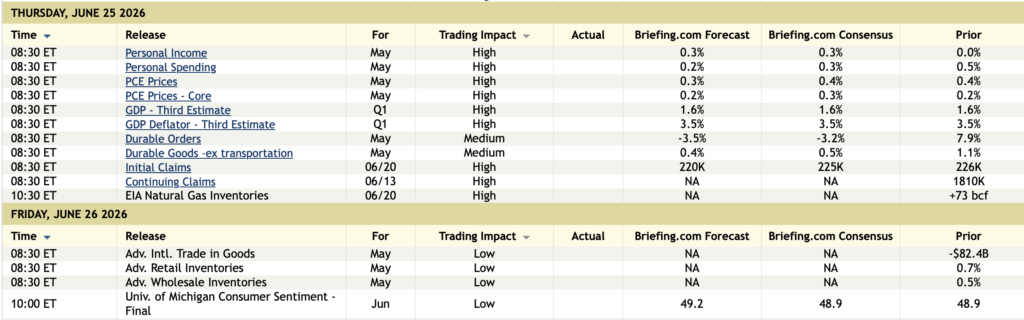

In May, the headline PCE rose .4% m/o/m and 4.1% y/o/y while the core rate was higher by .3% m/o/m and 3.4% y/o/y. Both about as expected due to rounding and up from 3.8% and 3.3% y/o/y gains seen in April. Of course oil prices have fallen sharply in June, making this data somewhat old news at the headline level. As CPI and PPI have already been seen, the PCE data rarely deviates from expectations.

Energy prices were up 4% in the month and by 24% y/o/y. Food prices grew by .6% m/o/m and 2.4% y/o/y. Goods prices for durable goods were up by 3.3% y/o/y. With services, prices were up by 3.8% y/o/y.

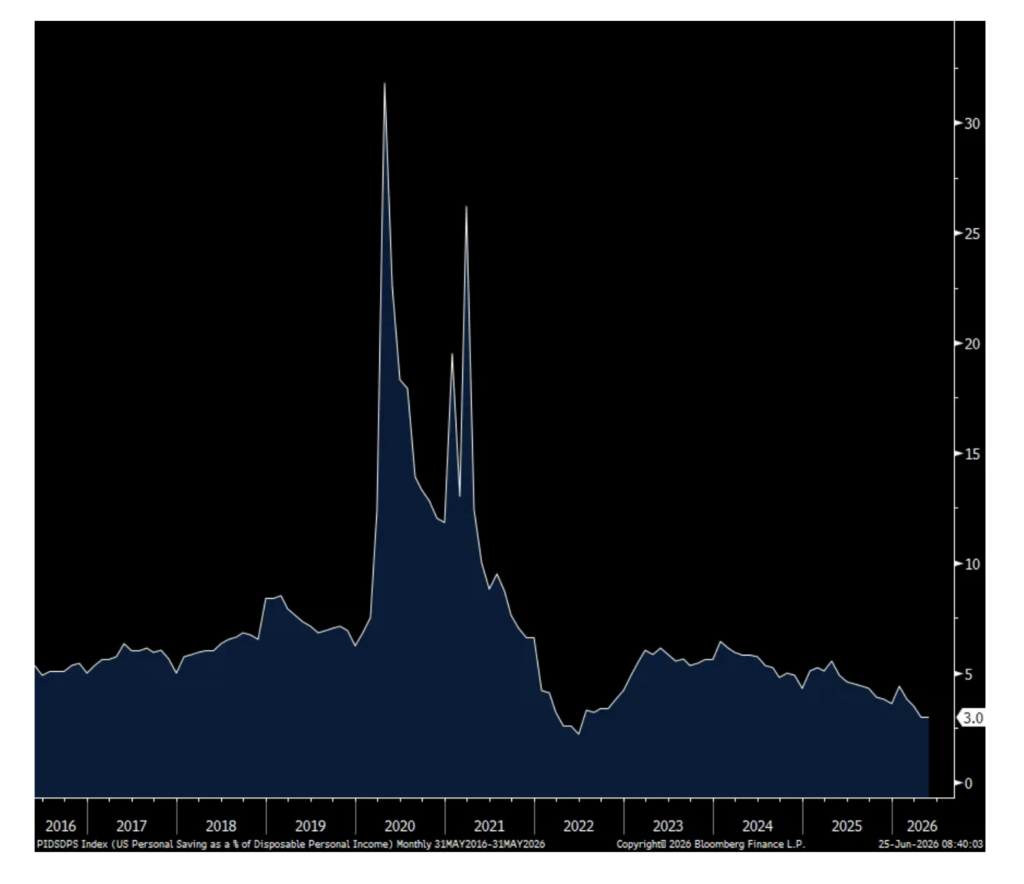

This matches up with an income rise of .7% m/o/m after no change in April while spending was higher by .7% m/o/m as expected when including the revision in the prior month. The savings rate at 3% combines this, unchanged with April but at the lowest level since June 2022.

With no surprise in the inflation stats and the anticipation of lower figures in the months to come, yields continue lower with the 2 yr yield now at 4.11%. That compares with 4.06% right before last week’s FOMC meeting and off the jump above 4.20% that followed. The 10 yr yield at 4.37% is now 6 bps below where it was before the meeting and further below the 4.50% key level.

Core PCE y/o/y

Savings Rate

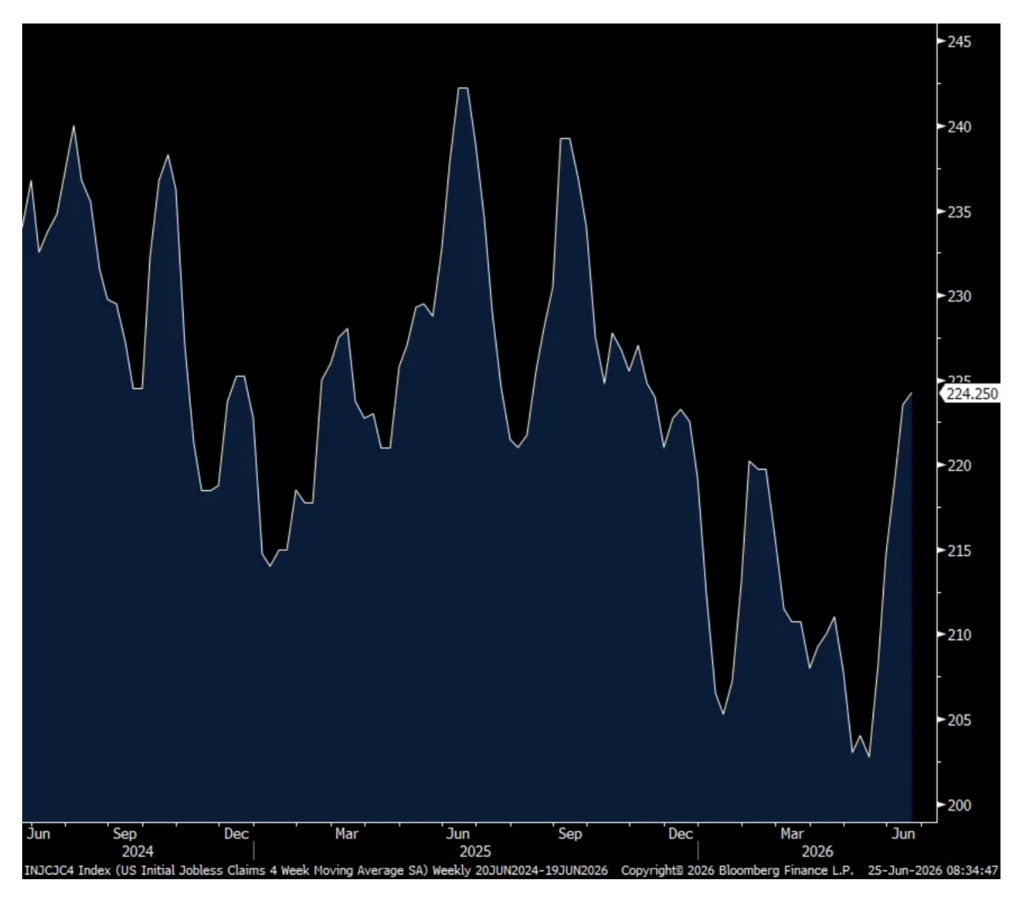

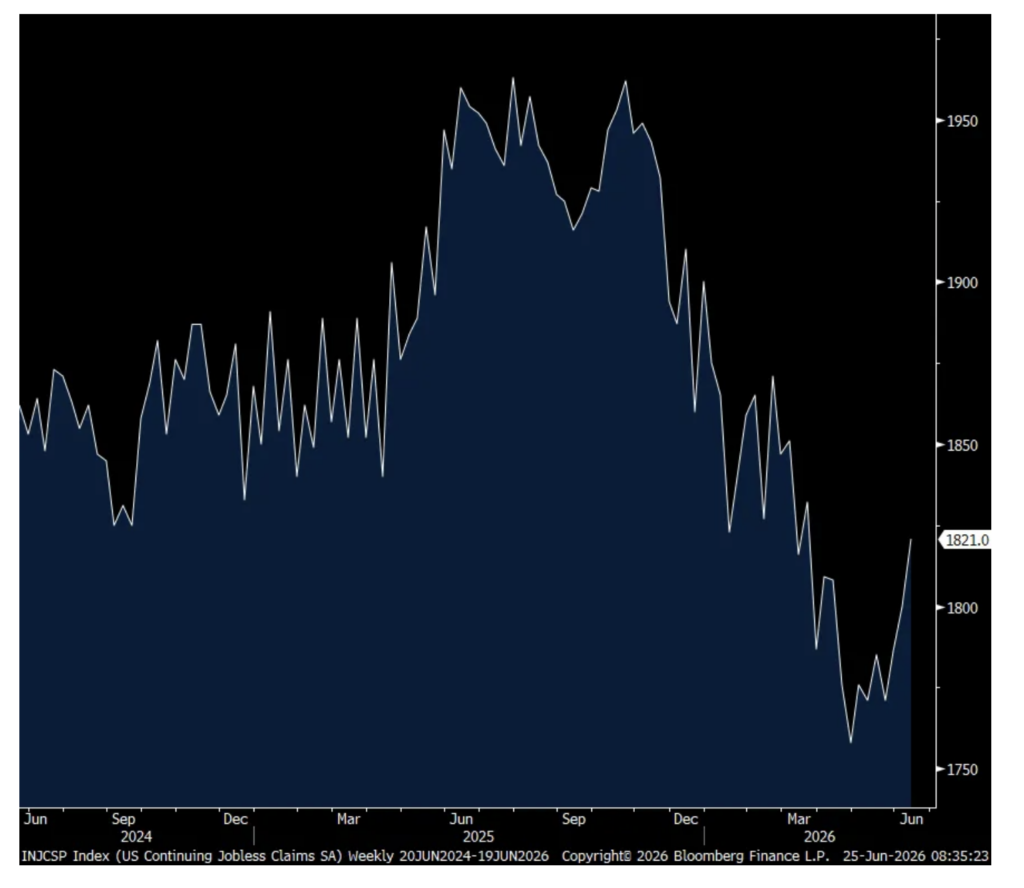

Initial jobless claims totaled 215k, 10k below expectations and down from 227k. Because of the holiday, we’ll combine this with next week’s print to smooth it out. Until then, the 4 week average of 224k is little changed with the previous week. Continuing claims, delayed by a week, totaled 1.821mm, up 21k w/o/w. That’s the highest since March but still well off its recent highs.

4 Week Avg Initial Claims

Continuing Claims

Core durable goods orders in May rose 1.6% m/o/m, well above the estimate of up .6% and follows a .7% fall in April (revised down from 1%). I still believe this includes some pull forward of orders. As part of the data center buildout, machinery orders were up another 1.9% m/o/m and 12.7% y/o/y. Orders for computers/electronics were up .3% m/o/m and 14.8% y/o/y. Electrical equipment orders rose .3% m/o/m and 5% y/o/y. Orders for metals too were strong in the month as you can’t build data centers without copper, silver, and other key minerals.

Shipments of core goods were as expected so won’t shift Q2 GDP estimates.

Positions: None.

BY Doug Kass · Jun 25, 2026, 10:14 AM EDT

From Peter Boockvar:

With WTI crude oil now just about $3 from where it was before the Middle East conflict began, the 14 day Relative Strength Index is now at the lowest since September 2020, when we were slowly coming out of Covid but before the vaccine news. The Daily Sentiment Index is down to just 12 (range of 0-100), according to my friend Helene Meisler. I still think prices eventually settle out in the $80s but no question I’m very surprised at how much they’ve fallen. By the way, the Daily Sentiment Index for gold and silver are now down to just 10 and the DXY is up to 83. All stretched readings.

The Dallas Fed released its quarterly energy survey and said this:

“Activity in the oil and gas sector jumped in second quarter 2026, according to oil and gas executives responding to the Dallas Fed Energy Survey. The business activity index, the survey’s broadest measure of the conditions energy firms face in the Eleventh District, increased from 21.0 in the first quarter to 46.1 in the second quarter, marking the strongest reading since second quarter 2022. The survey was in the field June 9–17 as the U.S. and Iran negotiated a memorandum of understanding about ending hostilities.”

And, “Oil production advanced modestly in the second quarter, while natural gas production saw only minimal gains, according to executives at exploration and production (E&P) firms. The oil production index increased from zero in the first quarter to 15.0 in the second quarter, whereas the natural gas production index remained relatively unchanged at 3.7.”

With input inflation, “Costs increased at a faster pace relative to the prior quarter. Among oilfield services firms, the input cost index surged from 34.9 to 64.4, with no respondents reporting a decrease in costs. Among E&P firms, the finding and development costs index increased from 22.3 to 40.0. Meanwhile, the lease operating expenses index rose from 30.0 to 43.7. All cost indexes were above their series averages, suggesting costs are growing at a faster-than-average pace.”

And where respondents think prices settle out at, “On average, respondents expect a West Texas Intermediate (WTI) oil price of $81 per barrel at year-end 2026; responses ranged from $60 to $150 per barrel. When asked about longer-term expectations, respondents on average said they expect a WTI oil price of $78 per barrel two years from now and $82 per barrel five years from now. Survey participants foresee a Henry Hub natural gas price of $3.36 per million British thermal units (MMBtu) at year-end 2026.” I bolded.

Micron certainly crushed it with their quarterly earnings, though I still wonder to the extent they’re seeing double and triple ordering. Coincident with the booming business we know is the also high level of speculation particularly in the South Korean Kospi (up 5% overnight) and the trading in Samsung and SK Hynix where each now have 2x leveraged ETFs and margin debt there is at a record high (as it is in the US at 4.5% of GDP).

If you didn’t see, this was an article in yesterday’s FT, “South Koreans pour AI stock windfalls into overheated property market.” It said, “Securities sales proceeds were used in 13.2% of home purchases worth more than Won1.5bn ($974,000) in April, according to data from the land ministry, the first time the figure reached double digits and nearly triple the monthly level in most of the past five years.”

“For years, South Korea’s government has struggled to convince its citizens to invest more in domestic equities and less in the overheated property market, which it blames for rising inequality and plunging birth rates as elevated housing costs deter couples from starting families.”

“Despite the (equity) rally, property still accounts for 75% of household wealth, far above levels in other rich countries and dwarfing the 9% held in equities,” according to Morgan Stanley.”

https://www.ft.com/content/4a7137ff-903f-4246-96bf-4919ccb53543?syn-25a6b1a6=1

Back to Micron, this of note from their earnings call:

“DRAM and NAND industry demand continues to significantly exceed industry supply. We expect tight conditions to persist beyond calendar 2027, as a result of AI driven demand across all segments, coupled with structural supply.”

“We are excited to announced that we have now signed 16 strategic customer agreements or SCAs, which we expect will fundamentally transform our business model. The memory industry has been structurally transformed by the proliferation of AI.”

With regard to these SCA’s, Micron is saying that they “cannot be canceled…These are designed to be take-or-pay agreements outside of automotive.” And, “There are annual volume commitments for each of those years (5)” and “they are obligated to pay for the price times the volume. The price itself for a lot of these large agreements has a price band. There is a price ceiling and a price floor. The price gets negotiated every quarter based on market conditions. The price cannot exceed the ceiling no matter what, cannot go below the floor no matter what, and consequently the value of these agreements can be readily determined.”

“We now expect supply demand conditions for both DRAM and NAND to remain tight beyond calendar 2027. In DRAM, we expect industry DRAM bit shipments in calendar 2026 to grow in the low-to-mid 20s percentage range, slightly above our prior outlook. In NAND, we expect industry NAND bit shipments in calendar 2026 to grow approximately 20%, unchanged from prior expectations.”

The operating margin of 81.2% is astonishing, “up 12 percentage points sequentially and 54 percentage points y/o/y.” The gross margin was 85% and they expect “approximately” 86% in the current quarter. I’ll add, incredible but will be tough to increase them further from here.

They did get a question about the competition from the Chinese, CXMT and Yangzte, something I mentioned this week. “I mean, certainly those two companies have grown over the years in terms of their capabilities and share. Most of their output, the overwhelming majority of their output tends to be sold within China. We haven’t really seen much by way of their product or competition from them outside of China.” I’m sure that will change in the coming years though.

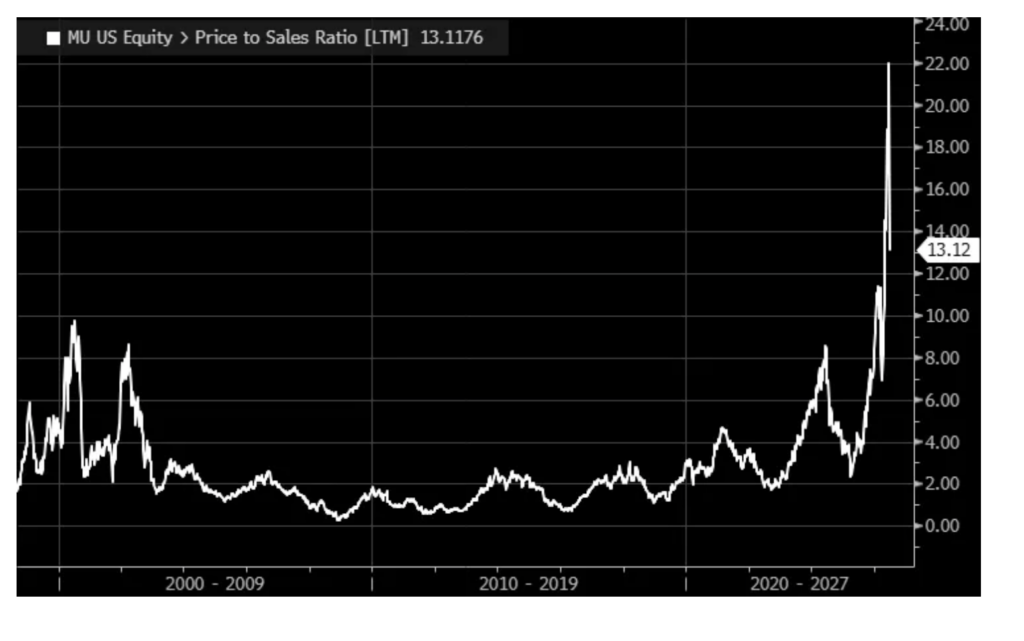

I will finish with Micron on the valuation debate. When analyzing a highly cyclical business and looking at a one year P/E ratio, it is a very incomplete picture when margins are very high, typically temporarily. I believe a better view is looking at Price to Sales and for Micron that sits at about 10x for their expected fiscal year. For perspective, it peaked at 10x price to sales in 2000.

Maybe this time is different and their business is structurally more sound. I have no opinion on that nor on the stock but just wanted to widen the debate on valuation because a P/E ratio on one year of earnings for a highly cyclical business is something I saw in 2005-2006 when I heard about how cheap homebuilder stocks were then. That of course was because they were dramatically over-earning.

Ignore the spike below as it’s calculating LTM and I’m talking about full fiscal year figures.

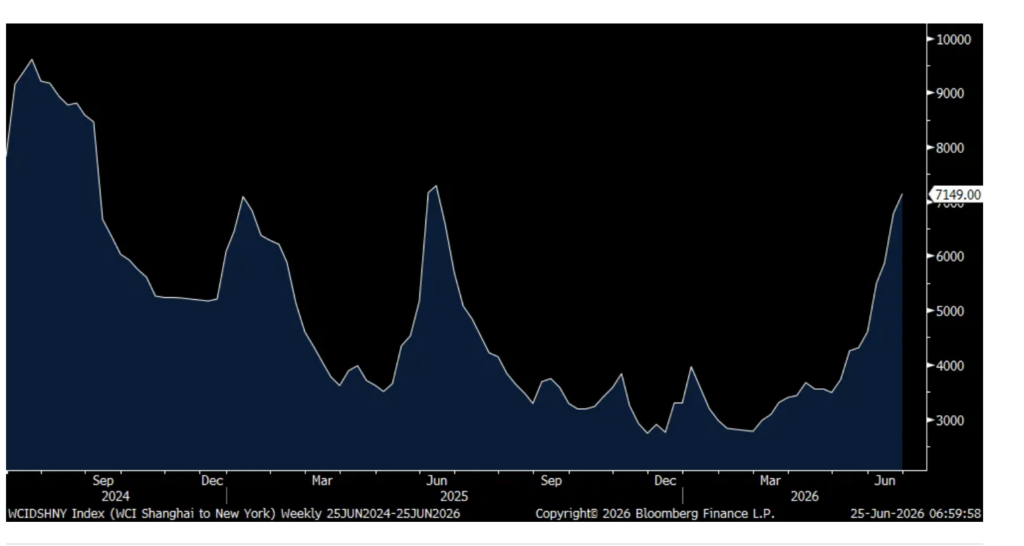

Hopefully we’ll get some relief soon with the Strait reopening but at least thru 6/25, container shipping prices continue to jump. The Shanghai to NY trip rose another 5.6% w/o/w, up for an 8th straight week to $7,149 for a 40 foot container. That’s the highest since last June. The price for the route to LA rose by a similar amount and less so to Rotterdam.

Shanghai to NY

Positions: None.

BY Doug Kass · Jun 25, 2026, 9:35 AM EDT

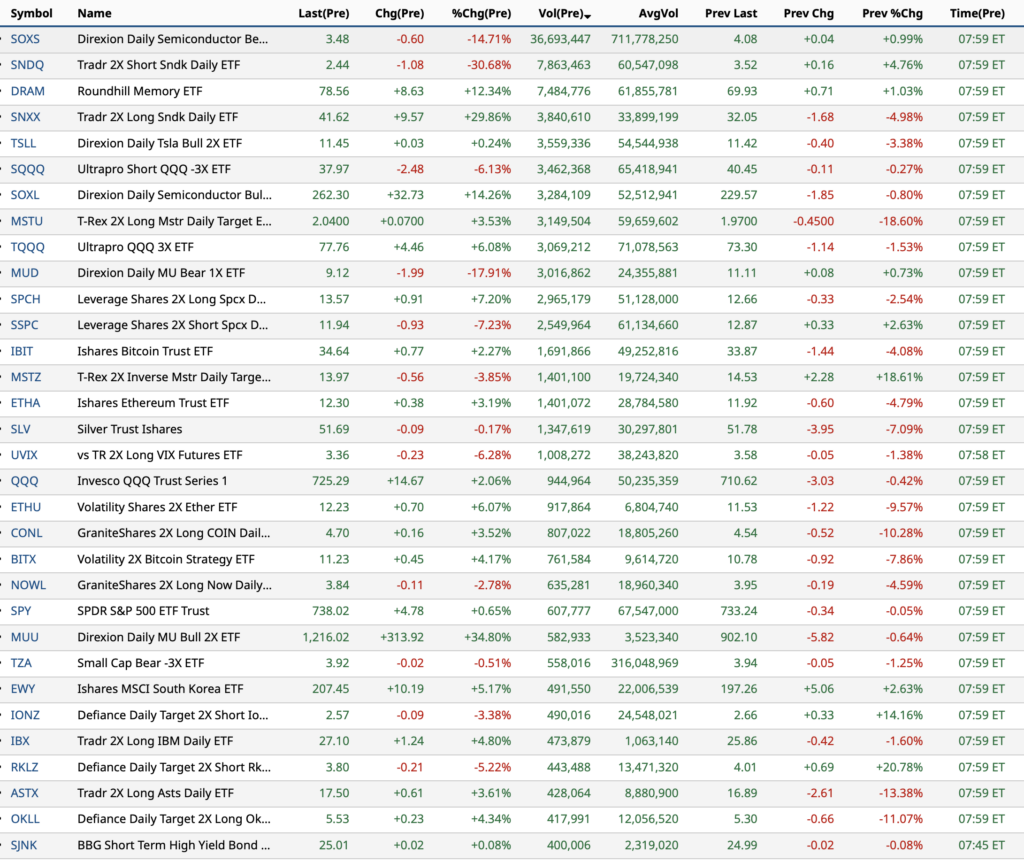

-WYY +45% (selected as the single awardee for 10-yr, $3.1B DHS Cellular Wireless Managed Services 3.0 IDIQ contract)

-TECH +19% (offered to be acquired by Merck KGaA at $73/shr in $11.3B cash deal)

-MU +17% (earnings, guidance)

-SNDK +15% (higher in sympathy with MU)

-WDC +12% (higher in sympathy with MU)

-KYMR +10% (completes enrollment in the Phase 2b BROADEN2 Trial of KT-621 in Atopic Dermatitis with topline data by year-end 2026)

-QCOM +10% (strength following Investor Day, guidance)

-SNX +8.4% (earnings, guidance)

-WEN +7.1% (meme momentum)

-BB +7.0% (earnings, guidance)

-UMAC +4.8% (signs lease for 14K sq ft Orlando manufacturing and operations facility)

-STM +4.0% (higher in sympathy with MU)

-MKC +3.0% (earnings, guidance)

-MDA +2.8% (selected by Mitsubishi Electric for next gen defence communications satellite program)

-IBM +2.7% (unveils sub-1 nm chip technology with 0.7 nm node and new nanostack architecture)

-VC +2.4% (authorizes $800M share repurchase program)

-SPCX +2.3% (momentum)

-ELME -28% (terminates Purchase Agreement with Riverside Apartments)

-SPRY -25% (no new formulary additions for neffy in July 1, 2026 cycle)

-FUL -10% (earnings, guidance; Ancora criticizes H.B. Fuller pursuit of Advanced Medical Solutions acquisition)

-TSHA -5.6% (prices $200M public offering of common stock and pre-funded warrants at $6.00/share)

-WGO -3.0% (earnings, guidance)

-DLTR -2.8% (to repurchase $500M of common stock alongside secondary block trade)

-DRI -2.6% (earnings, guidance)

-PVH -2.4% (Tier1 firm Cuts PVH to Underperform from Neutral, price target: $70 from $90)

BY Doug Kass · Jun 25, 2026, 9:33 AM EDT

Positions: None.

BY Doug Kass · Jun 25, 2026, 9:11 AM EDT

Positions: None.

BY Doug Kass · Jun 25, 2026, 8:43 AM EDT

Positions: None.

BY Doug Kass · Jun 25, 2026, 8:33 AM EDT

11:00 a.m.: Treasury announces a 3 and 6 month bill auction and a 6-Week Bill Auction;

11:30 a.m.; Treasury hosts a $70B 4 and a $75B 8 Week Bill Auction;

1:00 p.m.: Treasury hosts a $44B 7-Year Note Auction; 2:00PM: Treasury buyback (liq support);

2:00 p.m.: Fed Bank of Chicago President Goolsbee (Non-Voter) Television Appearance — CNBC;

3:40 p.m.: Fed Bank of New York President Williams (Voter) gives keynote before the Crane Money Fund Symposium organized by Crane Data, Jersey City, NJ (Text and moderated Q&A expected);

6:30 p.m.: Fed Bank of Chicago President Goolsbee (Non-Voter) participates in moderated question-and-answer session before hybrid Chicago Council on Global Affairs Global Economy Dialogue Series, Chicago, IL (Livestream available. Embargoed text TBD)

Positions: None.

BY Doug Kass · Jun 25, 2026, 8:21 AM EDT

Position: None

BY Doug Kass · Jun 25, 2026, 7:30 AM EDT

I have cautioned about private equity markets for years:

Position: None

BY Doug Kass · Jun 25, 2026, 7:05 AM EDT

Position: None

BY Doug Kass · Jun 25, 2026, 6:55 AM EDT

Position: None

BY Doug Kass · Jun 25, 2026, 6:45 AM EDT

Position: None

BY Doug Kass · Jun 25, 2026, 6:35 AM EDT

Added to MSFT at $364.65, AMZN at $234.23 and GOOGL at $340.73.

Position: Long MSFT (S), AMZN (S), GOOGL (S)

BY Doug Kass · Jun 25, 2026, 6:25 AM EDT

I have been bearish on Bitcoin for years.

As with most asset classes in markets that are dominated by those that worship at the altar of price momentum, the price of Bitcoin is collapsing:

Position: None

BY Doug Kass · Jun 25, 2026, 6:15 AM EDT

Position: Long GLASF

BY Doug Kass · Jun 25, 2026, 6:05 AM EDT

Position: Long MSFT (VS)

BY Doug Kass · Jun 25, 2026, 5:55 AM EDT

The S&P Short Range Oscillator remains overbought at 1.85% vs. 2.44%

Position: None

BY Doug Kass · Jun 25, 2026, 5:45 AM EDT

An almost perfect prediction of the current AI predicament — and what may ultimately unravel our entire economy — from almost three years ago (August 2023), at Marcus on AI: Nearly every word remains true.

This was very well done $Glasf @realsteveeisman @kylekazanceo @grahamfarrar

Despite the sharp fall in oil prices, the market is pricing in one and a half rate hikes by the Fed this year (Bloomberg data below). Meanwhile, several Fed watchers have revised up their rate expectations, with at least one opting for three (yes, three) hikes this morning. On my Show more

⚠️HOLY COW: US leveraged ETF assets under management (AUM) hit a record $198 BILLION. This figure has more than DOUBLED since the 2022 bear market. AUM in the 3x Leveraged Long Nasdaq 100 ETF, $TQQQ, alone is ~$40 billion. At the same time, AUM in the 3x Leveraged Long

DOJ investigating odd stated NAV behavior by one the largest private credit funds. Ever larger redemption requests across private credit each quarter. Lawsuits alleging valuation fraud and less than stellar liquidity feature explanations. “Don’t worry. Everything’s fine.”

Maybe instead of venting daily and complaining about the formulaic programming and too often BS narratives on Fin TV (read @cnbc) - which are harmful to the finances of its viewers - I am considering highlighting the most wrong footed recommendations from panelists (once a day).

Nvidia $NVDA is underperforming the rest of the Semiconductor Stocks by the largest margin in 2.5 years 🚨🚨

Breaking: The Magnificent 7 have lost over ~$5,000,000,000,000 of market capitalization from their all-time highs • Microsoft: -32.2% • Meta: -31.0% • Tesla: -18.2% • Nvidia: -17.5% • Amazon: -16.5% • Alphabet: -16.1% • Apple: -8.7%

Compelling Cannabis Chronology * Cannabis is (by far) my favorite market sector for the second half of 2026 $MSOS * Upside reward is 5x v risk, imho.... 1. Buybacks Now In Place (Company managements see value) 2. Trulieve and Glass House Start the Flood of NYSE and Nasdaq Show more

Gonna Fly Now <Cannabis upside reward> "Getting Even More Chai" now on the blog tab of seabreezepartnerslp.com

A Trump advisor tells The Marijuana Herald that the president “continues to support cannabis banking reform, including legislation filed today in the Senate.” The advisor said Trump plans to publicly back it, likely after the rescheduling process concludes.themarijuanaherald.com/2026/06/trump-…