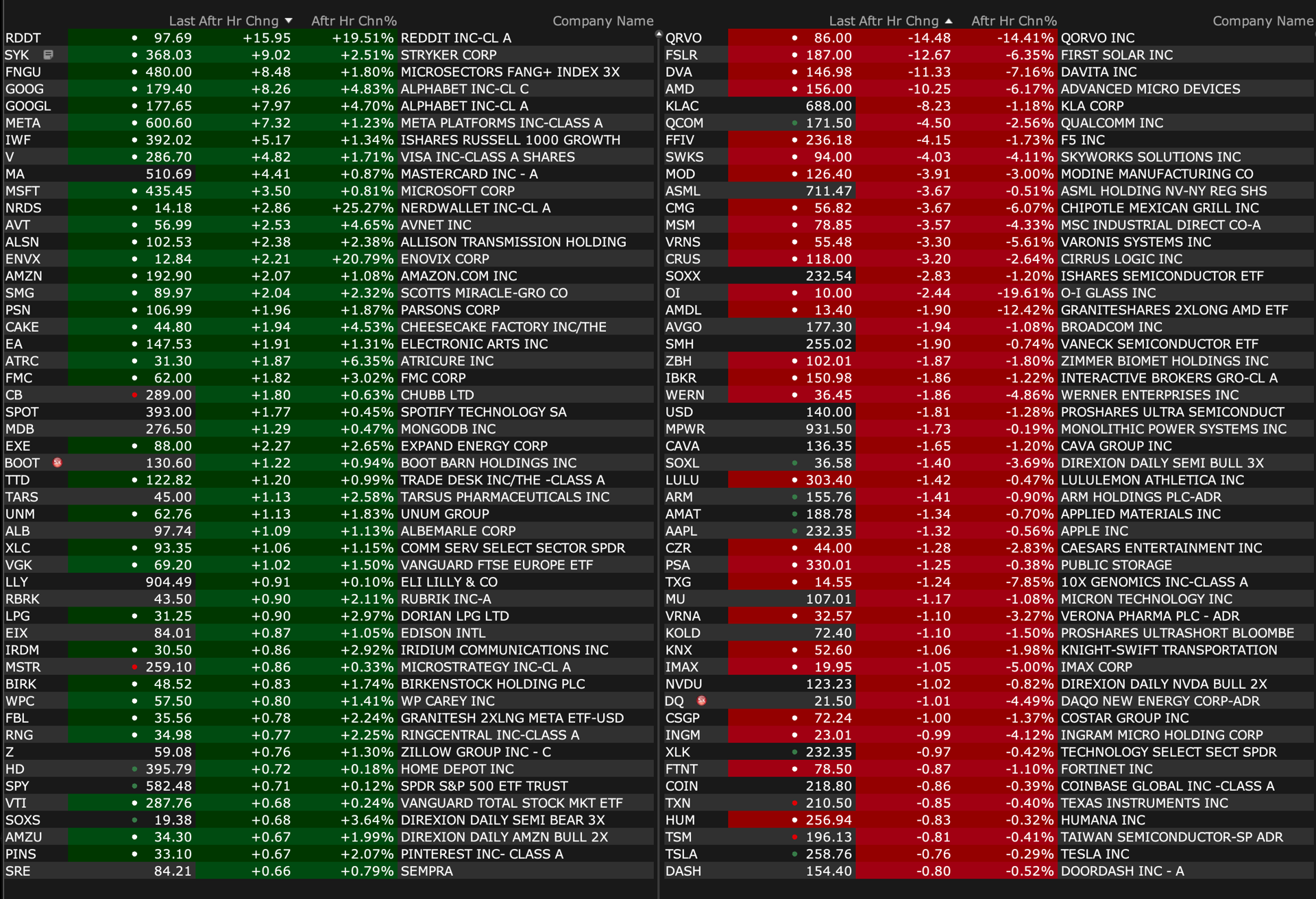

After-Hours Movers

As of 4:34 p.m.

BY Doug Kass · Oct 29, 2024, 4:46 PM EDT

As of 4:34 p.m.

BY Doug Kass · Oct 29, 2024, 4:46 PM EDT

BY Doug Kass · Oct 29, 2024, 4:25 PM EDT

I am out of my CMG long at $59.12 after the revenue miss.

BY Doug Kass · Oct 29, 2024, 4:16 PM EDT

BY Doug Kass · Oct 29, 2024, 3:20 PM EDT

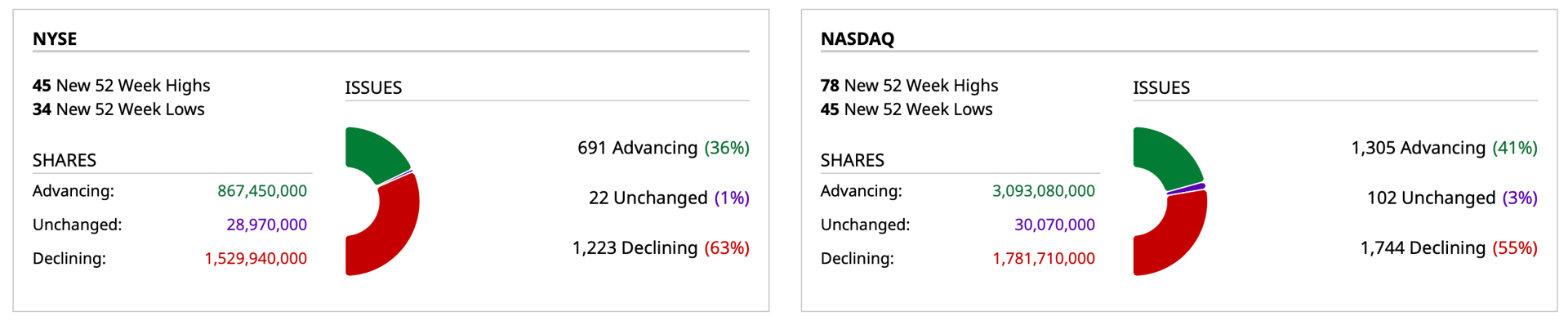

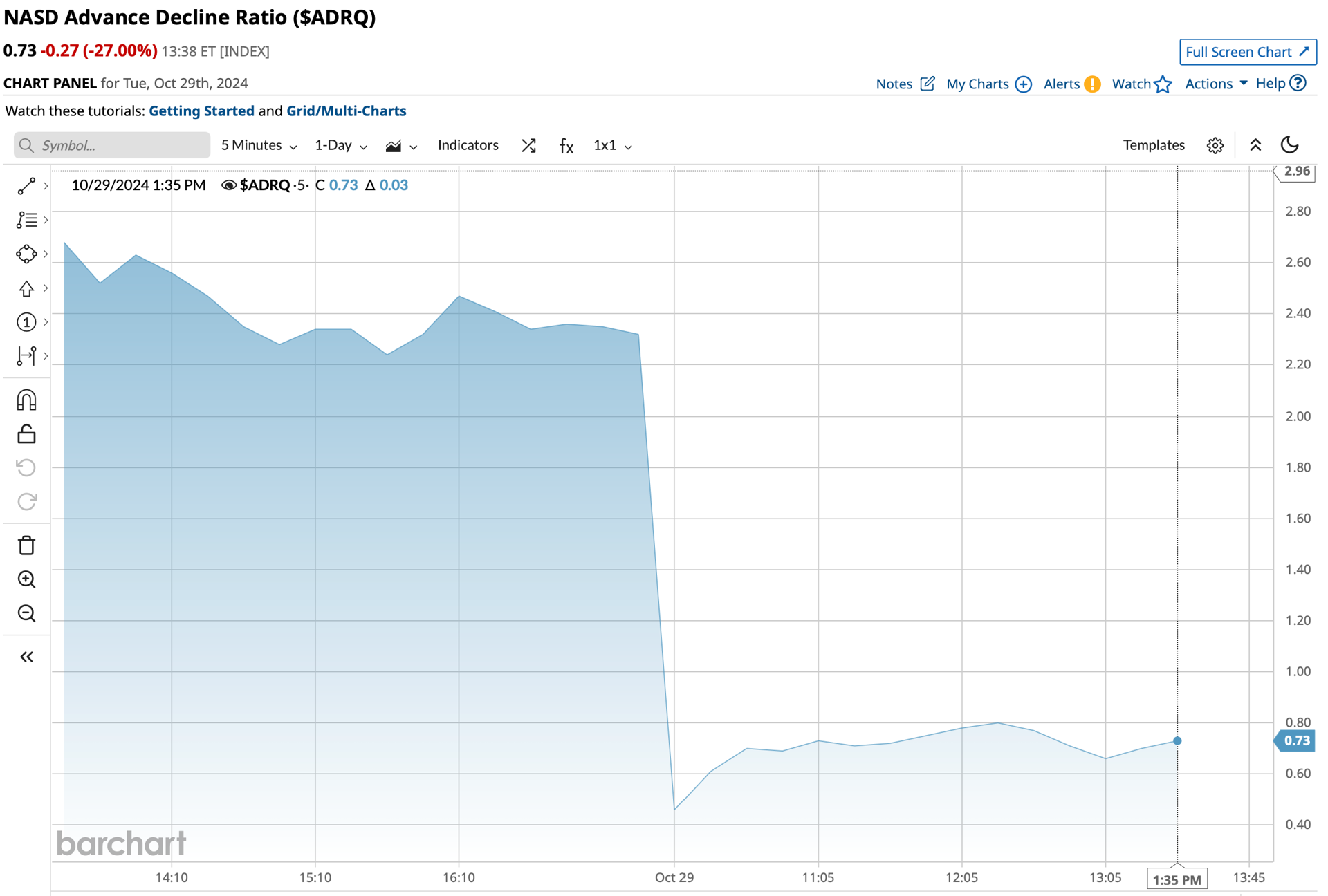

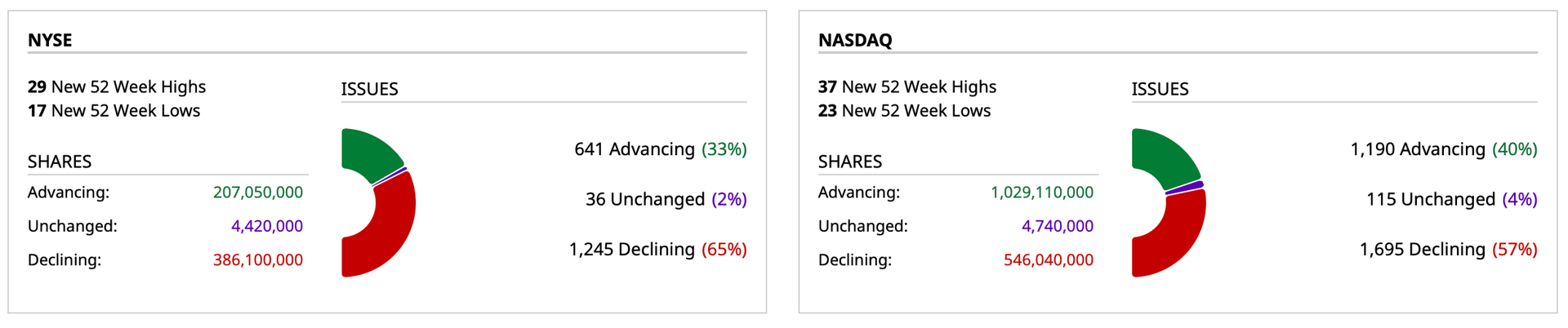

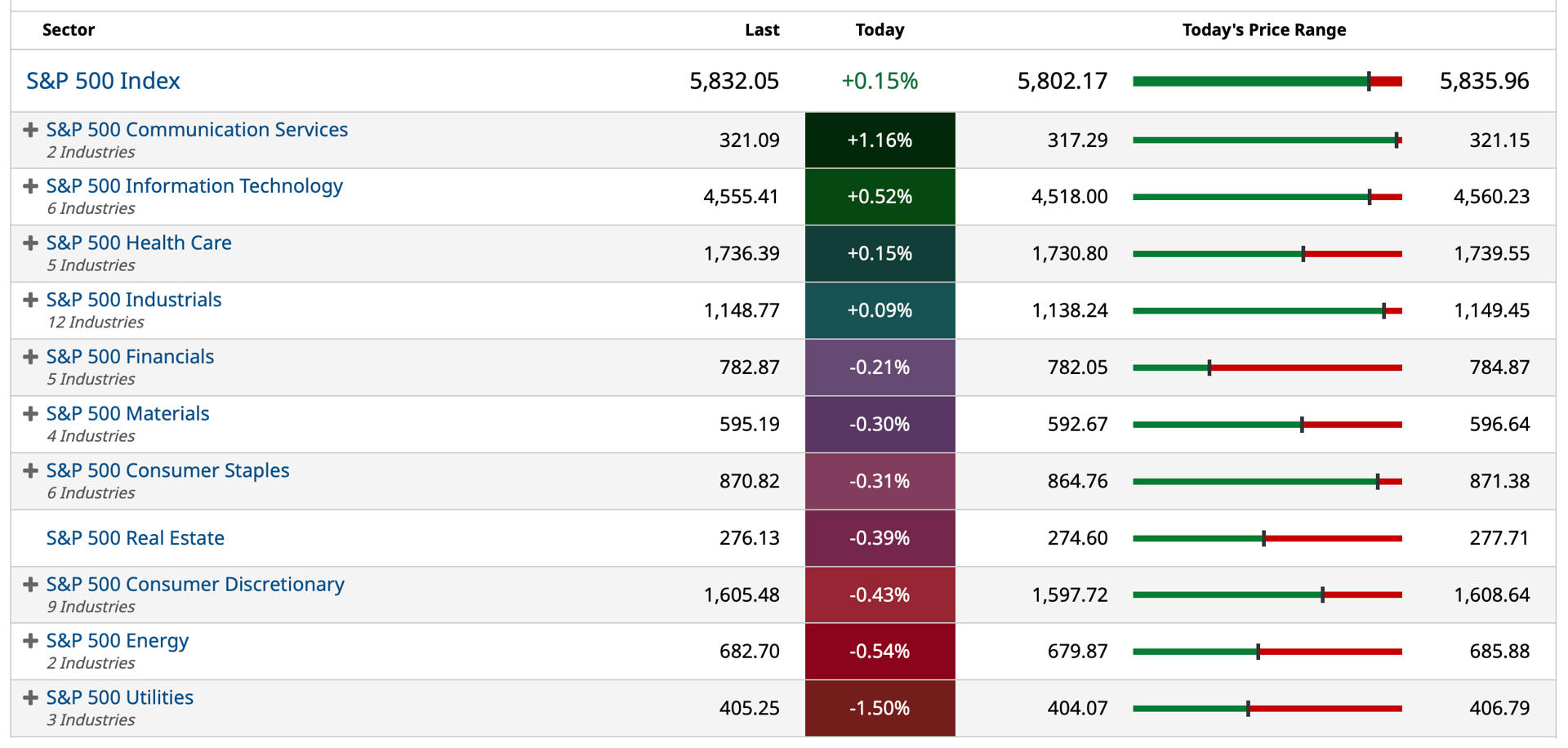

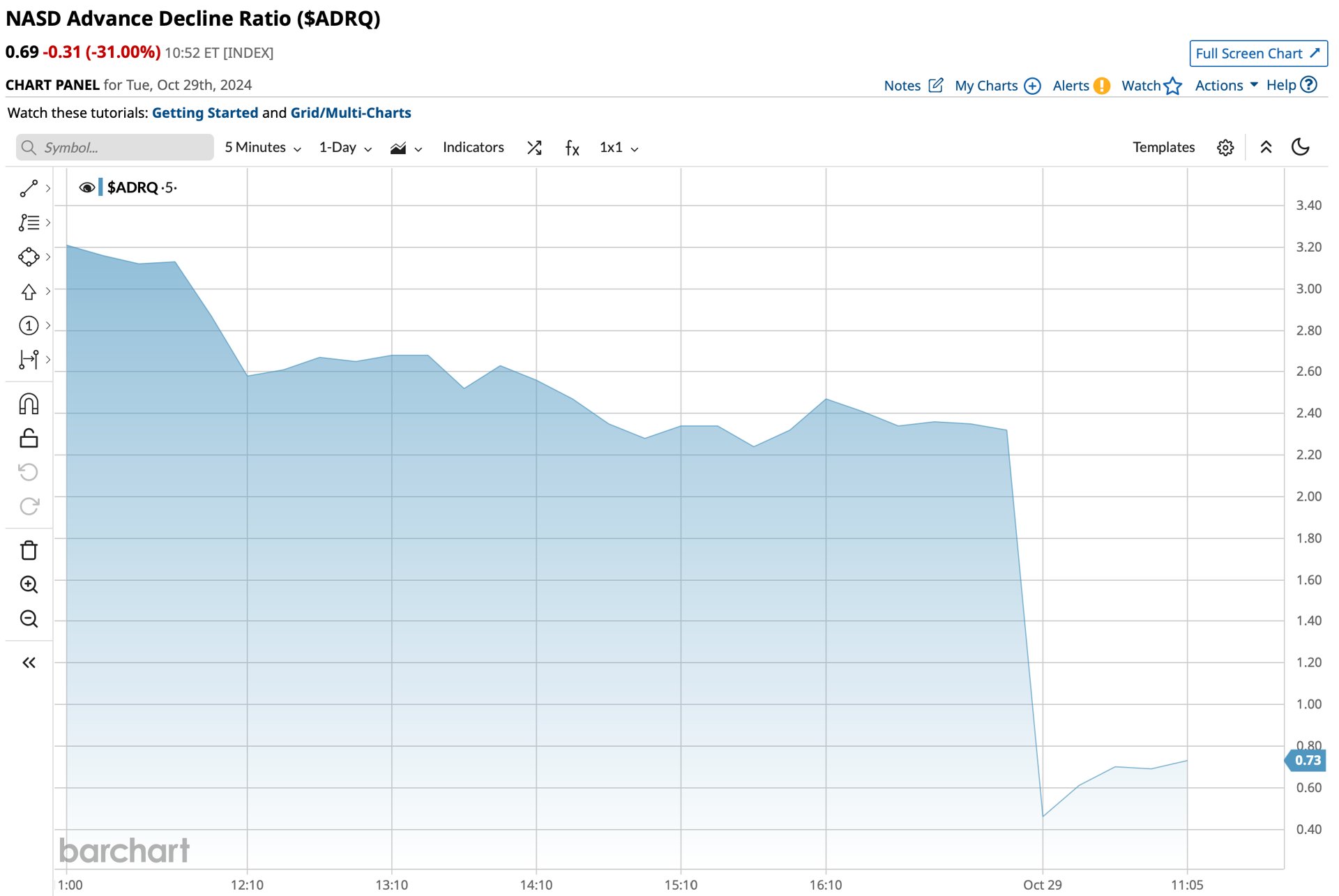

At 2:45 p.m. the S&P Index is +20 handles — rising steadily during the afternoon as breadth remains flat and shows little improvement (see last post, Voof!)

Both the equal weighted S&P (-0.12%) and the Russell Indices (-0.36%) are down modestly on the day. The S&P is unchanged, while the Nasdaq is up +0.97% ten lengths as we approach the top of the stretch.

Mostly research today and very little trading/investing.

Today's "things":

* I sold some Index common very early in the morning and took them back for a small profit. As the market ripped from the lows I added to my short Index calls.

* I covered over 90% of my homebuilder shorts right after the market opened at very good prices (and at the day's lows).

BY Doug Kass · Oct 29, 2024, 3:03 PM EDT

From Peter Boockvar:

With the big back up in long rates with Treasuries now oversold as stated this morning (and thus expecting a bounce) and ahead of the jobs data, the 7 yr note auction was solid. The yield of 4.215% was 2 bps below the when issued pricing. The bid to cover ratio of 2.74 was the highest since the global Covid panic in late March 2020. Before that, go back 12 years to see a higher ratio. Also, direct and indirect bidders took down a combined 92.5% of the auction, the most since January 2023.

Bottom line, this was a great auction and Treasuries are rallying off their lows in response though long end rates are still up on the day.

7 yr yield

Bid to Cover

BY Doug Kass · Oct 29, 2024, 2:40 PM EDT

Dr. Frederick Frankenstein: For the experiment to be a success, all of the body parts must be enlarged.

Inga: His veins, his feet, his hands, his organs vould all have to be increased in size.

Dr. Frederick Frankenstein: Precisely.

Inga: [her eyes get wide] He vould have an enormous schwanzschtücker.

Dr. Frederick Frankenstein: [ponders this a moment] That goes without saying.

Inga: Voof.

Igor: He's going to be very popular.

- Young Frankenstein Enormous Schwanzstucker

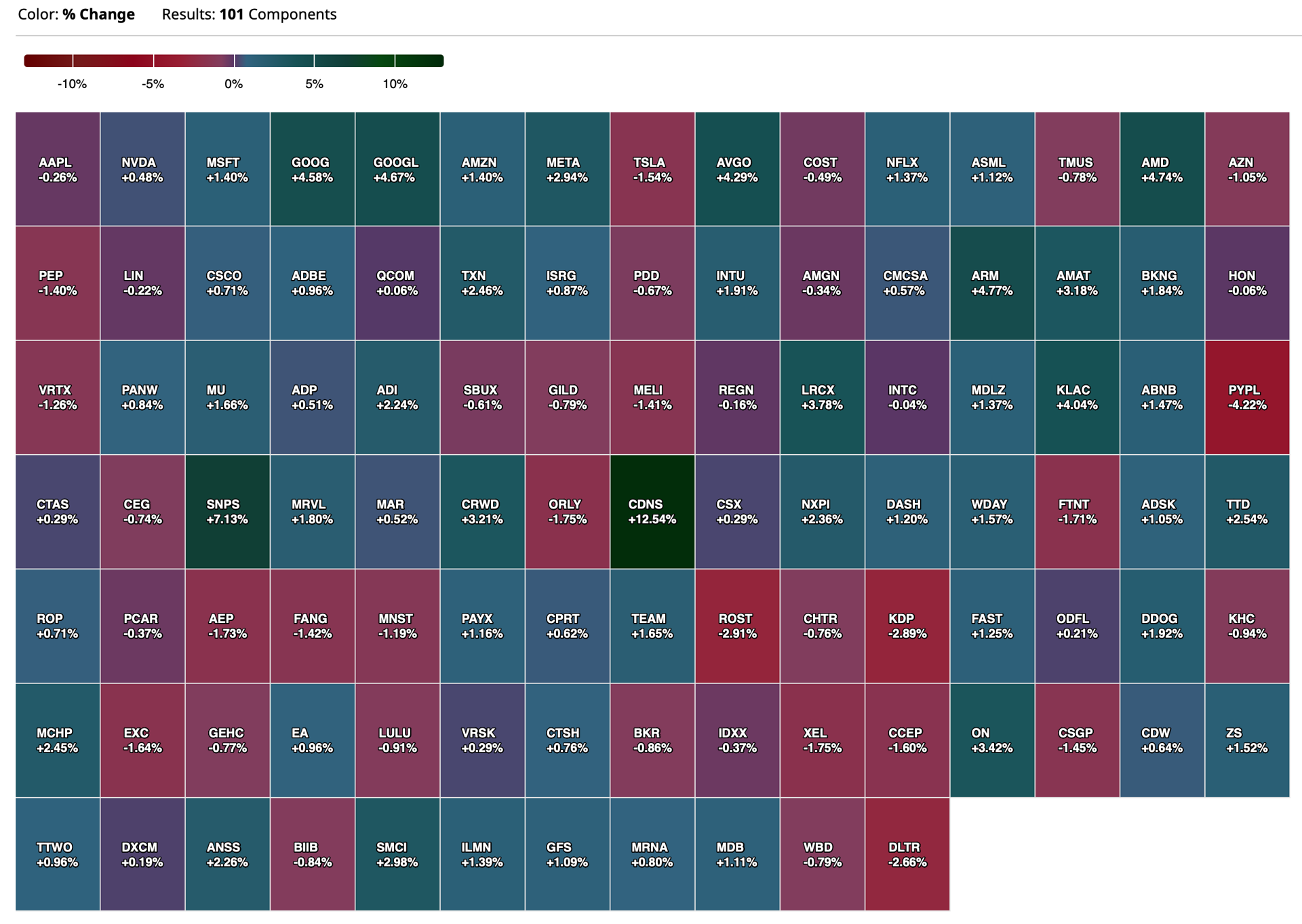

The market continues to move back to all-time highs - today the Nasdaq is the leading Index.

The market has been an enormous Shwanzstucker this year — surprisingly, undaunted from the last month of rapidly rising interest rates and political uncertainty.

As noted in yesterday's updated market outlook the upside reward vs. downside risk is terrible to me and it's only the price action that keeps me from expanding my short exposure.

And market breadth is bad, belying the advance in the Indices:

As seen in this chart, breadth has flatlined yet the Indices are rising as the market is again growing concentrated in large-cap tech (the RSP is DOWN on the day!):

Rest in peace, Terri Garr (Inga)!

Voof!

BY Doug Kass · Oct 29, 2024, 2:20 PM EDT

I knew I made a mistake in covering my PepsiCo PEP short.

At least I am still short Coca-Cola KO.

BY Doug Kass · Oct 29, 2024, 1:11 PM EDT

From Peter Boockvar:

A clip to Q3 GDP/Confidence rises, particularly in the stock market/Job openings continue to fall

We’re going to see a clip to Q3 GDP estimates after the much higher than expected goods trade deficit in September where imports grew by 3.8% m/o/m while exports dropped by 2%. On the import side, it’s tough to know how much was front loading ahead of the port strikes. The $108.2b goods trade deficit (so not including services) was the 2nd largest ever.

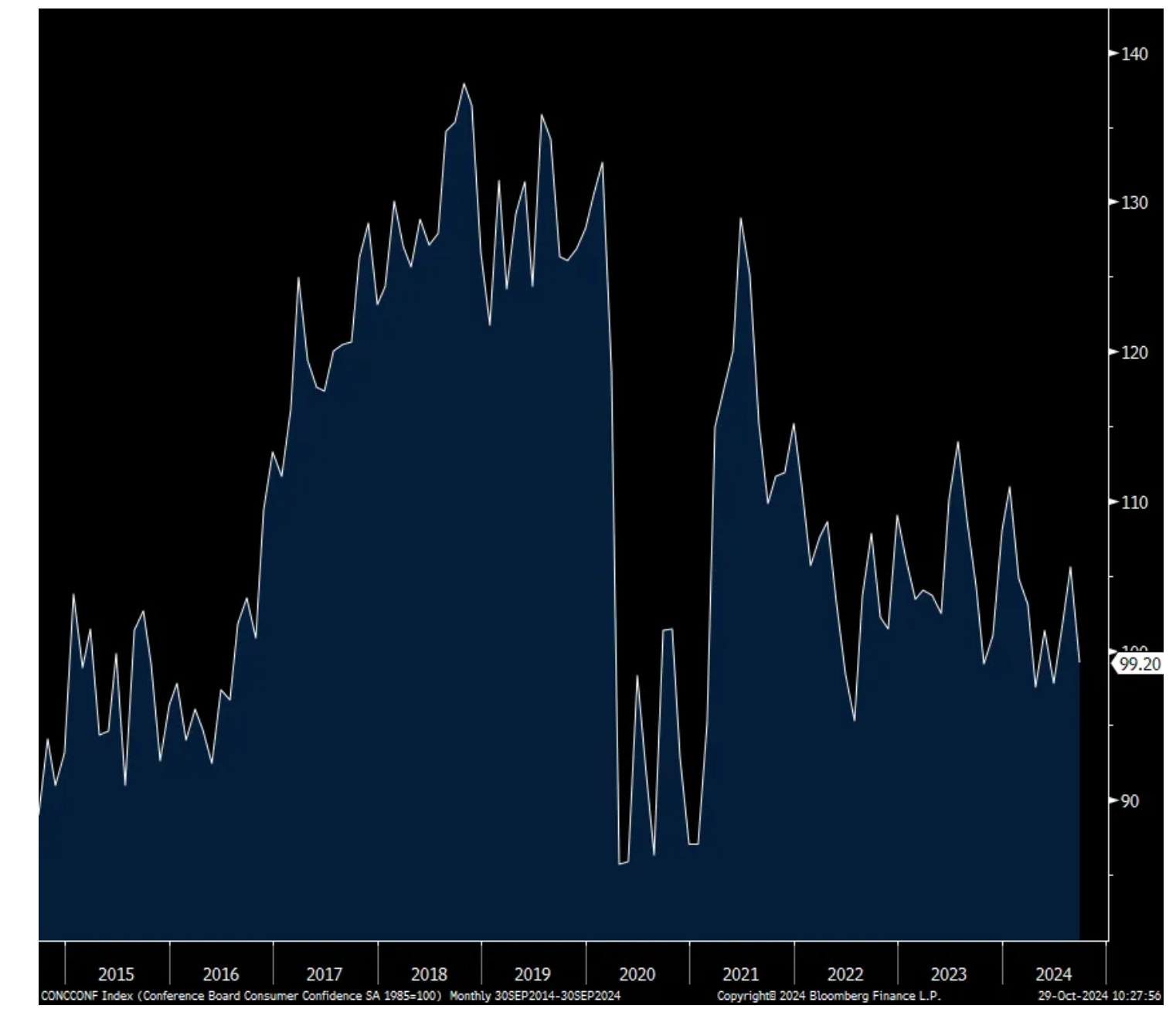

The October consumer confidence index from the Conference Board rose to 108.7 from 99.2 and that was much above the estimate of 99.5. Both main components were up m/o/m. One yr inflation expectations rose one tenth m/o/m to 5.3% which matches a 4 month high. The Conference Board said the uptick in inflation expectations could be led by food and services. They also said “Mentions of prices and inflation continued to top write-in responses as topics affecting consumers’ views of the economy, but more respondents mentioned slower inflation and lower grocery prices.”

The main reason for the confidence lift was the improvement in the answers to the labor market questions. Those that said jobs were Plentiful rose to a 4 month high while those that said they were Hard to Get fell after the rise last month. There was also a gain in those that expect ‘more jobs’ in the coming 6 months. Income expectations were unchanged m/o/m.

Spending intentions were mixed as they rose for autos but were unchanged for homes after rising in September with the drop in mortgage rates.

The Conference Board also said that “October’s increase in confidence was broad-based across all age groups and most income groups. In terms of age, confidence rose sharpest for consumers aged 35-54. On a six month moving average basis, householders aged under 35 and those earning over $100k remained the most confident.”

Also of importance, “The proportion of consumers anticipating a recession over the next 12 months dropped to its lowest level since the question was first asked in July 2022, as did the percentage of consumers believing the economy was already in recession.” Let’s hope this is not a contrarian indicator.

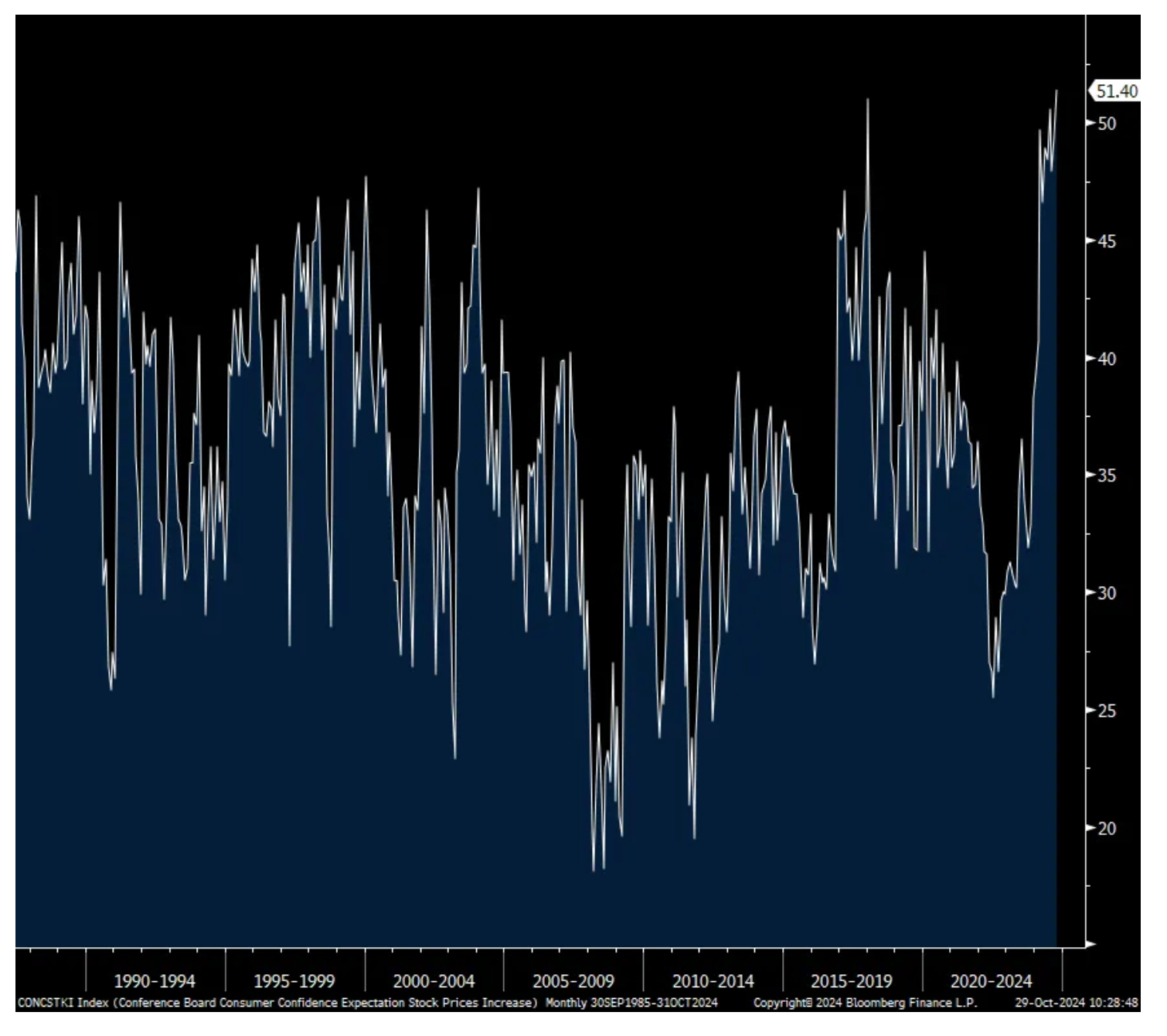

Let’s hope this one is not too, “51.4% of consumers expected stock prices to increase over the year ahead, the highest reading since the question was first asked in 1987. Only 23.6% expected stock prices to decline.”

Bottom line, consumer confidence continues to ‘trade’ in a range since 2022 of about 100-110 and compares to 132.6 in February 2020.

Consumer Confidence

% of those who expect higher stock prices

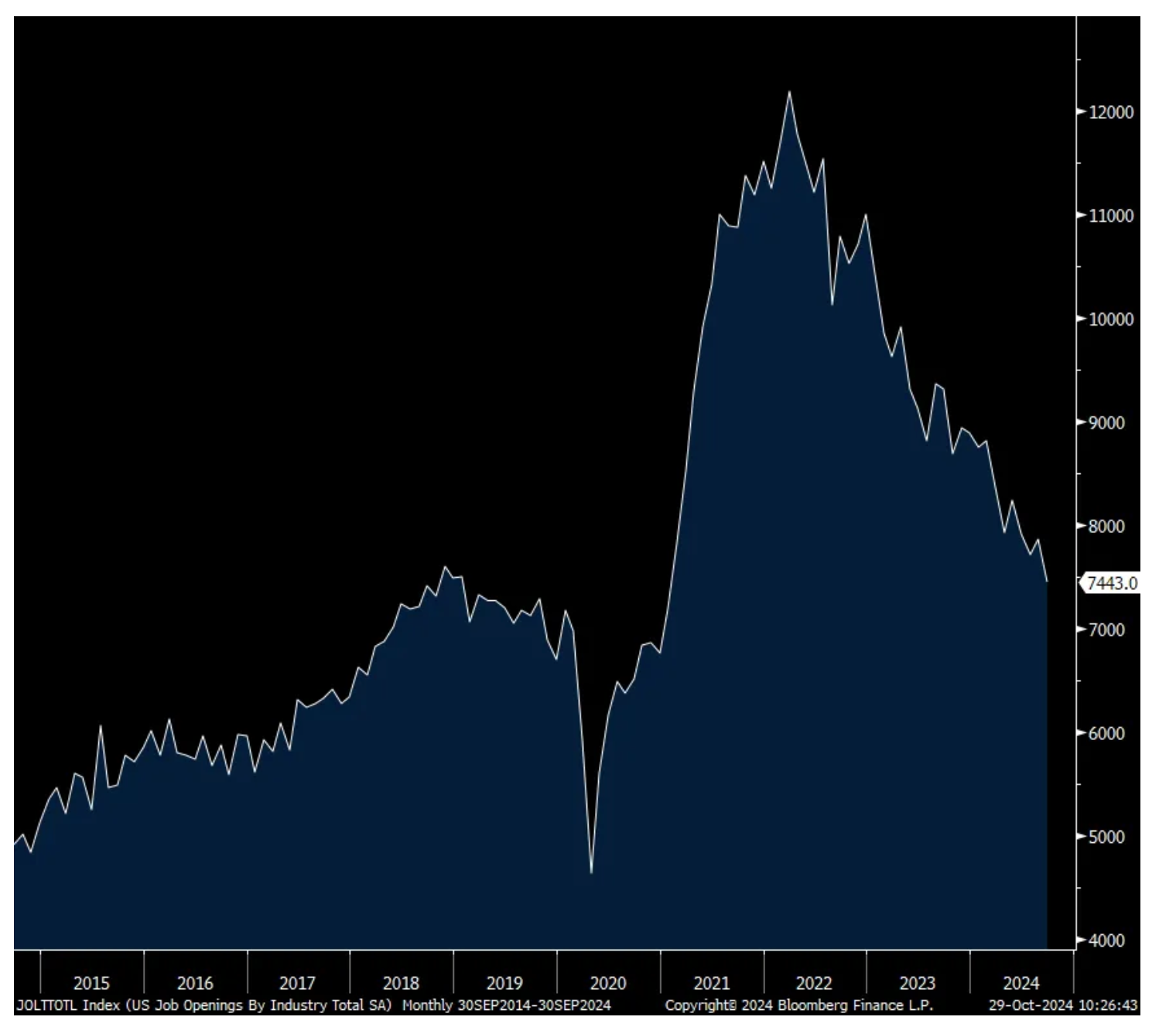

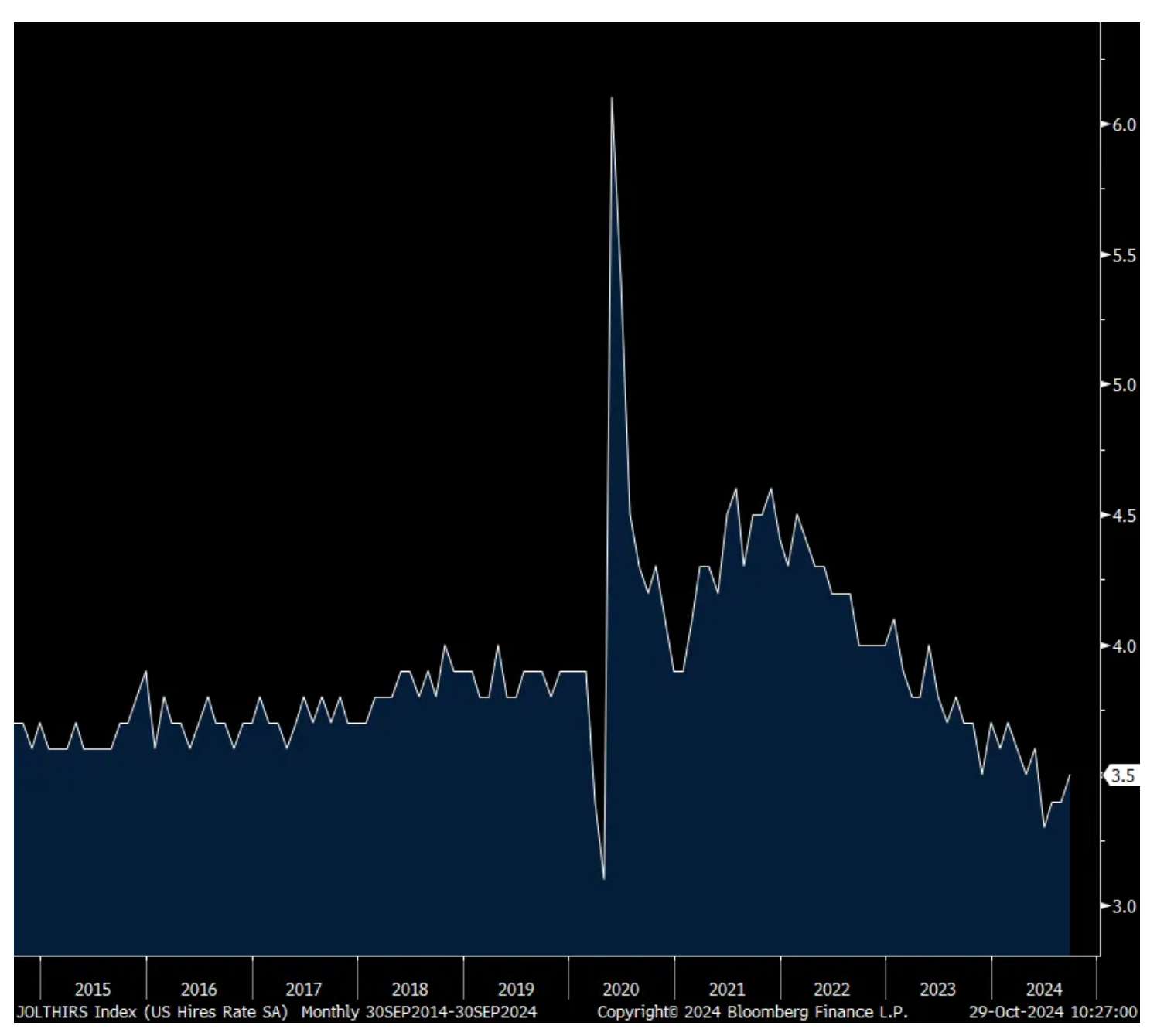

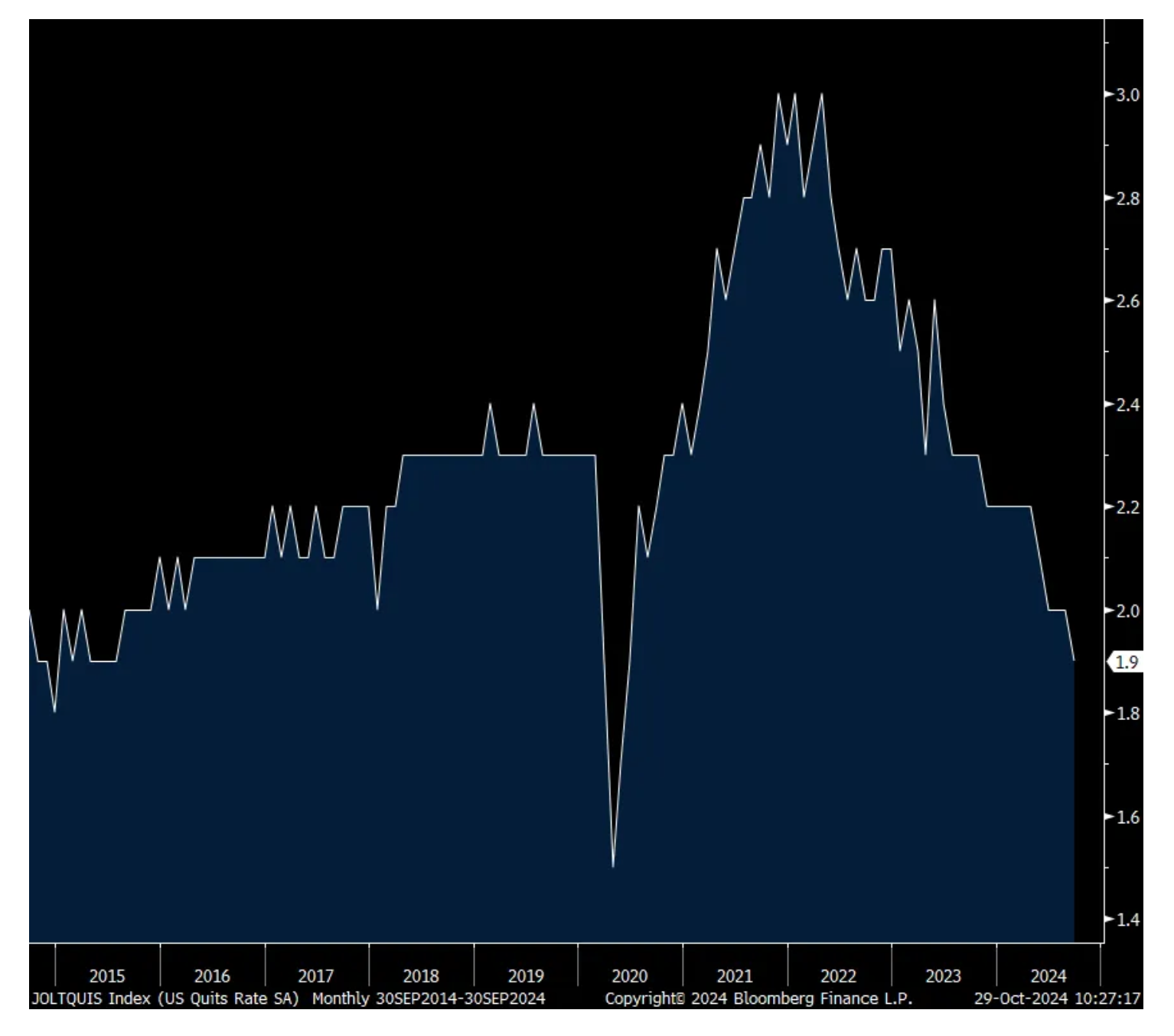

In contrast to the raised October job expectations in the confidence data above, job openings in September fell to 7.44mm, down about 400k m/o/m and well below the estimate of 8mm. That is the least since January 2021. The hiring rate did tick up to 3.5% from 3.4% but the quit rate fell to 1.9% which is the lowest since 2015 not including Covid.

Of particular note was the drop of 178k in job openings for health care/social assistance. There was also a drop of 132k in job openings at the government level, led by state and local ex education. I bring up these two sectors because they’ve been the main additions to overall payrolls. The other, leisure/hospitality, saw a reduction of 111k m/o/m.

Bottom line, this is further evidence of the slackening demand for labor. And while Treasury yields are still higher, the 10 yr yield was 4.33% right before the data release and is back at 4.30% as of this writing.

Job Openings

Hiring Rate

Quit Rate

BY Doug Kass · Oct 29, 2024, 12:40 PM EDT

- NYSE volume 8% above its one-month average.

- NASDAQ volume 25% above its one-month average.

- VIX: down 2.32% to 19.34.

BY Doug Kass · Oct 29, 2024, 12:15 PM EDT

I spent several hours on Pfizer PFE over the weekend and for the life of me I can't understand what the activists see in this name.

I will take a pass.

BY Doug Kass · Oct 29, 2024, 12:05 PM EDT

Boeing BA, after pricing its secondary (in the hole) at $143, appears to be making some believers today!

BY Doug Kass · Oct 29, 2024, 11:40 AM EDT

* With a hat tip to Yogi Berra...

BY Doug Kass · Oct 29, 2024, 11:30 AM EDT

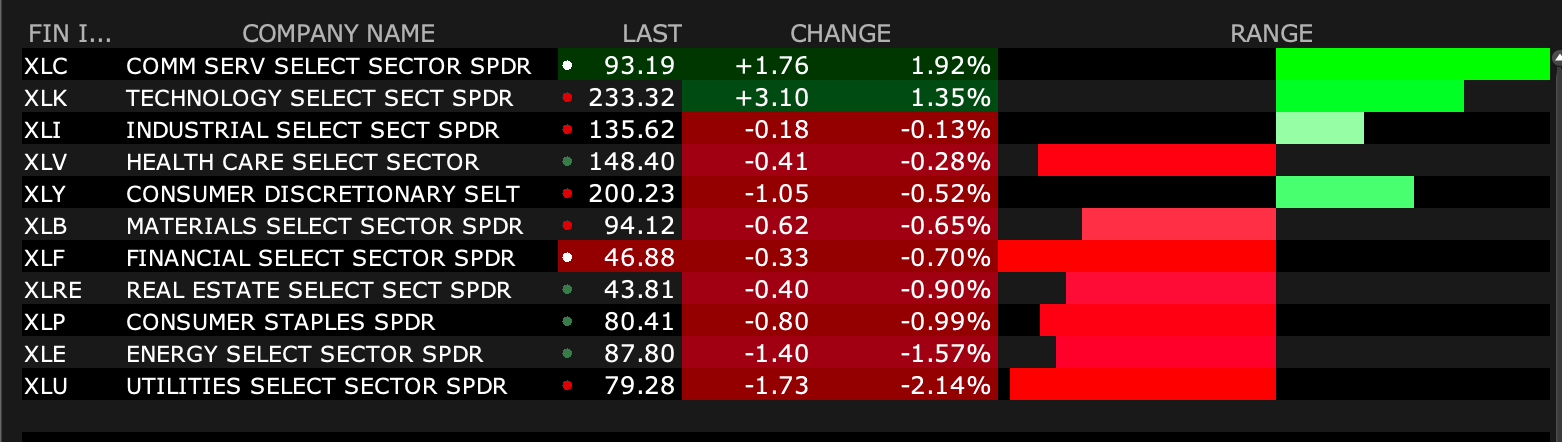

Financials, the object of my recent disaffection, are beginning to roll over (and have failed to follow thru to the upside from yesterday's action).

Added to XLF, BAC, C and JPM shorts.

BY Doug Kass · Oct 29, 2024, 11:15 AM EDT

Since this question was first asked in 1987, the Conference Board's consumer confidence index today saw the highest % of those who think we'll see higher stock prices from here.

BY Doug Kass · Oct 29, 2024, 11:05 AM EDT

With S&P cash +8 handles I am pressing my short Index calls and reducing my long Index common.

I added to my short DJT call holdings (still sized very small to reflect the vol).

BY Doug Kass · Oct 29, 2024, 10:37 AM EDT

From Peter Boockvar:

So we are now at that key 4.30% 10 yr yield level I've mentioned here a few times as it is the 50% retracement of the highs and lows in yield going back to last summer. An interesting set up ahead of the jobs data this week. I want to include here again, in case you missed it, what TriNet said on Friday about what they are seeing in the labor market:

"Slower economic growth, higher interest rates, and generally cautious outlook resulted in a third quarter of no net hiring amongst our customer base. While the headline jobs reports have been generally positive from the BLS over the last year, our experience has differed materially. Growth in several sectors, including government, construction, and healthcare are fueling aggregate headlines, while our core verticals of technology, life sciences, financial services, and other professional services have been muted."

With Treasuries now getting oversold, I would not be surprised if we have a bounce but I'm still bearish on duration and think longer end yields will continue higher after any short term drop.

While still negative, the October Dallas manufacturing index seen yesterday was the least bad since April 2022 at -3.0. Here were some of the comments from it, though that still reflect that contraction in activity:

Chemical Mfrg:

"Interest rate impacts continue to put pressure on the overall construction markets and auto industry, which are major customers of the basic materials space."

Computer & Electronic Product Mfrg:

"We need more interest rate cuts on leasing capital equipment to see a difference in our industry. Rates are still too high."

Fabricated Metal Product Mfrg:

"We are expecting a continued period of lower demand and production over the next six to 12 months. We have flexed down our workforce and supplier purchases accordingly."

Food Mfr'g:

"We are experiencing inflation related increases in the cost of doing business across the spectrum of operations with no real way to recoup or have margin protection."

"Sales volume is below projections for 4th quarter 2024. Geopolitical instability is increasing throughout the world, and the US presidential election may create more instability."

"We are seeing increased demand for our products, which is driving the increase in our production."

Machinery Mfr'g:

"Business remains slow; however, we are hopeful that after the election, business will pick up (if the "right" candidate wins)."

"Geopolitical conflict and aggression wreaks havoc with our planning. Our own election outcome cannot be known soon enough. We have prospective deals of significance on hold pending who takes office. Overall, it's been a really rough year through no apparent fault of our own, but our pivots have yet to yield favorable results despite being as nimble as possible. Hopefully, 2025 will be a year of jubilation!"

Misc Mfr'g:

"A prominent slowing of business began in October 2023, and it has continued to trend lower month over month for the last 12 months."

Paper Mfr'g:

"Orders and the outlook are trending down at the time."

Printing & Related Support Activities:

"We are now in month two of much slower business activity, something we have avoided for the previous 10 months. Hopefully, things will pick up soon, or else we will need to reduce head count in the plant. Naturally, this comes just as a huge capital expenditure machine has arrived and is in the process of being installed and training beginning."

Transportation Equipment Mfr'g:

"Our outlook is predicated on the election outcome."

Let's get to some earnings comments.

From On Semi, who is more of an industrial semi supplier and if you're not selling into the AI ecosystem, business is still tough:

"we have delivered on our commitments amid continued softness in the market. Over the last several quarters, we've talked about an L-shaped recovery. And as expected, the demand environment remains muted with ongoing inventory digestion and slow end demand. Our outlook for all markets remains unchanged as uncertainty persists among our customers. Automotive continues to be soft with slowing EV sell through. Industrial, which slowed first, has not broadly recovered expect for pockets and utility scale solar and aerospace defense."

From Ford:

On the EV business, "No doubt there's a global price war and it's fueled by overcapacity, a flood of new EV nameplates, and massive compliance pressure. In our home market in the US, no OEM is immune. Since Q1 of last year, EV volumes have grown 35% while revenues in total are flat at $14 billion. That means the progress on volume has been fully offset by prices. We're expecting roughly 150 new EV nameplates to hit North America by the end of 2026. And some of our competitors are already resorting to very aggressive lease tactics even on brand new products which creates huge residual risk and overhang and brand damage."

Hybrid remains the vehicle of choice in the battery space with sales up 30% in the quarter.

Stanley Black & Decker in their earnings press release referred to " a weak consumer and automotive production backdrop" as they reported sales down 5% y/o/y.

We know cruising has been an economic bright spot and Royal Caribbean said this in their release:

"Robust demand for its vacation experiences drives strong results and improved outlook."

They saw "stronger pricing on close-in demand, continued strength in onboard revenue and lower costs due to timing" and "We see elevated demand patterns continuing as we build the business for 2025."

"The demand and pricing environment accelerated since the last earnings call, exceeding 2023 levels. Closer-in demand for 2024 sailings exceeded expectations, contributing to higher load factors at higher prices and higher onboard revenue for the third quarter. Consumer spending onboard, as well as pre-cruise purchases, continue to significantly exceed 2023 levels driven by greater participation at higher prices."

From DR Horton, the homebuilder, under pre market pressure because...:

"Our sales pace was in line with normal seasonality from the 3rd to 4th quarter but was below our expectations. While mortgage rates have decreased from their highs earlier this year, many potential homebuyers expect rates to be lower in 2025. We believe that rate volatility and uncertainty are causing some buyers to stay on the sidelines in the near term. To help spur demand and address affordability, we are continuing to use incentives such as mortgage rate buydowns, and we have continued to start and sell more of our homes with smaller floor plans."

From McDonald's:

Their .3% rise in US comps "reflect average check growth, partly offset by slightly negative comparable guest counts."

The 2.1% drop in comps in their international operated markets "was impacted by negative comparable sales across a number of markets, driven by France and the UK."

Their international developmental licensed markets saw a drop of 3.5% for same store sales because of "The continued impact of the war in the Middle East and negative comparable sales in China" which "more than offset positive comparable sales in Latin America."

To the overseas economic data of note. Japan reported better than expected jobs data for September and yields moved slightly higher after yesterday's increase. The yen is little changed ahead of the BoJ gathering this week where no change in policy is widely expected but we wonder if in December or January they raise rates again which I think they will. The Nikkei was higher by .8%.

The thing of note in Europe was the slight improvement in the German consumer confidence index from GFK to -18.3 from -21. The estimate was -20.5 and while still negative, it's the best print since April 2022. While a slight m/o/m gain, GFK said "The uncertainty caused by crises, wars and rising prices is still very much present and is preventing factors that encourage consumption, such as real income growth, from taking full effect."

While good to see the gain, nothing market moving here and bond yields in Europe are higher too.

German Consumer Confidence

BY Doug Kass · Oct 29, 2024, 10:35 AM EDT

* Tesla's aggressive accounting (and "earnings beat") bears addressing.

I was weaned, cut my teeth and earned by bones reading Abraham J. Briloff's book, "Unaccountable Accounting" (h/t Alan Abelson/Barrons):

Tesla TSLA needed something to restore its faithful shareholders, after a long series of earnings disappointments, pricing pressures and slowing EV sales, a collapse of the resale values of Tesla cars, a disappointing Robocar event and a government investigation of the safety of its Full Self Driving system.

It delivered a third-quarter 2024 report that showed earnings of $0.12/share better than Wall Street's estimates. While 12 cents may not seem to be so significant to a stock over $200 per share, it triggered a massive rally in which the one-day increase in the company’s market value (late last week) exceeded the combined total market value of both Ford F and General Motors GM.

A review if Tesla’s financials raises many questions. Did aggressive accounting play a role in the reported numbers? When cash is expended by a company, it can be treated as an expense and will reduce reported profits. If instead, it is deemed to have future value, it can be capitalized and added to an asset. This would enhance reported profits as it would not be treated as an expense. In that context, the following analysis is offered:

* The ostensibly higher earnings than expected were $0.12 per share

* There are 3,497 million shares outstanding

* $0.12/share x 3,497 equals $420 million in post tax earnings

* The effective tax rate was 21.6%

So, pretax earnings would have ostensibly risen by $420 million divided by .784 (adjusting for taxes) and therefore been $535 million greater than expected. million than expected.

* Property Plant and Equipment in the second quarter was $32.902 billion. It increased by $1.488 billion in 2Q from 1Q 2024

* In 3Q it increased $3.214 billion from 2Q, which is $1.726 billion greater than the increase in the prior three months

* This differential alone, if extra expense were capitalized, could have enhanced reported earnings by $0.49/share!

* Does this make sense? (See prior analysis.) What was capitalized in 3Q that was not in 2Q or 1Q?

Prepaid expenses and other current assets rose from $4.325 billion in 2Q to $4.888 billion in 3Q -- a gain of $563 million, which if capitalized rather than expensed, would equal a 16 cents per share enhancement.

Other non-current assets rose from $4,458 million in 2Q to $4,989 million in 3Q an increase of $531 million, which, on the same basis, would equal 15 cents per share.

So, it appears that there are a lot of unusual gains in asset categories relative to what one might have expected, given the relatively flat shipments (quarter to quarter), By capitalizing them rather than expensing them, they could have easily enhanced earnings by much more than the reported earnings beat.

A review of stand-alone leased vehicle sales and expenses raises questions.

* In 2Q leased vehicle sales were $458 million and leased costs were $245 million, reflecting a cost of goods sold of 53.5%

* In 3Q leased vehicle sales were $446 million and costs were $247 million reflecting a cost of goods sold of 55.4%. So, at least in this area, costs per car actually rose, rather than fell, as claimed by Tesla

* The more expensive Cybertruck was more significant in 3Q, which would have tended to bias costs per vehicle higher, which further makes the claims of lower costs per vehicle lower, which is puzzling.

Further, the claimed free cash flow of $2.7 billion seems to be more reflective of Tesla’s slow payments of its liabilities than of operating efficiency. The increase of accounts payable alone was $1.6 billion and increase in the accrued liabilities was $1.0 billion.

None of this was questioned on the conference call following the earnings and, as I previously mentioned, only two analysts were able to ask questions, one of which was Adam Jonas, who represents Tesla’s lead investment banker.

The company needs to plausibly address these issues, especially in light of its comments on the call that these results would be difficult to sustaining the future. Only then can a real understanding of this quarter emerge.It is likely that Tesla found 12 cents somewhere around here:

1. Higher PPE 49 cents

2. Higher capitalized prepaid expenses 16 cents

3. Higher Noncurrent assets 15 cents

Late yesterday afternoon it was announced that three Tesla employees filed to sell up to $260 million of stock (or more than one million shares).

The sellers include Elon Musk's brother Kimbal (152,088 shares), Tesla Chairman Robyn Denholm (674,345 shares) and Tesla Director Kathleen Wilson Thompson (300,000 shares).

BY Doug Kass · Oct 29, 2024, 9:45 AM EDT

I have materially covered my homebuilder shorts at great prices this morning.

Now very small sized.

BY Doug Kass · Oct 29, 2024, 9:43 AM EDT

BY Doug Kass · Oct 29, 2024, 9:29 AM EDT

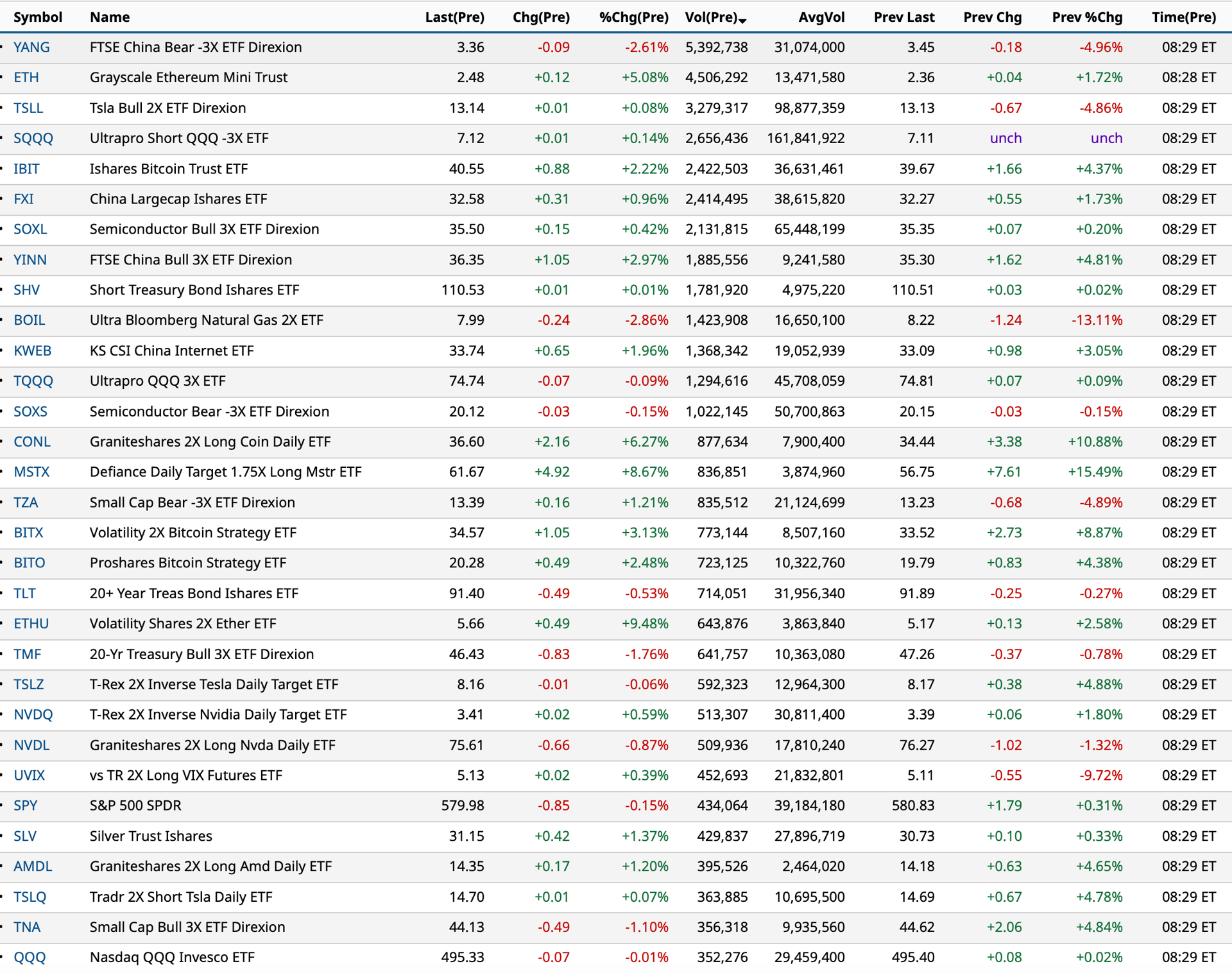

Charts from 8:29 a.m. ET:

BY Doug Kass · Oct 29, 2024, 9:23 AM EDT

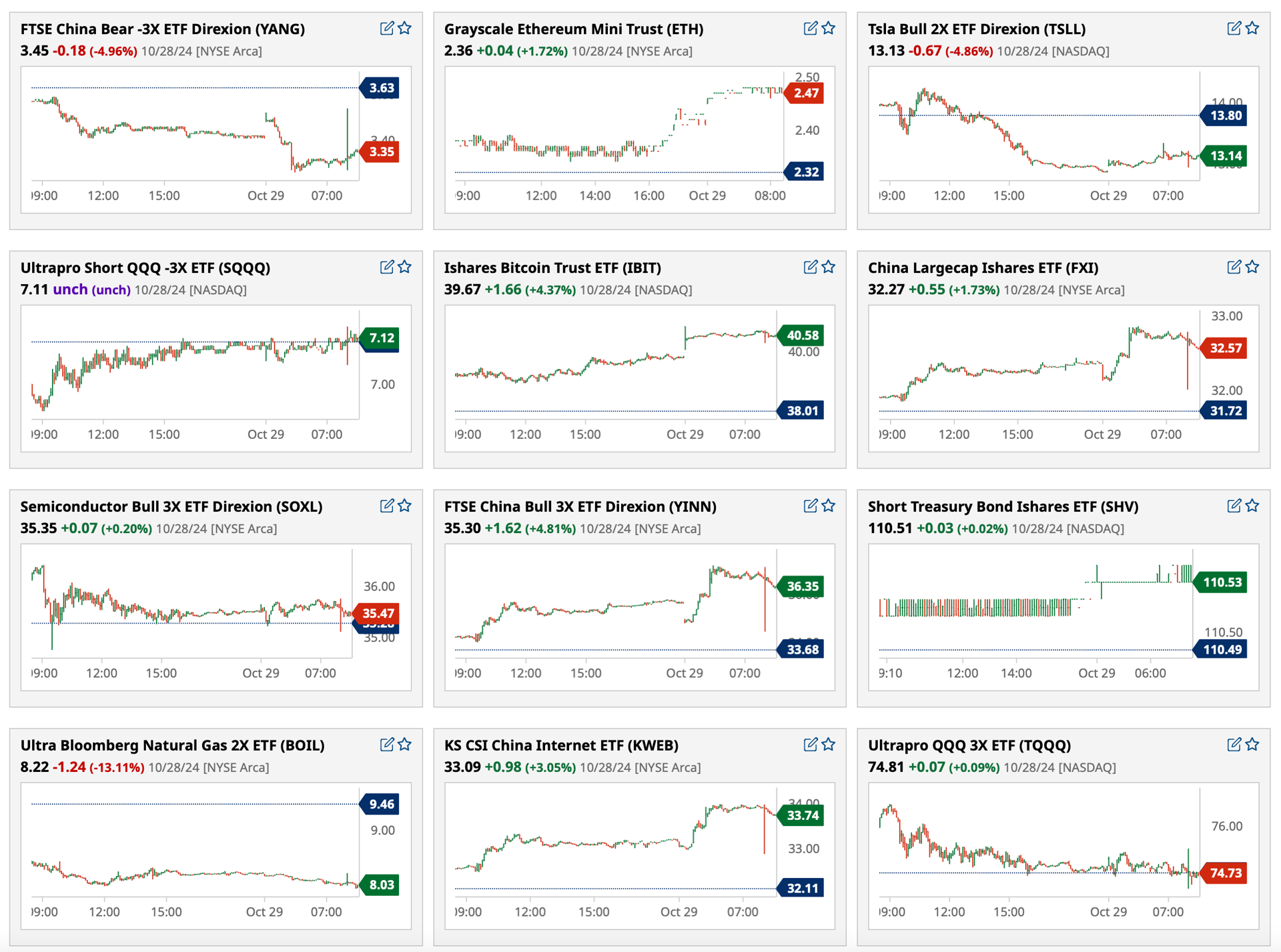

Chart from 8:48 a.m.:

BY Doug Kass · Oct 29, 2024, 9:13 AM EDT

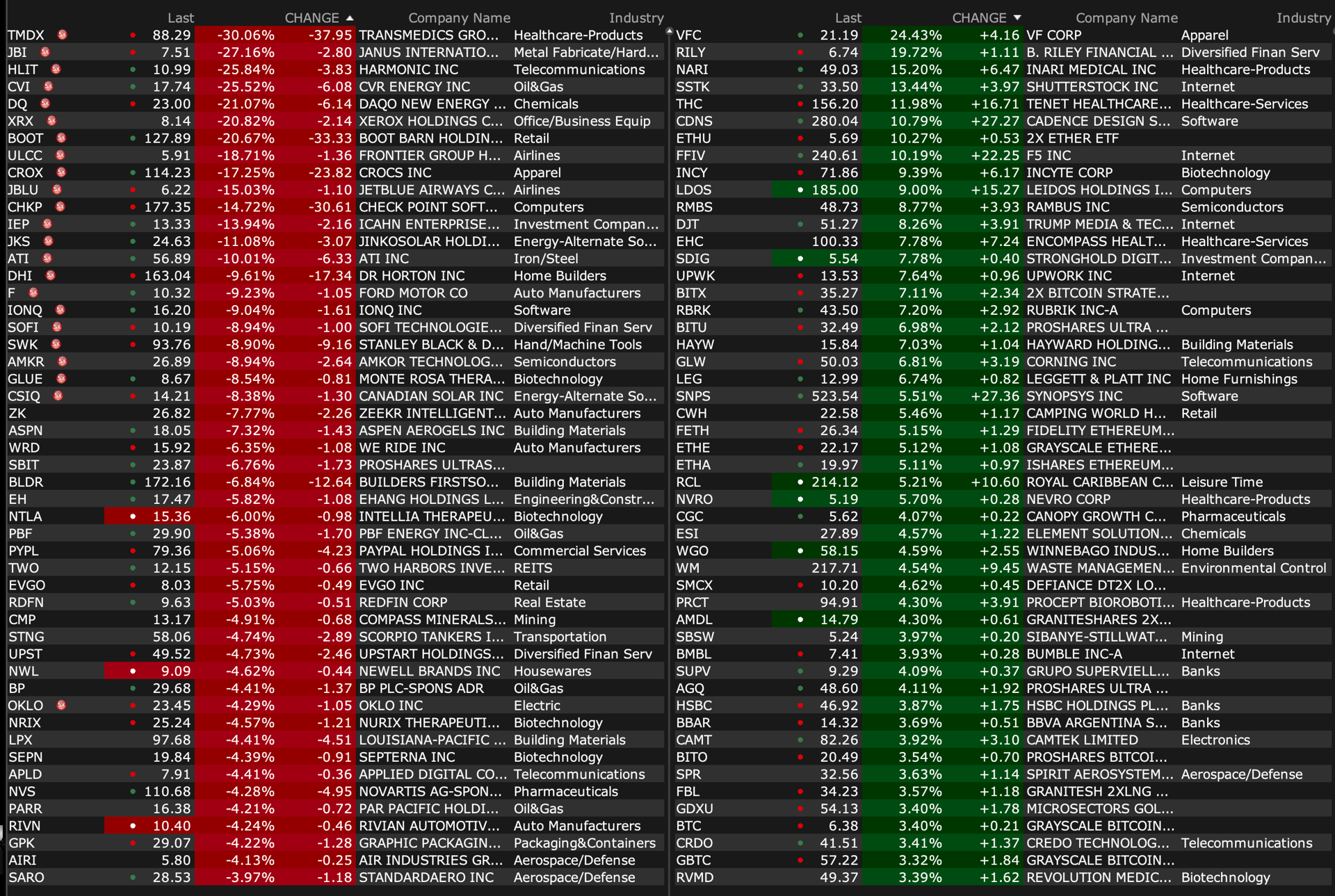

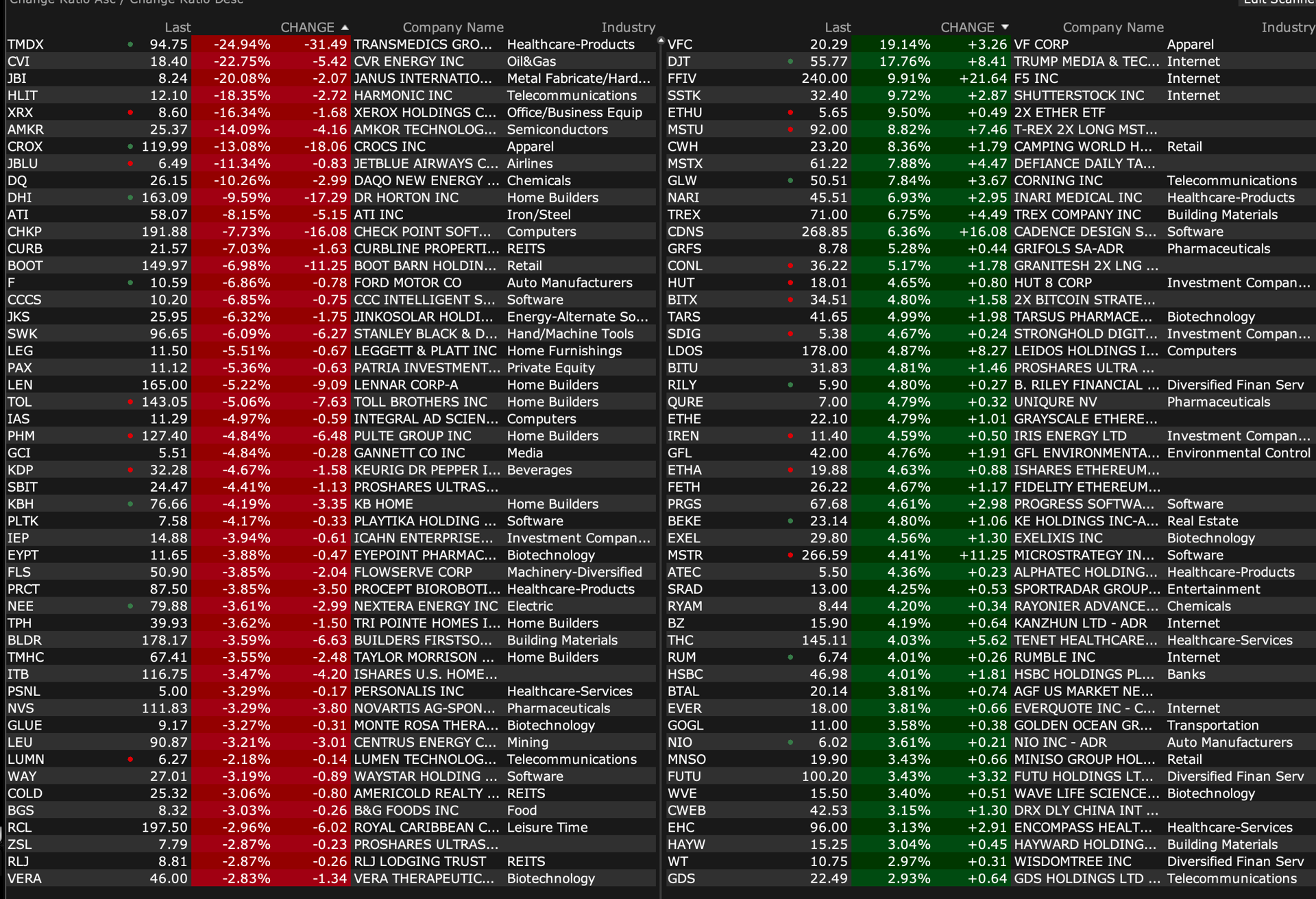

-VFC +19% (earnings, guidance)

-CVLT +10% (earnings, guidance)

-FFIV +10% (earnings, guidance)

-GLW +8.2% (earnings, guidance)

-ZBRA +7.3% (earnings, guidance)

-CWH +7.2% (earnings, guidance)

-TREX +7.2% (earnings, guidance)

-NARI +6.9% (earnings, guidance)

-CDNS +5.8% (earnings, guidance)

-THC +4.7% (earnings, guidance)

-SOFI +4.3% (earnings, guidance)

-IPGP +3.8% (earnings, guidance)

-BIOR -23% (files to sell 745K shares at $4.025/shr in $3M registered direct offering)

-CVI -23% (earnings)

-TMDX -23% (earnings, guidance)

-HLIT -18% (earnings, guidance)

-CROX -15% (earnings, guidance)

-AMKR -13% (earnings, guidance)

-BOOT -7.0% (earnings, guidance)

-JBLU -6.6% (earnings, guidance)

-F -6.4% (earnings, guidance)

-EYPT -5.1% (announces proposed public offering of common stock)

-FLS -3.9% (earnings, guidance)

-SWK -3.8% (earnings, guidance)

-NEE -3.7% (FPL outlines plan to pay for significant restoration efforts after four hurricanes slam Florida in 14 months)

-ULCC -3.7% (earnings, guidance)

-SYY -2.8% (earnings, guidance)

-PYPL -2.7% (earnings, guidance)

-MCD -2.3% (earnings, guidance)

-MNPR -2.3% (prices $19.2M offering at $16.25/shr)

-LEU -2.0% (earnings)

BY Doug Kass · Oct 29, 2024, 9:05 AM EDT

BY Doug Kass · Oct 29, 2024, 8:55 AM EDT

BY Doug Kass · Oct 29, 2024, 8:45 AM EDT

* 'My Basic Investing Tenets.'

I originally wrote this column in March 2013, but with markets near all-time highs, I think that it has some merit in repeating in it's entirety.

"You've got to be very careful if you don't know where you are going because you might not get there."

-- Yogi Berra

Arguably, the investment and asset-allocation processes can hold more weight and is more complex than nearly any other business decision. A host of variables, known and unknown, contribute to the investment alchemy. As well, subtle and unconscious influences and personal biases affect the process as we all seek Mr. Market's metaphorical green jacket (like the one to be given to the winner of the Masters golf tournament in mid-April).

What follows are some basic tenets which form my investment consciousness, which are admittedly simple to write about but more difficult to execute.

By Doug Kass Sep 3, 2014 10:27 AM EDT

BY Doug Kass · Oct 29, 2024, 8:00 AM EDT

Q4 FY 2024 Earnings Press Release

The shares are -$13 in premarket trading.

The weak guidance will likely weigh on all homebuilder stocks.

We remain short D.R. Horton DHI and four other homebuilder shares.

More to come...

Post Script: I spend a lot of time being critical of Fin TV, which is populated by too many without an investment process, who don't model or talk to managements and base their decisions on gut (and expressed those views in memorized sound bites).

DHI is another case in point — recommended yesterday and over the last few months. (See here and here)

Here is our investment case to be short homebuilders:

I have been extremely aggressive in shorting homebuilders.

Yesterday, homebuilder equities declined by about 4% with losses of between $4 to $8 in each company -- as interest rates globally were schmeissed.

Previously written:

On Wednesday I cautioned about the homebuilder space.

Since then, and over the last two trading days, I have more aggressively shorted merchant builder equities.

I would note that (TLT) (I remain short) dropped by $1.55/share yesterday -- reflecting a growing view that the U.S. economy is growing above potential (see Wolf Street):

1. The yield on the 1-year Treasury bill rose by five basis points.

2. The yield on the 3-year Treasury note also advanced by five basis points.

3. The yield on the 10-year Treasury note increased by eight basis points. (This is the rate that mortgage rates are generally set against).

4. The yield on the long bond rose by nine basis points.

Here are my Diary comments from Oct. 16:

* Homebuilder stocks are now vulnerable to a decline...

* But for now I treat these stocks as "trading sardines and not eating sardines" — actively trading around a small core short position.

The housing recovery (in price and activity) has slowed down for all of the reasons I have recently discussed in my Diary.

As expected, the abnormally low inventory of existing homes for sale is now rising and affordability (consider the quantum price increases in home prices between 2017-2022) is dulling demand despite some pressure off of mortgage rates (which have now stabilized). Moreover, the cumulative or stacked inflation in the cost of living since 2000 has pressured consumers' general ability to afford near record home prices.

Here Wolf Street howls about the weakness and current state of the residential real estate markets.

With the average merchant builder trading at a record multiple to book value (above 2.2x), the cost of new land acquisition expected to cut into future profitability and an emerging and growing imbalance between existing home demand and supply (serving as a competitive challenge to builders of new homes), I expect (in the fullness of time) for homebuilder stocks to retreat meaningfully from current levels.

But for now it appears that investors are considering a new paradigm of non-cyclicality and uninterrupted growth for the sector. This optimism is likely misplaced. (See Bob Farrell's Rule #3 on Investing below):

Translation: There will be a hot group of stocks every few years, but speculation fads do not last forever. In fact, over the last 100 years, we have seen speculative bubbles involving various stock groups. Autos, radio, and electricity powered the roaring 20s. The nifty-fifty powered the bull market in the early 70s. Biotechs bubble up every 10 years or so and there was the dot-com bubble in the late 90s. “This time it is different” is perhaps the most dangerous phrase in investing.

As Jesse Livermore puts it:

A lesson I learned early is that there is nothing new in Wall Street. There can't be because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again.

Until there is a break in share-price momentum I intend to treat the volatile and high beta homebuilder stocks as trading vehicles (and weigh them appropriately in size). Specifically, my strategy continues to be concentrated on trading around a very small core short position.

Yesterday I continued to do so — profitably.

By Doug Kass Oct 16, 2024 9:55 AM EDT

Position: Short TOL (S), KBH (S), LEN (S) DHI (S), GRBK (S)

By Doug Kass Oct 22, 2024 9:33 AM EDT

BY Doug Kass · Oct 29, 2024, 7:40 AM EDT

A combination of Florida Governor DeSantis' increasingly forceful objections to Florida's Amendment 3 (allowing adult recreational use of cannabis) and a flood of new contributions (aimed against passage) when combined with Florida Congressman Byron Donalds' call to reject the Amendment has likely reduced the chance of passage somewhat and lessened the positive impact of former President Trump's endorsement of Amendment 3.

As I noted in my Diary, most polls had a "yes" vote with about 65% of the vote (60% is necessary for passage of recreational cannabis in the State).

My guess is that it is now a few percent lower — making what was a "sure bet" a week or two ago less likely (but still favoring odds of passage).

Then there are the issues of timeline (a likely six months until implementation) and, if passed, how the legislation will be worded.

The next meaningful catalyst for cannabis will be the December DEA meetings and testimony. If rescheduling is approved, there is probably another six months before its implementation as well.

Finally, I have been skeptical with custody and institutional ownership issues still unresolved, whether the retail community can sustain much higher prices for cannabis equities even if Amendment 3 passes.

These are the likely messages and potential headwinds being told by the lackluster trading of MSOS over the last week or so.

BY Doug Kass · Oct 29, 2024, 7:30 AM EDT

The thing is that my pal Larry always tells the emes (the truth):

BY Doug Kass · Oct 29, 2024, 7:20 AM EDT

Bonus — Here are some great links:

November Is a Top Month During Election Years ("Jazzy" Jeff Hirsch)

BY Doug Kass · Oct 29, 2024, 7:05 AM EDT

From my pal Bloomberg's Tom Keene (a charter member of "Red Sox Nation"):

BY Doug Kass · Oct 29, 2024, 6:55 AM EDT

BY Doug Kass · Oct 29, 2024, 6:45 AM EDT

The rise in yields continues unabated:

* The yield on the 1-year Treasury bill is +2 basis points to 4.32%

* The yield on the 5-year Treasury note is +3 basis points to 4.14%.

* The yield on the 10-year Treasury note is +3 basis points to 4.31%.

* The yield on the long bond is +3 basis points to 4.56%.

BY Doug Kass · Oct 29, 2024, 6:35 AM EDT

At the market's close on Monday the S&P Short Range Oscillator stood at -1.25% compared to Friday's close of -1.44%.

BY Doug Kass · Oct 29, 2024, 6:25 AM EDT

BY Doug Kass · Oct 29, 2024, 6:15 AM EDT

* Booted out this short for a profit...Boot Barn BOOT shares fell by nearly -$20 last night on the management announcement.

We covered our short:

BY Doug Kass · Oct 29, 2024, 6:05 AM EDT

In very early trading (4:45 a.m.) I sold SPY (long) at $581.56 and QQQ (long at $496.43).

BY Doug Kass · Oct 29, 2024, 5:55 AM EDT

BY Doug Kass · Oct 29, 2024, 5:45 AM EDT