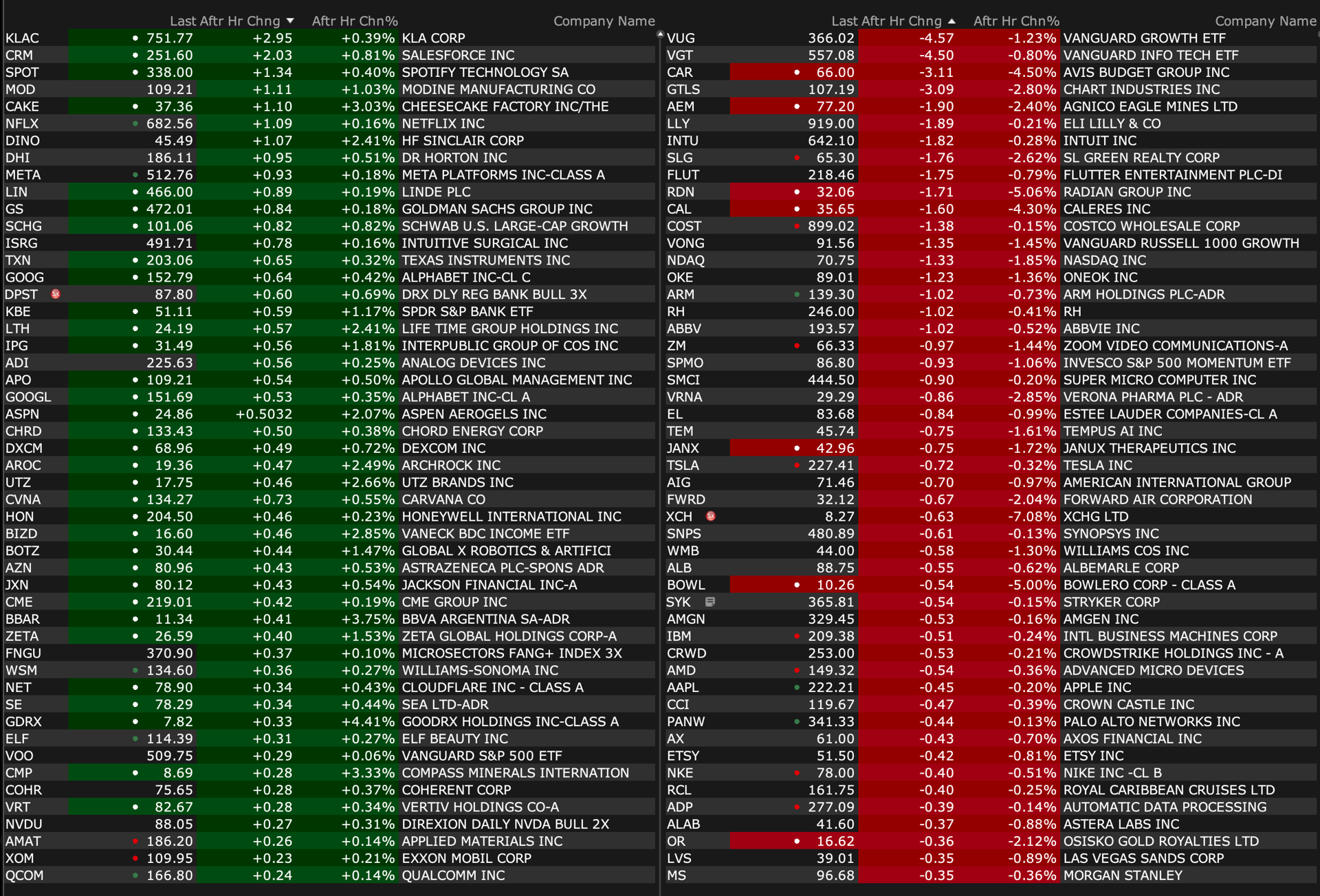

After-Hours Movers

As of 4:23 p.m.:

BY Doug Kass · Sep 11, 2024, 4:55 PM EDT

As of 4:23 p.m.:

BY Doug Kass · Sep 11, 2024, 4:55 PM EDT

BY Doug Kass · Sep 11, 2024, 4:18 PM EDT

The volatility today was mind boggling.

I can't see how it is constructive.

BY Doug Kass · Sep 11, 2024, 3:05 PM EDT

Wolf Street peels some layers of inflation.

BY Doug Kass · Sep 11, 2024, 2:32 PM EDT

I shorted size XLU at $77.04 just now.

BY Doug Kass · Sep 11, 2024, 2:23 PM EDT

From Peter Boockvar:

10 yr note auction was solid

The 10 yr note auction was solid. The yield of 3.648% was under the when issued pricing of 3.662%. The bid to cover of 2.64 was above the one year average of 2.50. Also, direct and indirect bidders took down about 90%, the most since September 2023.

Bottom line, solid as stated but yields are still up on the day as we take out the odds of a 50 bps rate cut next week. To try to account for some reasons for the strong bid: Are buyers comforted by the in line inflation print? Are recession worries growing? Do US debts and deficits not matter? Does the weaker US dollar dissuade foreign buying of US Treasuries. At least for today, the first three questions should be answered yes and the last one, a no.

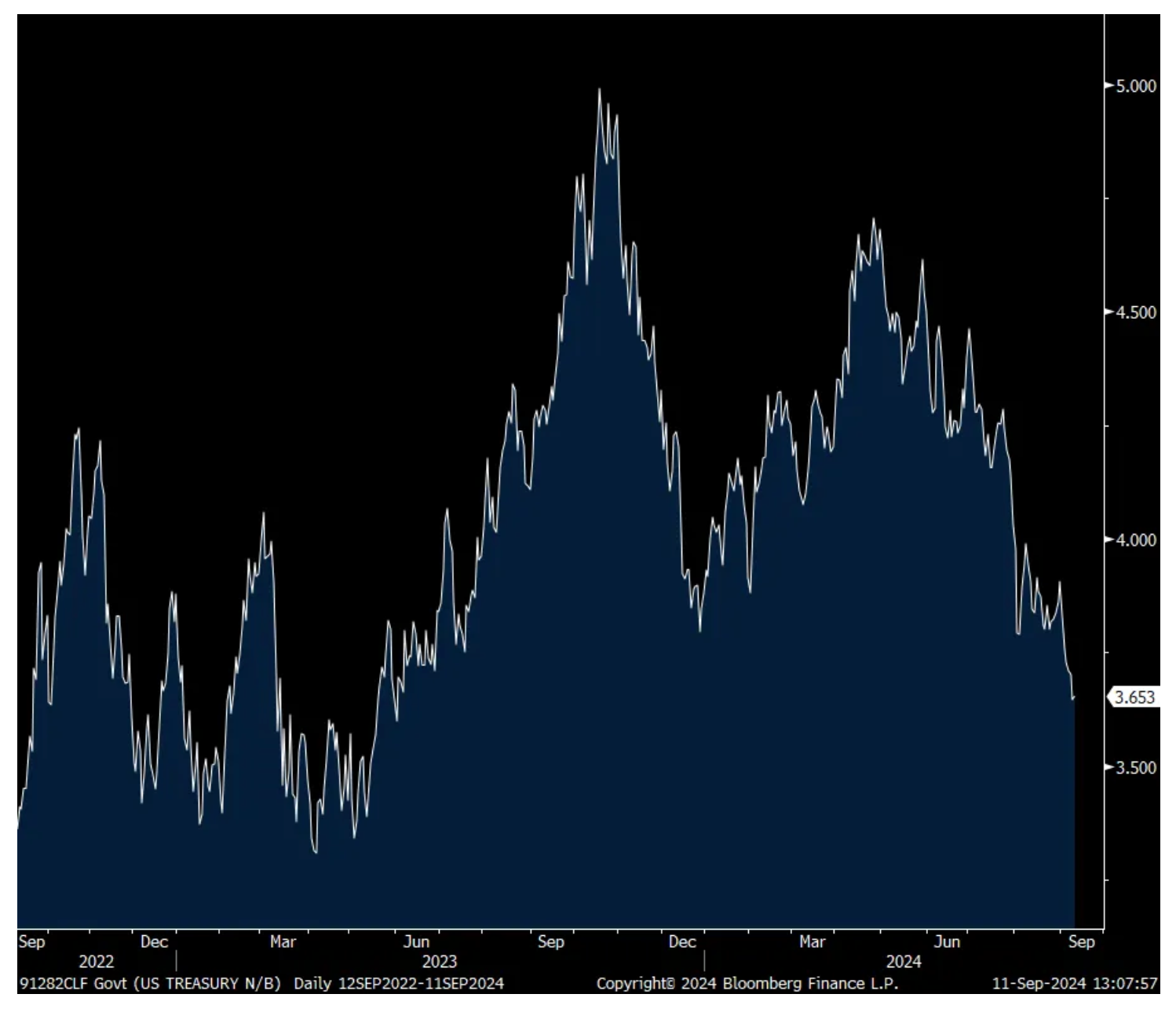

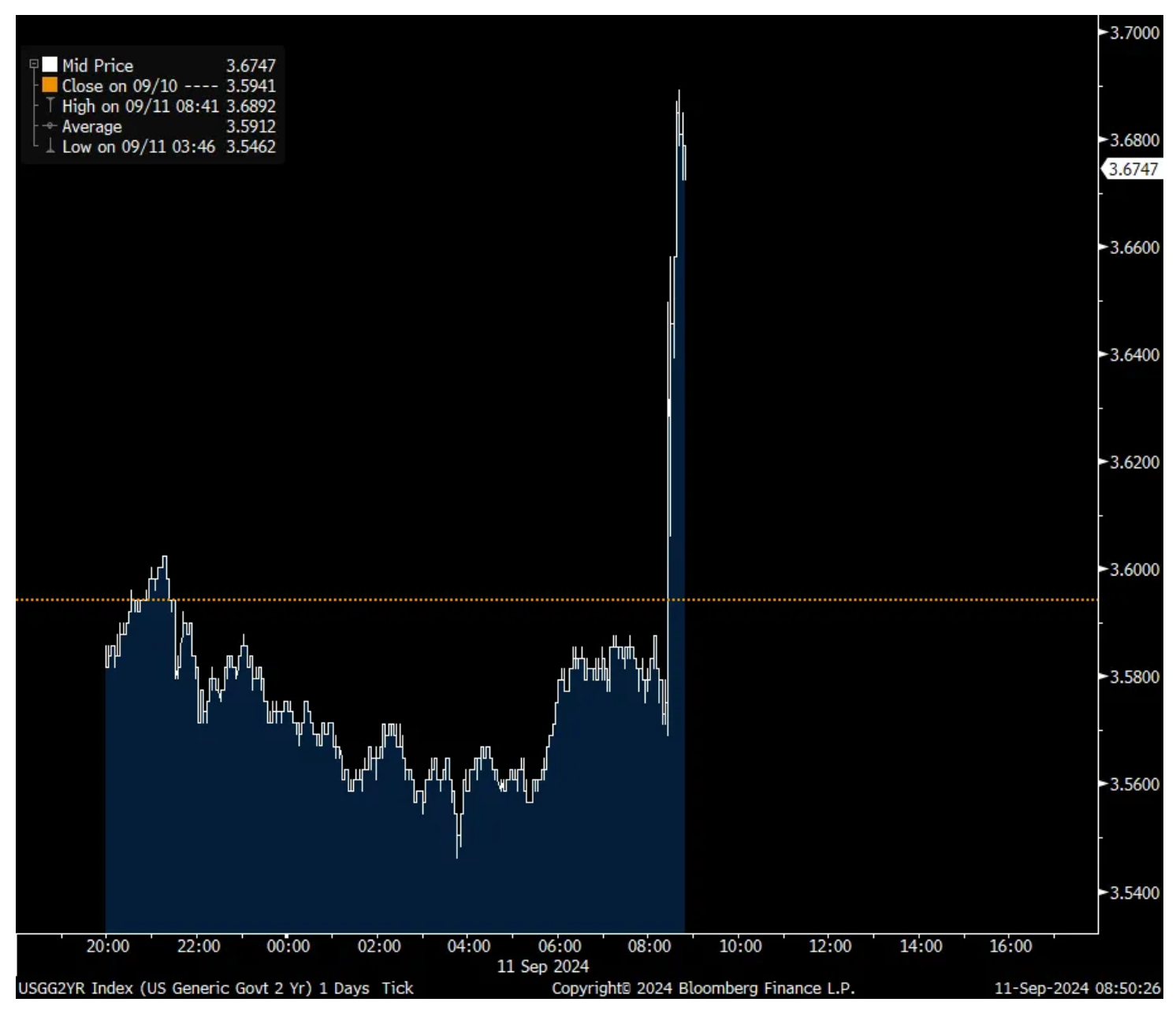

10 yr yield

BY Doug Kass · Sep 11, 2024, 2:10 PM EDT

* From the acorn grew the oak...

* And that was fast!

OIH traded at around $262.18 this morning (I was adding on weakness).

Now up on the day at $268.75:

From this morning:

My Ludacris Forecast is that after trading much lower this morning, energy stocks have a reversal day to the upside.

I added to (SLB) , (OIH) and (OXY) on weakness this morning.

Or just wishin' and hopin'!

By Doug Kass Sep 11, 2024 12:10 PM EDT

BY Doug Kass · Sep 11, 2024, 1:17 PM EDT

My Ludacris Forecast is that after trading much lower this morning, energy stocks have a reversal day to the upside.

I added to SLB, OIH and OXY on weakness this morning.

Or just wishin' and hopin'!

BY Doug Kass · Sep 11, 2024, 12:10 PM EDT

BY Doug Kass · Sep 11, 2024, 11:39 AM EDT

I made a mistake in covering my recent Berkshire Hathaway BRK.B short. (I also covered too early my Apple AAPL and Goldman Sachs GS shorts)

I got the top and took a small amount out of the short.

BY Doug Kass · Sep 11, 2024, 11:25 AM EDT

Moved to very large MSOS on weakness.

BY Doug Kass · Sep 11, 2024, 11:15 AM EDT

Homebuilders and private equity are the downside leaders.

BY Doug Kass · Sep 11, 2024, 10:55 AM EDT

I'm adding to VRNOF, TSNDF and MSOS.

BY Doug Kass · Sep 11, 2024, 10:45 AM EDT

From Peter Boockvar:

CPI about in line, 50 bps rate cut odds down to just...

August CPI rose .2% headline and .3% core m/o/m with the former as expected and the latter one tenth above. Due to rounding, the y/o/y figures were in line at 2.5% and 3.2% respectively. Energy prices were down by .8% m/o/m and 4% y/o/y. Food prices rose .1% m/o/m and 2.1% y/o/y. Eating out continues to be where the food inflation is as prices here rose .3% m/o/m and 4% y/o/y. Offsetting this is eating at home as prices were flat m/o/m and up just .9% y/o/y.

Services inflation ex energy rose .4% m/o/m and 4.9% y/o/y and continues to be driven by higher rents as calculated here. Yes, they are delayed in reflecting the reality on the ground but they NEVER fully reflected the rise seen a few years ago. Owners’ equivalent rent was up .5% m/o/m and 5.4% y/o/y. Rent of Primary Residence saw a .4% m/o/m and 5% y/o/y increase. In reality, blended rents are rising by 2-3%. The other major contributor to CPI is medical care where prices fell for a 2nd month, by one tenth m/o/m, though are up 3% y/o/y. Keeping a lid on prices in healthcare was the one tenth fall in ‘professional services’ which includes lower prices for dental and eye care and no change in physicians services. Hospital care though rose .4% m/o/m and by 5.8% y/o/y. Health insurance prices rose .1% m/o/m and by 3.8% y/o/y and that reality does not exist unfortunately, and is dramatically understanding reality.

Insurance prices are still out of control on the vehicle side, rising by .6% m/o/m and 16.5% y/o/y (only slowing because of the tough comps). Vehicle maintenance prices also were up .6% m/o/m and higher by 4.1% y/o/y. Airline fares rebounded by 3.9% m/o/m after sharp declines in the months before. They were lower by 1.3% y/o/y though. Hotel prices jumped 2% in the month and are up 1.8% y/o/y. Rental car prices fell 1.5% m/o/m and by 8.4% y/o/y.

On the goods side, core prices fell for a 3rd month, by .2% and down by 1.9% y/o/y. Lower used car prices again were the main reason as prices here fell 1% m/o/m and down by 10.4% y/o/y. New car prices were flat m/o/m and down by 1.2% y/o/y. Apparel prices rose .3% m/o/m and by the same amount y/o/y. They were down by .4% in July from June. Goods deflation continued with anything related to the home as ‘household furnishings and supplies’ prices fell .3% m/o/m and 2.6% y/o/y.

Bottom line, the goods deflation continues on, offset by persistent gains in services. Rents should continue to moderate but at some point goods prices will bottom, especially used car prices as discussed this morning. As the data was about in line, inflation expectations in the TIPS market are rebounding after the big declines. Treasury yields jumped too as the Fed is only likely raising 25 bps next week. The 2 yr yield went to 3.68% from 3.58% and the 10 yr yield rose by 6 bps to 3.68%.

Odds of a 50 bps rate decrease next week have fallen to just 14% vs 30% Friday and 44% one week ago.

2 yr yield intraday

BY Doug Kass · Sep 11, 2024, 10:35 AM EDT

Viking Therapeutics initiated with an Overweight at JPMorgan JPMorgan initiated coverage of Viking Therapeutics with an Overweight rating and $80 price target. The firm also placed the shares under a "positive catalyst watch" ahead of the the Phase 1 data readout for the oral-2735 drug at Obesity Week, November 3-6. The data could point to a highly competitive profile, which is underappreciated in the shares, the analyst tells investors in a research note. The firm continues to think the market for GLP-1s will be substantial, with U.S. market sales of $120B in 2030, and says orals will play an increasingly important role. It recommends being long Viking shares into the upcoming readout for oral-2735, which it thinks "should lead to substantial up move for shares."

Petco price target raised to $3 from $2.75 at Wells Fargo Wells Fargo raised the firm's price target on Petco to $3 from $2.75 and keeps an Equal Weight rating on the shares. The firm leans positive post-Petco's Q2. Profits/free cash flow are a clear priority, Q2 comps beat and Q3 is expected to be better quarter-over-quarter with a profit inflection on deck. While a step in the right direction, strategic details are still thin and a heavy lift remains, Wells adds.

Arm remains a favored play on emerging Edge AI, says Morgan Stanley Morgan Stanley analyst Lee Simpson notes that the Apple (AAPL) iPhone 16 release on Monday suggested the utilization of an Arm-based A-series processor, the A18, in device. Arm (ARM) remains a favored play on the emerging Edge AI opportunity, adds the firm, which expects mobile to drive initial upside, followed by infrastructure and autos. The firm keeps an Overweight rating and $175 price target on Arm, which Morgan Stanley named as "joint Top Pick" in the space along with ASM International (ASMIY) on September 5.

BY Doug Kass · Sep 11, 2024, 10:14 AM EDT

As global economic growth weakens, more signs of "slugflation":

douglas cassel

Europe has been worrying about economic decline and techno-stagnation for a quarter of a century. The gnawing angst has finally given way to something closer to panic.

The eurozone has scarcely grown for seven quarters, and fiscal austerity has yet to begin. Germany has seen no accumulated growth since 2018. The dawning awareness that next year may be just as bad has finished all remaining illusions. So has fear of the “China shock 2.0”, this time larger and rising far up the technological ladder. “If we go on like this, Europe is simply going to die,” said a doyen of the EU illuminati.“

America innovates, China replicates, Europe regulates. It is an extraordinary picture of our situation, because it’s true,” said Italy’s prime minister, Giorgia Meloni.“

In 1990 the EU of 12 states made up 26.5 percent of world GDP. Today the EU of 27 states makes up 16.1 percent, while the US is still at 26 percent. We were a big weight in the world but that is no longer the case,” she said. (Source: telegraph.co.uk)

BY Doug Kass · Sep 11, 2024, 10:00 AM EDT

Bonus — Here are some great links:

Massive Top in Consumer Discretionary

Gold Attempting a Break Out From 50 Year Rising Channel

BY Doug Kass · Sep 11, 2024, 9:45 AM EDT

I am pressing my XLU short.

BY Doug Kass · Sep 11, 2024, 9:40 AM EDT

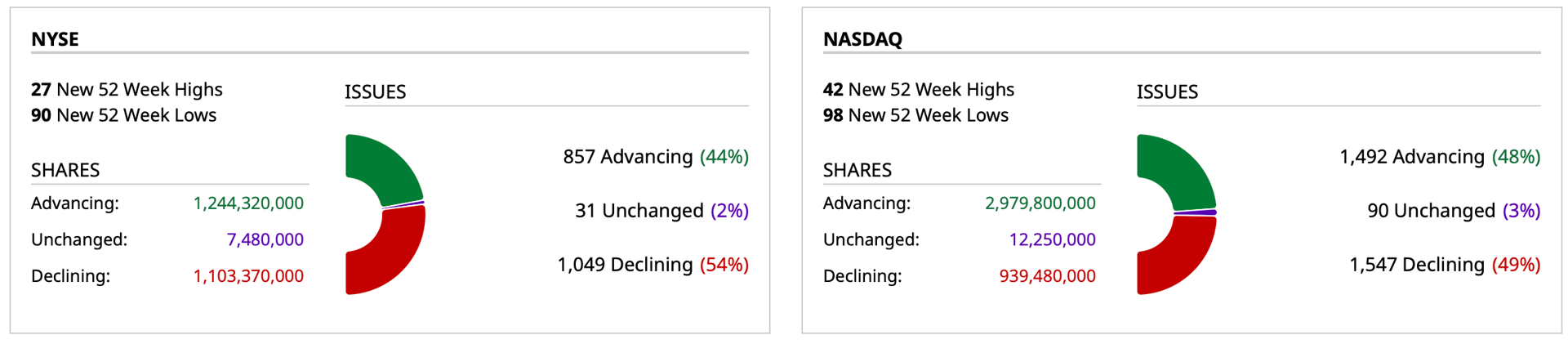

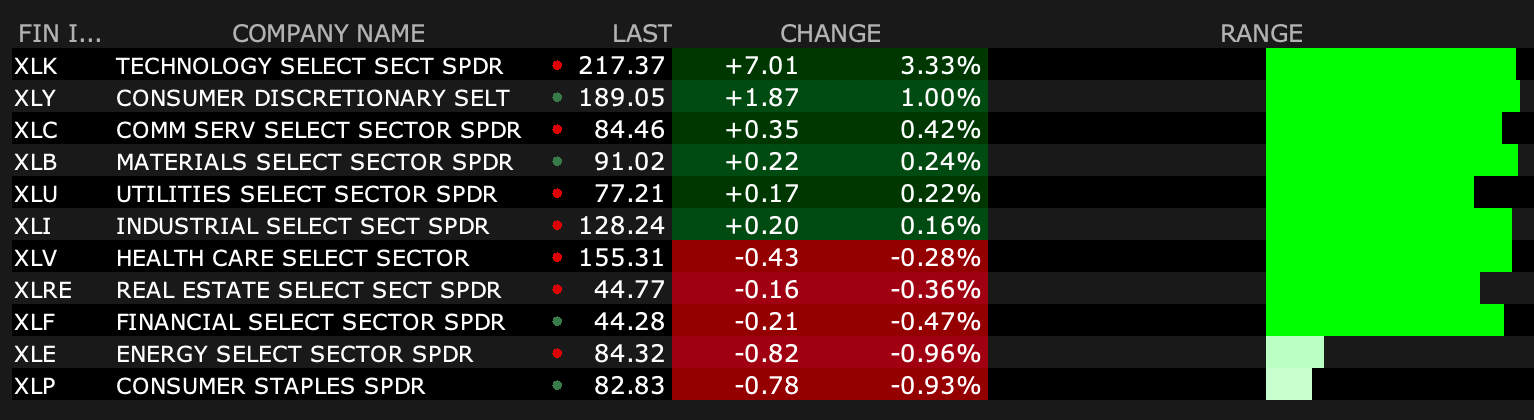

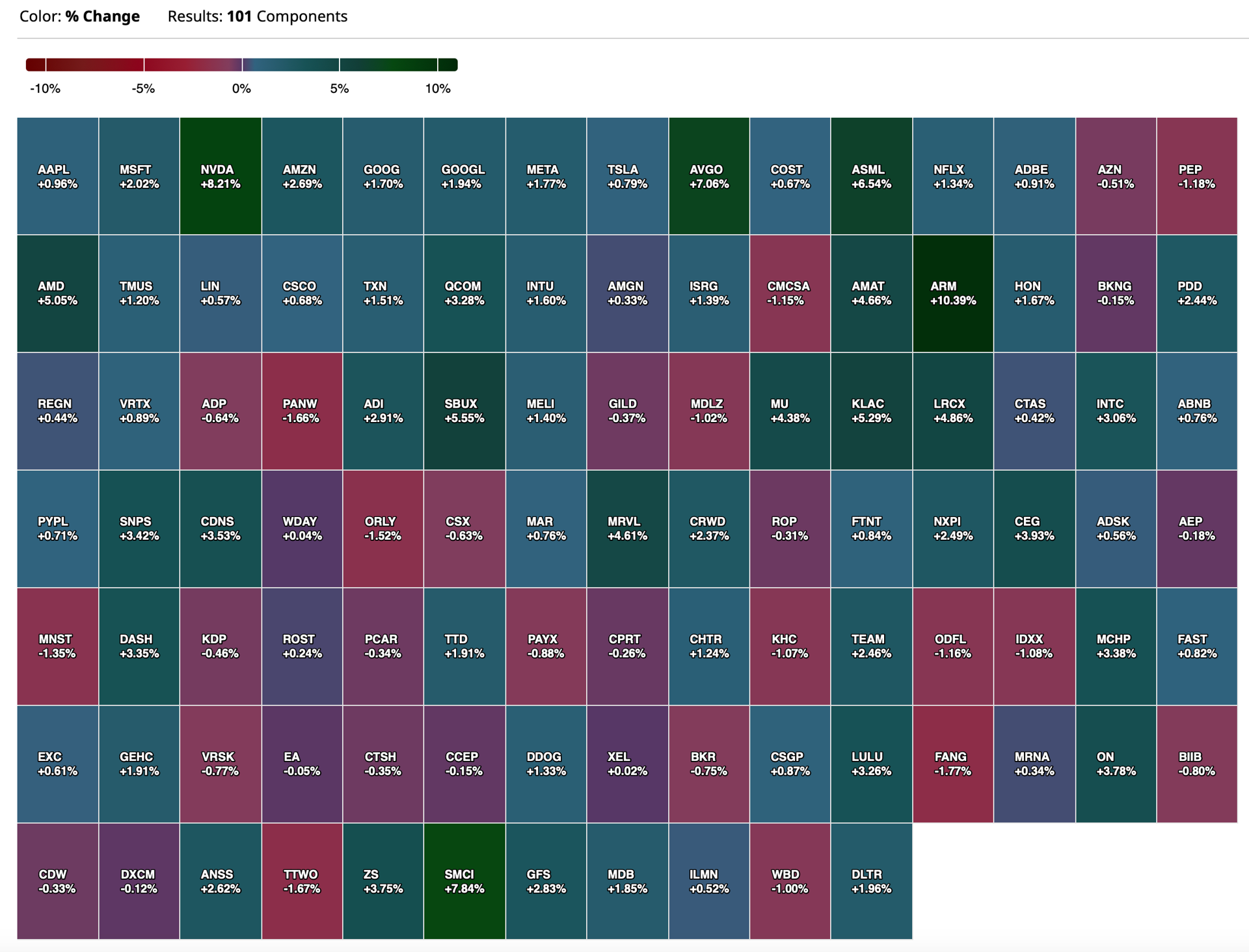

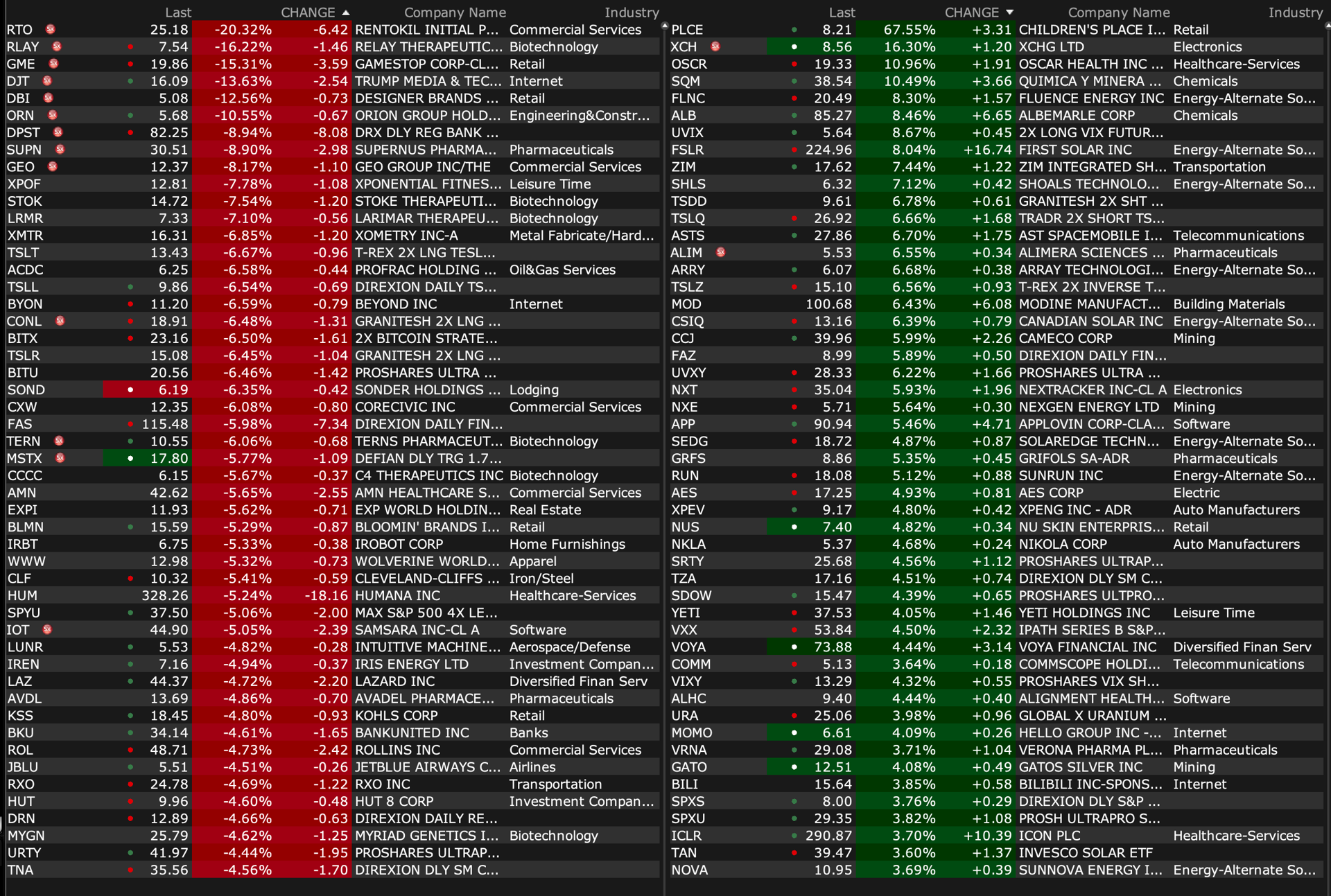

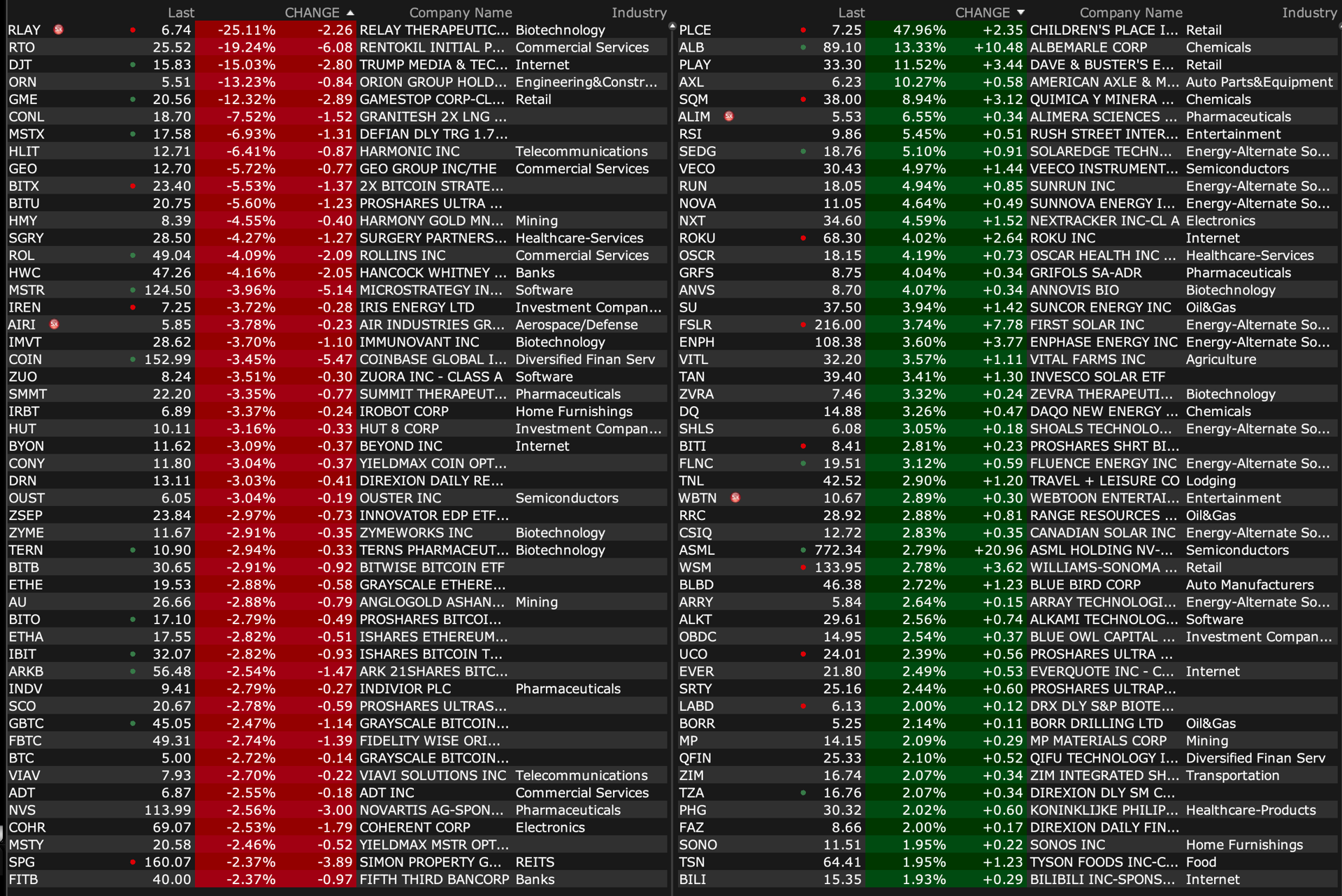

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Sep 11, 2024, 9:30 AM EDT

-BCTX +126% (Phase 2 Bria-IMT study demonstrates Median Overall Survival of 15.6 months in most recent patients (treated since 2022) v 6.7-9.3 months for similar patients reported in the literature, with no drug related discontinuations to date)

-FTCI +66% (announces multi-year Tracker Supply Agreement with Strata Clean Energy)

-PLCE +51% (earnings)

-ALB +14% (Contemporary Amperex Technology confirms it will adjust production from its lithium carbonate mine in Yichun, China)

-MSB +14% (earnings)

-PLAY +12% (earnings)

-INNV +12% (earnings, guidance)

-ACTU +5.7% (receives FDA Orphan Drug Designation for Elraglusib for Treatment of Soft Tissue Sarcomas)

-SIDU +5.3% (announces an additional contract award for NASA ASTRA)

-VKTX +4.5% (JPMorgan Chase and Co Initiates VKTX with Overweight, price target: $80)

-EPM +3.2% (earnings)

-RIG +2.8% (announces $232M ultra-deepwater drillship contract)

-TBIO -59% (plans to delist its securities from the Nasdaq Stock Market)

-DBI -27% (earnings, guidance)

-RLAY -24% (prices ~28.6M shares at $7/share)

-TOVX -14% (files $200M mixed shelf)

-DJT -13% (weakness following Harris/Trump Presidential debate, Taylor Swift endorsement of Harris)

-GME -13% (earnings)

-ORN -13% (prices underwritten public offering of 4.86M shares of its common stock at a public offering price of $5.15/shr)

-VRA -13% (earnings, guidance)

-CTLP -6.7% (earnings, guidance)

-MANU -4.7% (earnings, guidance)

-GEO -4.4% (weakness following Harris/Trump Presidential debate)

-MAMA -3.5% (earnings)

-ROL -3.4% (UK competitor Rentokil warned of weakness in N.A.)

-FEIM -3.1% (earnings)

-NVS -2.5% (Tier 1 Firm downgrade)

-WOOF -2.2% (earnings, guidance)

BY Doug Kass · Sep 11, 2024, 9:15 AM EDT

As of 8:29 a.m.:

BY Doug Kass · Sep 11, 2024, 9:05 AM EDT

From JPMorgan:

US: Futs are lower post-Debate and pre-CPI. Betting markets reflecting a Harris victory in the debate as her odds to win had her leading Trump by 1-point as the debate started to now 10-points this morning; Treasuries had minimal moves during the debate, but yields are 3-4bps lower now. Pre-mkt, Mag7 and Semis are lower as Energy/Materials are higher. USD is lower and cmdtys are higher led by Energy, Ags, and Precious. The macro data focus today is on the CPI print, Mortgage Applications, and the 10Y bond auction.

and...

EQUITY AND MACRO NARRATIVE: Much of yesterday’s price action seemed to reflect increasing concerns over economic growth as evidenced by our Delta One team’s Recession L/S basket (JPRECES Index in BBG) moved as much as +2.0z, before closing +0.6z, and at the sector level more cyclical sectors (Energy, Financials, Industrials, and Materials) underperformed. The move was acute in WTI which fell more ~3.5% to under $66.31, its lowest level since summer 2023. This behavior echoes some of what we experienced in August where an extreme shock gave way to a growth scarce that was assuaged by Retail Sales. The next Retail Sales print is next week; the Fed’s GDPNow is forecasting 2.5% growth for 24Q3 as of Sep 9. This is aligned with PMI commentary from S&P’s Chief Economist who sees their data pointing to 2.0 – 2.5% real GDP growth this quarter. The early bearish action in the market gave way to a rally in the second half of the day. Client conversation reveal a sense of uncertainty with a lack of consensus across the upcoming catalysts.

BY Doug Kass · Sep 11, 2024, 9:00 AM EDT

As of 8:48 a.m.:

BY Doug Kass · Sep 11, 2024, 8:55 AM EDT

* Adding to MSOS long $6.94.

* Adding to XLU short $77.26.

BY Doug Kass · Sep 11, 2024, 8:40 AM EDT

* This column emphasizes the obvious and something I should spend more time dwelling on.

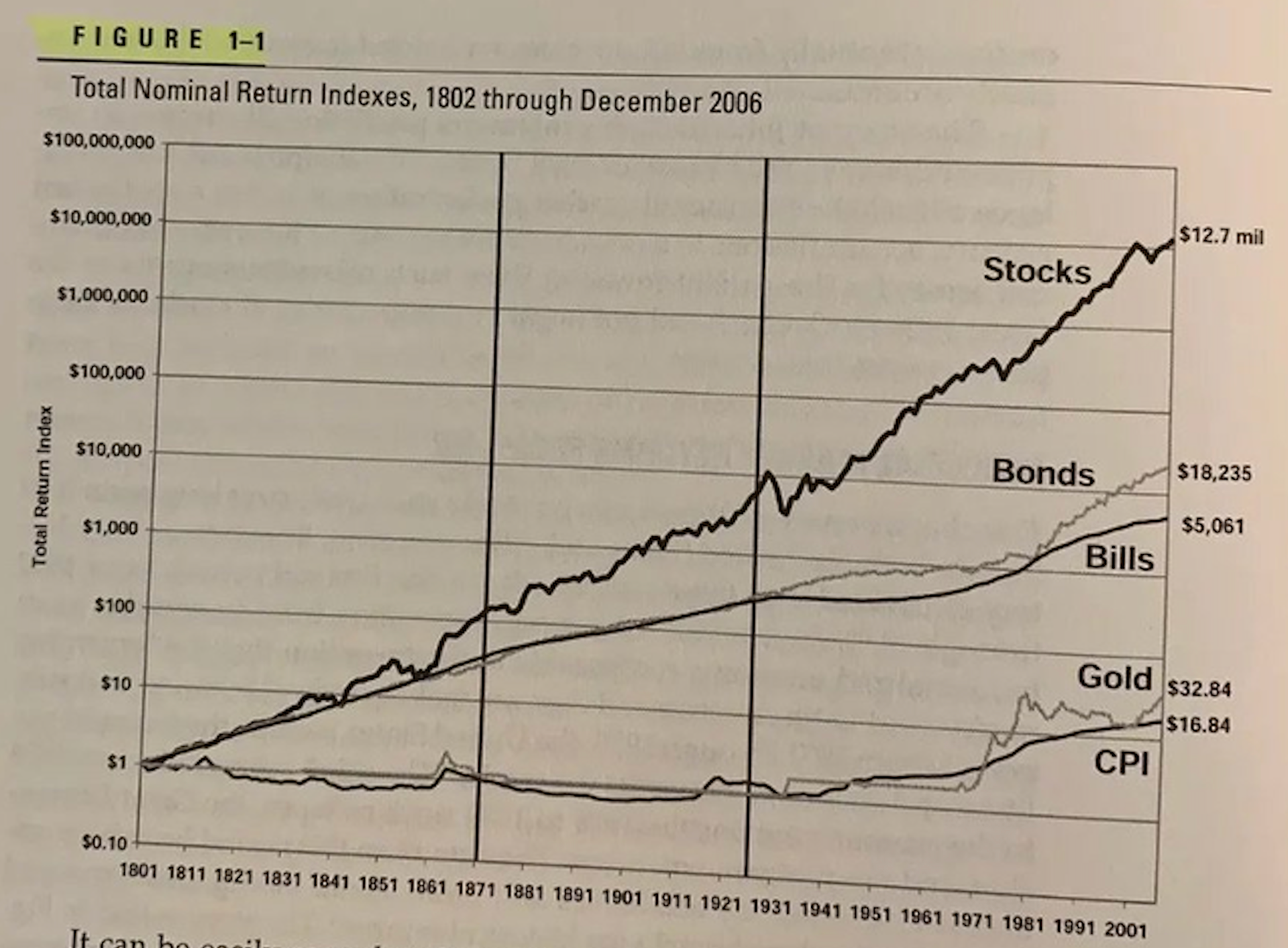

* It is frankly sometimes lost by myself (and by others) that equities perform better than any other asset class over lengthy periods of time.

* As well, the asymmetry of returns on long positions vs. returns on short positions are both profound and tautological.

* Currently, many equities have been ignored by investors and have performed far weaker than the averages — this is the fertile ground for my long selections (now).

* Moreover, the multitude of my fundamental concerns (listed in this column) are slowly being embraced by the consensus and are beginning to be discounted in the markets' recent decline (as always we should be "second level" thinkers).

* For these reasons and others I am now transitioning somewhat from my pairs strategy of the last nine months.

* I have also retreated from my layer of shorts that were superimposed with the pairs.

* I am now returning to "the land of the living" and an expanded net long exposure — particularly if those specific stocks that I currently deem attractive on a risk/reward basis (MSOS, OXY, SLB, OIH, DIS, VVV, CMG, etc) and others that I am yet to own — continue to the fall as they notably have during the first week of September and over the last few months.

What follows is a compilation of recent commentary in my Daily Diary on the TheStreet Pro and comments delivered to my investors at my hedge fund, Seabreeze Partners:

In early August I warned my investors:

"As a result, we are growing more confident that stocks will ultimately decline to a level in which we will want to participate on the long side... While a good entry point may lie ahead — it may come from still lower levels."

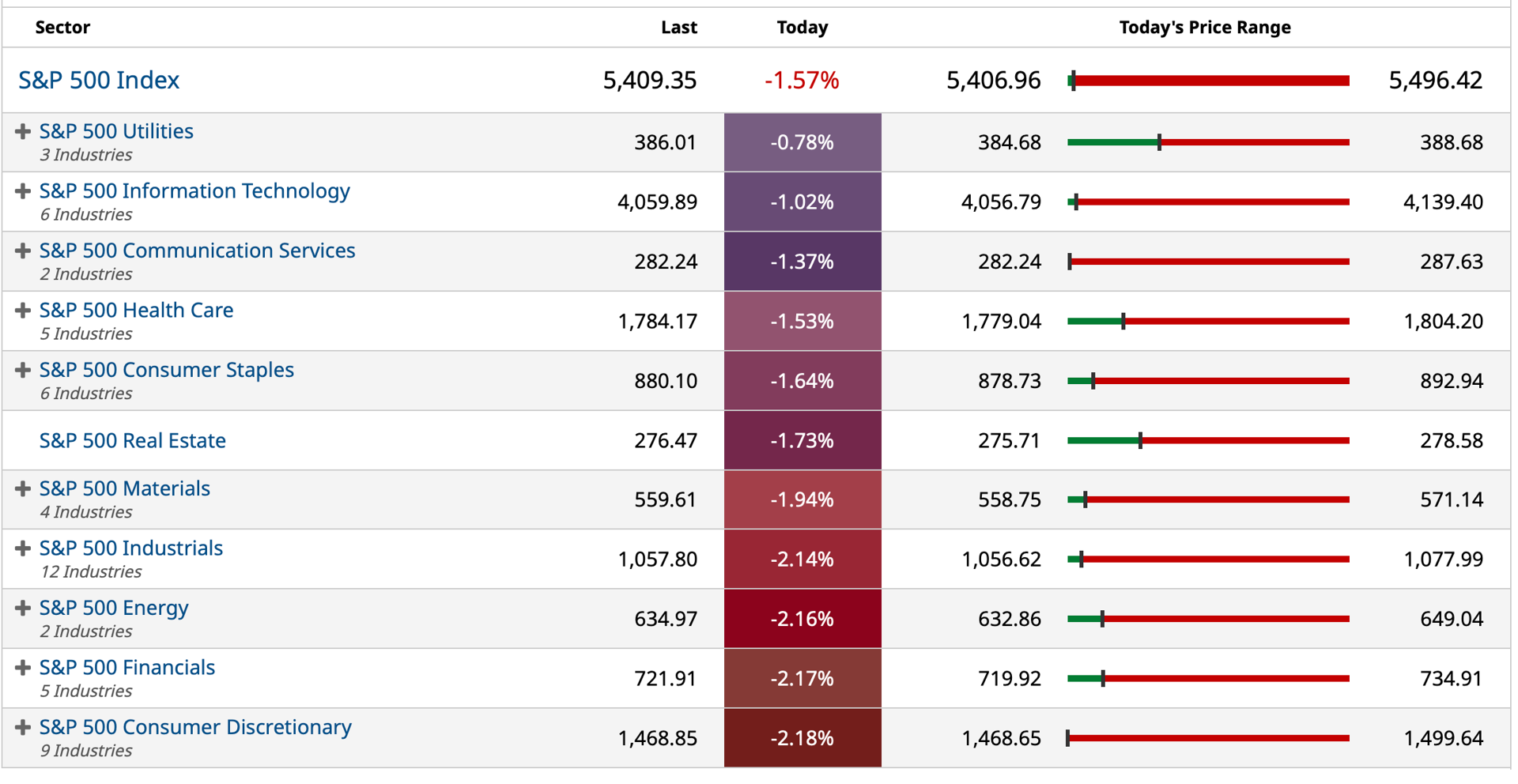

Over the first few days of September equities quickly declined by about five percent — and have rallied a bit from there but remain lower for the month:

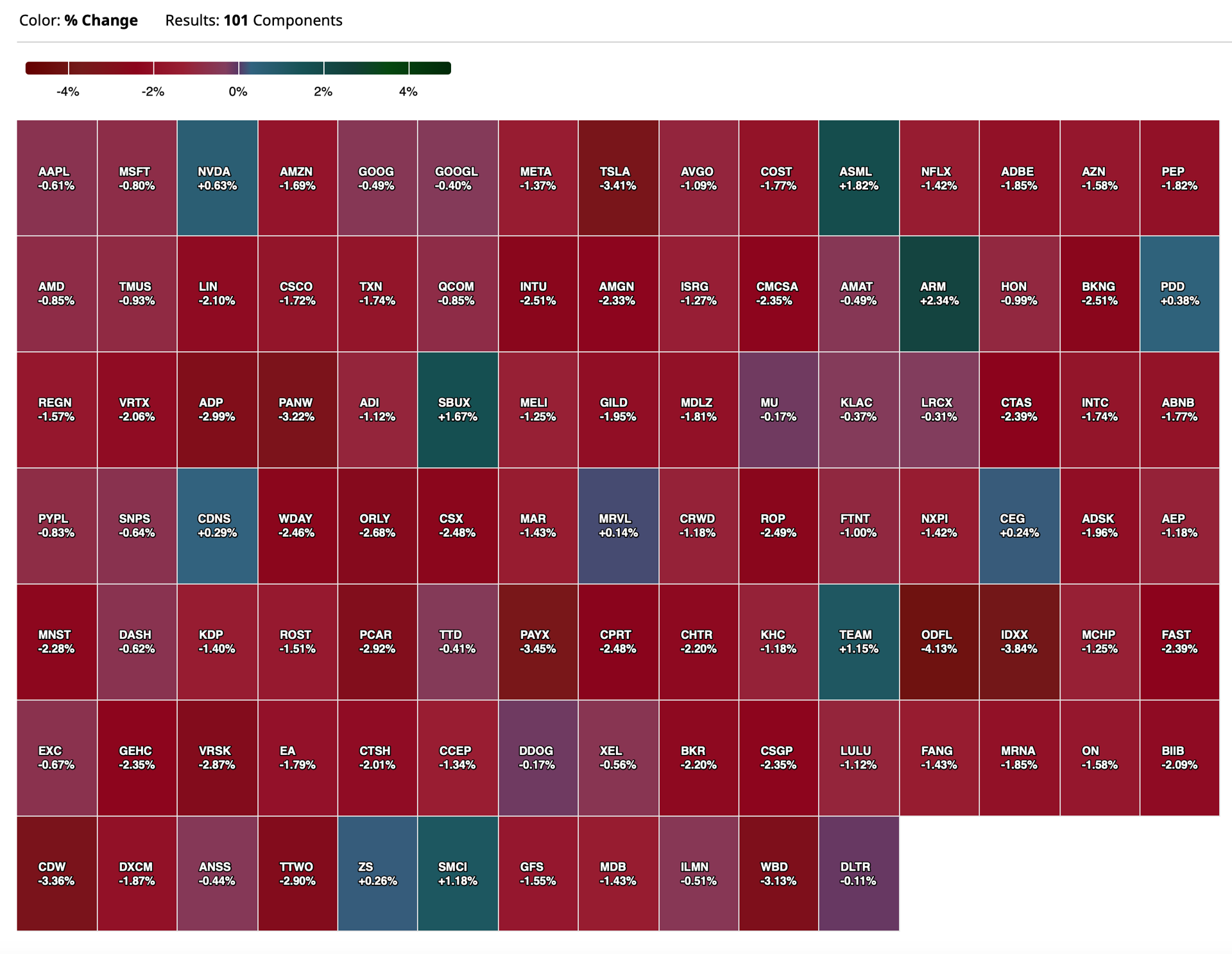

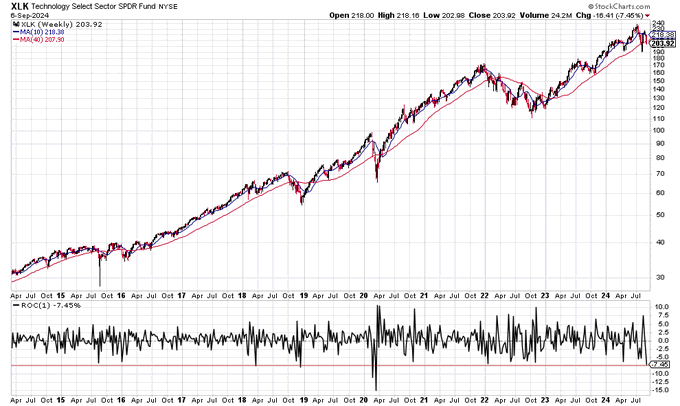

My defensive positioning has insulated our hedge fund (Seabreeze Partners) from the September decline — which has been far worse (on a percentage basis) for The Magnificent Seven (Microsoft MSFT, Amazon AMZN, Apple AAPL, Alphabet GOOGL, Meta Platforms META, Nvidia NVDA and Tesla TSLA) and some of the other former market leaders. Indeed, large-cap technology stocks (as measured by XLK) had its worst week since Covid (and one of its worst weeks in the past decade):

In Act I, Scene 3 of William Shakespeare's "Hamlet," Polonius (Ophelia's father and King Claudius' chief minister) delivers a long monologue that contains several seemingly good pieces of advice — the most important of which appears below:

I have long held to the notion in my Diary and to my Limited Partners that we don't believe in being "Perma" anything — I manage my Partnership's portfolio by evaluating upside reward vs. downside risk — with a calculator in hand and through sharp and hard-hitting primary analysis. As a contrarian — armed with a sense of intrinsic values — I am willing to buy weakness and sell strength. (Of importance I avoid distractions and invest/trade unemotionally. I generally avoid charts of which there are many nice ones that lie at the bottom of the sea! Nor do I listen to the memorized sound bytes and confident but superficial analysis in the business media).

So, to paraphrase Shakespeare, "neither a Perma Bull, nor a Perma Bear be.”

The most important feature of this morning's column is that I want to emphasize, again, that I fully recognize that equities perform better than any other asset class over lengthy periods of time.

Long investments generally create and generate wealth (see the chart below) while being short equities (though providing asymmetric returns over extended timeframes) can protect capital over more limited intervals:

This year I have held to an ursine market outlook reflecting the prospects for slowing global economic growth and sticky inflation (we call this "slugflation"), that high short-term interest rates provided equity-like returns (with little volatility and risk), the perils associated with market structure and a changing market landscape (in which machines and algos had a disproportionate role on stock prices), feckless fiscal (the massive annual deficit and accumulated U.S. debt load are draining the potential for economic growth) and wrong-footed monetary policies, growing political and geopolitical risks and too ebullient bullish investor sentiment (which was reflected in high valuations).

Though I maintained a negative market view, I elected not to run a large short book.

Rather, I adopted a defensive pairs trading and investing strategy that incorporated both longs and shorts (much like the father of the hedge fund industry, Alfred W. Jones, introduced 75 years ago).

On top of our pairs strategy, I superimposed a short book of between 10% and 20% gross short exposure, on average, throughout 2024. Many of those unhedged and core investment shorts fared well, despite the market's gains (e.g. RILY, WGO, CHGG, WOOF, FIGS, MCD, SBUX, etc.). Others (like Index hedges) sometimes proved problematic in the FOMO — like rally this year. But also helping was opportunistic trading — the benefit of which was derived by the dominance and influence of machines and algos that often exaggerate short term price moves.

This strategy provided our hedge fund with positive returns — without taking unnecessary risks — despite our gloomy market view.

While I continue to be concerned about the equity markets I am now less so for the following reasons:

* The multitude of my concerns (listed above) are slowly being embraced by the consensus and are beginning to be discounted in the markets' recent decline.

* While overall valuations are still elevated, a number of individual equities have suffered even as the averages have enjoyed robust market gains this year. This expanding universe of beaten-down stocks provide us with fertile territory for selecting new long investments.

* Interest rates are likely to drop significantly — providing less of an alternative to equities.

Accordingly, I am now transitioning from our pairs strategy and I have retreated from our layer of shorts. I envision returning to "the land of the living" and an expanded net long exposure — particularly if those specific stocks that I currently deem attractive on a risk/reward basis continue to the fall as they notably have during the first week of September and over the last few months.

As always, my plan to increase our net long exposure is a dynamic one. It will be a function of a continued evaluation of the bigger picture (economy, interest rates, inflation, policy, sentiment, valuations, etc.). But given that many stocks have retreated far deeper than the Indices, our exposure decision will now be as much subject to the opportunities presented in individual securities as in our market macro view/judgment.

I have already shifted from a sliver of being net short to a sliver of being net long — with a number of opportunistic buys late last week. This shift is consistent with last month's comments to my investors in which I wrote:

"As (or if) stocks continue to fall and we begin to transition from a defensive pairs strategy into a modestly more bullish (and opportunistic) longer positioning, our monthly returns are likely to exhibit much more volatility than we have experienced over the last nine months."

I expect more volatility ahead. While this may scare some investors, at my hedge fund I relish the opportunity to invest opportunistically and unemotionally. The continued lack of predictability will also provide us with trading opportunities intended to complement our investing.

I remain confident in my ability to navigate the volatile markets and uncertainties of economic outcomes because my analysis is objective, fundamental (understanding intrinsic values), hard-hitting and my investing is dispassionate.

As often stated, high stock prices are the enemy of the rational buyer and low stock prices are the ally of the rational buyer.

Since I am a value buyer, my fundamental approach and emphasis on in-depth security analysis (hopefully) provides me with a clear understanding of the intrinsic value of equities — allowing me to be increasingly greedy when others are overcome by fear.

BY Doug Kass · Sep 11, 2024, 7:45 AM EDT

* On this day, as has been the case for the past 23 years, my eyes remain full of tears

* The wound remains fresh and it doesn't get easier as time goes by

I repost this opening missive annually with a heavy heart...

Death leaves a heartache that no one can heal but love leaves a memory no one can steal.

As many subscribers are aware, on every anniversary of the World Trade Center tragedy on Sept. 11, I honor my closest friend who was lost 23 years ago — Chuck "Brown Bear" Zion — as well as the other victims of the terrorist attacks that day.

After more than two decades, it doesn't get easier.

Relatedly, five years ago I received this email from a mutual friend of Chuck's, Don Gher:

Dougie

A bit of a tear in the eye as I think about tomorrow. I remember the first time you and I talked. You called me and said Chuck told you we should meet. As we were about to hang up after talking, I said you should ask Chuck what was the best baby gift he ever received. About a minute after we hung up, my phone rang and I heard, "A leather bound book of magazines from the week Zachery was born with his name and birthday embossed in gold on the front!" Chuck proceeded to tell me that all these years later, there were times with no one in the house that he would pull the book out that I had made for him and, as he flipped through it, he would cry remembering when Zach was born.

Stay safe, my friend.

Donald L. Gher, CFA

A year ago I received another email from Don:

As we approach the day Chuck was murdered with so many others, I saw the following 9/11 prayer in my Parish Newsletter that is so appropriate and comforting:

May all of us remember with

love and compassion this day.

May we grieve with those who still mourn,

And share memories with those who cannot forget.

May we draw strength from those who bravely responded,

And gave their lives to save others.

May we stand with strangers who became neighbors that day,

And remember their generosity and hospitality.

Above all God may we remember your faithfulness

And learn to trust in your unfailing love.

Xavier University

Peace

Don

Sadly, Chuck Zion's dad, Rabbi Martin Zion, has passed away. Three years ago, the lovely Jane, Chuck's mom and Rabbi's wife, died. They have joined Brown Bear after all these years of separation.

Please read this column, "Keys to a Life Well Lived," that I had written about Rabbi Zion, based on a letter he sent me in October 2016, two months before his death:

"Who is wise? One who learns from every man ... Who is strong? One who overpowers his inclinations ... Who is rich? One who is satisfied with his lot ... Who is honorable? One who honors his fellows."

- Ben Zoma, Ethics of the Fathers

Today marks 23 years since the Sept. 11 World Trade Center tragedy. (Please take some time that day to watch Ground Zero Rising, Jim "El Capitan" Cramer's brilliant documentary on the attack and the subsequent rebuilding).

Sept. 11, 2001, is a day that we will forever remember with clarity and disbelief. I lost my best friend, while members of TheStreet community lost one of our own — the late Bill Meehan.

It still seems like only yesterday to me, and it's a day that I'll forever remember vividly. As I've written before, 2001 will for many of us forever be annus horribilis, the year of disaster.

On this day, as has been the case for the past 23 years, my eyes remain full of tears. I'm drafting this column in memory of all of those I knew (and didn't know) who lost their lives in the World Trade Center, in Pennsylvania and in Washington, D.C.

As I've written previously, it's said that death leaves a heartache that no one can heal, but that love leaves a memory no one can steal. And so it will be today as we observe the anniversary of the Sept. 11 attacks.

As I've done in each of the intervening years, I want to use my opening missive to repeat the thoughts that I've often expressed about Sept. 11. As always, I dedicate this column to those who were lost — especially to my best pal, Chuck Zion (a.k.a., "Brown Bear"):

"Chuck worked at Cantor Fitzgerald, the brokerage firm that lost nearly 700 employees 18 years ago. It was the hardest-hit company in the World Trade Center tragedy, accounting for nearly one-quarter of the building's deaths that day. I lost many friends at Cantor on Sept. 11: Eric, Pat, Timmy — too many to count. So did many others. And of course, we all lost one of TheStreet's own, Bill 'Budman' Meehan.

In Cantor Fitzgerald's equity division, none had more of a presence (literally and figuratively) than Chuck Zion. He was known to his friends and clients as "The Brown Bear," a sensitive, giving and caring friend; father to Zack; son to Martin and Jane; and husband to the amazing Carole ("Cheezy"). His love was pure, and there was never any pretense — not wordy, he was on point.

The largest producer over the past decade at Cantor Fitzgerald, Chuck was master of his universe. He was straightforward and clear-cut, a no-nonsense and respected partner who was remarkably generous but never, ever wanted others to know it. He gave often and substantially but always anonymously, without strings attached. Chuck, who also worked at Salomon Brothers and Sanford C. Bernstein, put on some of the largest trades in the history of the equities market. He was the player the "big boys" went to when they wanted anonymity. And I am talking multimillion-share trades, the really big prints.

And it was Chuck who introduced me to Bill Meehan. He even had me fill in for Budman on a few occasions in the Cantor Daily News.

I cherished and loved Chuck Zion — he was my confidante and a brother that I never had. When I moved to Florida in the late 1990s, Chuck introduced me to his father and mother — asking me to take them out once or twice a year, to look after them a bit. In time, Rabbi Zion and Jane became more than casual dinner mates; they became my mother and father, so Chuck and I really were like brothers (though absent the same blood).

I spoke to Chuck every morning at around 6:15 a.m. If I didn't call him on my direct line to Cantor's trading desk by 6:20 a.m., he'd get angry and yell at me in no uncertain terms! Invariably, legendary money managers Neil Weissman, Stanley Shopkorn, Dan Tisch or Phil Marber (Cantor's former CEO) would interrupt our daily calls. He would take their calls, and then shortly, Chuck would call me back. We rarely talked about the stock market, preferring to talk sports and food (his favorite activity!). Sometimes Chuck would tell me to check out Maureen Dowd's editorial piece in The New York Times ("Dougie, she is mandatory reading"), or who was on Imus that morning. I got him to buy a couple of harness horses with me for fun and he got a kick out of them as we followed their losing races. "We'll get him next time," he would say (his credo) — though we never did!

We played golf together (Chuck wrote the word "Lost" on each of his golf balls because he lost so many of them that he wanted the other players to know they were his), usually with Phil Marber or SAC's Andy Smoller. We talked NCAA football and basketball, especially about Syracuse University's teams (his alma mater). But mostly we talked about our children.

The Friday before Sept. 11, 2001, was my last day in the office, as I was leaving for Europe for 10 days. That day we spent a lot of time talking about his son Zack, reminiscing about the trip Zack and I had recently taken to New Haven to Yale University, where he watched me lecture at Dr. Robert Shiller's class on short-selling. Chuck was so proud of the way Zack had become a man. And he was nervously awaiting Greenwich High's football season with such anticipation. (They had won the state title the previous year, with Zack playing the offensive line.) Every time he talked about the upcoming season, his voice would rise several decibels. He was the proudest father on the face of the earth.

That Friday morning, the last day I spoke to Chuck, I was playing a Grateful Dead song in the background and I had Chuck on the speaker. Chuck was never what I would call "into" music. He was certainly not a fan of the Grateful Dead — maybe Motown, but not the Dead. Surprisingly, in our early morning talk, Chuck remarked how beautiful the song was. The song was Box of Rain, and the lyrics captured the concept of how short life can be.

Chuck's New York Times obituary is still taped to my stock monitor in my office as a forever reminder of his loss. The paper is now aged, yellowed and torn, but the scars still seem fresh.

Today, after writing this missive, I will again share Chuck's memories with his many friends (like Phil Marber) and with numerous longtime subscribers to TheStreet and TheStreet Pro (like Don Gher who has already sent me a note and prayer posted earlier). They were all Brown Bear's business associates, recipients of his wise advice or just friends — and who, as they have every year, will pass on their day's thoughts to me in e-mails or phone calls, which I eagerly anticipate and will always cherish.

TheStreet Pro subscriber Don Gher mailed me a classic story [four years ago] about Brown Bear. Don was thinking about Chuck and relayed that one of his pals, ex-Cantor Los Angeles and Dallas trader Eddie Weber, told him that one day he was at Cantor's NYC office, and he and Brown Bear walked out of the World Trade Center to grab lunch. There was a hot dog vendor there, and Chuck asked how many he had left. The guy said 12, and Chuck said, "Sold!" And then they proceeded to eat all of them. That was my brother, Chuck — an original.

I will never forget Mark Haines' report on CNBC of the first, second, third and fourth incidents that day, as I watched the horror on a television on a cruise ship in the Mediterranean.

And I will never forget the real-time reporting — the confusion and emotion — at TheStreet on that fateful day, the revelation of the extent of the tragedy and the follow-up tributes by our contributors. (TheStreet's headquarters were physically very close to Ground Zero.)

Ironically or sadly, the Jewish New Year (Rosh Hashanah) and Yom Kippur (the Day of Atonement) quickly followed on the heels of Sept. 11, 2001.

The most poignant recollection on TheStreet was the following post by Jim "El Capitan" Cramer, who recalled an incident at his synagogue. To this day, it always brings me to tears:

"At our synagogue last night on the eve of the Jewish New Year, our rabbi asked us to shout out the names of friends and family that we'd lost that day. There were so many names, it was frightening and I was glad we had left the kids at home. I felt honored to yell out Bill's name. And I feel honored to have gotten to meet and work with him in his short time on earth. Oops, wanted to cry as I wrote that. Could feel it coming on. Nope, no can do. Not with that picture of him in my mind wearing that funny floral shirt. He wouldn't want us to remember him in any other way than with laughter. God bless your soul, Bill. God bless the Meehan family."

- Jim Cramer, Remembering Bill Meehan

Today I will also share my fond memories of TheStreet's and Cantor Fitzgerald's Bill Meehan with his good pals Jim Cramer, Tony Dwyer, Herbela Greenberg and others, and we will all toast him as so many subscribers did in the fall of 2001.

"All that's necessary for the forces of evil to win in the world is for enough good men to do nothing."

- Edmund Burke

Fortunately, on May 2, 2011, some very good and courageous men gained revenge for Osama bin Laden's deeds some 10 years earlier. I hope bin Laden rots in hell, but revenge doesn't reverse the loss of so many.

As Samuel Johnson once wrote: "Revenge is an act of passion; vengeance of justice. Injuries are revenged; crimes are avenged."

I suppose that living and remembering are the best forms of revenge.

Thanks for reading this, and thanks for letting me wear my feelings on my sleeve.

... As you watch the annual tribute in downtown New York City this morning, I think about our lost loved ones and how lucky we all are. We all miss you, Chuck.

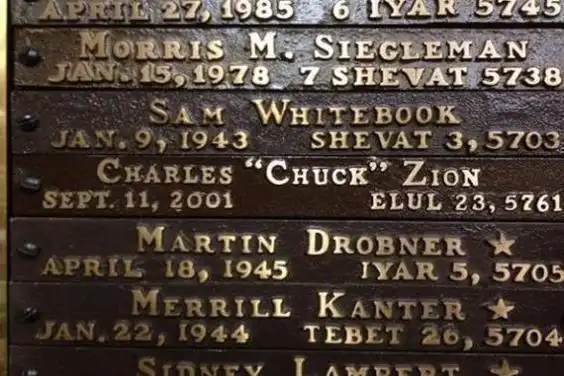

Below is a plaque memorializing Chuck at Temple Emanuel in Davenport, Iowa, where his dad Rabbi Martin Zion led the congregation:

Finally, I dedicated my book, Doug Kass on the Market: A Life on The Street to Chuck Zion — so that every time I pick up my book, I think about and feel ever closer to my pal.

__________

Though decades ago, the wound is still fresh as I think about Chuck often — I know I will for the rest of my life.

That was the way it was meant to be.

Last night, with tears in my eyes and with such respect for the first responders, I was watching 60 Minutes, which devoted a full hour to 9/11 and the FDNY — and the many that gave their lives to rescue others.

I suppose what separates us from the animals, what separates us from the chaos, is our ability to mourn people we've never met.

I mourn them all and I am in awe of the ultimate sacrifice that so many made twenty three years ago today.

RIP Brown Bear.

BY Doug Kass · Sep 11, 2024, 7:00 AM EDT

BY Doug Kass · Sep 11, 2024, 5:58 AM EDT