* In response to my opener on AI and my musings on OXY...

Dougie

ICYMI, I did an interview with Jeff deGraaf where I asked when "OXY becomes a better stock to buy than NVDA -- and "never" is not an acceptable answer".

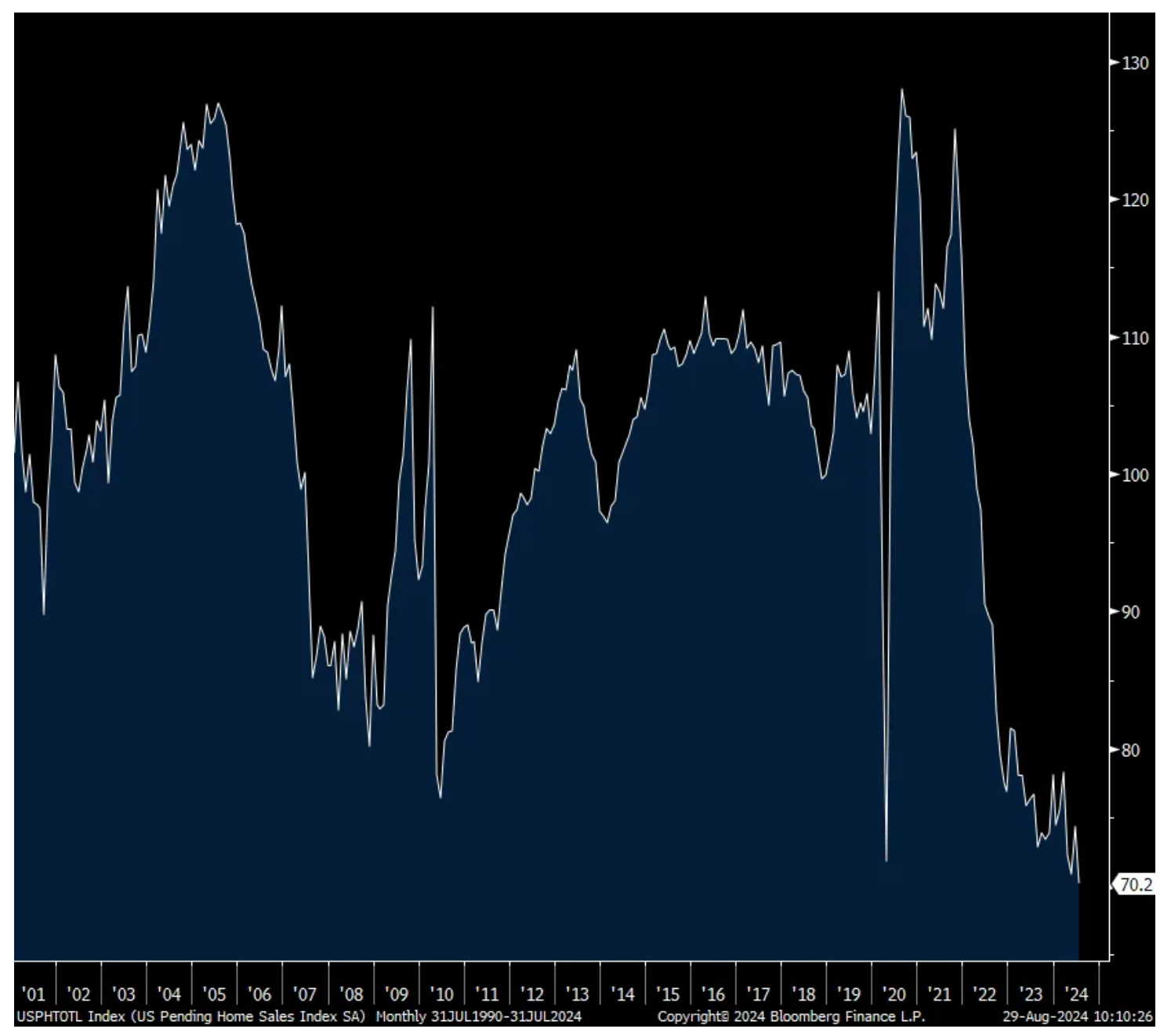

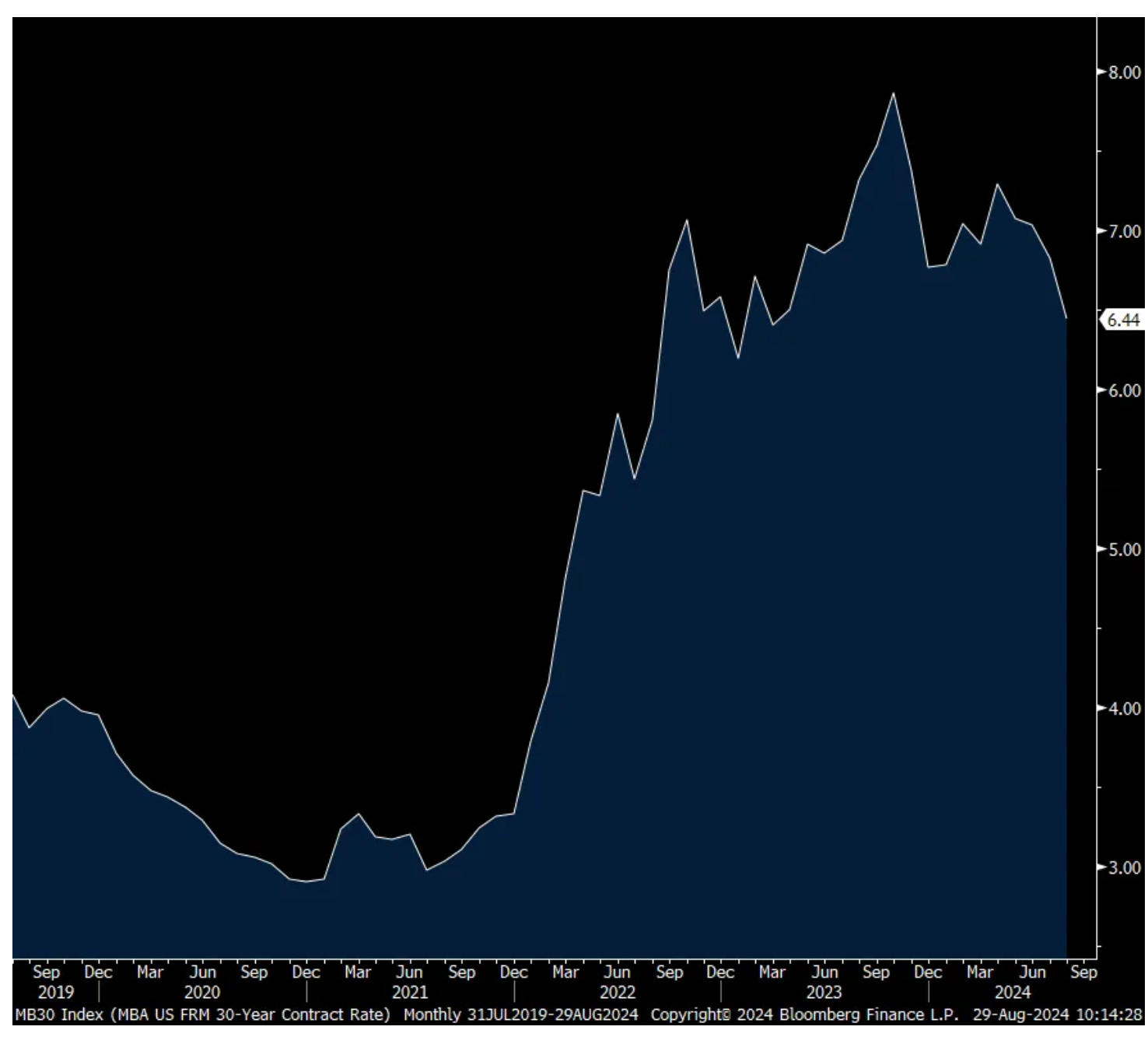

Not yet really capturing the timeframe where mortgage rates fell the most (that happened in August), July pending home sales were soft, falling by 5.5% m/o/m vs the estimate of up .2%. This follows a 4.8% rise in June and they are down 4.6% y/o/y.

The NAR said “A sales recovery did not occur in midsummer. The positive impact of job growth and higher inventory could not overcome affordability challenges and some degree of wait-and-see related to the upcoming US presidential election.” I’ll fade the latter excuse as while one side has offered $25k to a prospective home buyer if elected, it has almost zero chance of being passed and even if it did, the price of the home will likely go up by $25k and completely offset it.

The real challenge remains price and supply, as we know, and I think we should wait to see the September/October housing data to really glean the impact of the recent move lower in mortgage rates. As for potential supply, a 6% mortgage rate may not bring that much more as around 80% of mortgage holders have a rate less than 5% but we’ll take all the supply that can be provided.

Bottom line, this index goes back to 2001 and the July read was the lowest seen. As stated though, let’s wait a few months to see to what extent the move lower in mortgage rates, if sustained, triggers more activity as it hasn’t happened yet as seen with weekly mortgage applications. And if all the lower mortgage rates do is bring more demand without a corresponding pick up in supply, ever higher home prices would just offset the benefit of lower rates.

The Question Every Index, Big-Cap Investor Now Needs to Ask

From Peter Boockvar:

The question every index, big cap investor now needs to ask/Earnings run through

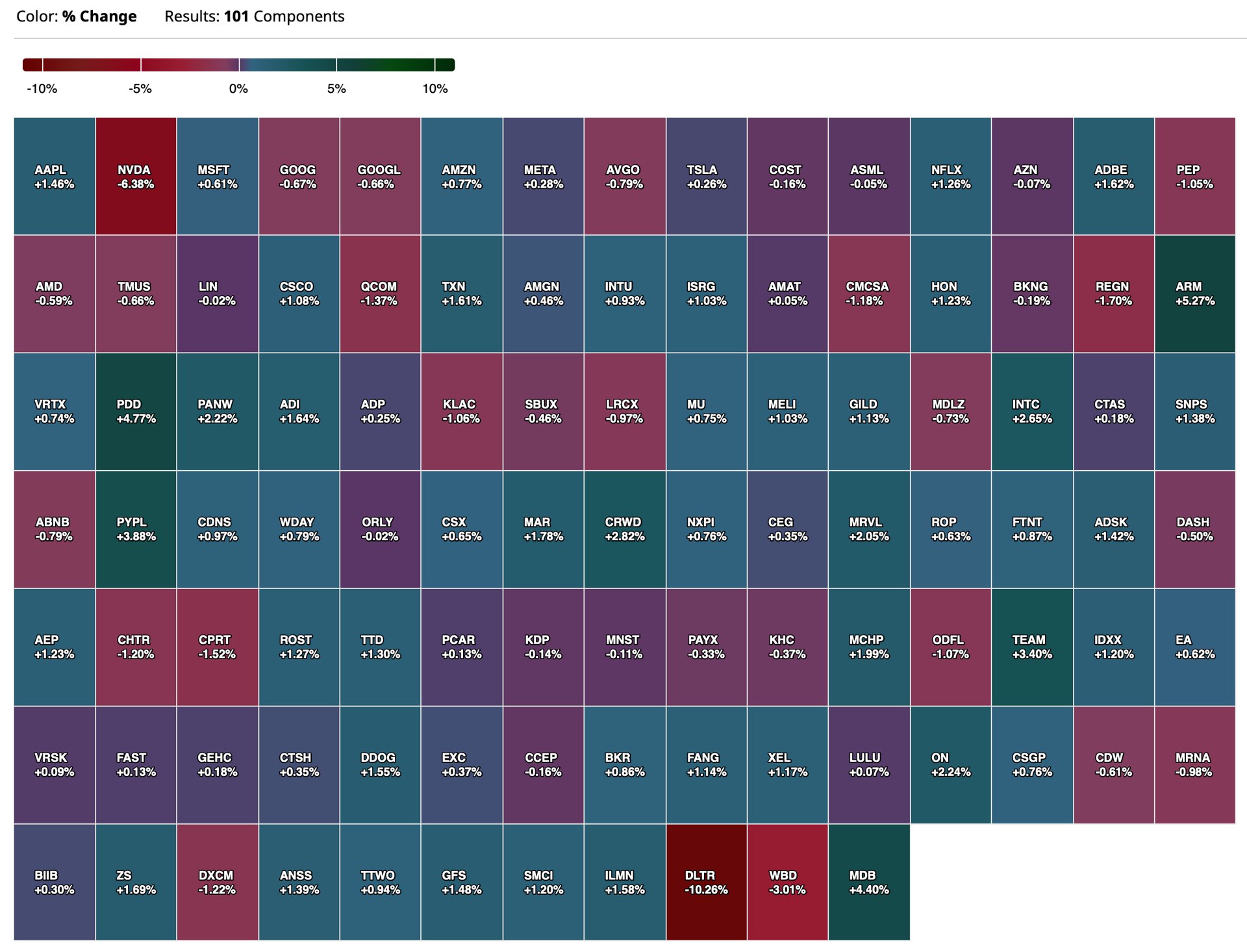

The stock market question we should now all be asking, post Nvidia's earnings where its clear that Wall Street earnings expectations and actual results have dramatically closed the gap, and where 5 of the 7 biggest stocks are now trading below their pre earnings levels (Meta and Apple above), even with the S&P 500 near its highs again, is there a possibility that a market baton could be passed now to other things. Is it now possible that the incredible outperformance where the biggest stocks now have market caps exceeding entire country GDP's will now be more pedestrian relative to the rest of the market as the AI spend/monetization hype quiets down? I believe it is but we'll of course see.

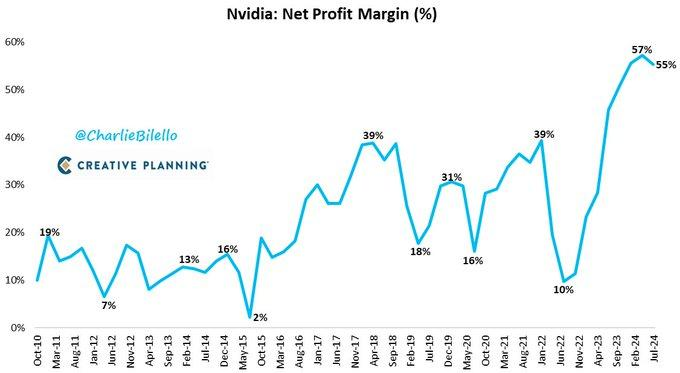

By the way, I believe that unless Nvidia's gross profit margin of 75.7% (non GAAP) is sustainable, which I don't believe it is, the stock should be valued as a percent of sales rather than earnings and on that count, it's at 25x sales for the year ended 1/31/25. Stretch it out to 1/31/26 and it's at 18x. So when I hear from some that it's cheap, I cover my ears.

With so many earnings releases to go thru, let's get to them and you'll still see a very mixed economic picture.

I'll leave Nvidia to others and get to other areas of tech and then retail.

From HP Inc who grew revenue y/o/y by 2%:

"Commercial PC recovery was strong, in line with our expectations and a signal of ongoing market stabilization. That said, the recovery of the print market was slower than expected, which impacted print revenue." They talked about AI driven PC's and they "are charging ahead." Consumer PC revenue though was down 1%.

And the breakdown of growth in the commercial PC business was "enterprise growing close to 5%, government between 6% and 7%, SMB 3% and education 1%." And why? "The installed base has been aging and the companies are seeing the need to refresh that."

From SalesForce who spoke a lot about AI:

"AI is not only my top of mind, but I can tell you because I've met with hundreds of customers this quarter that it is the top of mind for every customer, for every CEO, for every CIO. But I want to tell you before I get into this that I think that there's a lot of misconceptions about AI with my customers. I have been out there very disappointed with the huge amount of money that so many of these customers have wasted on AI. They are trying to DIY their AI. It's not so unlike when we first saw cloud emerge or even other technologies, where they feel like they have to roll their own, build it themselves, get in the weeds, try to figure out, and they're not going to do it better than we're going to do it."

"We saw strong new business growth in Japan, India, and Canada, while the US and parts of EMEA remained constrained. From an industry perspective, in Q2, public sector HLS (health and life sciences), and comms and media performed well, while travel, transportation, and hospitality, and manufacturing, automotive, and energy were more constrained."

Specifically with the US business, "I think the measured buying environment is really what's impacted the largest business we have" when addressing a question about the slowing rate of growth here. They mentioned small and medium sized businesses, which is what BOX said the other day.

On to retail and from Five Below whose comps fell 5.7%:

That decline was "driven by a decrease in comp transactions of 5.4% and comp ticket of .3%. Traffic to the stores was positive, with conversion the driver of the negative comp. The comp ticket decline was driven by lower unit per transaction nearly offset by an increase in the average unit retail price."

"Many of the categories that underpinned our comp performance in the 1st quarter continued as customers remained discerning with their discretionary spending. Our version of consumables in our candy and style worlds delivered positive results. But was more than offset by underperformance in other worlds, including the now world summer set and the sports world, including games and toys, as a result of the slowing Squishmellow trend." I'm not particularly familiar with that trend.

More on the consumer, "Around the customer behaviors, it was actually very similar to what we saw in Q1, where our lower income demographic was underperforming, and our higher income demographic was outperforming, which tells us two things along with the other information. One, we were getting some trade down there from the higher income demographic, and the lower income was probably more around value, which I just mentioned that we have to do better on."

From Foot Locker whose comps rose 2.6%:

"our comp trend strengthened as we moved through the quarter with July our strongest month, as we saw a solid start to the back-to-school season, especially in our stores, and with that strength continuing into August."

Their sneaker business is doing better than apparel as on the latter, "challenges persisted with comps down mid-teens" and they mentioned that the "promotional environment in apparel remains difficult."

Dollar General stock is getting hammered pre market as they missed expectations. "While we believe the softer sales trends are partially attributable to a core customer who feels financially constrained, we know the importance of controlling what we can control."

Their comp gain of .5% was "driven by an increase in customer traffic, partially offset by a decrease in average transaction amount. Same store sales in the 2nd quarter of 2024 included growth in the consumables category, partially offset by declines in each of the seasonal, home and apparel categories."

From Abercrombie & Fitch who has seen a remarkable business turnaround:

"Progression of sales throughout the quarter, a nice Q2, double digit growth in each month of the quarter...And again, talking about double digit growth as we get here into Q3."

"Promotional, nothing is jumping off the page to us. I think you're seeing the brands that are performing well being promotional, but promotional in their own way...We always talk about being a promotional business, and we continue to do that, and we like the promos we're delivering, the customers responding well."

From Chewy, where their consumable business has outperformed the more discretionary type products, which they call 'hard goods':

"With respect to hard goods, we would characterize hard goods as having kind of stabilized and being broadly flat on a q/o/q basis. I think the positive signals that we're seeing from hard goods is that we've reached a level of stability, which to us indicates with active customers growth sequentially Q1 to Q2 for the first time since Q1 of '23, with some of the pet household formation."

From Kohl's:

"During the 2nd quarter, we attracted more new customers to Kohl's and experienced an increase in overall transactions, both of which are positive developments. At the same time, however, our customers exhibited more discretion in their spending, which pressured overall sales and overshadowed strong performance in our key growth areas, including Sephora, home decor, gifting, and impulse."

"our outlook for the balance of the year assumes the macroeconomic environment will remain challenging."

From JM Smucker:

"in the convenience channel, we did see a bit of an acceleration in consumers shopping less or less frequently in the convenience stores. And although we did see some of that earlier, it did seem to accelerate a bit in the quarter...So, our performance in that channel is good, but as consumers have been a bit more cautious and have less discretionary income to spend, that is why we have seen a bit of an impact on both sweet baked snacks and pet snacks."

Affirm had a "killer quarter" as CEO Max Levchin described it as "on both growth and profitability side of the ledger":

To the perpetual question of their credit exposure he said, "So, in terms of credit, just a friendly reminder to everybody, these numbers are not an accident. We decide what we want to see. Obviously, there is variability, but we have a really short-term exposure. Our consumers don't borrow money from us for too long. Every transaction is underwritten separately. We are by design and definition in control of our credit outcomes. What you see today are the numbers that we wanted to have, and we're happy with them...Every time we plan our credit outcomes, we tell ourselves what it is that we want to see, the delinquencies, and that's what we typically end up with, plus or minus minor noise."

From the Best Buy earnings release this morning:

"We see a consumer who is seeking value and sales events, and one who is also willing to spend on high price point products when they need to our when there is new compelling technology."

"As we look to the back half of the year, we expect our industry to continue to show increasing stabilization." They expect Q3 comps down by about 1%.

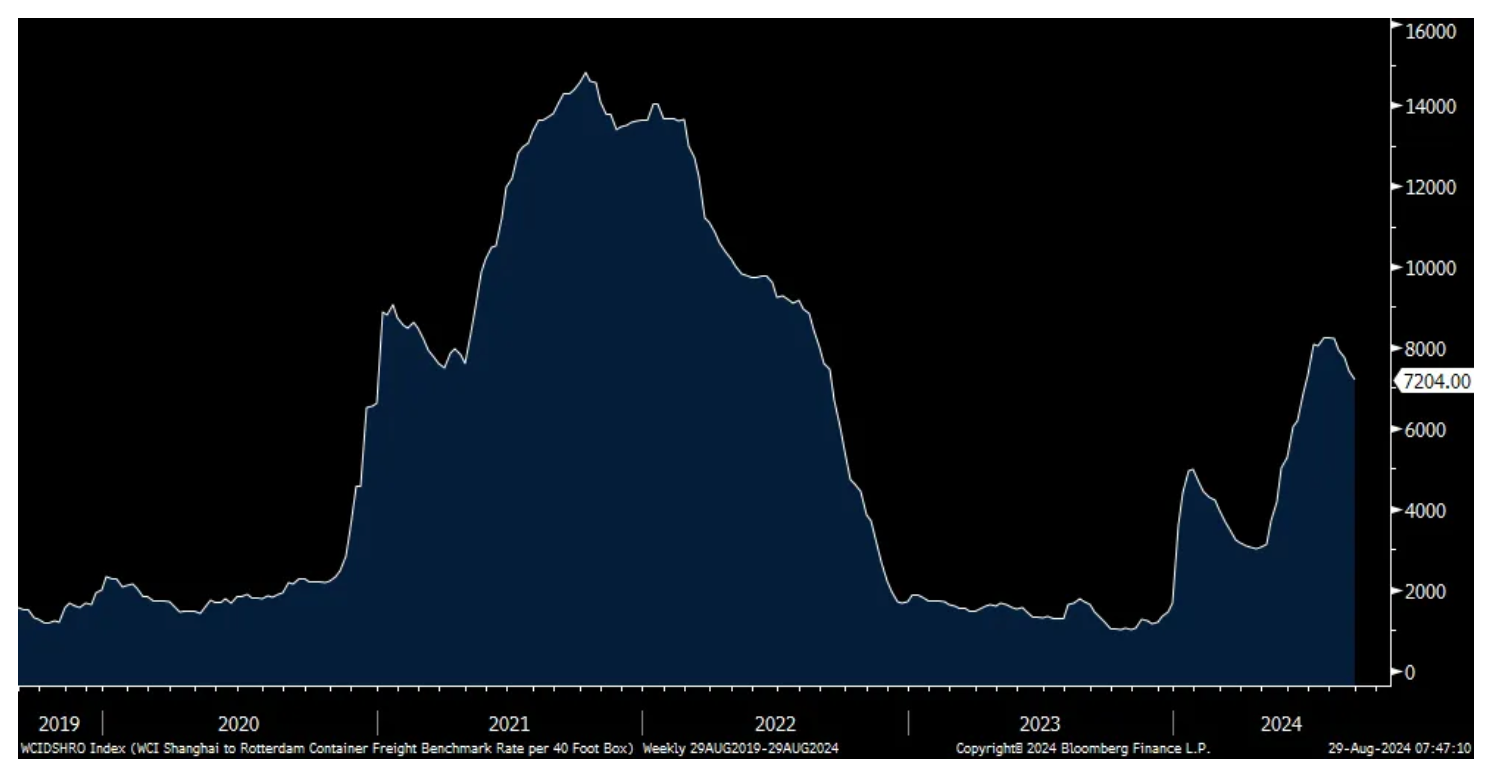

Burlington Stores, a purveyor of value stuff, saw a better than expected comp of 5%. They did however mention "some incremental cost pressure from ocean freight."

With regards to ocean freight prices, they continue to cool off the late spring spike. The Shanghai to Rotterdam route fell $225 to $7,204 which is the lowest since mid June, though still well above where they started the year. The Shanghai to LA trip cost $153 less w/o/w to also the lowest since mid June at $6,248, though still triple the level at the beginning of the year.

Shanghai to Rotterdam

Quickly overseas, Spain's CPI was about as expected with a headline gain of 2.4% vs 2.9% in the month before. The core rate was higher by 2.7% vs 2.8% in July. Yields in Europe are down about 1-2 bps with the euro lower after the recent gains. Stocks there are higher.

I have written more than 30 Tales of Nvidia columns in my Diary describing what I believe to be bonafide concerns.

These concerns include, but are not restricted to, supply outpacing demand during the AI buildout, the pace of adoption, that the real return on AI investment may be disappointing (as there might be a mismatch between capital spend and revenues being generated), potential production problems and the ultimate size of the total addressable market.

Notably, NVDA's profit margins have peaked and will shrink going forward:

I have concluded — in that series — that AI and Nvidia's NVDA role and prospects in the AI industry might be more than discounted in the share price of industry participants.

Up until recently investors have ignored most of my concerns — as well as a number of thin reed indicators like the CEO's large stock sales, the fact that Jensen Huang had become a rock star of major proportions (he now signs t shirts) and even the existence of a NVDA EPS Watch Party:

And then there is the excitement of Nvidia's modest (relative to capitalization) $50 billion buyback (announced last night):

A Tale of Two Cities

Warren Buffett buys back Berkshire BRK.ABRK.B shares when it is at 1.2x or less book value. (Berkshire Hathaway's issuance of options is virtually at zero.)

Jensen Huang buys back Nvidia's shares when it trades at 64x book value. (And when he buys it, at least in the latest round of $50 billion, it barely offsets the issuance of options.)

Finally, here is an objective summary and solid analog of Nvidia to Cisco CSCO during the dot-com boom/bust by the lynx-eyed Dan Niles (we will no doubt hear the opposite view from the other Dan in the business media today!):

I see volatility and underperformance ahead as the share prices of Nvidia and others digest their large gains — reflecting, in large measure, the growing likelihood of increasingly small sales and profit beats (especially relative to the consensus).

Nvidia earnings selloff should be bought. says UBS UBS analyst Timothy Arcuri recommends using the post-earnings selloff in shares of Nvidia as a buying opportunity. The firm keeps a Buy rating on the shares with a $150 price target. Nvidia's purchase commitments and supply obligations - the most important metric UBS watches, and historically a harbinger of future growth - grew significantly for the first time in several quarters, the analyst tells investors in a research note. The firm says that while the Q3 revenue guidance of $32.5B was "maybe a touch below investor expectations" and the Q4 implied gross margin outlook is down a few 100 basis points, this is "not only missing the forest for the trees, but also wholly consistent with what NVDA was suggesting last call as Blackwell will have lower margins out of the gate given its complexity."

Nvidia price target raised to $150 from $144 at Morgan Stanley Morgan Stanley raised the firm's price target on Nvidia to $150 from $144 and keeps an Overweight rating on the shares. July quarter revenue was $2B above guidance, "again," while October guidance for $2.5B of revenue growth was higher than prior quarters' pattern of $2B, the analyst tells investors. The stock "reacting negatively to a good quarter can feed cautious sentiment," but Blackwell is around the corner and should be a positive through all of next year, adds the analyst, who maintains Nvidia as the "Top Pick in semis."

Nvidia price target raised to $155 from $130 at Bernstein Bernstein raised the firm's price target on Nvidia to $155 from $130 and keeps an Outperform rating on the shares. The firm says Nvidia's Q2 was very solid with record Datacenter revenues at about $26.3B amid continued strong demand for its Hopper products. Q3 guidance was also very good with quarter-over-quarter growth largely driven by continued Datacenter strength, Bernstein adds. Management also indicated that the Blackwell production ramp is still expected in Q4, though acknowledging a change to the Blackwell GPU mask to improve yields, with Blackwell expected to deliver "several billion dollars" in Q4. Overall, the company continues to deliver amid high expectations, and it seems clear that datacenter sequential growth is still well in the cards into year-end, the firm argues.

Nvidia price target raised to $165 from $150 at BofA BofA raised the firm's price target on Nvidia to $165 from $150 and keeps a Buy rating on the shares. Following a "solid" Q2 report, the firm is raising its FY25 and FY26 pro-forma EPS estimates by 9% apiece to $2.81 and $3.90, respectively. However, the stock is "likely to be volatile" as the Q3 sales outlook of $32.5B is "only modestly" ahead of the $31.9B consensus and below some more bullish $33B-$35B expectations, which is likely due to the Blackwell ramp being pushed out by a quarter.

Nvidia price target raised to $165 from $155 at Wells Fargo Wells Fargo raised the firm's price target on Nvidia to $165 from $155 and keeps an Overweight rating on the shares following quarterly results. The firm finds it hard to see the negatives in Nvidia's Q2 print, Q3 guide, and/or forward-looking Blackwell cycle comments. Wells recommends buying the pullback in the shares.

Nvidia price target raised to $155 from $115 at JPMorgan JPMorgan analyst Harlan Sur raised the firm's price target on Nvidia to $155 from $115 and keeps an Overweight rating on the shares. The company reported July quarter results above consensus estimates and slightly lower than market expectations and guided to an 8% quarter-over-quarter increase in the October quarter revenue, above consensus but a bit lower than market expectations, on continued strong spending from its customers, the analyst tells investors in a research note. The firm says Nvidia maintains a "1- 2 step lead ahead of competitors with its silicon/hardware/software platforms."

Nvidia selloff 'simply another buying opportunity,' says Cantor Fitzgerald Cantor Fitzgerald says that despite the after-hours share selloff, Nvidia reported a solid earnings report amid Blackwell delay concerns. Hopper shipments were guided to increase in the the second half of 2024, which, when added to expectations for "several billion dollars" in Blackwell revenues in Q4, implies revenues tracking to $35B-plus, thus the worry about Blackwell delays and revenue impact "appears to be a nothing burger ahead of one of the biggest and baddest product cycles in NVDA's history," the analyst tells investors in a research note. The firm does not see any change to the artificial intelligence story underpinning Nvidia, and thinks the stock's pullback is "simply another buying opportunity." Cantor reiterates Nvidia as a top pick with an Overweight rating and $175 price target. At around $117 per share, the stock is "still too cheap to ignore," Cantor writes.

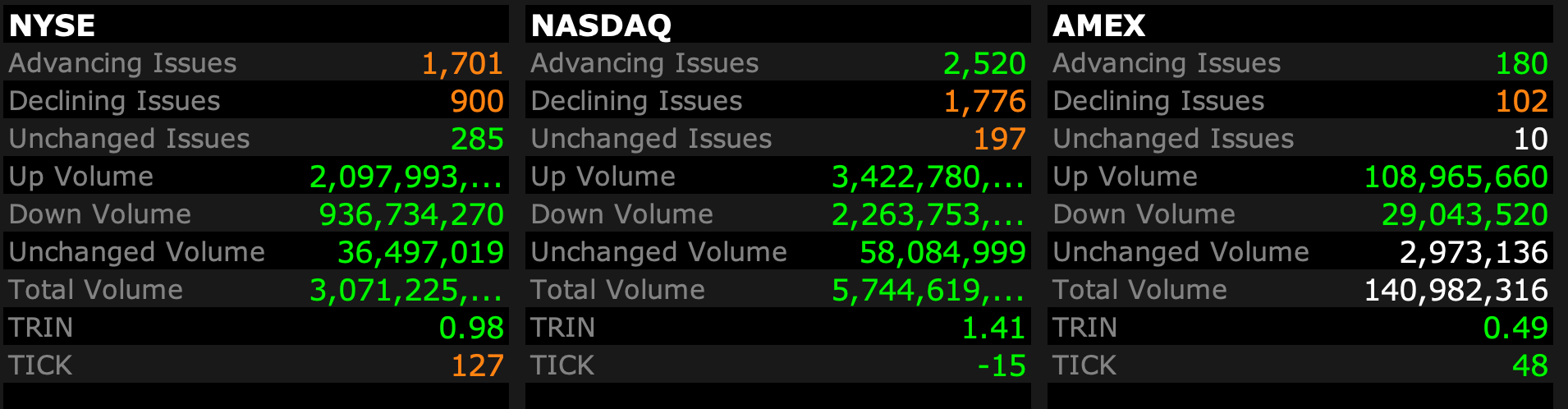

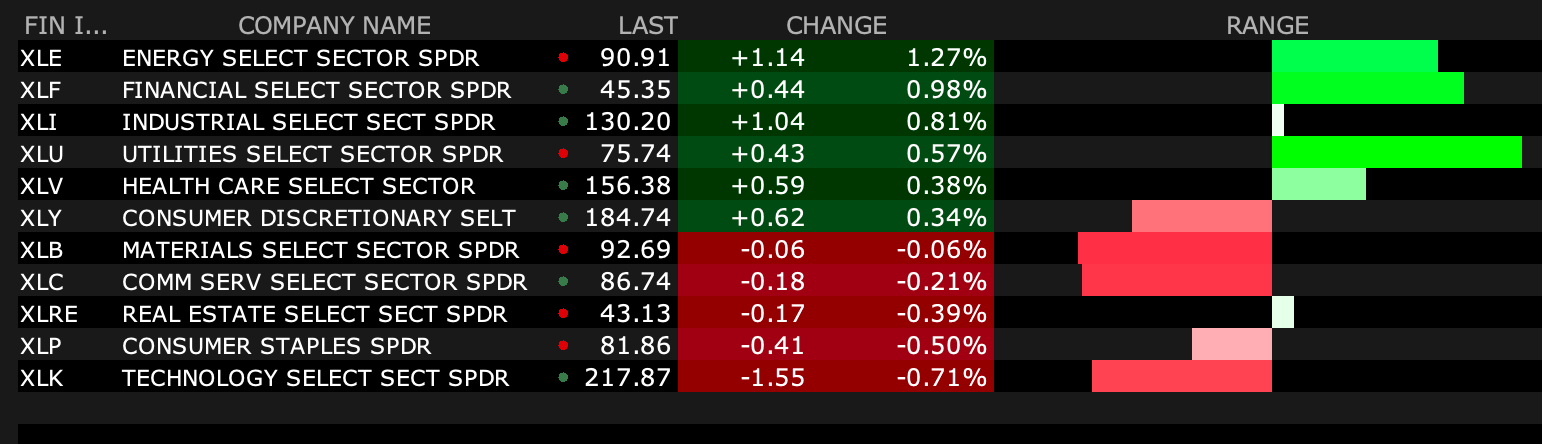

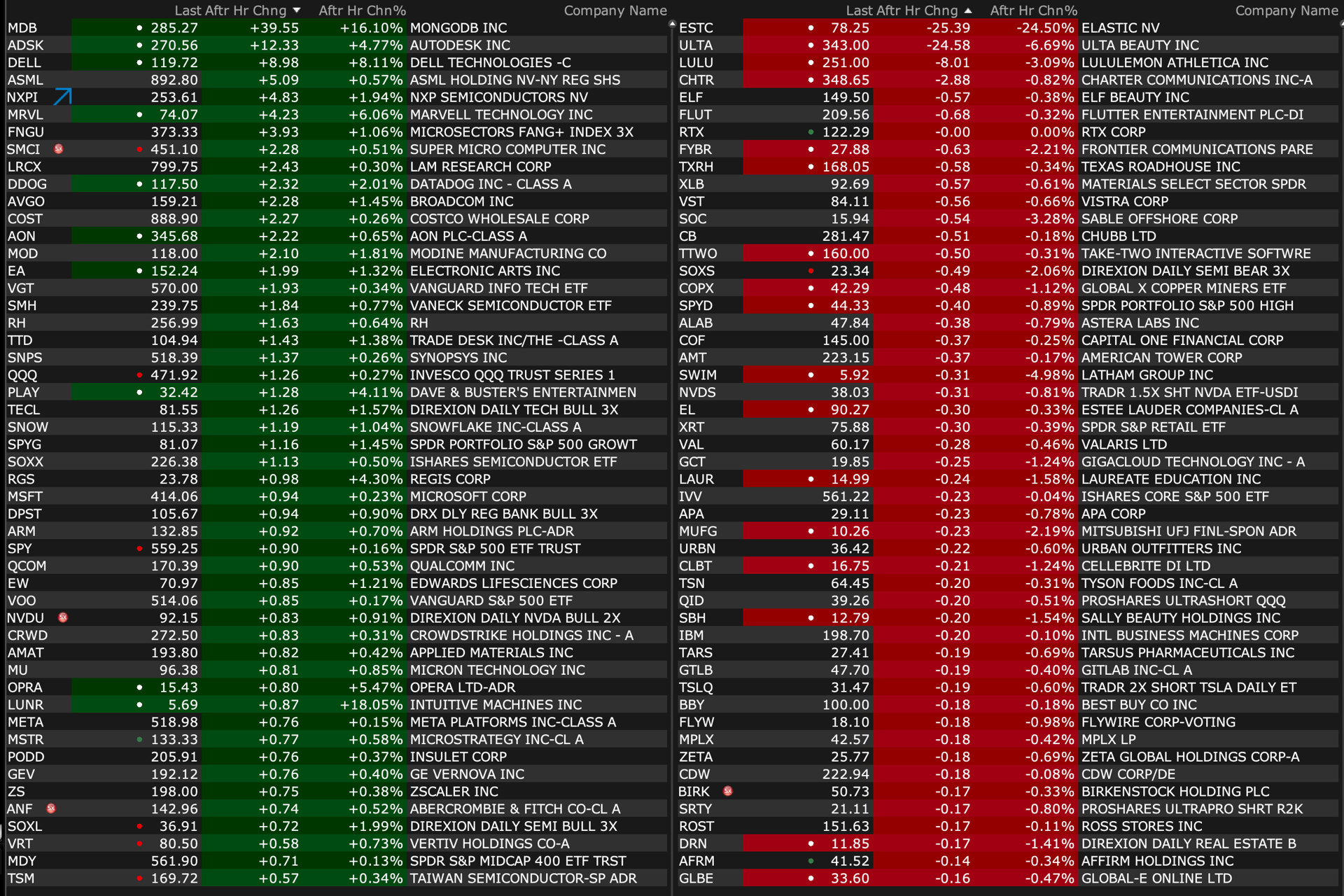

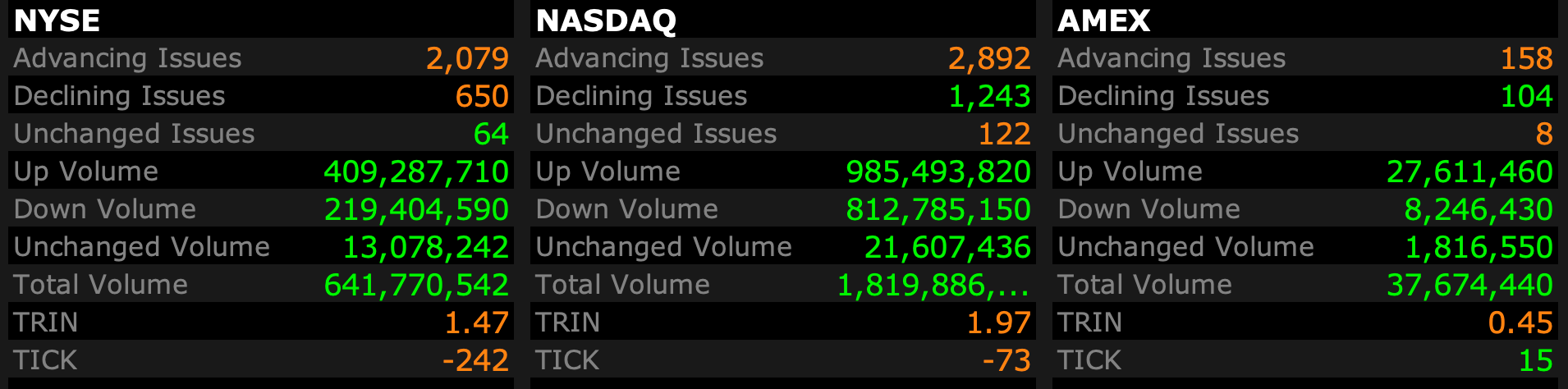

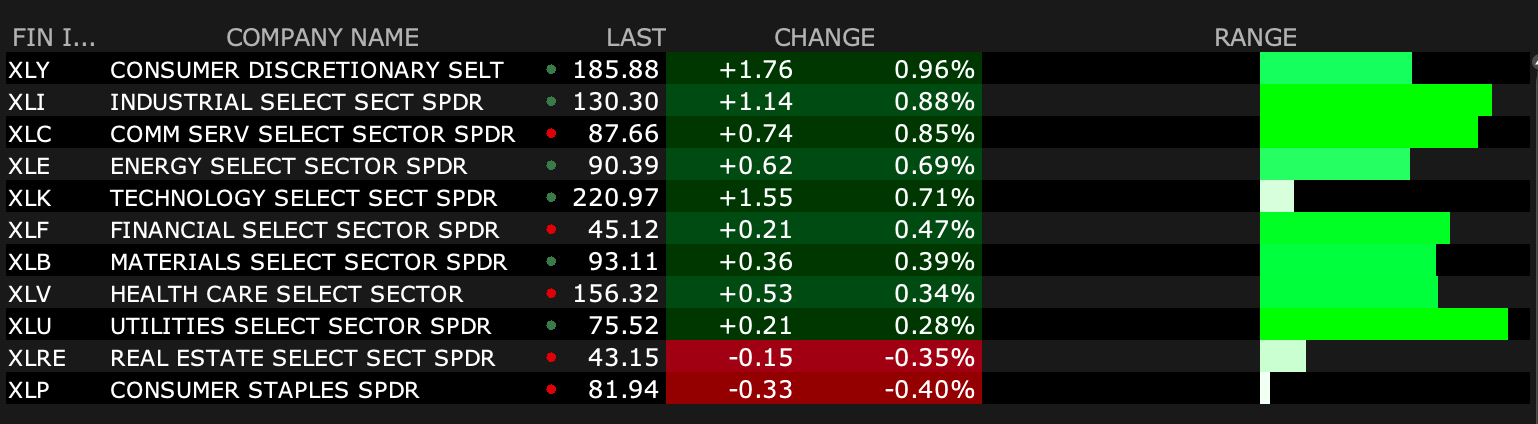

US: Futs are higher led by small-caps. NVDA Day was at first a disappoint with the stock losing 8% post-market as investors sold an extremely strong print and while all questions were not answered the story remains intact and on track to beat analyst expectations. The stock has trimmed its losses and is now -2.7% pre-mkt with the balance of Mag7 higher and SMH is -60bps. Bond yields are 1-4bps lower as USD sees a bid for the second consecutive day. Cmdtys are mixed with Energy weaker, Ags stronger, and Metals mixed (precious up, base down). Macro data today will be an update on 24Q2 metrics, Inventories, Jobless/Continuing Claims, and Pending Homes Sales. Tmrw’s data is more important with the monthly PCE, and Personal Income/Spending.

and...

EQUITY AND MACRO NARRATIVE: Now that we are past NVDA Day, the market now shifts back to macro with PCE and Personal Income / Spending data on Friday and then ISM and NFP next week. The balance of this note is a post-mortem on NVDA. I hope that everyone has an enjoyable holiday weekend and US Market Intel publications will return next week.

My friends at Miller Tabak talk about an emerging inflationary threat:

Wednesday, August 28, 2024

As Rates Fall, Expect Another Housing Price Surge

Our outlook (which we detail later) remains for 100 bps of rate cuts this year, with another 125 bps next year to take the Federal Funds rate to 300-325 bps by the end of 2025. We also continue to put the chances of a U.S. recession starting within the next year at 20%. We have been asked what would cause us to raise these odds? In addition to a significant deterioration of the labor market, a failure of housing to respond to lower rates would also be a major cause for concern.

June’s Case-Shiller housing price index showed y/y growth falling from 6.8% to 6.3% and many forecasts are for even slower housing price growth in the near-term. These figures, however, do not yet reflect falling rates and we instead expect that, as the Fed cuts interest rates, real housing prices could rise by another 7-10% over the next year.

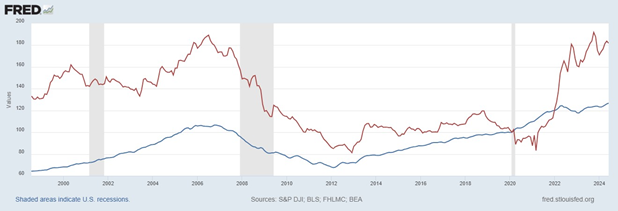

Figure 1 shows two measures of housing affordability. The first (red) is the share of the average households’ disposable income needed to make the monthly payment on a newly purchased home, using a 30-year mortgage. The second (blue) is simply the Case-Shiller national index, adjusted for CPI-inflation, ex-shelter. The former measure, which we prefer, remains 81% (as of June) above its pre-pandemic level, essentially at its 2006 peak. This motivates many forecasts for lower housing price growth.

Figure 1: Monthly Payments (red) and Inflation-Adjusted Prices (blue) Feb 2020=100

We continue to expect yields to fall rapidly as the Fed starts easing, with the 10-year Treasury yield around 350 bps by year’s end. Likewise, we expect 30-year mortgage rates to fall to around 5.5% by mid-2025. By itself, this will reduce monthly payments on new sales by about 15%. Lower rates will not resolve the regulatory issues that have constrained construction in recent years. As a result, housing shortages will persist and much of the impact of lower rates will be passed back into even higher housing prices, leaving only a modest impact on affordability.