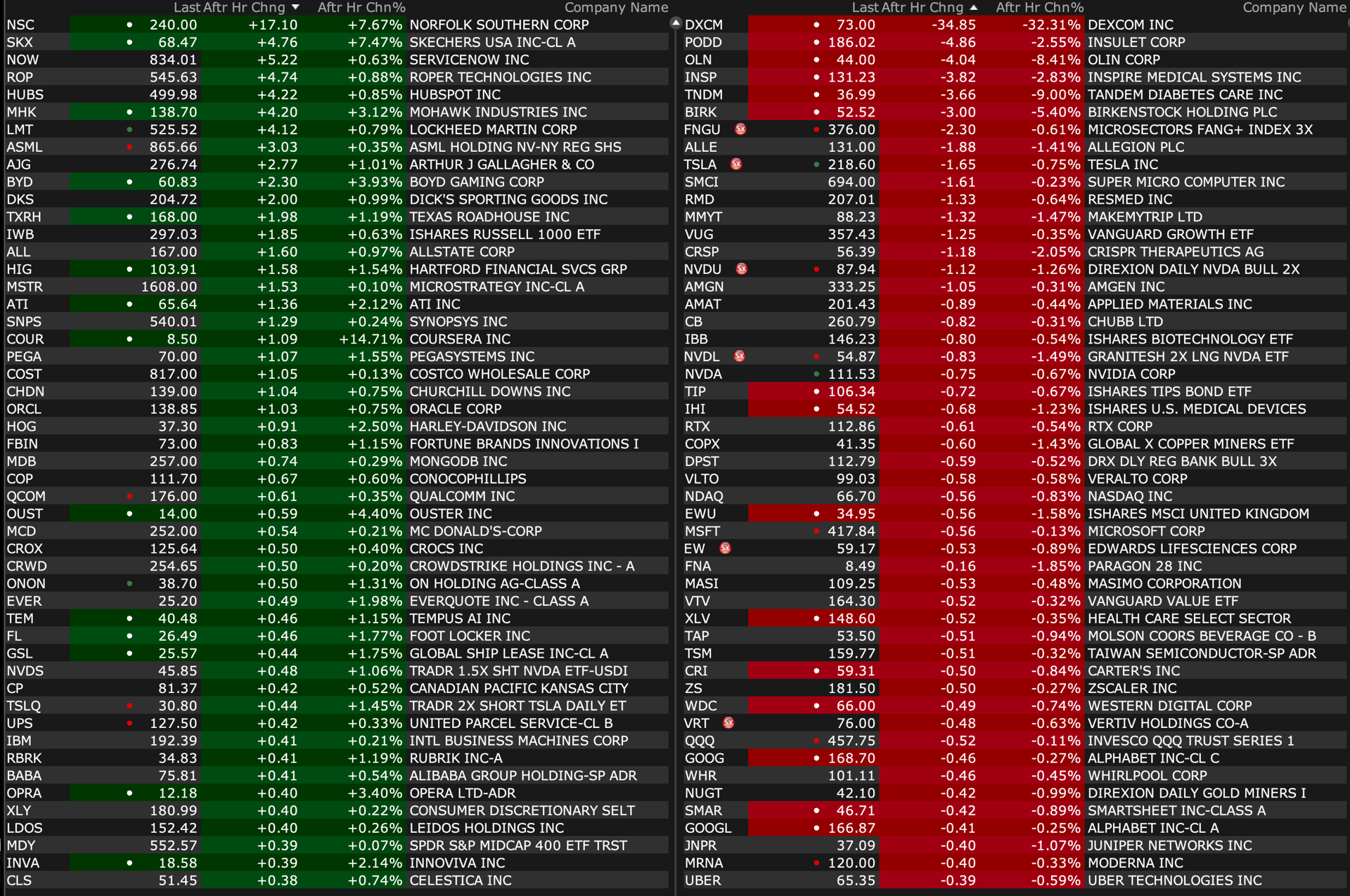

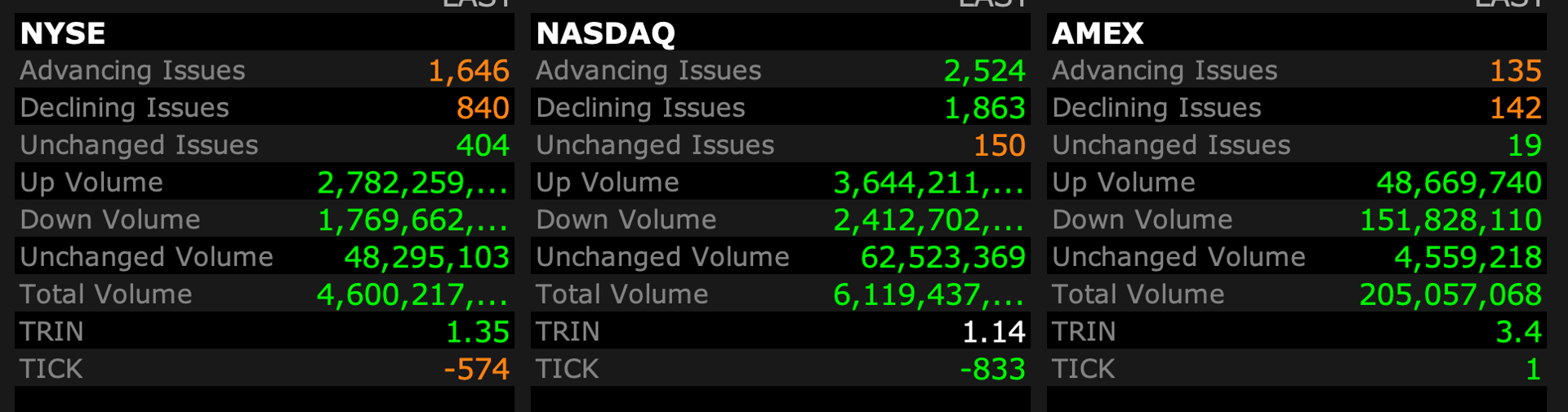

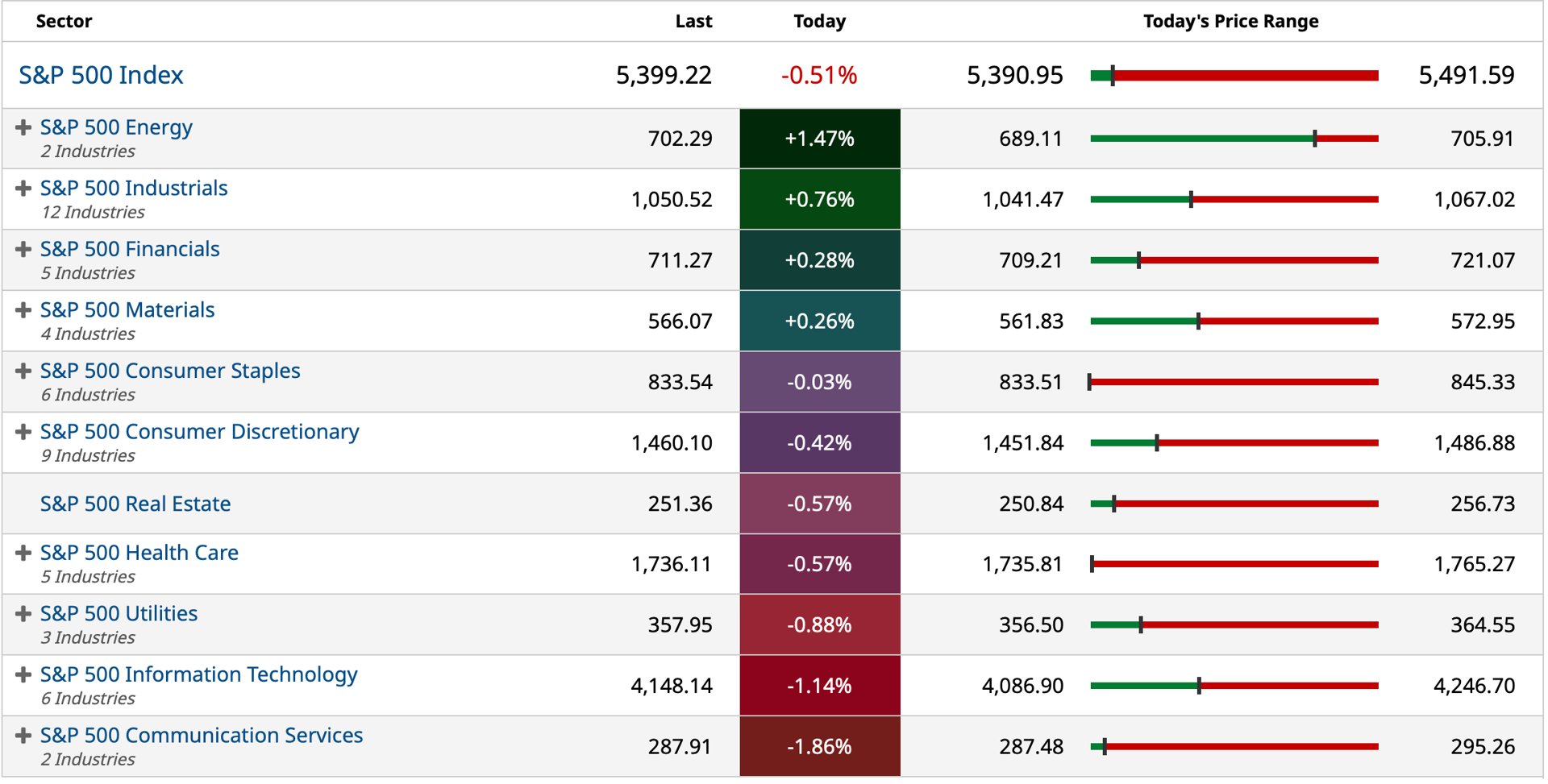

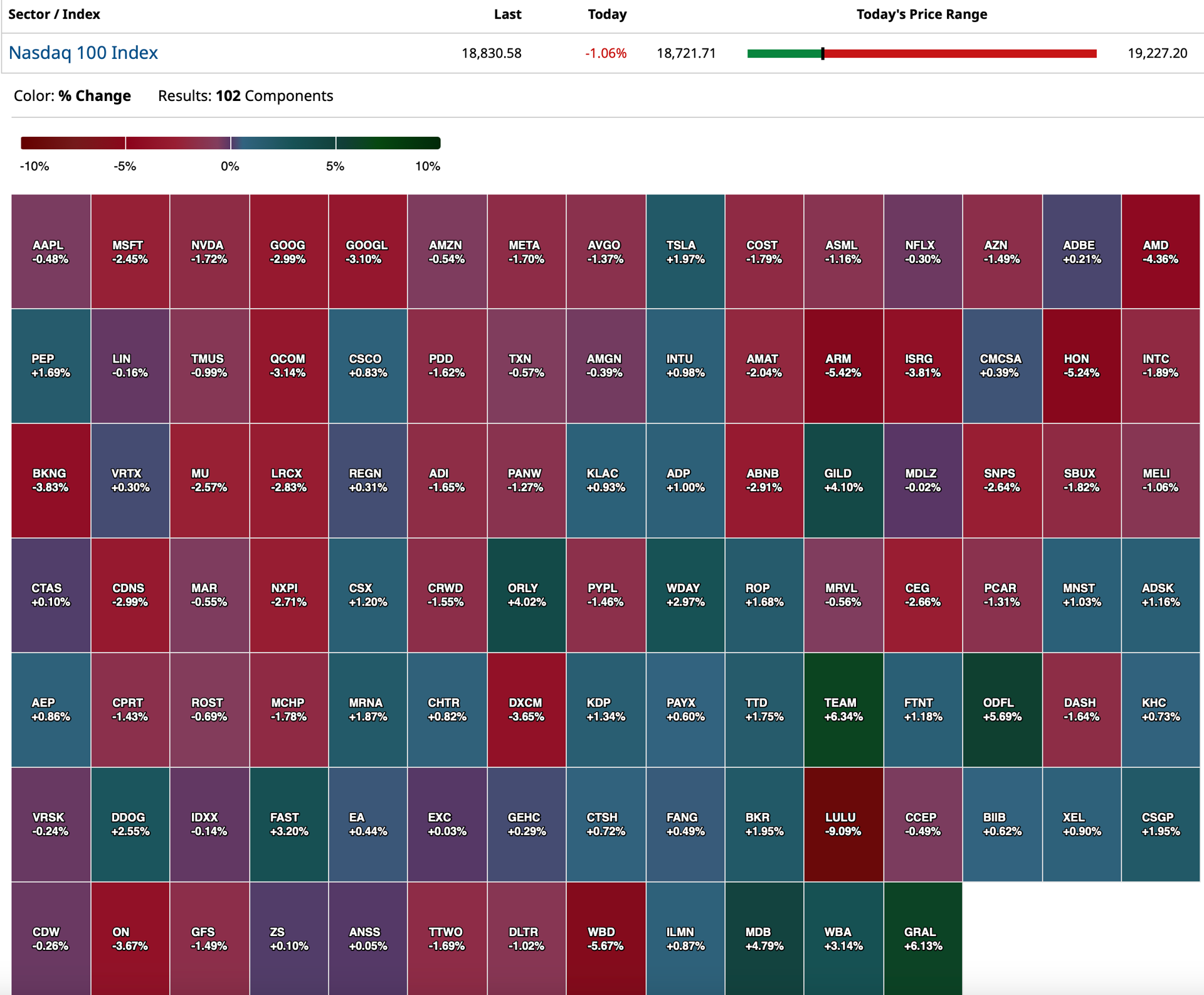

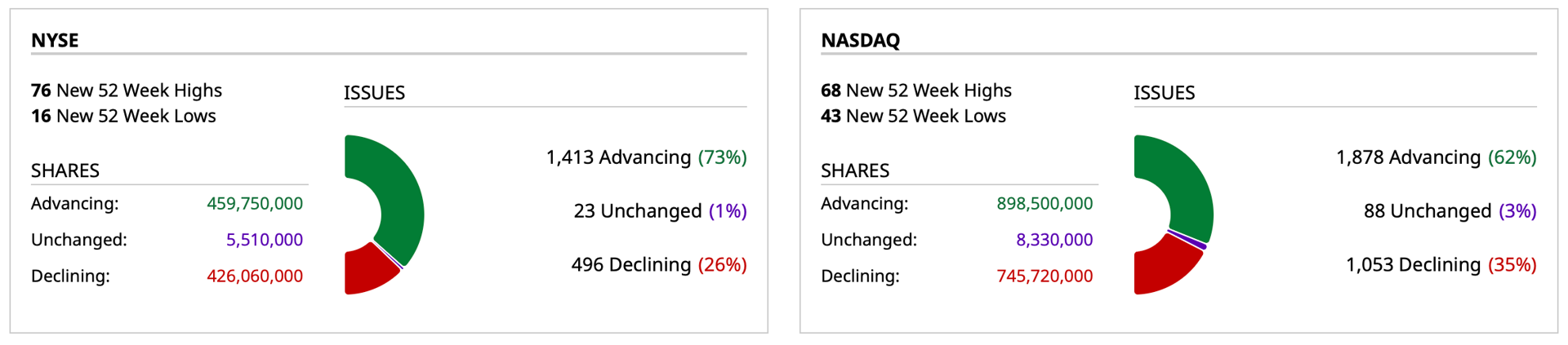

After-Hours Movers

As of 4:22 p.m.:

BY Doug Kass · Jul 25, 2024, 4:46 PM EDT

As of 4:22 p.m.:

BY Doug Kass · Jul 25, 2024, 4:46 PM EDT

BY Doug Kass · Jul 25, 2024, 4:35 PM EDT

I am calling it a day.

See you in the morning.

BY Doug Kass · Jul 25, 2024, 2:20 PM EDT

As of 11:40 a.m.:

- NYSE volume is 31% above its one-month average

- NASDAQ volume is 26% above its one-month average

BY Doug Kass · Jul 25, 2024, 12:04 PM EDT

I am still sick with flu - going back to the Dr. at noon.

Probably light posts this afternoon.

BY Doug Kass · Jul 25, 2024, 11:45 AM EDT

* The movie is now in reverse...

I have long warned about the market structure risk.

Too many (that worship at the altar of price) and are on the same side of the boat (long). They know nothing about value but everything about price.

An inflection point in momentum is the root cause of yesterday's and today's market declines.

Too few remember October 1987 ... when portfolio insurance contributed to a waterfall decline in equities.

Kill the machines before they kill our market.

BY Doug Kass · Jul 25, 2024, 11:35 AM EDT

S&P futures have risen by +20 handles, sunk by -40 handles and have moved back positive in less than two hours.

If anyone in the business media expresses a confident view of the relatively short term market outlook — tune them out, keep them away from your portfolios and your children.

Given market structure and the ramifications for intraday and daily volatility — they make fortune tellers look good.

BY Doug Kass · Jul 25, 2024, 11:17 AM EDT

What a jerk Sam Altman is.

See articles below:

Vox.com/future-perfect/361749/universal-basic-income-sam-altman-open-ai-study

Businessinsider.com/openai-sam-altman-universal-basic-income-idea-compute-gpt-7-2024-5?op=1

Apparently Sam Altman thinks AI is going to put a lot of people out of work.

I don’t, because I don’t think it will function well enough to broadly put a lot of people out of work.

But Altman does.

His solution is universal basic income (UBI) to solve the problem. For all intents and purposes, he wants to enrich himself with AI, and then have everyone else that still has a job, and income, to pay for it.

Apparently, according to Elon Musk, Open AI was originally set up as a non-profit, too, and Altman reversed all that, ostensibly to enrich himself.

I would love to understand how the math works, too. Nobody has a job, but the government will have enough money to pay UBI? The border is wide open too, the white collar jobs will be gone, they will sit at home and collect UBI and go out to dinner and use that money to pay the busser, who will also be on supplemental UBI and sill won’t be able to afford a place to live? And there will be no inflation, either, from all the money printed to do this, since the tax base was decimated? My head is going to explode – can 100,000 h100’s solve for this problem because I can’t.

Why did I waste my whole life working when I didn’t need to?!

These Silicon Valley guys all contradict themselves with virtue signaling and all of their related activist itinerary. Many send their kids to school where no cell phones are allowed and some don’t let their own kids on social media. They lecture us about the environment, while they fly private jets and own yachts. They operate data centers that consume more power than a small country. It would be nice if they would all shut up.

My opinion.

BY Doug Kass · Jul 25, 2024, 10:59 AM EDT

I added to Disney DIS $89.78,

BY Doug Kass · Jul 25, 2024, 10:42 AM EDT

I bought back VKTX last night.

Press release. Viking Therapeutics Reports Second Quarter 2024 Financial Results and Provides Corporate Update (prnewswire.com)

Big positives:

* Skip to Phase Three (moves up production by a year and dramatically raises odds of a takeout)

* 100 mg dosing

* Possible monthly dose

BY Doug Kass · Jul 25, 2024, 10:33 AM EDT

From Boockvar:

Yesterday didn't come out of nowhere. 1)A few weeks ago we had the S&P 500 that was nearing 15% above its 200 day moving average, highly stretched and mentioned here. 2)The bullishness has been excessive as seen in the Citi Panic/Euphoria index, Investors Intelligence and AAII. 3)All year there has been a fragile underpinning due to the extreme narrowness of the rally. 4)We have growing global growth concerns and 5)now we finally have investors asking tough questions about whether all this AI spend will be worth the investment in terms of returns. 6)Lastly, we can throw in the yen rally where carry trades are getting unwound.

Updating the Investors Intelligence survey by the way, as of Friday and thus not capturing yesterday, saw the Bull/Bear spread nearing 50 with Bulls at 64.2 and Bears falling to just 14.9. I've said before that anything above 40 is extreme.

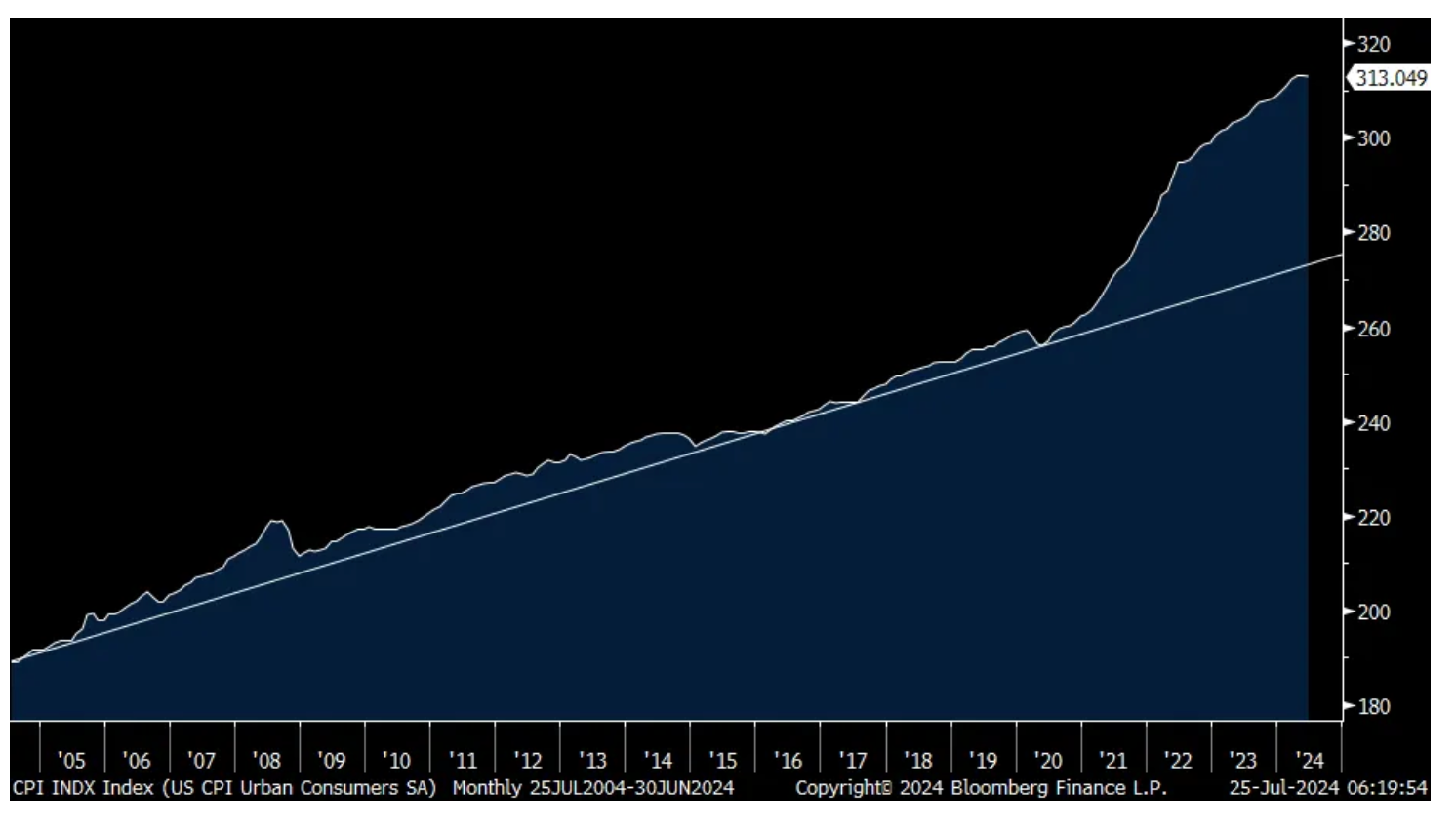

Considering inflation as transitory was an epic fail by the Federal Reserve as we know and now that inflation has moderated, especially on the goods side, it is not a sign of victory for the average person. To visualize the reason why so many consumers feel so stretched I've charted the CPI index over the past 20 years and drew a trend line. The picture tells the story.

CPI Index

From Robert Half, the staffing firm, and trading down pre market:

“Client and candidate caution continues to impact hiring activity and new project starts as macroeconomic and interest rate uncertainty persist.” Their revenues fell 10% y/o/y in the 2nd quarter and things didn't get better in July as revenues for the first two weeks were down 14% y/o/y.

"Client budgets remain constrained and candidates are selectively changing jobs. This subdues short term demand and elongates sales cycles."

From O’Reilly Automotive, the auto parts retailer:

“Our comparable store sales results were below our expectations for the 2nd quarter, as the soft demand environment we experienced at the beginning of the quarter persisted through May. Sales trends improved in June, in line with our expectations, aided by strong performance in summer weather related categories in many of our markets.”

From Ford, whose rising warranty costs was the problem this quarter but investor focus is also on EVs:

On the EV situation, "We see excess capacity that will lead to more pricing pressures, which is in our business plan, more consolidation and many, many more partnerships...And we see a lot more openness to hybrids and extended range electric vehicles we call E-REVs."

"In general, we see supply and demand for vehicles in balance...Our outlook for the year assumes a flat to slightly higher SAAR in both US and Europe...Lower industry pricing of roughly 2%, driven by higher incentive spending as we move through the 2nd half of this year."

From Chipotle, who continues to crush it, helped by a healthy portion of food, notwithstanding some allegations, that some buyers are turning into two meals (from a survey I've seen):

Comps grew 11% y/o/y helped by the Easter shift into April but they settled in at 6% in June and are trending there in July.

As for the portion accusations, "We have leaned in and reemphasized generous portions across all of our restaurants as it is a core brand equity of Chipotle."

They expect 6% wage inflation "And as a reminder, about half of the wage inflation is due to the nearly 20% step-up in wages in California as a result of the increase in minimum wage."

On their other costs, they've seen a jump in avocado prices and outside of this and a protein mix shift, "we anticipate underlying cost of sales inflation will be in the low single digits range for the remainder of the year."

From Lamb Weston, the potato producer:

“Our financial results for the 4th quarter and for the year are disappointing, reflecting executional challenges both commercially and in our supply chain, as well as soft global demand for fries.”

Being blamed in part to “softer than expected restaurant traffic trends in both the US and many of our key international markets.”

“According to restaurant industry data providers, US restaurant traffic softened over the past year, as consumers continued to adjust to the cumulative effect of menu price inflation. During our fiscal 4th quarter, overall US restaurant traffic, as well as QSR traffic, was down about 3% vs the prior year. Traffic at QSR chains specializing in hamburgers, a highly important channel for fry consumption, was down more than 4%.” In addition, traffic trends in QSR hamburger weakened sequentially each month of the quarter, with May down nearly 6%.”

They are hoping that the new promotions from McDonald’s and others drives more traffic.

Group 1 Automotive, focused mostly on the new car retail dealer business:

The CDK outage had an obviously disruptive impact on their business in late June.

“I can’t, looking at our data for Group 1, say that we saw or are seeing any changes in the consumer – any material changes in the consumer.”

Capital One has a glass half full view on the US consumer:

“the US consumer remains a source of strength in the overall economy. Of course, the labor market remains strikingly resilient. Rising incomes have kept consumer debt servicing burdens relatively low by historical standards despite high interest rates. When we look at our customers, we see that on average, they have higher bank balances than before the pandemic and this is true across income levels.”

“on the other hand, inflation shrank real incomes for almost two years and we’ve only recently seen real wage growth turn positive again. And you know in this high interest rate environment, the cost of new borrowing has gone up in every major asset class, mortgages, auto loans, and credit cards. So we’ll obviously keep an eye on that. And I think at the margin, these effects are almost certainly stretching some consumers financially. But on the whole, I think I’d say consumers are in reasonably good shape relative to most historical benchmarks.”

We heard from NXP Semi and Texas Instruments tell us both this week about their softer auto chip business. Today ST Microelectronics said in their earnings release, "During the quarter, contrary to our prior expectations, customer orders for industrial did not improve and automotive demand declined."

From Kering, the maker of Gucci, and joining LVMH, Richemont, Burberry, Hugo Boss and Swatch in seeing slower business:

"In Western Europe, local demand was rather subdued, while tourism spending was more or less supportive, with some contrasts across brands and nationalities."

"North America remained in negative territory, but polarization based on brand positioning persisted, and Bottega Veneta in the higher end segment continued to outperform."

"Japan was up 22% comparable, with Q2 accelerating up 27%. The market is fueled by strong tourism spending, notably from China and other Asian countries. Most of our houses implemented tactical price increases to account for the weak yen, but the price gap remains attractive." Chinese spend in Japan was taken away from the mainland, along with Hong Kong and Macau.

"considering the current uncertainty regarding consumer confidence and demand for luxury in particular, we have issued new guidance...Kering's recurring operating income could be down approximately 30% in the 2nd half of the year compared to the same period last year."

IBM is a tech bright spot today:

"We had strong performance in software and infrastructure above our model as investment in innovation is yielding organic growth, while consulting remained below model. Our results underscore the continued success of our hybrid cloud and AI strategy and the strength of our diversified business."

This was their take on the macro:

"Technology spending remains robust as it continues to serve as a key competitive advantage, allowing businesses to scale, drive efficiencies and fuel growth. As we stated last quarter, factors such as interest rates and inflation impacted timing of decision making and discretionary spend in consulting."

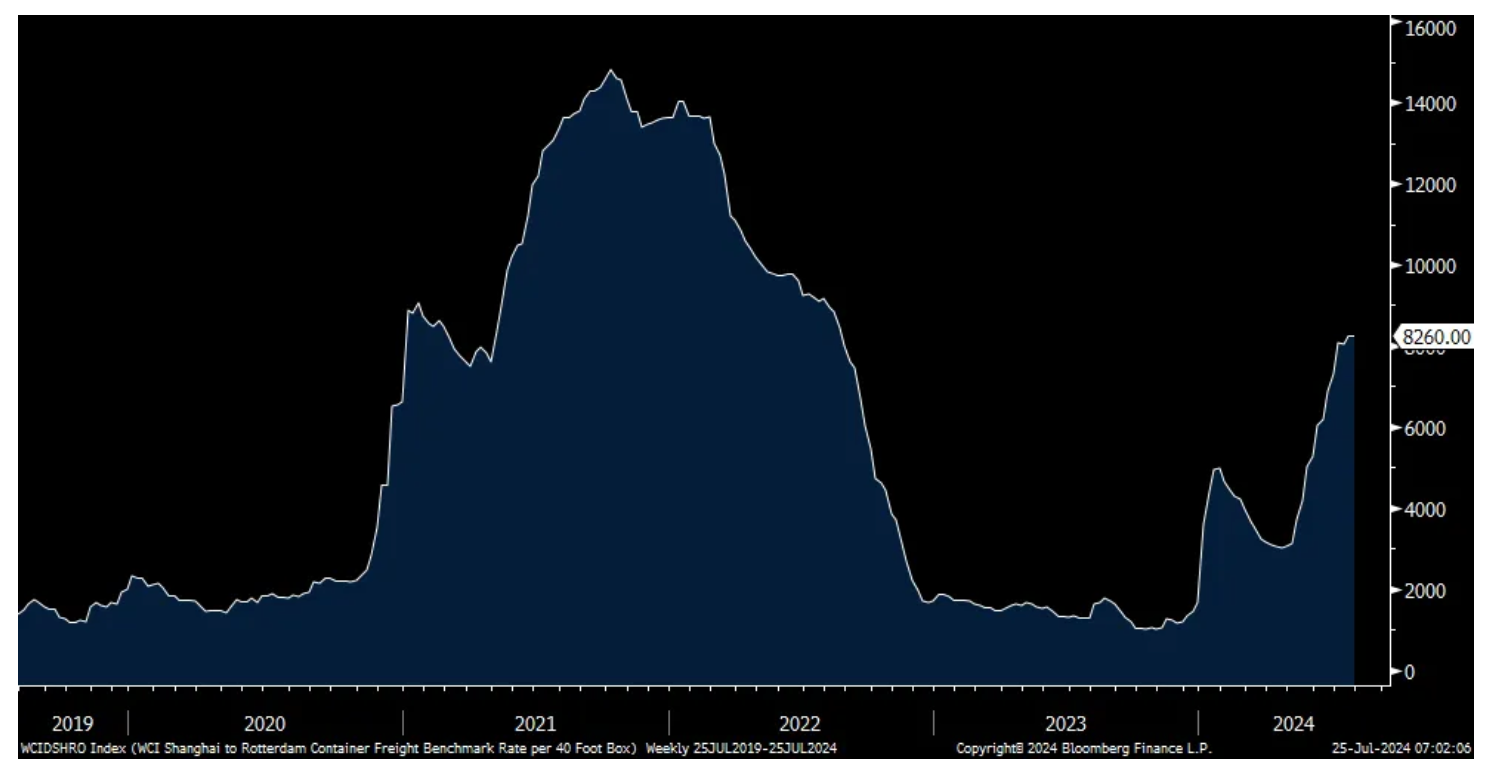

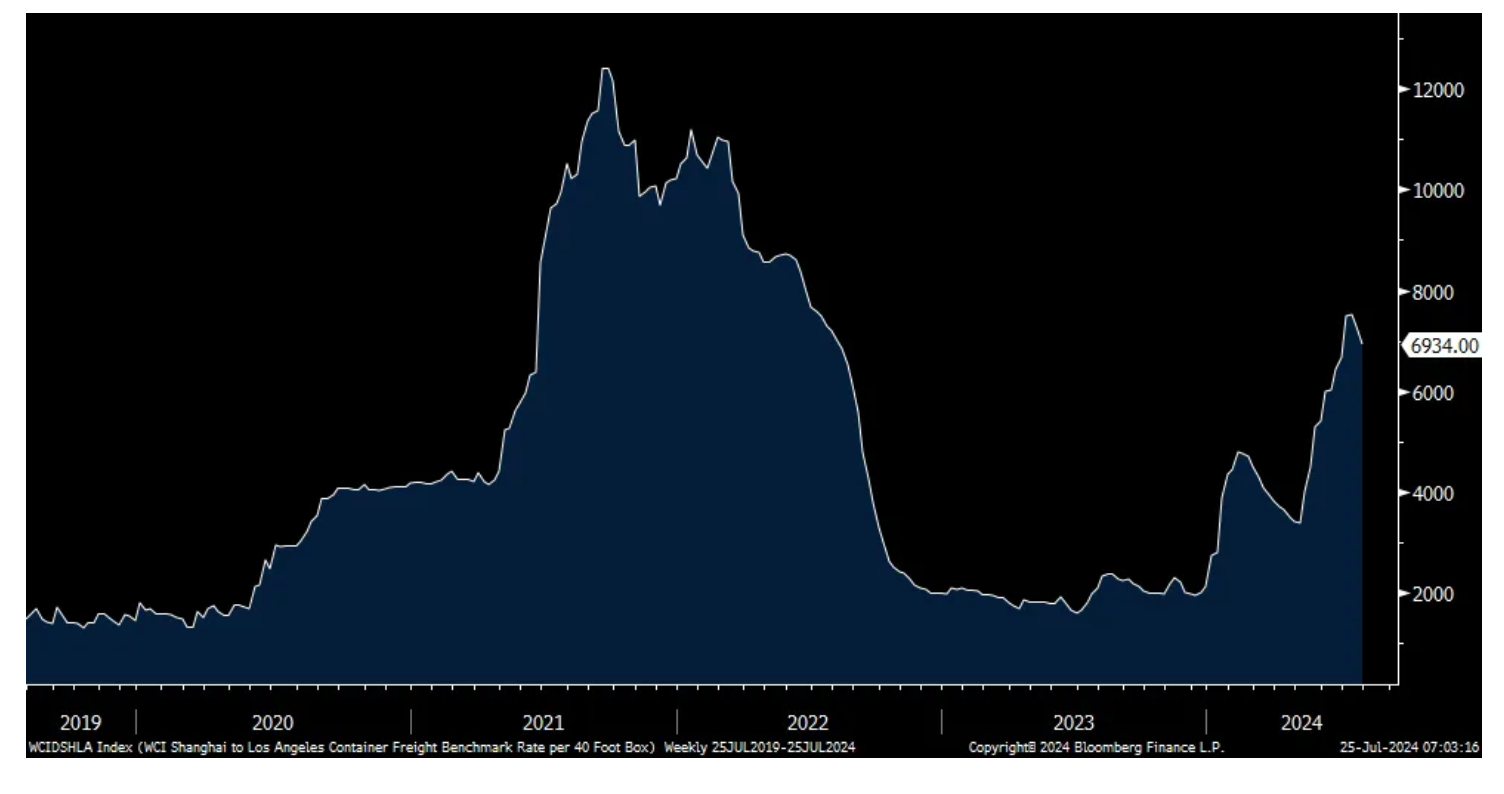

Container shipping prices were mixed w/o/w. The Shanghai to Rotterdam trip was down a slight $7 at $8,260 and as a reminder it started the year at just under $1,700. The route to LA fell $354 w/o/w to $6,934 vs $2,100 at the beginning of the year. We are beginning to hear some mention these rising costs, especially in yesterday's PMIs.

WCI Shanghai to Rotterdam

WCI Shanghai to LA

Yesterday, the June US Architecture Billings Index came out and it rose to 46.4 from 42.4 as hopes grow for interest rate cuts. The AIA chief economist said, "Architecture firms continue to face a period of headwinds in the construction sector, driven by elevated interest rates, high construction costs, and generally weak property values. This is the 17th consecutive month of a billings decrease and yet, despite the softness firms remain generally optimistic that conditions will start to improve once interest rates begin to ease." I'll add, the Fed to the rescue again is the belief.

South Korea said its economy unexpectedly contracted in Q2 from Q1 by .2% vs the estimate of slight growth of .1%. Lower private spending and investment were the main factors. South Korean stocks remain cheap but always seem to be.

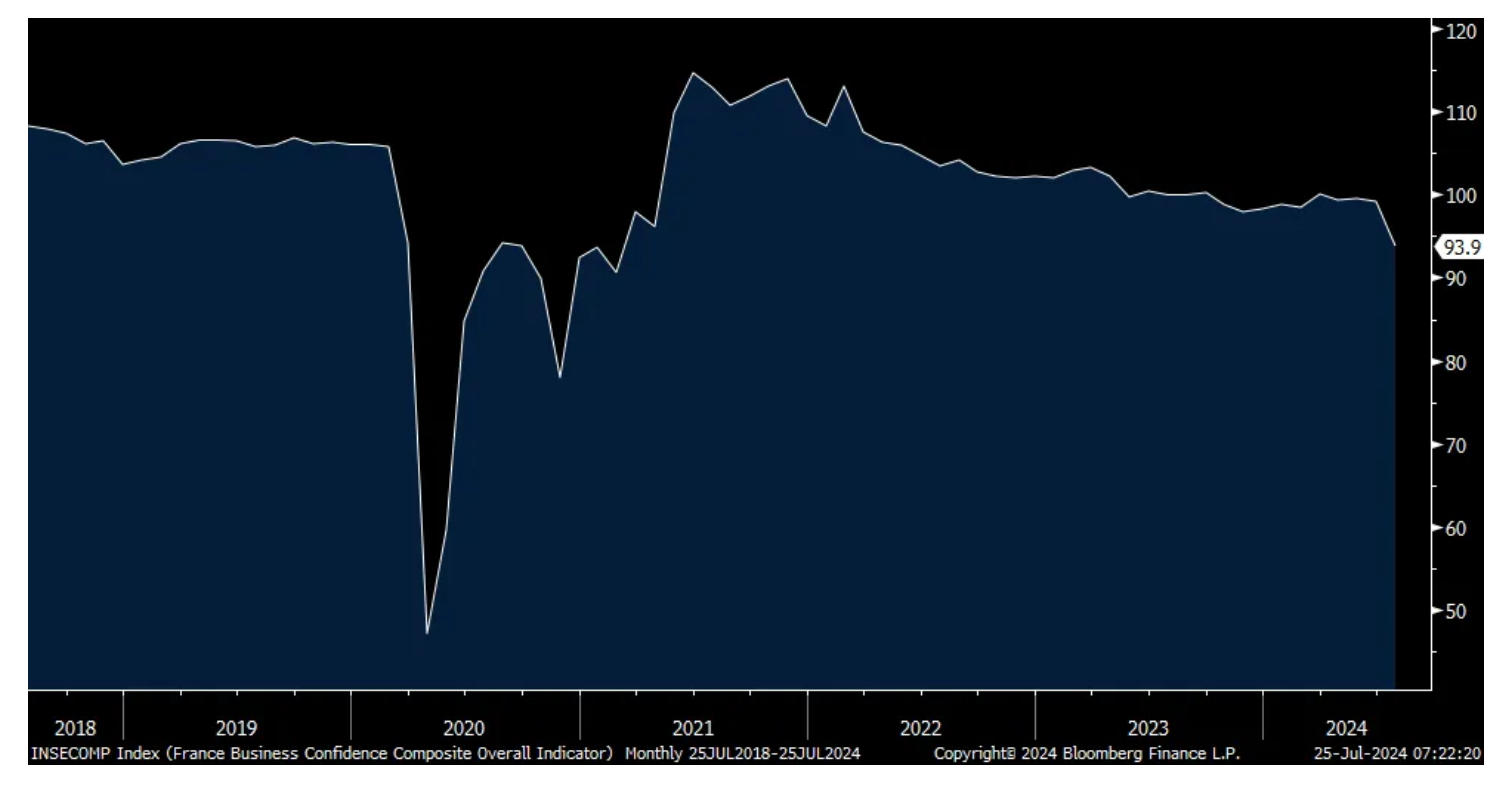

In Europe, there was a notable drop in French business confidence in July, likely influenced by the political mess. The index fell to 94 from 99 and the estimate was for no change. That's the weakest since February 2021.

The German business confidence index, the IFO, fell to 87 from 88.6 and the forecast was for a gain to 89. Both the Current Assessment and Expectation components fell m/o/m. The IFO said simply, "Skepticism regarding the coming months has increased considerably. The German economy is stuck in crisis." Bund yields are falling in response as is the DAX while the euro is little changed.

Lastly, the July UK CBI industrial orders index weakened to -32 from -18 and vs the estimate of -20. There is optimism though that things will improve from here as the expectations piece of the survey rose to "the strongest in over two years. Firms are looking to increase stock levels to meet expected demand." That is what the global manufacturing sector needs, some inventory restock at some point. UK stocks are cheap too and we find some attractive.

German IFO

French Business Confidence

BY Doug Kass · Jul 25, 2024, 10:18 AM EDT

From Bookvar:

GDP beats estimates/Claims data

Q2 GDP growth was 2.8%, above the estimate of 2%. Three tenths of this upside was due to a lower than expected price deflator of 2.3% vs the estimate of 2.6%. Core PCE though of 2.9% was two tenths higher than expected.

On the personal spending side, the biggest chunk, it rose 2.3% vs the estimate of 2%. This follows a 1.5% gain in Q1 and averaging the two together has first half consumption growth at 1.9%. Real final sales grew by 2% vs 1.8% in Q1. Spending on goods rebounded after the Q1 drop while spending on services grew by 2.2% vs 3.3% in Q1.

Gross private investment was the 2nd biggest contributor to GDP, adding almost 150 bps with equipment spending and IP helping out the most. I’m sure AI and AI data center spend are helping to lift these figures. Residential investment was flat.

Inventory growth helped to goose GDP too, adding 82 bps after subtracting about 90 bps over the prior two quarters. Government spending added 53 bps to GDP with most of the contribution coming from defense and state/local spending.

On the drag side, net exports subtracted 72 bps as imports jumped 6.9%, offsetting the increase of 2% with exports.

Bottom line, on the first look of Q2 before multiple revisions, smoothing out the first half of 2024 has average GDP growth of 2.1% with 1.9% growth coming from consumption as stated. It’s better than the 1.5% type of economy that I’ve guessed at based on everything I look at but not by much.

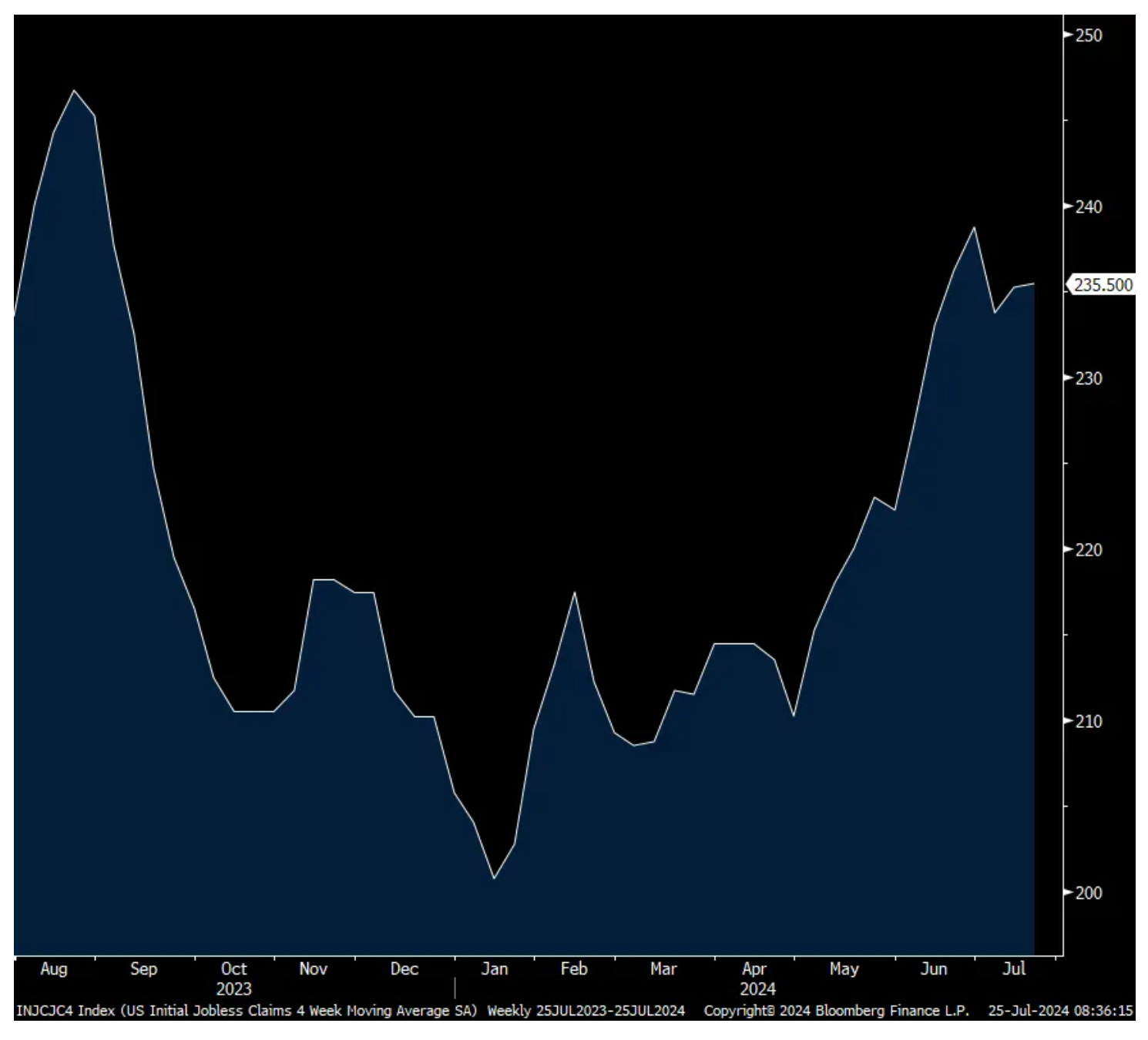

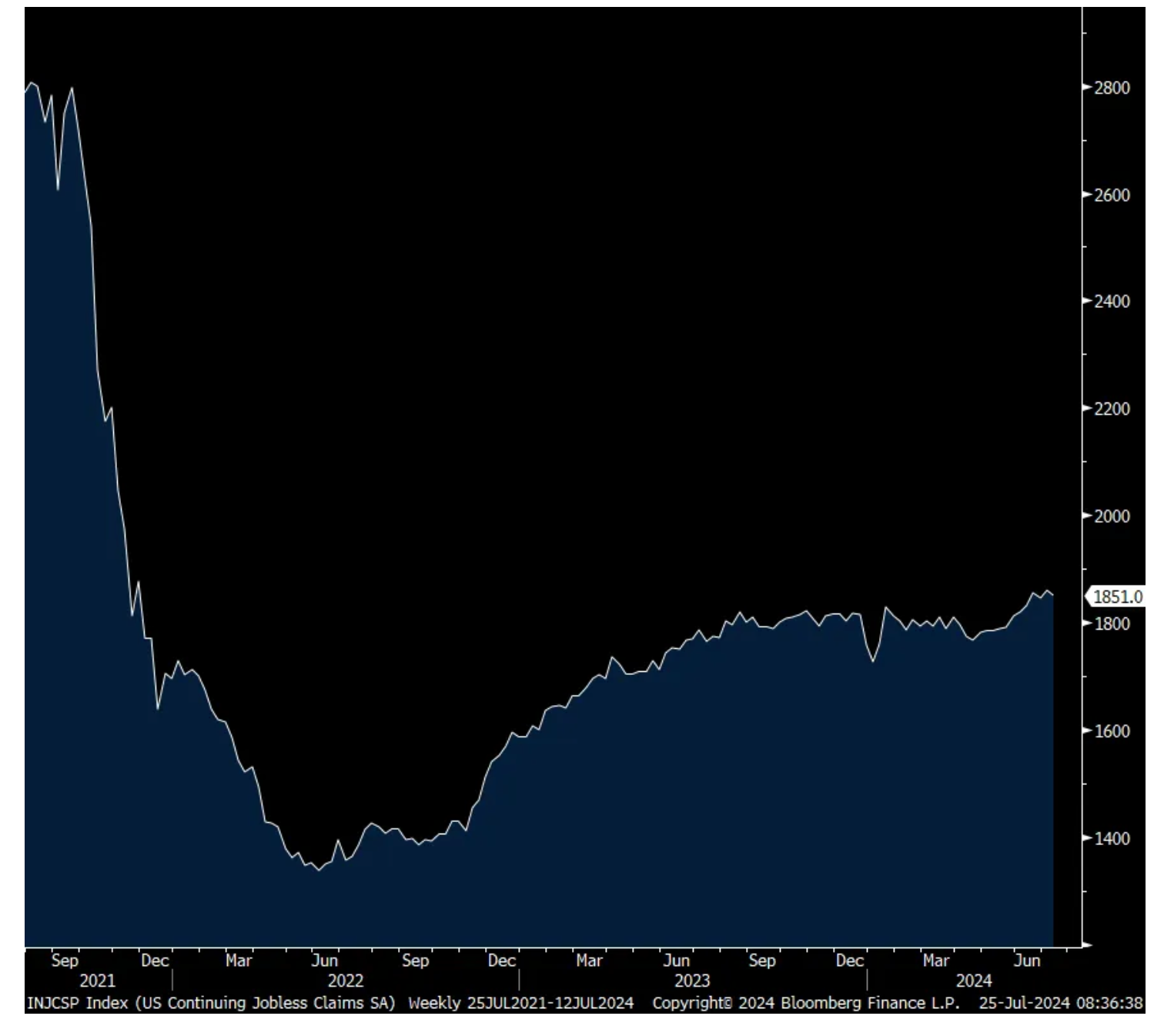

Initial jobless claims totaled 235k, remaining elevated relative to recent trends but 3k less than expected and down from 245k last week which included people filling after the July 4th holiday. Smoothing all this out puts the 4 week average at 236k vs 235k last week, hovering around the highest since last September. Continuing claims slipped by 9k to 1.851mm, but after rising by 13k in the week before.

Bottom line, while happening slowly, the rate of firing’s has picked up at the same time employers have moderated their demand for labor and subsequent hiring’s. We heard both this week anecdotally from Polaris on the former and Google on the latter and from others too.

Treasuries are not responding to the upside because it’s old news and yields are at the lows of the morning after rising yesterday on the long end, notwithstanding the stock market selloff.

4 Week Avg Initial Claims

Continuing claims

BY Doug Kass · Jul 25, 2024, 9:45 AM EDT

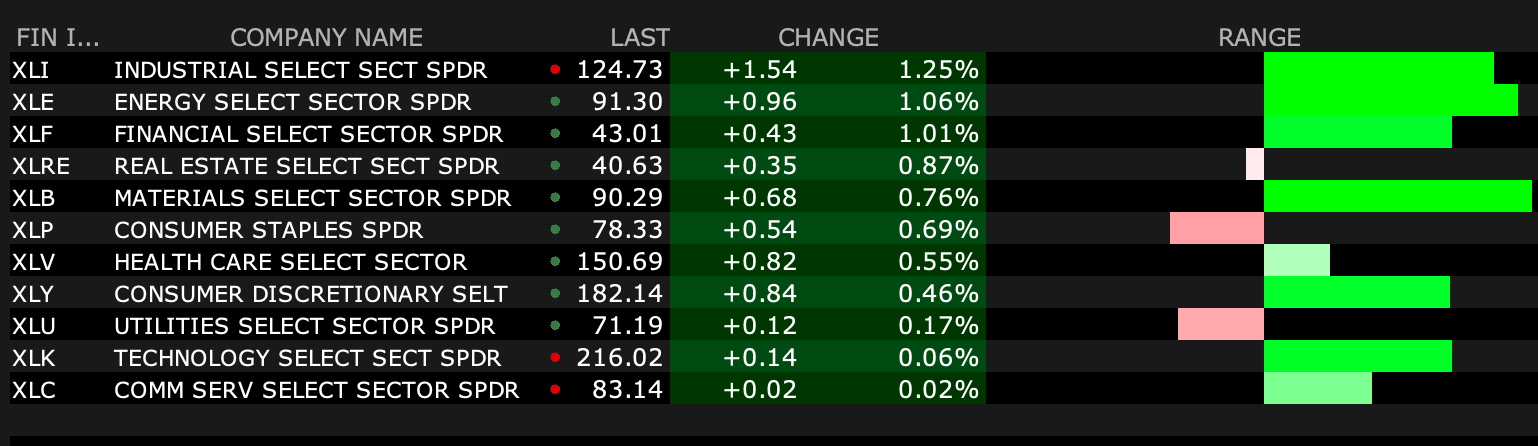

Most active premarket exchange-traded funds as of 8:35 a.m.:

BY Doug Kass · Jul 25, 2024, 9:20 AM EDT

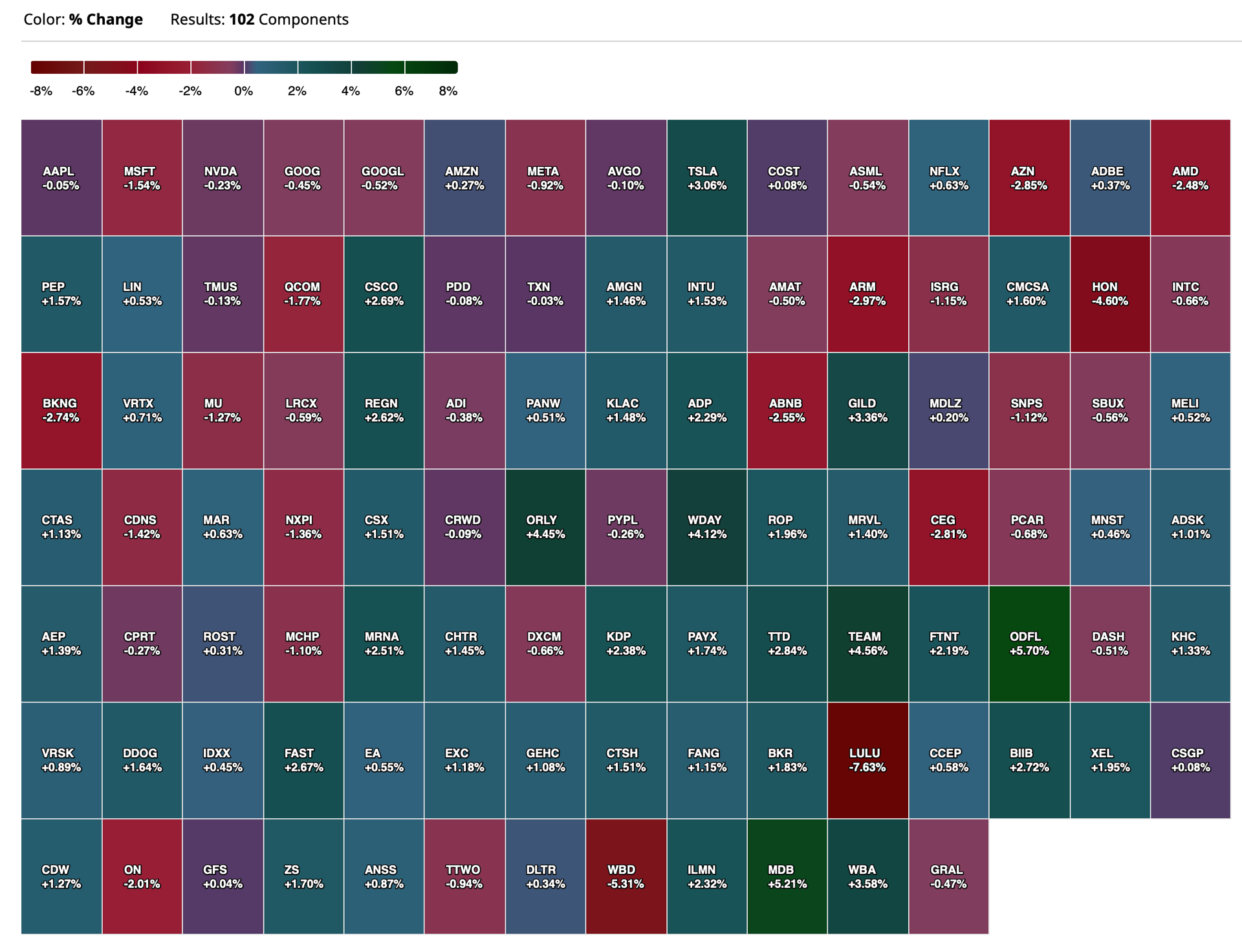

As of 8:52 a.m.:

BY Doug Kass · Jul 25, 2024, 9:13 AM EDT

Here are the U.S. Select Premarket Movers as of 8:28 a.m. ET:

-BALY +26% (enters merger agreement with affiliates of Standard General LP at $18.25/shr at Bally's EV of ~$4.6B)

-VKTX +15% (earnings)

-MOH +11% (earnings, guidance)

-HAS +9.7% (earnings, guidance)

-WINT +8.5% (expects Phase 2 SEISMiC Extension Study in SCAI Stage B early cardiogenic shock patients to complete enrollment in next several weeks and report topline data by the end of this quarter)

-NOW +6.7% (earnings, guidance)

-CLS +6.0% (earnings, guidance)

-NTCT +5.5% (earnings, guidance)

-IMAX +5.1% (earnings)

-CKPT +4.6% (FDA accepts BLA Resubmission of Cosibelimab for the Treatment of Advanced Cutaneous Squamous Cell Carcinoma)

-MAS +4.1% (earnings, guidance)

-CRS +3.3% (earnings, guidance; authorizes $400M share buyback)

-IBM +3.3% (earnings, guidance)

-RTX +3.3% (earnings, guidance)

-WHR +3.1% (earnings, guidance)

-SLGL +3.0% (signs Six Exclusive License Agreements to Commercialize TWYNEO and EPSOLAY in Europe and South Africa)

-CMG +2.2% (earnings, guidance)

-ALT +2.1% (announces Publication of Clinical Study of Pemvidutide in Metabolic Dysfunction-Associated Steatotic Liver Disease (MASLD) in Journal of Hepatology)

-CNC +2.1% (divests management services organization Collaborative Health Systems to Astrana Health)

-HP +2.0% (earnings, guidance; to acquire KCA Deutag for $1.97B in cash)

-EW -24% (earnings, guidance)

-F -13% (earnings, guidance)

-NYCB -8.6% (earnings, guidance)

-AAL -7.3% (earnings, guidance)

-LUV -5.9% (earnings, guidance)

-DOW -4.9% (earnings, guidance)

-HON -4.5% (earnings, guidance)

-LVS -3.5% (earnings)

-LULU -3.0% (pauses sales of Breezethrough Yoga wear)

-BC -2.7% (earnings, guidance)

-XRX -2.7% (earnings, guidance)

-KLAC -2.1% (earnings, guidance)

BY Doug Kass · Jul 25, 2024, 8:59 AM EDT

From David Rosenberg this morning:

And what about Lamb Weston and its huge miss on fiscal Q4 earnings — what does it say about the consumer when it cuts back on frozen potatoes, for crying out loud?

Post Script: Remember that Fin TV panelists have continued to preach a strong consumer (and consumer stocks like SBUX, MCD, HD,etc.) .... Res ipsa loquitor.

BY Doug Kass · Jul 25, 2024, 8:43 AM EDT

* Much lower prices on rising volume...

From my pal Keith McCullough at Hedgeye:

BY Doug Kass · Jul 25, 2024, 8:28 AM EDT

This table is a valuable resource for momentum-based short term traders:

BY Doug Kass · Jul 25, 2024, 8:15 AM EDT

From JPMorgan:

US: Futs are lower. Pre-mkt, MegaCap Tech are mixed: AAPL -43bp, NVDA -20bp, AMZN +23bp, GOOG/L +27bp. Ford (F) fell -13% post earnings miss and unchanged guidance. Bond yields are 5-8bp lower, led by the front end. Commodities are weaker: WTI fell -1.8%; base metals are mostly lower. USD is lower. Today, the macro data focus will be 2Q data release: Feroli looks for 2Q GDP to print 2.0% QoQ saar vs. 1.4% prior, in line with the Street. He expects nominal GDP to print 4.1% QoQ vs. 4.5% prior.

and..

EQUITY AND MACRO NARRATIVE: Yesterday, we saw a risk-off event in Tech as the rotation continued. Despite a relatively positive PMI print (PMI-Srvcs surprised to the upside at 56.0 vs. 54.9 survey vs. 55.3 prior), the main catalysts of yesterday’s selloff were (i) worse-than-expected Mag 7 earnings (GOOG/L and TSLA) and (ii) rising concerns on consumers (LM comments on restaurant weakness, Citi/Capital One credit card and LVMH earnings yesterday). The selloff was further fueled by positioning headwinds and weaker seasonality expectations in August and September.

While macro data are still pointing to resilient economic growth, in near-term, investors are focusing on earnings strength, especially how the remaining of MegaCap Tech earnings can justify AI growth. Ahead of MSFT’s earnings on Tuesday AMC, stocks may stay under pressure given the positioning headwinds. Friday’s PCE could provide some positive news to the market, but in near-term, earnings will still remain the key theme for equities.

· We shared the following immediately after the PMI release: “the weakness in manufacturing was presaged by the regional activity data and it appears the strength in retail sales boosted the services/composite portions. While bonds may be looking at this as a negative I think this is a positive as it assuages some of the concerns on the consumer given the deterioration in housing and does not to change the Fed view that cuts begin in Sept. Ultimately, no changes to the investment thesis.”

BY Doug Kass · Jul 25, 2024, 8:00 AM EDT

There is a message here (slowing domestic economic growth relative to consensus expectations):

BY Doug Kass · Jul 25, 2024, 7:35 AM EDT

“Many receive advice, only the wise profit from it.”

- Harper Lee

Bonus — Here are some great links:

The Stealth Bull Market of 2024

BY Doug Kass · Jul 25, 2024, 6:35 AM EDT

* Inflation will stay prickly (as 'slugflation' arrives)

* Same here with Ollie and Daisy (my doxies)...

From "Meet" Bret Jensen:

Bret Jensen

Tell me how inflation is running at 3% again dept.

Took my Golden Retriever Mateo to the vet this morning as he was due for his annual vaccinations, also had to get his six-month supply of heartworm medication, needed ear drops, and had a hotspot on his right leg. I have had three goldens over the past 20 years and they always tend to get a hotspot breakout once a year or so, almost always in early summer here in South Florida for some reason. Pre-Pandemic this visit would have cost $500 - $550, maybe $600 tops depending on the vet. Today's tab $1010.53. Are vet bills even included in the CPI? I know the government is reporting that health care premiums have dropped over the past three years. Call me a skeptic, I am not buying that either. AKA, inflation is much higher than official statistics, and the average consumer is under much more duress than believed imho

BY Doug Kass · Jul 25, 2024, 6:20 AM EDT

BY Doug Kass · Jul 25, 2024, 6:05 AM EDT

The S&P Short Range Oscillator has declined from a deep overbought of over 8% last week to 3.15% last night (from 6.35% the night before).

Given that this is a 30-day moving average, I expect the number to continue to drop this week.

BY Doug Kass · Jul 25, 2024, 5:53 AM EDT

* I have moved back to market neutral...

S&P futures have reversed about 52 handles from the night's high to the morning's low (S&P futures are now -23 handles at around 420 a.m. after being +29 handles).

At 420 a.m. I have moved back from net short to market neutral.

More when you all wake up!

BY Doug Kass · Jul 25, 2024, 5:46 AM EDT