14:05 (US) Fed's Goolsbee (non-voter for 2024): Inflation has been moving sideways and if it continues to do so it makes me wonder if we should cut rates at all this year

- Housing inflation has to come down and I still believe it will; If it does not, that is a threat to our 2% target

- I think there is room to get us to 2% if we begin to see housing inflation come down to more normal levels

- The real Fed Funds rate has not been this high in a very long time; We are pretty restrictive on policy so question is how long we stay there

14:04 (US) Fed's Kashkari (non-voter): Need to see more inflation progress before cut;Question of why rates should be cut if the economy remains strong

- I wrote down 2 rate cuts in my March SEP projection

- Does not see any reason why when we cut Fed Funds rate we cannot continue with our balance sheet plan

- Can keep reducing balance sheet once rate cuts begin

-TCBP +36% (announces execution of non-binding Letter of Intent for acquisition of NK Platform Technologies)

-CADL +24% (announces positive interim data from Randomized Phase 2 Clinical Trial of CAN-2409 in Non-Metastatic Pancreatic Cancer)

-LEVI +12% (earnings, guidance)

-ADN +11% (signs Joint Development Agreement with Siemens Energy to develop an integrated 500kW High-Temperature Proton Exchange Membrane fuel cell solution for maritime applications)

-HCTI +11% (announces strategic partnership with Cynomi to enhance cybersecurity in healthcare)

-BTM +4.7% (expands into Australia with 125 Bitcoin ATMs)

-TOI +4.0% (The Oncology Institute and Healthly forge strategic alliance to elevate cancer care access to pateitns in SoCal)

-CAG +3.9% (earnings, guidance)

-PLTR +3.2% (Oracle and Palantir announce partnership to provide secure cloud and AI solutions aiming to power businesses and governments around the world)

-RIGL +3.0% (announces publication of data on REZLIDHIA (Olutasidenib) in Post-Venetoclax patients with Mutant IDH1 AML in Leukemia & Lymphoma)

-COIN +2.4% (secures restricted dealer license in Canada)

-ABOS +2.3% (collaborates with Lonza to Advance Sabirnetug for the Treatment of Alzheimer’s Disease)

-SYF +2.0% (Wolfe Research Raised SYF to Outperform from Underperform, price target: $50)

Downside

-LW -13% (earnings, guidance)

-ACHL -11% (earnings)

-RDUS -7.0% (earnings, guidance)

-BV -4.8% (Goldman Sachs Cuts BV to Sell from Neutral, price target: $10)

-BIOR -4.0% (announces interim results of BT-600)

-EFTR -3.5% (Phase 2 KICKSTART Trial of Tomivosertib Combined with Pembrolizumab in Non-Small Cell Lung Cancer did not meet the pre-specified threshold of p=0.2; Will NOT move forward in frontline NSCLC)

-AXNX -3.3% (Axonics received a request for additional information from the U.S. FTC in connection with the FTC’s review of the Merger with BSX)

10:00AM: Fed Bank of Philadelphia President Harker (Non-Voter) participates in fireside chat on "Second Chance Employment" before the Business Case for Second Chance Employment Conference, Philadelphia, PA ( No text. Audience Q&A expected. No media Q&A);

12:15PM: Fed Bank of Richmond President Barkin (Voter) speaks on economic outlook at the Home Building Association of Richmond, Richmond, VA (Text available at speech time, posted to richmondfed.org. Audience Q&A expected. In-person event only);

12:45PM: Fed Bank of Chicago President Goolsbee (Non-Voter) participates in moderated question-and-answer session before the Multi-Chamber Economic Outlook Luncheon and Expo, Hilton Chicago/Oak Brook Hills, Oakbrook, IL (Embargoed text TBD. Livestream at www.chicagofed.or);

2:00PM: Fed Bank of Cleveland President Mester (Voter) participates in conversation on the economic outlook before virtual Global Interdependence Center Executive Briefing (Audience Q&A expected. No text);

5:00PM: Federal Reserve Bank of St. Louis First Vice President Kathleen O'Neill Paese (Non-Voter) gives welcome remarks before the 2024 Women in Economics Symposium hosted by the Federal Reserve Bank of St. Louis, St. Louis, MO and Virtual;

7:20PM: Federal Reserve Bank of St. Louis President Alberto Musalem (Non-Voter) gives introductory remarks before the 2024 Women in Economics Symposium hosted by the Federal Reserve Bank of St. Louis, St. Louis, MO (No monetary policy remarks. No media availability. In-person event with virtual option);

7:30PM: Fed Board Governor Kugler (Voter) speaks on "Enriching Data and Analysis in Economics with Real Life Experiences" before the 2024 Women in Economics Symposium hosted by the Federal Reserve Bank of St. Louis, MO (Text available. No Q&A. In-person event with virtual option)

My good buddy Peter Boockvar, chief investment officer with Bleakley Advisory Group, sees more evidence of our mixed economy and notes that all that glitters also can be silver:

Is the US economy strong like I still hear some say or much more mixed as I believe? More evidence yesterday from Ulta Beauty that it's much more mixed. Here is what they said that resulted in a 15% drop in its stock, coming from a very healthy space within in retail in terms of persistent demand:

"Economically, there's kind of mixed data points around the economic situation for the majority of consumers with healthy employment rates, wage growth, but also pressures that we see with rising credit card debt, student loan dynamics, other pressures that we certainly within our guests. Then more broadly, we know what's going on in the world around us, whether it's some of the political challenges, global complex and then our political environment here as we go through an election year. So it just creates this soup of activity for our consumers that they're trying to navigate through."

And here is what it means for their business, "What we're seeing right now as we're two months into our fiscal year, we have seen a slowdown in the total category. That category has grown - we came into the year and we talked about this on our call a few weeks ago - but expecting the category to moderate it after several years of very strong growth...So we have planned for moderation in total category growth to kind of the mid single digit range."

And then this, "What we've seen so far is a slowdown in the total category across price points and segments. That's a bit earlier and a bit bigger than we thought. Still growing, still a lot of engagement, all those things that I've had, but we've seen this growth rate come down probably faster than we anticipated."

With 7 Fed members speaking today, I recommend some Advil. Most of them expect to cut rates this year with only the degree in doubt, as we know, and this rise in energy and other commodity prices are only complicating the decision making. Powell mentioned yesterday inflation expectations being calm and taking comfort in that but I guess he hasn't yet noticed the one year high in 5 yr breakevens.

One VERY important and costly piece of one's cost of living, and experienced by homeowners and only indirectly by renters, is property taxes. If there is an inflation aspect that is NEVER transitory and NOT calculated in CPI and PCE in the housing component it is property taxes. Bloomberg News has a story today titled "US Homeowners See Biggest Property Tax Rise in Five Years." It says that data collected by ATTOM, a real estate data firm, reflected an average 4.1% rise in 2023 while in total dollars, it was up 6.9%. The CEO of ATTOM said "Property taxes took an unusually high turn upward last year, pushing effective rates up, while huge gaps in average tax bills between different parts of the country remained in place." Congrats to those who live in Essex County, NJ (which I did for 21 years) who pay the highest average property tax in the country.

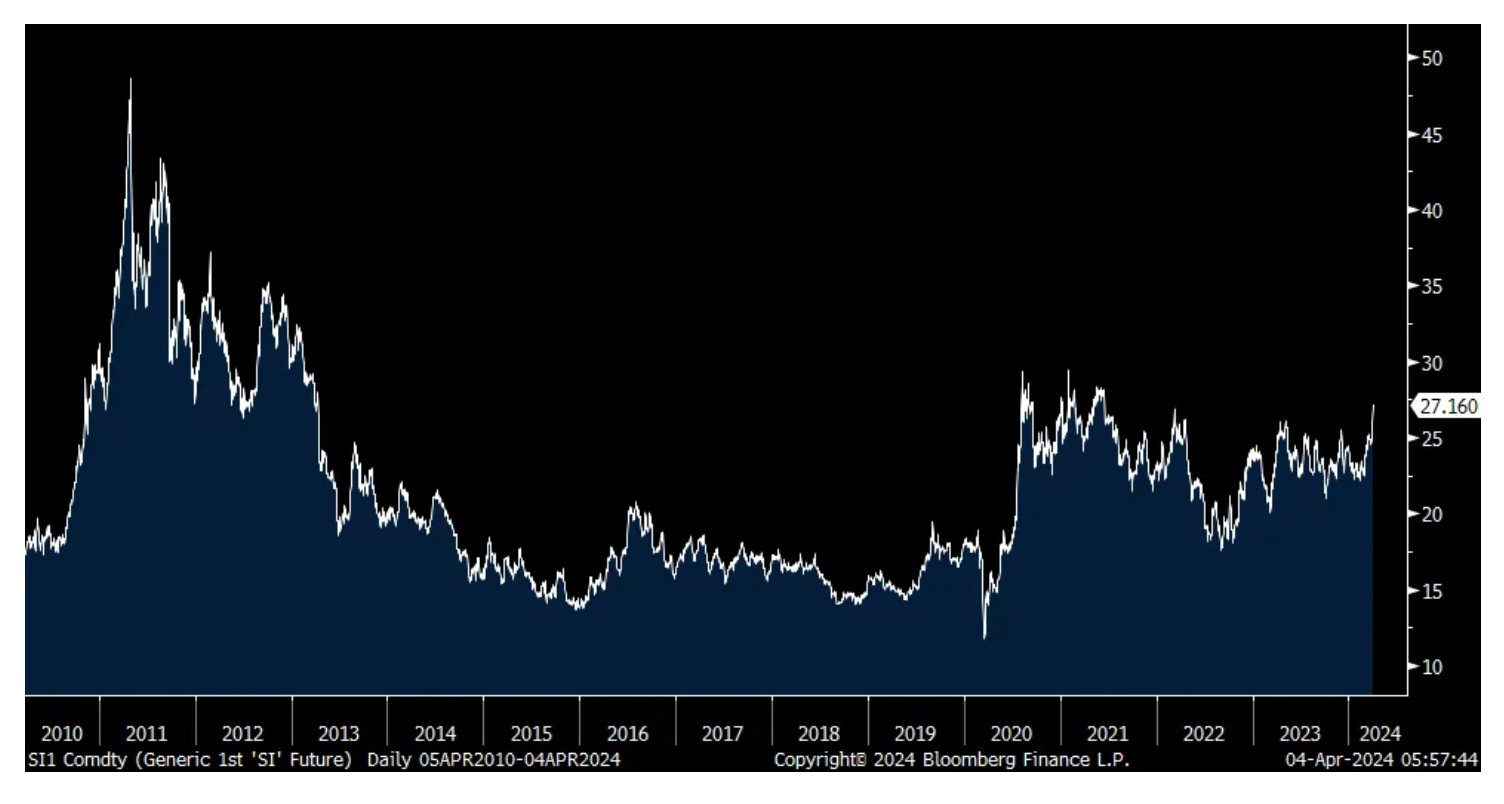

All that glitters is not always gold (which people are FINALLY talking about but has outperformed the S&P 500 from the year 2000 if you didn't know after 20 years of underperformance), it can be silver too. The small sibling of gold, with about half the demand coming from industrial uses, is finally playing some catch up and I believe has a lot more room to run. Silver still remains nearly 50% from its record highs. Not the best way to value silver but to provide some perspective, going back to 1971 when Nixon officially took us off what was left of the gold standard, the gold to silver ratio averaged about 60x. Today it stands at 84. Getting back to that long term average would currently put silver at $38. We remain very bullish and long of silver.

Silver front month contract

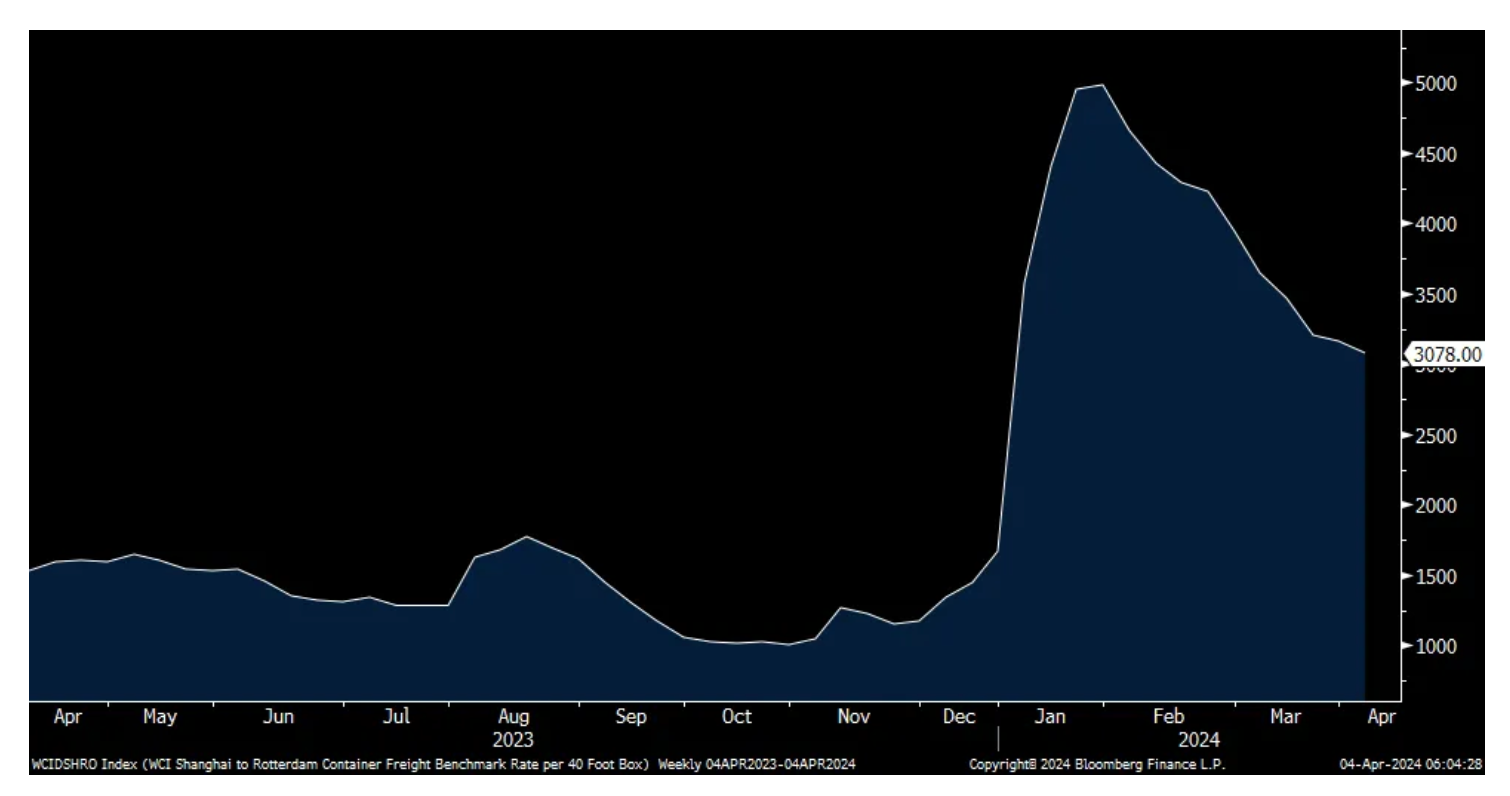

Here's an update on shipping rates as they continue to moderate after the spike seen off the lows in January. The World Container Index trip from Shanghai to Rotterdam for a 40 ft container averaged $3,078, down $81 on the week. That's still about double the 2023 year end rate but off the January highs of $4,984. The Shanghai to LA route, the price fell $121 to $3,704 for the week ended 4/4. It started the year at $2,100 and touched $4,344 at the end of January.

WCI Shanghai to Rotterdam

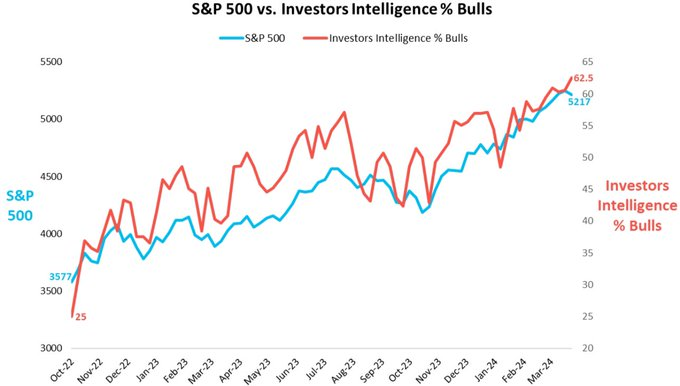

The Investors Intelligence survey got even more extreme with the Bull/Bear spread. As seen yesterday, Bulls rose to 62.5 from 60.6 while Bears shrunk to just 14.1 from 15.2. That 48.4 spread is the most since January 2018 right after the corporate tax cut was signed. I usually consider above 40 extreme and now we're approaching 50. Combine this with the Tobias Levkovich Citi Panic/Euphoria which is now in Euphoria territory and take heed and now be VERY aware of your sentiment surroundings because the current reads aren't seen much.

We saw some revisions to service PMI's. The March Eurozone's read was revised to 51.5 from 51.1 and up from 50.2 in February. S&P Global said, "The improvement in new orders was confined to domestic markets, however, as new export business continue to fall (albeit only marginally)." Employment did rise for a 38th straight month but did slow." Price pressures did ease "but remained steep overall." With respect to expectations from here, "The outlook for business activity over the next 12 months improved for a 4th month in a row." We know that the service sector has well outperformed manufacturing over the past few years as consumers shifted their spend and manufacturers and retailers right sized their inventories.

The UK services PMI for March was revised to 53.1 vs 53.4 initially and down from 53.8 in February. It's been above 50 for 5 consecutive months "supported by sustained improvements in new order intakes...Survey respondents once again commented on a turnaround in business and consumer spending, despite constraints on clients' budgets from strong inflation and elevated borrowing costs." Input costs "continued to rise sharply" but prices charged did slow. "However, this index only edged downwards since last summer and it remains well above the long-run trend, therefore adding to signs of sticky inflationary pressures in the domestic economy so far this year."

The ECB and BoE can't wait to cut rates this year but inflation, while moderating, isn't an easy situation for them either.

US: Futs are higher with both Tech and small-caps outperform; markets were assuaged by Powell remarks and an ISM-Srvcs print that was less hawkish/inflationary as the ISM-Mfg print. Pre-mkt, all Mag7 are higher ex-GOOG. Semis are rallying as chips production resumes following the earthquake in APAC the day prior. Bond yields are +1-2 bps, but USD weakness continues for a third day. In cmdtys, Energy is lower, Metals are mixed, and Ags are stronger; copper the notable outperformer. Today’s macro data focus is on jobless claims but likely will be ignored with NFP tmrw; 4x Fedspeakers today.

and...

EQUITY AND MACRO NARRATIVE: Yesterday, we saw markets react positively to both the ISM-Services print and to Powell’s press conference. With ISM-Srvcs, the market mostly paid attention to the decline in the Prices Paid component, which fell from 58.6 to 53.4. The 24Q1 average is 58.7 vs. 57.4 for 24Q4 but the January print of 64.0 looks like an outlier, similar to most of the January data. My thoughts after the print were:

This report should assuage fears of runaway inflation but also begs the question as to the degree of slowing the US may experience in the coming quarters. Details of the report point to a still tight labor market but companies doing a better job of managing that condition. While new orders are slowing, delivery times are improving. Another positive was the ISM’s Business Activity Index increasing from 57.2 to 57.4, indicating the 46th consecutive month of growth. This report appears to conflict with the ISM-Mfg report but would say this one is more important given the heavier percentage of GDP. To me, this still supports the growth without inflation narrative, though that “without inflation” part is sticky around 3% and may take longer than expected to get to 2%. The read-through to Equity markets is that this means both Tech and Cyclicals should remain supported and elevated level of rates should leave investors with a bias towards Size/Quality names irrespective of sectors.

More Night Moves: A Detailed Look at Overnight Futures and Why/What Markets Are Moving

* Markets bent but didn't break on Wednesday, rebounding from day's lows

* It was another Groundhog Day as rising rates and higher crude oil prices were disregarded in favor of continued price momentum

* The overbought remains elevated with the S&P Short-Range Oscillator standing at an elevated (but reduced) 2.09% vs. 2.62%

* Bond yields are materially unchanged this morning

* The U.S. dollar is modestly stronger against the yen

* Oil is flat after a big run

* Gold is -$3.70 following a move to all-time highs (silver has been turbocharged!)

* Bitcoin is +$400 and its uptrend is well intact

"I lost Thursday I had it somewhere Don't say it's where I left it I lost Thursday like it was nothing That fact is uncontested I am sleepy I'm not strong but it was like any day Where I left it Take it back Now I suspect foul play"

"Workin' on our night moves Trying to lose the awkward teenage blues Workin' on our night moves In the summertime And oh the wonder Felt the lightning And we waited on the thunder Waited on the thunder."

This daily Futures feature is like inside baseball. I try to show you and write about what I believe thoughtful hedge fund managers are looking at when they awake -- let's call it our normal routine -- setting the stage for their strategy for the day. The market is a complicated mosaic and the more info you have, the better trader and investor you will be!

The market (and money) never sleeps -- and neither do I, it appears! I have previously described the importance that overnight futures trading hold for me here. It is a guidepost to my strategy in the regular trading session. Moreover, the overnight/early morning futures hold opportunities as they are (1) inefficient, though liquid and (2) it seems fear and greed are often exaggerated outside the regular trading session. I frequently try to capture those efficiencies by trading actively both in the pre- and after-market sessions.

Here are brief observations I wanted to highlight and provide a summary of overnight price movements in various asset classes:

* Stock futures were higher overnight. S&P futures peaked at +18 and bottomed at +1. Nasdaq futures peaked at +110 and bottomed at +8. At 4:40 a.m. ET, S&P futures were +15 and Nasdaq futures were +75.

* Commodities were mixed with Brent crude -$0.32 after a stellar run higher. Precious metals are having some profit taking with gold -$2.60/ounce.

* The S&P Short-Range Oscillator is overbought at 2.09% vs. 2.62%.

* The VIX is at 14.25 (-0.08). I re-established some straddles on the recent VIX run over 15.

* The U.S. dollar is stronger against the yen:

* Treasury yields are flat. The 2-Year Treasury yield is +1 basis point to 4.685% and the 10-Year is unchanged to 4.355%. Over there, the yield on the 10-Year U.K. Gilt bond is -5 basis points.

* Overnight, the inversion of the 2s/10s Treasuries curve is down to -33 basis points

* Gold is -$2.40 and sits at $2,312. Turbocharged silver (on everyone's radar now) is +$0.11 to $27.18.

* Bitcoin is +$400 to $66.2k.

Here is a synopsis of some of my columns I believe were important, or in the event you were out for the day and/or did not read my Diary. The principal intent is to review the logic of my market moves and other factors:

"One of the frustrating things for people who miss the first rally in a bull market is that they wait for the big correction, and it never comes. The market just keeps climbing and climbing."