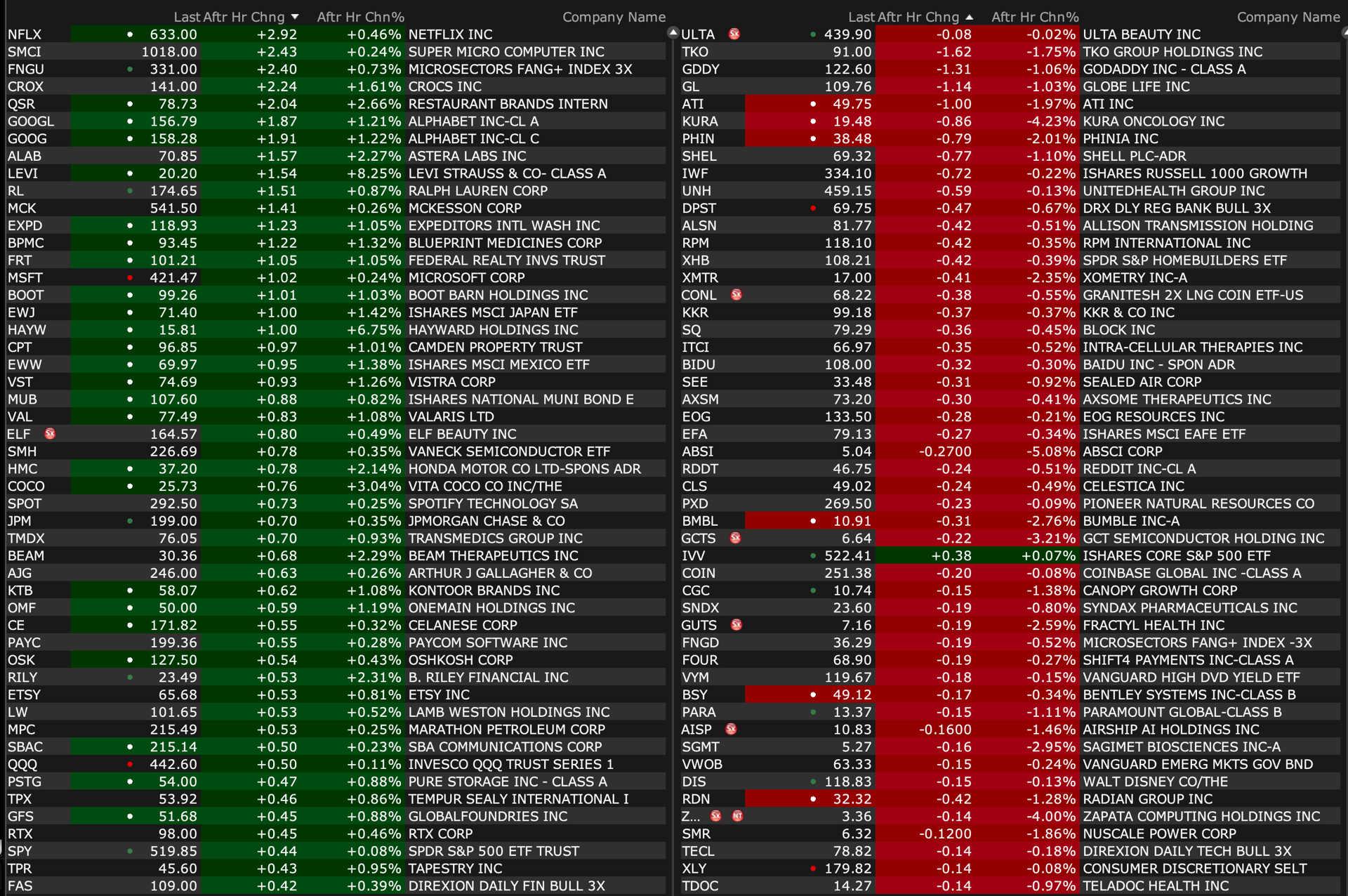

After-Hours Movers

BY Doug Kass · Apr 3, 2024, 5:47 PM EDT

BY Doug Kass · Apr 3, 2024, 5:47 PM EDT

Averages down on the day!

From earlier:

A Ludacris Day?

BY Doug Kass · Apr 3, 2024, 3:24 PM EDT

I picked and added to regional bank PGC today.

BY Doug Kass · Apr 3, 2024, 3:14 PM EDT

From my pal and best selling author (buy the book!)

BY Doug Kass · Apr 3, 2024, 1:50 PM EDT

If I owned Disney DIS, I would sell it now.

BY Doug Kass · Apr 3, 2024, 1:33 PM EDT

From Randorama:

Randy

Fed's Powell Says If Economy Evolves As Central Bank Expects, Most Federal Open Market Committee Participants See It As Likely Appropriate To Begin Cutting Policy Rate At Some Point This Year; To Do So, Fed Still Needs Greater Confidence Inflation Moving Sustainably Down Toward 2% Target

Powell Says Too Soon To Say Whether Recent Inflation Readings Are More Than Just A Bump; Fed Has Time To Let Incoming Data Guide Its Policy Decisions; Central Bank Is Making Decisions Meeting By Meeting; Recent Readings On Job Gains And Inflation Higher Than Expected, But Do Not Materially Change Overall Picture

Says Fed Is Not And Does Not Seek To Be Climate Policymaker; On Climate, Fed Has A Narrow Role As A Bank Supervisor, Which Over Time Is Likely To Include Climate-related Financial Risks

Chair Powell Says Outlook Still Quite Uncertain, Fed Faces Risks On Both Sides Of Its Mandate; Those Risks Continue To Move Into Better Balance; Fed Continues To Believe Policy Rate Likely At Peak For This Cycle; To Keep Public's Trust, Fed Must Avoid 'Mission Creep'

BY Doug Kass · Apr 3, 2024, 12:46 PM EDT

I put VKTX on my Best Ideas List yesterday:

At $74.82, I moved to medium-sized (VKTX) .

My lottery ticket calls go out on Friday.

Now at $74.40, I am placing VKTX on my Best Ideas List.

I will deliver my analysis in the next week.

Position: Long VKTX common (S) and calls (VS)

APR 2, 2024 10:30 AM EDT

_____

The shares have responded well to yesterday's selloff and have picked up a bid today - trading close to $79.

Normally I would take some off and trade around core - but with a +$60-$70 upside v. -$10-$15 downside, I like the upside reward v. downside risk.

Long VKTX common (S) and calls (M)

BY Doug Kass · Apr 3, 2024, 12:20 PM EDT

Here are the cost basis for my private equity shorts today:

* APO $112 58

* BX $126.80

* KKR $100.13

BY Doug Kass · Apr 3, 2024, 12:08 PM EDT

* Back to premarket levels of Tuesday...

BY Doug Kass · Apr 3, 2024, 11:55 AM EDT

Adding back to my private equity shorts.

BY Doug Kass · Apr 3, 2024, 11:45 AM EDT

Out of DJT short calls ("unpredictable" trading sardines) for a good profit.

These were Friday's expiration and given proximity I have covered.

I plan to reshort strength.

BY Doug Kass · Apr 3, 2024, 11:35 AM EDT

As expected, cannabis stocks have been sold off (a bit!) after the Florida news -- MSOS is now under $10 after trading close to $11 last week:

With (MSOS) trading at $10.65:

I wouldn't be surprised if we see a sell on the news now on MSOS - after the initial bump higher as expected.

There is still a lot of heavy lifting for voters to approve the measure on the ballot.

_____

I am a $9-$9 1/2 buyer of MSOS.

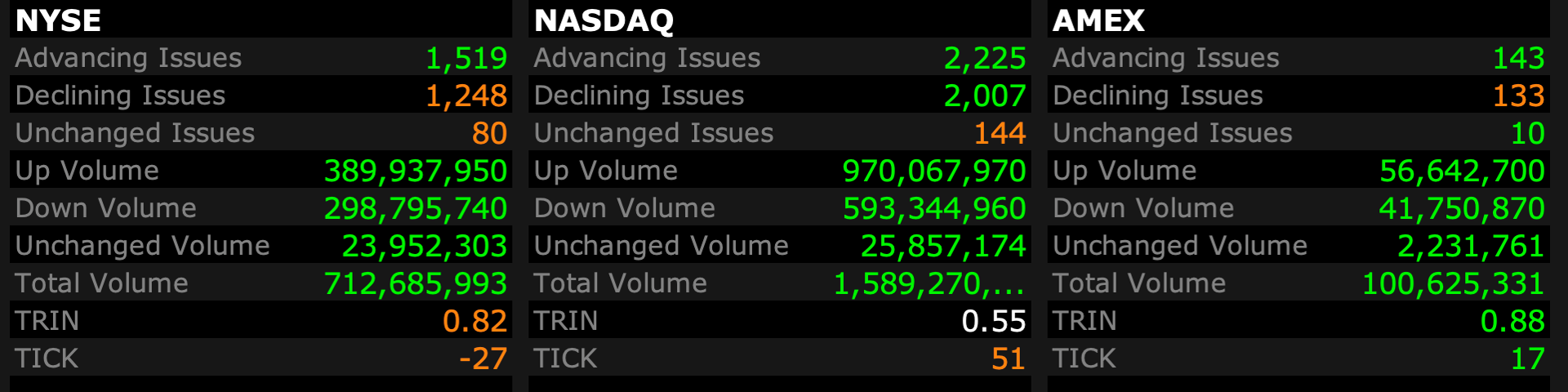

BY Doug Kass · Apr 3, 2024, 11:24 AM EDT

- NYSE volume 124M shares, 21% below its one-month average

- Nasdaq volume 1.53B shares, 6% above its one-month average

- VIX Down 0.48% to 14.54

Breadth

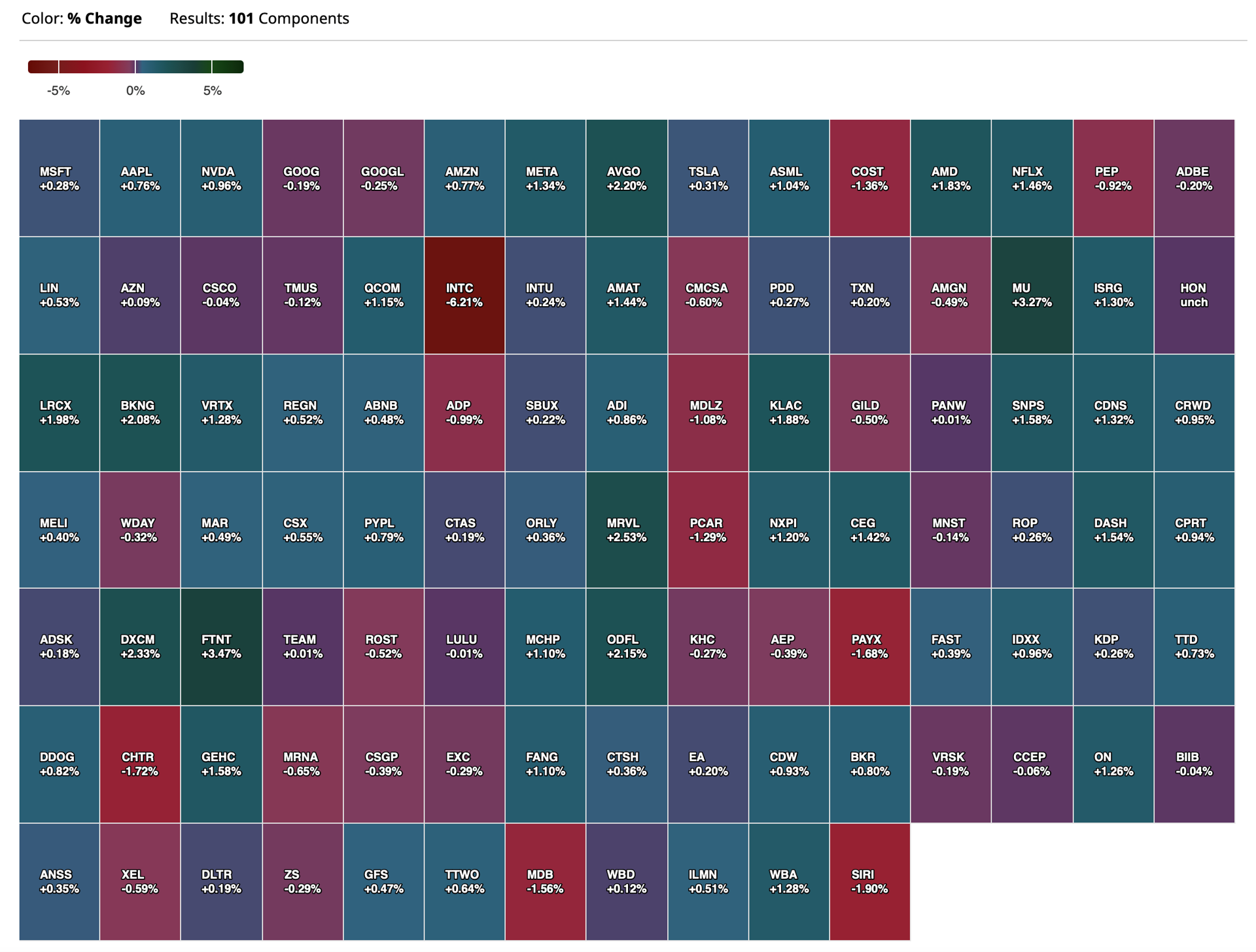

Nasdaq 100 Heat Map

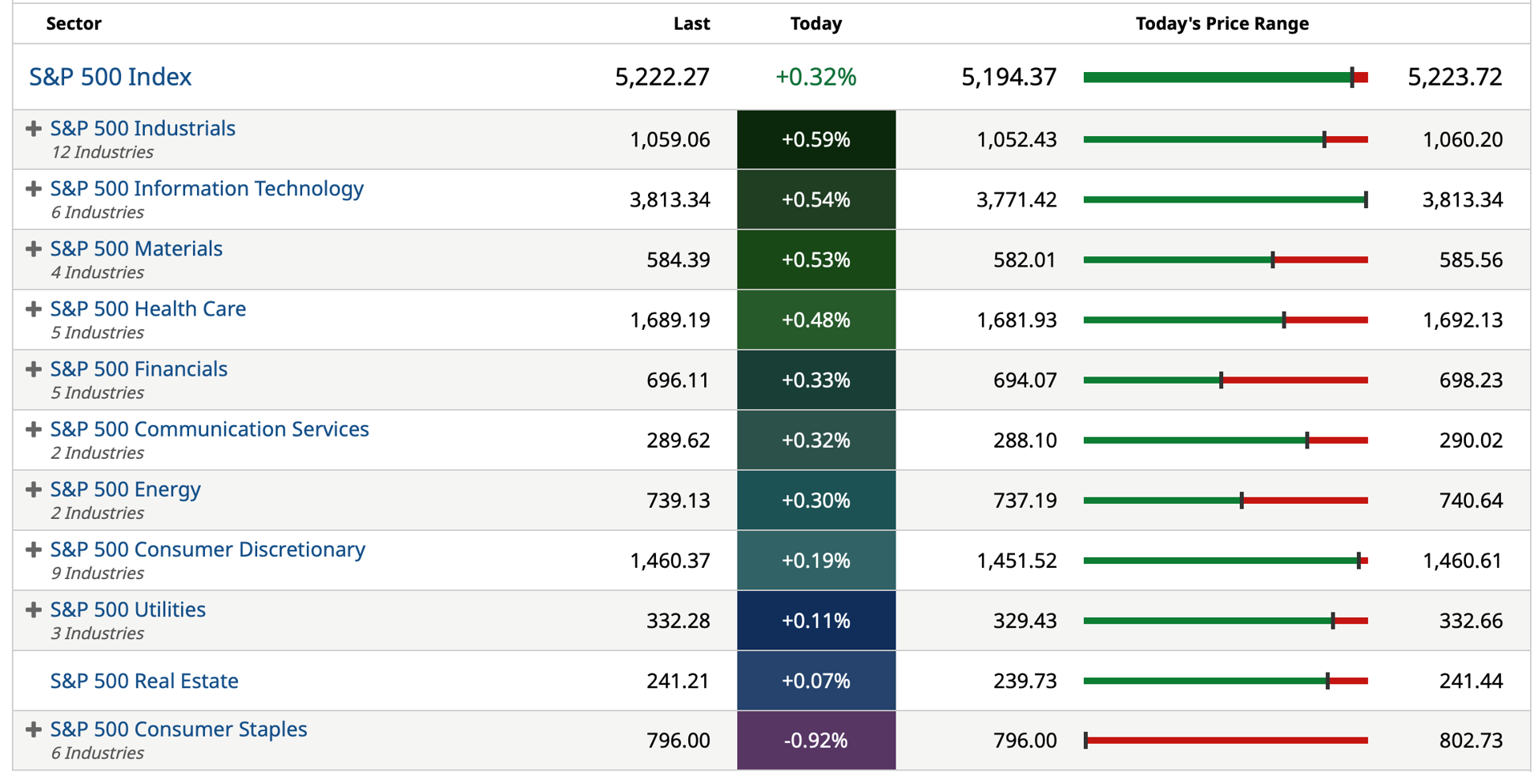

S&P 500 Index

BY Doug Kass · Apr 3, 2024, 11:10 AM EDT

I added to my June SPY/QQQ straddles.

BY Doug Kass · Apr 3, 2024, 11:00 AM EDT

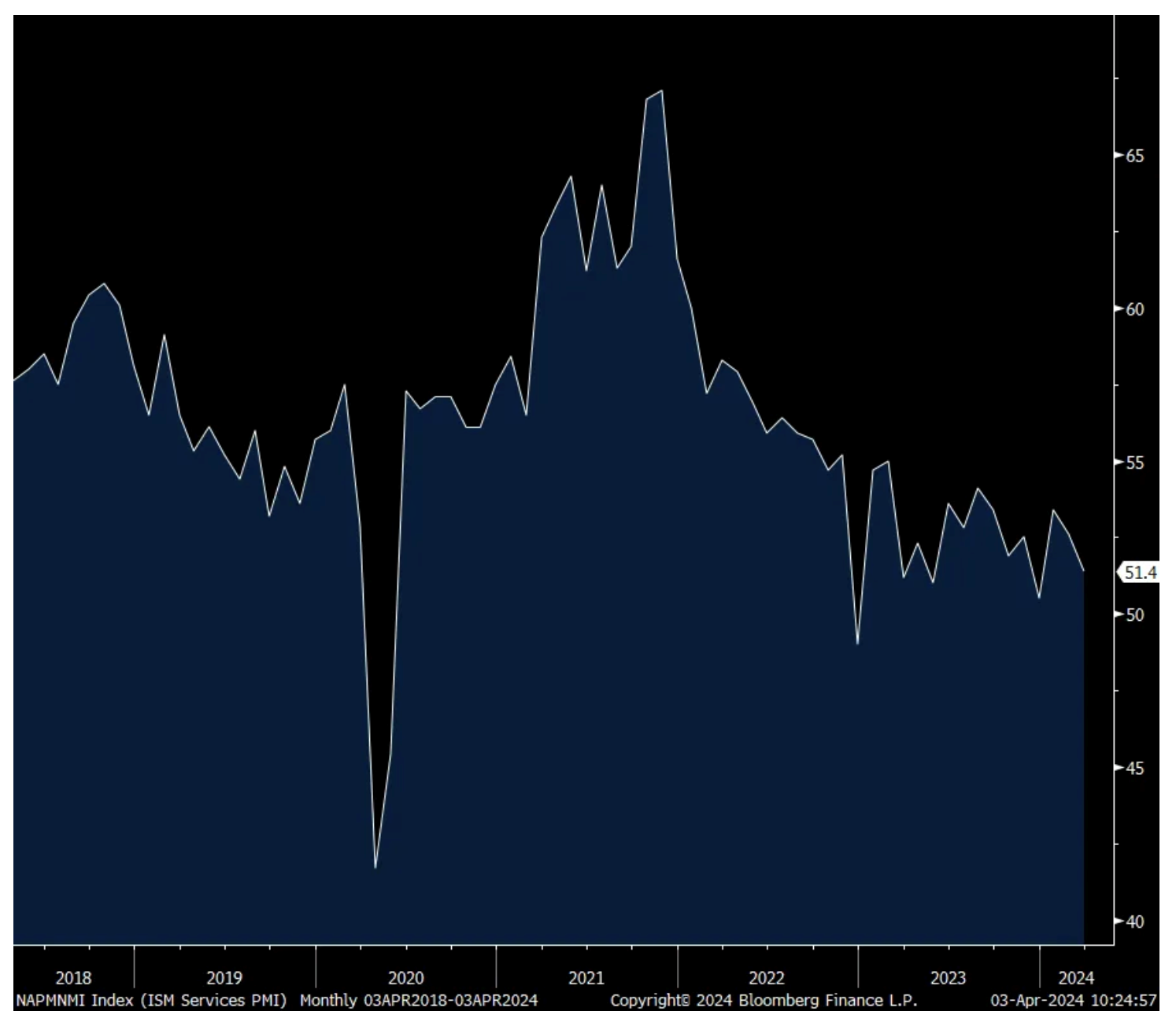

The March ISM services PMI fell by 1.2 pts m/o/m to 51.4 and that was below the estimate of a slight gain to 52.8. That’s a 3 month low and the 2nd lowest print since May 2023.

New orders were down by 1.7 pts to 54.4 and that puts it just under the 6 month average of 54.7. Backlogs were very weak, down by 5.5 pts to 44.8. No sign yet of inventory restocking as this component fell 1.5 pts to 45.6, the lowest since December 2022.

Employment was up .5 pt but at 48.5 is below 50 for the 3rd month in the past 4 and follows a below 50 print seen in manufacturing. Only 6 industries are seeing growth in employment and ISM said “Employment challenges remain a combination of difficulties in backfilling positions and/or controlling labor expenses.

Supplier deliveries fell by 3.5 pts to 45.4 (ISM said “Respondents indicated continuing improvement in logistics and the supply chain”) and prices paid were down by 5.2 pts to 53.4, the lowest since March 2020. Though 13 industries out of 18 reported paying higher prices, the same level as in February and off the low last year of 10. And ISM said, “respondents indicated that even with some prices stabilizing, inflation is still a concern.”

Breadth weakened too as 12 of 18 industries saw growth vs 14 in February and 4 reported a contraction vs 3 last month.

In the S&P Global measure of US services in March that does not include ag, mining, utilities, construction, wholesale and retail trade that ISM does, its index was 51.7 vs 52.3 in February and also a 3 month low. According to their model, this pace of services, combined with their manufacturing index, equate to about 2% GDP growth.

Of note, they saw a much different inflation picture than ISM. S&P Global said “Both input costs and output costs increased sharply in March, often as a result of rising wages. In fact, the respective rates of inflation quickened to six and eight month highs to rise further above pre-pandemic averages.”

Add in their manufacturing index and they said this, “Rising raw material and fuel prices are also adding to cost burdens, which is in turn driving average selling prices for goods and services higher at a rate not seen since July of last year. Both manufacturers and services providers alike are seeing intensifying cost and selling price inflation rates, which is likely to feed through to higher consumer price inflation in the near term.”

While Treasury yields fell in quick response to the ISM headline and prices paid component, maybe after they read the S&P Global press release and what they said on inflation, changed their mind as yields are about back to where they were at 9:59am est.

ISM Services

BY Doug Kass · Apr 3, 2024, 10:45 AM EDT

With S&P cash +15 handles on the ISM Manufacturing print slowdown relative to expectations, I am selling more April SPY and QQQ in the money calls (short).

BY Doug Kass · Apr 3, 2024, 10:15 AM EDT

From The Street of Dreams:

Tesla reported big delivery miss vs. lowered expectations, says Morgan Stanley Tesla reported a big delivery miss vs. lowered expectations, with deliveries in Q1 falling 9% year over year, marking the first annual decline since 2020, Morgan Stanley tells investors in a research note. The firm's Q2 delivery estimate of 496,000 units implies nearly a 30% sequential improvement quarter over quarter, far too large a gap to bridge given continued pressures on demand, competition and lack of new product. The firm would prepare for Tesla to initiate cost cutting initiatives to help preserve margin rather than to double down on price cuts.

Tesla price target lowered to $115 from $130 at JPMorgan JPMorgan lowered the firm's price target on Tesla to $115 from $130 and keeps an Underweight rating on the shares. The analyst slashed estimates and the price target for Tesla after updating for the company's Q1 deliveries, which tracked materially softer than its expectations. The delivery report "could spell trouble for investor confidence in the company's long-term growth outlook that is so critical to sustaining the stock's rarified valuation multiple," the analyst tells investors in a research note.

The firm says that while its price target implies 31% downside from yesterday's close, Tesla shares "could fall much further still" should the company not be successful in quickly restoring unit volume and revenue growth. JPMorgan thinks investors could elect to no longer assign the stock its "still hyper growth company valuation multiple."

Tesla units likely to decline year-over-year again in Q2, says Bernstein Bernstein notes Tesla reported Q1 deliveries of 387K, well below sell-side consensus of 443K. Q1 units produced were 433K, 46K higher than deliveries, with inventory significantly increasing, which will be a material headwind to free cash flow in the quarter, the firm says. Bernstein notes that Tesla cited production issues with Model 3 Highland and in other areas for its shortfall, but production was not the issue - demand was.

Not only are Q1 units down year-over-year for only the second time in history - with the other occurrence being at the onset of COVID - but consensus EPS estimates for 2024 were nearly $7 in late 2022 and the firm now forecasts about $2. Bernstein believes units are likely to decline year-over-year again in Q2 - and could potentially for the year. The firm has an Underperform rating on the shares with a price target of $120.

BY Doug Kass · Apr 3, 2024, 10:01 AM EDT

* The 2 year US note is +4 bps to 4.733%.

* The 10 year US note is +5 bps to 4.417%.

* The long bond is +5 bps to 4.558%.

BY Doug Kass · Apr 3, 2024, 9:45 AM EDT

ADP said a net 184k private sector jobs were created in March, 34k more than estimated and follows a gain of 155k in February (revised up by 15k). Most of the jobs came from medium and large companies with just 16k coming from small ones.

Services added 142k with leisure/hospitality leading the gain, contributing 63k, followed by trade/transportation/utilities (29K), education/health (17k) and financial activities (17k). ‘Information’ added 8k. There was a loss of 8k in ‘professional/business services.’ On the goods side, 33k of the 42k gain came from construction and I’m sure a lot had to do with the manufacturing facilities being built with the help of government largesse. Manufacturing added a modest 1k jobs.

On wages, for ‘job stayers’ they grew by 5.1% y/o/y, the same pace seen last month. Wages for ‘job changers’ spiked by 10% y/o/y and a notable rise from the 7.6% y/o/y gain in February. ADP said “The three biggest increases for job-changers were in construction, financial services, and manufacturing.”

Smoothing out the monthly volatility in the data, the 3 month average is 150k vs the 6 month average of 137k and the 12 month average of 204k. These figures remain above what the BLS is reporting but will converge when all is said and done with revisions.

I think the main reason for that spread is the still BLS reliance on the birth/death model which continues to add likely more jobs than are actually being created. If Friday’s figure for the private sector is as expected, the 3 month average would be 190k in their calculation.

Bottom line, as the ADP jobs figure is rarely market moving relative to BLS, that ‘job changer’ wage figure was eye popping and why yields are higher across the yield curve again with the 10 yr yield now kissing 4.40%. The 2 yr is at 4.72%.

BY Doug Kass · Apr 3, 2024, 9:35 AM EDT

Upside

-KTRA +102% (enters Definitive Merger Agreement with TuHURA Biosciences and will trade under the ticker "HURA")

-ABIO +91% (ARCA Biopharma and Oruka Therapeutics announce all-stock merger)

-VNDA +25% (Fanapt (iloperidone) receives U.S. FDA approval for the acute treatment of Bipolar I Disorder)

-LNZNF +19% (Phase 3 CLARITY Presbyopia Trials met Primary endpoint)

-ONMD +13% (discloses CEO succession plan along with convertible note sale)

-SGHT +12% (announces results of the 3-yr prospective GEMINI Trial and the Cross-Over Phase of the SAHARA RCT at the 2024 American Society of Cataract and Refractive Surgery (ASCRS) Annual Meeting)

-MOVE+10% (secures strategic investment from Tier-One multi-billion dollar medical device company; announces $24M private placement)

-CALM +6.4% (earnings)

-PLAY +6.1% (earnings; increases share buyback program)

-ALDX +5.6% (Oppenheimer Raised ALDX to Outperform from Perform, price target: $10)

-FLNC +5.0% (Raymond James Raised FLNC to Outperform from Market Perform, price target: $22)

-OWL +3.7% (confirms to acquire Kuvare Asset Management for $750M; also invested $250M in Kuvare UK Holdings)

-ALTM +3.4% (hearing Raymond James Raised ALTM to Strong Buy from Outperform, price target: $9)

-SIG +3.1% (adjusts guidance as a result of Preferred Shares repurchase agreement with Leonard Green & Partners, L.P.)

Downside

-CASA -78% (initiates court-supervised Chapter 11 sale process for businesses; to sell its 5G Mobile Core and RAN businesses, which include its Axyom Cloud Native 5G Core Software & RAN Assets, to Lumine Group without terms disclosed)

-VIEW -62% (reaches agreement with Cantor Fitzgerald and RXR to become a private company)

-VLD -11% (has substantial doubt of ability to continue as going concern)

-GOEV -8.6% (downside momentum following broker note stating company needs to raise funding)

-ATRA -7.2% (downside momentum)

-INTC -5.1% (sets targets for foundry and products business separately; Foundry losses expected to peak in 2024, to reach break-even by end of 2030)

-OUST -3.3% (Chardan Capital Markets Cuts OUST to Neutral from Buy, price target: $10)

-ALLY -2.9% (JPMorgan Chase and Co Cuts ALLY to Underweight from Neutral, price target: $39)

BY Doug Kass · Apr 3, 2024, 9:20 AM EDT

BY Doug Kass · Apr 3, 2024, 9:15 AM EDT

BY Doug Kass · Apr 3, 2024, 9:05 AM EDT

I am speechless that Cathie Wood continues to be provided a platform for her views, but maybe its just me!

BY Doug Kass · Apr 3, 2024, 8:55 AM EDT

8:30 AM: Fed Bank of Atlanta President Bostic (Voter) on CNBC;

9:45 AM: Fed Board Governor Bowman (Voter) speaks on "Bank Liquidity, Regulation, and the Fed's Role as Lender of Last Resort" before the Committee on Capital Markets Regulation Roundtable on Lender of Last Resort, Washington, DC (Text available. No Q&A. No webcast);

12:00 PM: Fed Bank of Chicago President Goolsbee (Non-Voter) gives opening remarks before virtual Federal Reserve Bank of Chicago event, "Preventing Elder Financial Exploitation: Research, Policies, and Strategies.” (Livestream at www.chicagofed.org. Embargoed text TBD);

12:10 PM: Fed Chair Powell speaks on the economic outlook before the Stanford Business, Government and Society Forum, Stanford, CA (Text available. Q&A from moderator);

1:10 PM: Fed Vice Chair for Supervision Barr (Voter) participates in "Community Rein- vestment Act" discussion before the National Community Reinvestment Coalition "Just Economy Conference 2024," (No text. Q&A from moderator. Webcast at https://www.youtube.com/watch?v=T6h5Ek0eboU);

4:30 PM: Fed Board Governor Kugler (Voter) speaks on "The Outlook of the U.S. Economy and Monetary Policy" before a conversation hosted by the Washington University in St. Louis, MO (Text available. Q&A from moderator and audience. Livestream at https://wustl.zoom.us/j/93119963702)

BY Doug Kass · Apr 3, 2024, 8:45 AM EDT

Ahead of the ADP report today, the employment component within the ISM services report (after the below 50 print in ISM manufacturing) and before the BLS jobs number Friday, lets go through what Paychex said in its earnings call yesterday.

"While our new client volumes remained solid and in line and both client and revenue retentions were in line with our expectations, several factors, including our decision to wind down the ERTC program based upon the recent legislative developments on Capital Hill, continued moderation of employment growth within our client bases, and slightly lower realized rates, all combined to create headwind - a larger headwind than what we had anticipated in the quarter." I bolded for emphasis.

Here is more, "The macroeconomic and labor market remains challenging for small and mid sized businesses. A tight job market for qualified workers, reduced access to affordable growth capital, and inflationary pressures continue to be headwinds for small businesses. Our small business employment watch continues to show moderation in both job growth and wage inflation.

But however, a relatively stable macro environment. The softening in hiring we started to see in the 2nd quarter continued in the third quarter. There is more choppiness in hiring across all customer segments and industries now. Our clients tell us they still can't find qualified employees and are not willing to hire just anyone at higher wage rates, especially in areas with recent minimum wage increases and aggressive legislative changes." I bolded, again.

This all squares with what I pointed out yesterday, C&I loans outstanding are at the lowest level since September 2022 and small and medium sized businesses are very reliant on their banks. I keep hearing from some about the 'solid' US economy and I have to respond that its very mixed instead. Some pockets might be solid (travel/leisure, high end spend, government boosted facility manufacturing) but others are reflecting softness and combined is a very confusing, uncertain picture.

On the experiential side, which has been a source of economic strength, Dave & Buster's had a good quarter and marketing helped after a weather impacted January. "Here recently, we've introduced $2 beers that timed with the NCAA tournament. We have all you can eat wings and on Thursday both of those are going very well. And we have kids eat free, that's really aimed at families." They are also benefiting from special events like birthday parties and such and game price increases too they talked about. "There's an opportunity to add a 10% increase in strategic game pricing over a period of time, and we're still committed to that."

As for the overall US consumer, they are confused too. "As we look forward to the consumer trends and everything else, I think it's kind of hard for us to pinpoint, given the uncertainty, and I'd say what uncertainty is, there's so much holiday mismatch around spring breaks at this point in time, and the continued choppiness that we're seeing...The unknown is just the macro environment. And what's going to happen with the consumer and any uncertainties."

Finally on their customer, "the choppiness we've seen is really from a visitation perspective. But once people are in the door, they're still spending at the same levels they've always spent. The dwell times are just the same as they were before. So it's really more of that visitation aspect of it than it is anything else...We've seen a little bit of weakness on the lower income consumer. But at the same time, we've seen strength on the higher end consumer. And everybody in between is kind of acting in their normal fashion." My bold.

With respect to PVH whose stock fell sharply yesterday if you didn't see, it seemed like most of their weakness was in Europe and US wholesale. "Since we spoke in December, we have seen consumer sentiment further slow across Europe, especially in our two biggest markets, Germany and the UK, and we have seen our wholesale partners there become even more cautious." It's Asian business was good and in North America, retail did ok while wholesale was soft as said. And bottom line in terms of their guide, "we have taken a cautious approach to planning 2024 due to the softening consumer backdrop we saw in January and February in a conservative wholesale environment."

Weekly mortgage applications were down slightly w/o/w with purchases flattish and refi’s lower by 1.6%. The average 30 yr mortgage rate is back to a one month high according to Bankrate.

Lastly on the US consumer, March auto sales were weaker than expected totaling 15.49mm SAAR, below the estimate of 15.85mm. For perspective, sales were 17.5mm in March 2019. This is a solid economy? The consumer is showing major cracks and the high cost of financing a car is certainly not helping.

Overseas, China's private sector Caixin services PMI rose a touch to 52.7 from 52.5 and better than the estimate of no change. Caixin said "Faster new business growth underpinned the latest acceleration of services activity expansion. The rate of new business growth was solid and the quickest since last December. Anecdotal evidence revealed that improvements in underlying demand conditions and business development efforts helped to boost the rise in new work."

As for the outlook, "Surveyed companies expressed confidence for the coming year, keeping the gauge tracking business expectations about future activity in expansionary territory. However, the reading was below its historical average." Not a market mover but Chinese stocks pulled back as did many in Asia after the US selloff. Outside of residential real estate, which is still working thru its pain but doing so, the Chinese consumer has shown signs of life while Chinese manufacturing is possibly bottoming.

Singapore continues to be a standout in Southeast Asia as its PMI printed 55.7, though down 1.1 pts m/o/m. S&P Global said "Singapore's private sector continued to expand at a solid pace in March, extending the strong growth conditions seen throughout the first quarter of 2024. Notably, forward looking indicators including new orders and backlogs of work continued to rise at steep rates, hinting at sustained business activity growth in the coming months." We remain bullish on Singapore and long some stocks there.

Lastly, March CPI in Eurozone rose 2.4% headline y/o/y and 2.9% core, both one tenth below expectations and each down 2 tenths from the month before. A slowdown in the pace of gains in non-energy good prices drove the deceleration as service prices rose 4% y/o/y for a 5th straight month. The 5 yr 5 yr inflation swap was unchanged in response at 2.33% as the rise in commodity prices threatens to reverse that goods price deceleration. The ECB seemingly can't wait to cut rates in June.

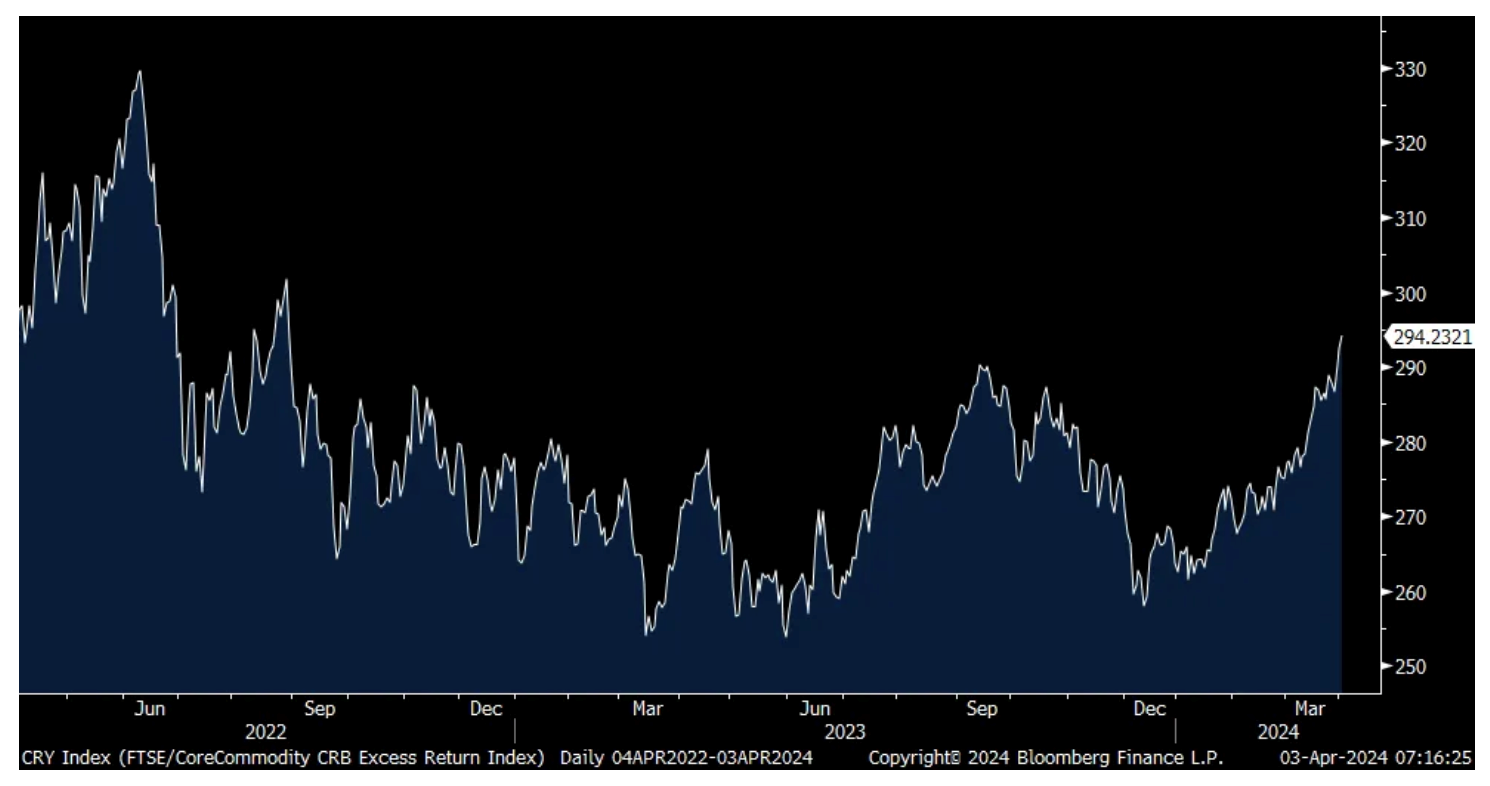

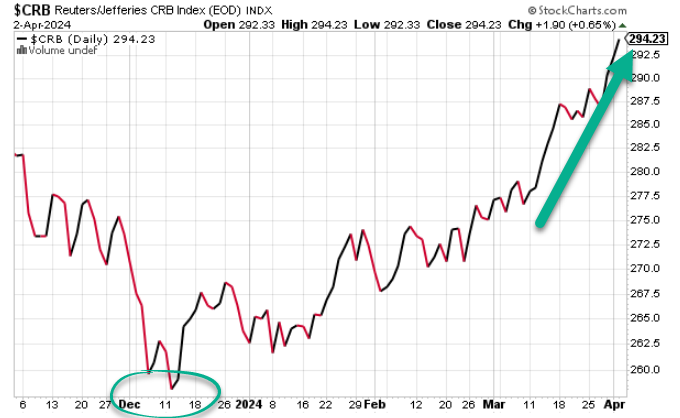

CRB Index

BY Doug Kass · Apr 3, 2024, 8:33 AM EDT

I am at a business breakfast so there will be no "Futures" column this morning.

Incidentally, the S&P Short Range Oscillator has dropped from 3.96% to 2.62%.

BY Doug Kass · Apr 3, 2024, 8:15 AM EDT

BY Doug Kass · Apr 3, 2024, 7:45 AM EDT

* Will former President Trump vote in favor of weed legislation?

Donald Trump will decide on marijuana legislation as a Florida voter.

BY Doug Kass · Apr 3, 2024, 7:33 AM EDT

I have muted yesterday's hater so I care not and will not be responding to him in the future for the reasons mentioned previously.

My credo in the way I live my life and how I engage professionally - is that I try to combine intelligence/analysis with high energy and integrity.

But I would like to briefly respond to the criticism that I don't routinely provide expirations, etc. for my options activity.

With the exception of the rare (and minimum capital employed) directional and offensive play in call or put options -- my options activity is pretty much confined to hedging longs with the sale of slightly in, in or out of the money calls (sold at a premium to underlying) and/or straddles and strangles which doesn't require specific expiration date or prices as they are traded and rarely kept on to expiration, and are usually done approximately at the cash price (for example, yesterday I sold straddles for June on SPY $517-$520) when cash was in that range, e.g., selling June monthly $518 puts and calls.

But the hater already knows what a straddle is. Whether I sold the $514 straddle or the $522 straddle - esp given small size is more or less irrelevant (as wont be holding to maturity).

Moreover, it is too tedious and I don't have the time to record my options trades and that is not the objective of my Diary to give a recommended list or blow by blow diary of every trade.

As noted I provide a relatively complete menu of my activity - from there you analyze and evaluate my ideas with yours and other input.

Criticism in my limited disclosure of options activity, which represents a very small of my total activity or portfolio weighting v. the sort of transparency I deliver in all my other trades and investments (in common shares/ETFs where I give size, timing and price! - something very few, especially considering the volume of my trading daily) is cherry picking to all except from a subscriber who simply is looking for something to criticize and pick a fight.

I also found the observation by the hater that I intentionally post done options trade (relative to my overall activity daily, weekly and monthly) as laughable. Haters think this is intentional but most know sometimes trades fall in the crack. Remember I have other obligations, most importantly managing my hedge fund, unlike some other contributors - this is not my full time job, not even close.

Consider the volume of my aggregate daily activity v. others - and the amount that I routinely memorialize.

I try my best to record most trades save the speculative ones. You don't know me if you feel I am trying to be deceptive. Perhaps the deceptive one is the hater.

Stated simply.

Haters gonna hate and always find something to criticize - whether justified or not!

I won't spend the time further explaining my modus operandi.

Hate on... but you are now muted.

Doug Kass

BY Doug Kass · Apr 3, 2024, 6:55 AM EDT

This is a valuable table for momentum-based short term traders:

BY Doug Kass · Apr 3, 2024, 6:45 AM EDT

From JP Morgan:

US: Futs are are off small with Tech underperforming and small-caps flat. Yields are higher pre-mkt ahead of Powell’s 12.10pm ET speech; despite his dovish rhetoric at the Mar 20 Fed Meeting press conference investors are nervous of a hawkish pivot. This comes amid a surge a cmdty prices and a spike in geopolitical tensions; pre-mkt all 3 cmdty complexes are higher with gold the notable laggard despite USD being flat. Pre-mkt, Mag7 and Semis are under pressure with INTC -4.9% on profit concerns. Today’s macro focus is on ADP (has not been reliably predictive of NFP), ISM-Srvcs, and 2x Fedspeakers (including Powell).

and...

EQUITY AND MACRO NARRATIVE: Yesterday’s move triggered a number of incoming inquires about whether this is the end of the rally, how worries people should be about markets, and whether the price action foretells something much worse in the economy. I think none of these; the market closed within 1% of its all-time high … set last week. It is possible that we could see a 2-3 % pullback but think you need to see either deterioration in the macro story or an earnings season that shows negative sequential growth. Equities remain sensitive to bond vol, more so than yield levels, which is what we have seen this week with the 10Y yield moving higher ~15bps and SPX selling off less than 1%. A few more thoughts:

· The broader equities moves were driven by rapid rates repricing today with rates vol moving higher. Unsurprisingly, the more yield sensitive sub-sectors got hit with things like ARKK -3%. As rates stabilized, the Equity selloff slowed and caught a mild bid, adding ~40bps from its intraday low.

· Ex-TSLA’s 5.6% decline, the balance of the Mag7 held up. META was +1.2% and NVDA was the only other laggard. If you look at the momentum index, it is still in green.

· If the move in yields is a repricing due to higher growth, then some of the sectors/sub-sectors that underperformed are inconsistent with that narrative of stronger growth, e.g., Homebuilders, Transports, and Retailers.

· Jay Barry on Treasuries – he is neutral, waiting for a moment to add duration. May add duration due to valuation, but the selling momentum pushed him to the sidelines.

· What comes next? Tactically bullish. NFP may end up being a non-event since Powell stated that a strong, or even strengthening, labor market would not be a reason to delay cuts. However, a portion of the market appears to be expressing a view that Powell will make a hawkish pivot. This pushes the onus to CPI to determine vectors for Equities and Treasuries. Given the repricing in the yield curve, this may have de-risked the CPI. We will do a deeper dive on CPI next week but the commentary from Flash PMIs point to another inflation increase that may show as soon as next week’s print. From a micro perspective, Banks kickoff earnings season next week (Apr 12) and Mag7 names kick off on Apr 25. Those Mag7 earnings may be the lynchpin to stall or reverse this bull market.

- From S&P Global’s Chief Economist on the March Flash PMI print, “Costs have increased on the back of further wage growth and rising fuel prices, pushing overall selling price inflation for goods and services up to its highest for nearly a year. The steep jump in prices from the recent low seen in January hints at unwelcome upward pressure on consumer prices in the coming months.”

BY Doug Kass · Apr 3, 2024, 6:35 AM EDT

“A bull market is a bull. It tries to throw off its riders.” - Richard Russell

Bonus- Here are some great links:

BY Doug Kass · Apr 3, 2024, 6:20 AM EDT

Source: Hedgeye

BY Doug Kass · Apr 3, 2024, 6:10 AM EDT

BY Doug Kass · Apr 3, 2024, 6:00 AM EDT