With Fantastic Results, Why Is Meta's Stock Down? Here's How to Play It

This is CEO Mark Zuckerberg's 'Year of Efficiency' and it sure looks like it as profitability has been prioritized and expenses minimized.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Perplexing for sure.

On Wednesday afternoon, Meta Platforms META released the firm's third quarter financial results. From just about every way one can slice the data, Meta Platforms had a nice quarter, a really nice quarter. Still after a bloody day on Wall Street where META gave up 4.17% during the regular session, the stock continued to selloff after hours. So, what gives? Let us explore.

For the three month period ended September 30th, Meta Platforms posted a GAAP EPS of $4.39 on revenue of $34.146B. The revenue print was good enough for year over year growth of 23.2% as both the top and bottom line results beat Wall Street quite decisively.

As revenue was growing 23.2%, costs and expenses decreased 7.5% to $20.398B. This put operating income at $13.748B, which was good for growth of 142.7% as operating margin popped from 20.4% for the year ago comp to an impressive 40.3%. After interest and taxes, net income printed at $11.583B, which was up 168%.

Remember, this is CEO Mark Zuckerberg's "Year of Efficiency" and it sure looks like it as profitability has been prioritized and expenses minimized.

Segment Performance

- Family of Apps generated revenue of $33.936B (+23.7%) that produced an operating income of $17.49B (+87.3%). Both of these lines beat expectations.

- Reality Labs generated revenue of $210M (-26.5%) that produced an operating income/loss of $-3.742B. Revenue here fell short of expectations. That said, the massive operating loss for this segment was less than feared.

Geographic Performance (mostly ad sales)

- US & Canada generated revenue of $15.19B (+16.5%)

- Europe generated revenue of $7.777B (+34.2%)

- Asia-Pacific generated revenue of $6.928B (+19.8%)

- Rest of World generated revenue of $4.251B (+37.1%)

Engagement Metrics

- Family daily active people (DAP) averaged 3.14B for September (+7% y/y).

- Family monthly active people (MAP) were 3.96B as of September 30th (+7% y/y).

- Facebook daily active users (MAUs) average 2.09B for September (+5% y/y).

- Facebook monthly active users (MAUs) were 3.05B as of September 30th (+3% y/y).

Outlook

For the current quarter, Meta expects to drive revenue of $36.5B to $40B, which would come to growth of 13.5% to 24%. A 2% forex related tailwind is expected. That was just a touch below Wall Street's expectations. For the full year, Meta sees total expenses of $87B to $89B, down from prior guidance of $88B to $91B. This includes a rough $3.5B in restructuring costs. For next year, Meta sees full year expenses of $94B to $99B.

Fundamentals

For the period reported, Meta Platforms generated operating cash flow of $20.402B (+110.5%). Out of that came CapEx of $6.496B (-30.6%) and principal payments of $267M (up from $163M). This left free cash flow at a robust $13.639B, up from $173M. No, I'm not figuring out the year over year percentage gain there, but it's a lot. Out of that number came the repurchase of $3.57B worth of common stock for the firm's treasury. META does not pay shareholders a dividend. Much of the rest ended up as cash on the balance sheet.

Glancing at that balance sheet, Meta ended the period with a cash position of $61.123B and current assets of $78.378B. Current liabilities add up to $30.531B, mostly accrued expenses and "other" current liabilities. This puts the current ratio at 2.57, which is better than solid.

Total assets amount to $216.274B, including $21.481B worth of goodwill and other intangibles. At less than 10% of total assets, this is not a problem whatsoever. Total liabilities less equity comes to $73.401B, including long-term debt of $18.383B, which is something that the firm could pay off out of pocket more than three times over. As an analyst, it is an absolute pleasure to look over a statement of cash flows and a balance sheet this strong. Meta Platforms is as fundamentally sound as large corporations come.

Wall Street

Since Meta Platforms released these earnings last night, I have come across 24 sell-side analysts that are both rated at a minimum of four stars at TipRanks and have opined on the stock. Among these 24 analysts, there are 23 "buy" or buy-equivalent ratings and one "hold" rating. That "hold" rating and one of the "buys" elected not to set a target price, leaving us with 22 targets to work with.

The average target price across those two analysts is $388.36 with a high of $425, three times (Lloyd Walmsley of UBS, Ronald Josey of Citigroup, and Mark Mahaney of Evercore ISI) and a low of $345 (Colin Sebastian of Robert W. Baird). Once omitting one of those highs and that low as potential outliers, the average target across the other 20 rises slightly to $388.70.

My Thoughts

I've just written up a fantastic analysis of a firm that seems to be hitting on all cylinders, while controlling costs and standing atop a more than solid foundation. So, why is the stock down? This is why...

During the call last night, analyst Mark Shmulik of Bernstein asked, "As we kind of look ahead here to the fourth quarter, there's certainly been a lot of unfortunate geopolitical kind of activity around the globe. Would love to just understand some color on how that affects kind of Meta's ad business. Thank you."

CFO Susan Li answered honestly. The keyword reading algorithms flew into action when she answered and then the rest of Wall Street noticed.

Li stated: "I think I should start by saying that our thoughts are with everyone who has been impacted by the horrific violence in the Middle East, and we know that our services can be a vital tool for information and connection and expression at a moment like this. And we're continuing to monitor the situation and are doing everything we can to keep people safe and to keep our services secure."

Then Li added: "Now in terms of how this translates into impact on the Q4 business, first of all, I should say that coming into Q4, we've been seeing continued strong advertiser demand in key segments, including online commerce and gaming. But having said that, we are also seeing more volatility at the start of the quarter. That's in part why we widened our guidance range to capture that uncertainty. And so for instance, while we don't have material direct revenue exposure to Israel and the Middle East, we have observed softer ad spend in the beginning of the fourth quarter, correlating with the start of the conflict."

Li explained that this was built into the firm's Q4 guidance, which you read above was just a bit lighter than expected.

That was all the algos needed to hear and undid all of the good stuff (at least in the short-term) in this report.

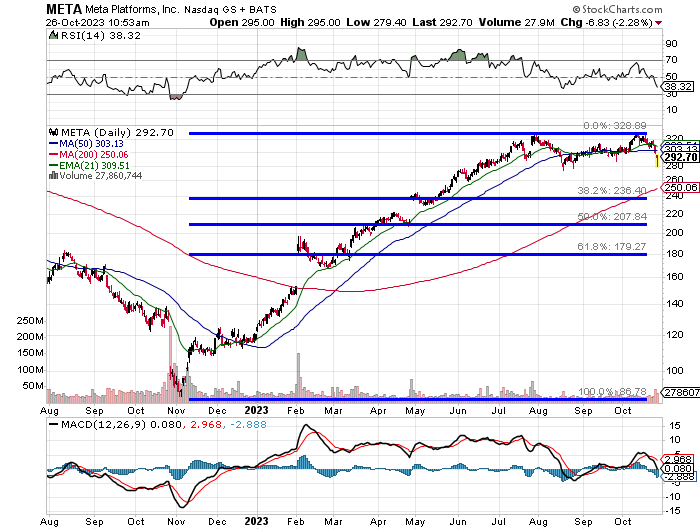

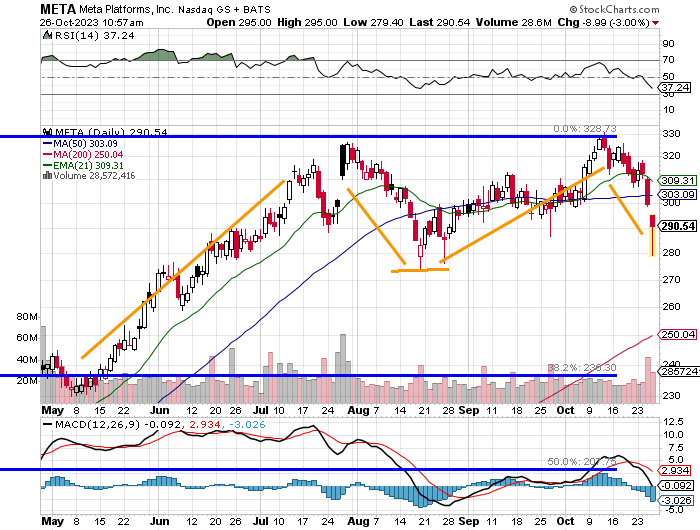

As readers can see, META could drop as far as $250 just to find its 200 day SMA (simple moving average), or as far as $235 just to hit a 38.2% Fibonacci retracement of the stock's November through July rally. Even amid this selloff, the shares are up 231% in twelve months. Let's zoom in...

This is a good company trading at just 18 times twelve months' forward looking earnings. That's in line with the S&P 500 and this firm is a standout compared to the average S&P 500 stock. Yet, technically, we are looking at a double top reversal pattern with a $274 downside pivot. If these shares trade that low, they could indeed trade much lower.

That said, I think as an investor who is flat this name, that I become very interested below pivot. The downside target if the pivot fell would be the 38.25 Fib level. That said, I don't think I will wait that long to dig in. I start at pivot and scale in from there. Conversely, if META retakes the 50 day SMA ($303) without hitting pivot all bets are off as the double top would have failed.

Trade Ideas (minimal lots)

- Sell (write) one January META $275 put for about $12.80.

- Purchase one January META $265 put for about $9.70.

- Sell two January METS $235 puts for roughly $3.80.

Net credit $10.70

Note: The first two executions are just an attempt to pick up some shares should META barely reach pivot. The trader is getting paid $3.10 to risk losing $10 if he or she gets run over. The last transaction is an attempt to get paid to buy the shares at the 38.2% Fib level if they should fall that far by January. Best case? None of these options are ever exercised and the trader pockets the credit.

At the time of publication, Stephen Guilfoyle had no position in the securities mentioned.