Why I'm Not Joining in on the Lockheed Martin Sell-Off

A pair of defense names are selling off after reporting their earnings.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Thursday morning, long-time Sarge-fave Lockheed Martin LMT posted the firm's third-quarter financial results. Lockheed posted an adjusted EPS of $6.84 (GAAP EPS: $6.80), beating Wall Street's expectations quite handily, while generating revenue of $17.104 billion, which was up 1.3% year over year, but just short of consensus view.

Elsewhere, RTX RTX, which is the old Raytheon Technologies, reported an adjusted EPS of $1.45 (GAAP EPS: $1.09), also beating Wall Street decisively, while posting revenue of $20.089 billion. That was up 5.8% year over year, while outperforming expectations. Both firms revised their full year outlooks for 2024 to the upside.

Lockheed Martin

The firm made 48 F-35 deliveries, increased production of its missile programs and built up a record order backlog of more than $165 billion. President and CEO Jim Taiclet commented in the press release, " As a result of our strong year-to-date results and confidence in our near-term performance, we are raising the outlook for full year 2024 sales, segment operating profit, EPS and free cash flow. Looking forward, we continue to make progress on the three key initiatives of our 21st Century Security strategy of strengthening the resiliency and scalability of our production system, accelerating cutting edge digital and physical technologies into all our mission solutions and our internal operations, and expanding international partnerships to broaden our production capacity and drive more international sales."

Segment Performance

- Aeronautics generated sales of $6.487 billion (-3.4%), which produced an operating profit of $659 million (-1.7%) on a segment operating margin of 10.2% (up from 10%)

- Missile and Fire Control generated sales of $3.175 billion (+8%), which produced an operating profit of $456 million (+14.6%) on a segment operating margin of 14.4% (up from 13.5%)

- Rotary and Fire Control generated sales of $4.367 billion (+6%), which produced an operating profit of $483 million (+0.2%) on a segment operating margin of 11.1% (down from 11.7%)

- Space generated sales of $3.075 billion (-0.8%), which produced an operating profit of $272 million (+5%) on a segment operating margin of 8.8% (up from 8.4%)

Cash Flows

For the quarter, Lockheed generated operating cash flow of $2.438 billion, out of which came capex spending of $355 million. This left $2.083 billion in free cash flow. Year to date, over nine months, Lockheed has produced free cash flow of $4.846 billion.

Guidance

For the full year, Lockheed Martin now projects net sales of $71.25 billion, up from a previously issued range of $70.5 billion to $71.5 billion in July. The firm also sees business segment profit at $7.475 billion, up from a range of $7.35 billion to $7.5 billion, GAAP earnings per share of $26.65, up from a range of $26.10 to $26.60 and free cash flow of $6.2 billion, up from a range of $6 billion to $6.3 billion.

With that realized and expected free cash flow, Lockheed has increased its share repurchase authorization from $7.3 billion to $10.3 billion, while increasing its quarter per share cash quarterly dividend 5% to $3.30.

RTX

The firm's order backlog is now up to $221 billion, which comes when broken down from the commercial sector ($131B billion) and from defense ($90 billion). The firm realized $90 million in incremental gross cost synergies during the quarter, reaching the $2 billion post-merger target. President and CEO Chris Calio also commented in his firm's press release, "RTX delivered another strong quarter of organic sales growth, adjusted segment margin expansion, and free cash flow. Demand across our portfolio, particularly within commercial aftermarket and defense, remains robust and gives us the confidence to again raise our full year outlook for adjusted sales and adjusted EPS."

Segment Performance

- Collins Aerospace generated sales of $7.075 billion (+7%), which produced an operating profit of $1.062 bilion (+18%) on a segment operating margin of 15% (up from 13.6%)

- Pratt & Whitney generated sales of $7.239 billion, which produced an operating profit of $557 million on a segment operating margin of 7.7%. The year-over-year comparisons for this unit are not meaningful. Once adjusted, these comparisons work out to +14% for sales, +45% for operating profit and 8.2%, up from 6.5% for segment operating margin

- Raytheon generated sales of $6.386 billion (-1%), which produced an operating profit of $647 million (+16%) on a segment operating margin of 10.4% (up from 8.8%)

Cash Flows

For the quarter, RTX generated operating cash flow of $2.523 billion, out of which came capex spending of $552 million. This left $1.971 billion in free cash flow. Year to date, over nine months, RTX has produced free cash flow of $4.042 billion.

Guidance

For the full year, RTX has upwardly revised the firm's previously issued guidance. RTX now sees adjusted sales of $79.25 billion to $79.75 billion, up from $78.75 billion to $79.5 billion, and adjusted EPS at $5.50 to $5.58, up from $5.35 to $5.45. The firm also now sees full-year free cash flow printing at approximately $4.7 billion, which is a reiteration.

The Stocks

Both of these names are selling off this morning, Lockheed quite severely. That said, Lockheed went out last night up 36.6% year to date, while RTX was up 50%, so we who have been long defense and aerospace really do not have a lot to complain about after a 2023 that saw the entire space (no pun intended) run sideways to lower.

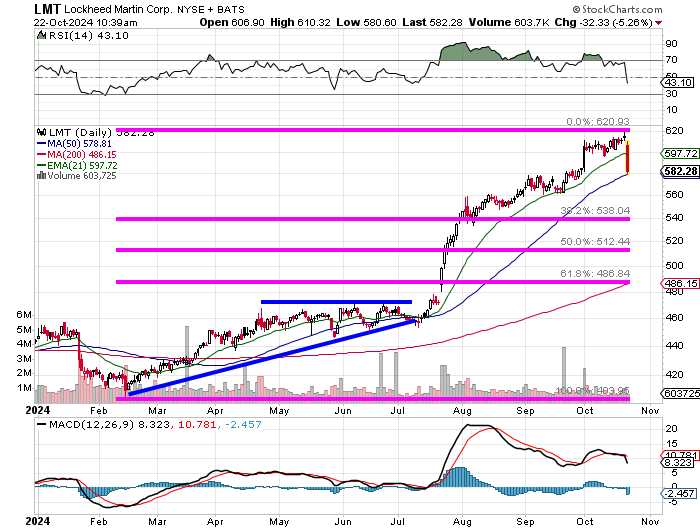

Lockheed gave up a quick 5%-plus this morning, finally groping around for support at its own 50-day SMA. Relative strength has fallen in one morning from nearly being overbought to neutral, while the daily MACD has reacted quite similarly to this round of profit taking. Have I sold any? Not today. I have made sales as target prices have been surpassed. As readers can see, LMT got just about as much as it could out of that ascending triangle that culminated with a breakout in mid-July.

If one were thinking about adding on this dip, I would make sure that the 50-day line holds first. One would not enjoy adding at or above that line and then seeing the stock look for its next line of support. The halfway-back point is around $512, and a 61.8% Fibonacci retracement of that rally would take the stock all the way back to $486, which just happens to be where the 200-day SMA currently resides.

Should the 50-day SMA fail to hold, I will likely make a sale on a partial with the intent of adding that partial back on when the next positive set-up appears.

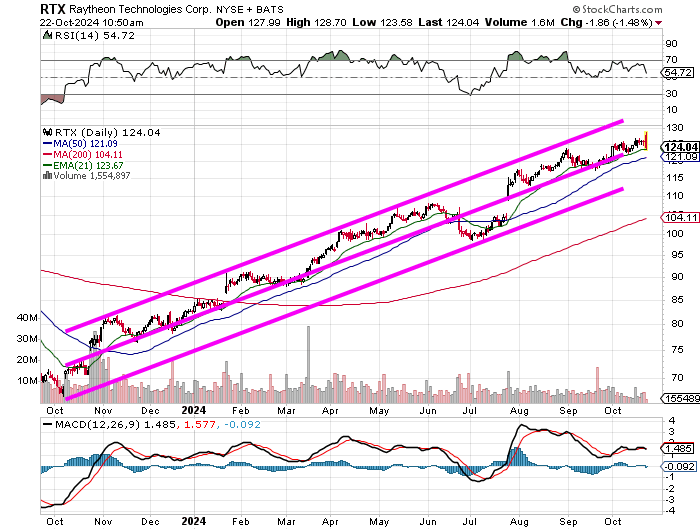

Look at that beauty. They say that the trend is your friend, and RTX is certainly still in an unbroken trend. Relative strength is nothing special, but better than neutral. The daily MACD is sending a slightly-bearish message. Do I need to add to RTX on this dip? No. The 50-day SMA has not even been tested since late July. That said, if there is one of these stocks to initiate on the long side or to add to a long position in the coming days, I am thinking that more likely than not, the stock is RTX.

Ready for more fun? Northrop Grumman NOC reports on Thursday morning.

At the time of publication, Guilfoyle was long LMT, RTX and NOC equity.