Walmart Is Still Champion to Struggling Consumers: Here's How to Trade It

Guidance for the full year is excellent, but the firm is going to have to get on its horse and better manage its free cash flow.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

There are just a few retailers where budget minded consumers turn to when times get tough. By all accounts, pandemic driven helicopter savings have run dry, credit card balances are up, and so are delinquencies. The struggling consumer reaches for help. The "middle class" consumer who might be new to the struggle, or perhaps back in a position they had once hoped never to revisit does as well.

There are dollar stores. There are retailers that buy overstocked inventories in bulk and then offer consumers a "break" on last year's styles.

Then there is the one retailer who has always been champion to the commoner. I speak of no other firm than America's largest retailer... Walmart WMT. "Thank goodness for Walmart,'' said every American ever who has spent even one day on the wrong side of the coin, or who made a turn when they should have gone straight.

The Champ Reports

On Thursday morning, Walmart went to the tape with the firm's first quarter financial results. Traffic was slowed on the way as there was some rubbernecking as motorists worked their way around the Deere DE wreckage. For the three month or so period ended April 30th, Walmart posted an adjusted EPS of $0.60 (GAAP EPS: $0.63) on revenue of $161.508B. A small negative adjustment was made for realized/unrealized gains/losses on investments and business reorganization charges.

The top and bottom-line results both exceeded Wall Street's expectations, while the sales print reflected year over year growth of 6%. Comp store sales were up 3.8%, beating expectations for growth of 3.4%. Quite notably, global advertising grew 24% as a business, including 28% growth for Walmart Connect. Global e-commerce sales were up 21% led by store fulfilled pickup and delivery.

Operations

As revenue was growing by 6%, the cost of sales increased 5.3% to $121.431B, leaving a gross profit of $40.077B (+8.3%) on a gross margin of 24.8%, which was an improvement from 24.3% for the year ago period. Operating expenses increased 8% to $33.236B. That left a GAAP operating income of $6.841B, which was up 9.6% from the year ago comp. GAAP operating margin printed at 4.2%, up from 4.1%.

After accounting for interest, other income/losses and taxes, net income attributable to Walmart shareholders was $5.104B, up 205% (not a misprint) from $1.673B for the comparable period last year. This works out to a GAAP EPS of $0.63 versus just $0.21 for the April 2023 quarter.

Business Unit Performance

- Walmart US generated net sales of $108.7B (+4.6%), as comp sales ex-fuel grew 3.8%, number of transactions grew 3.8% and average ticket size was flat. Operating income grew 7% to $5.3B. Adjusted operating income grew 9.6% to $5.5B.

- Walmart International generated net sales of $28.7B (+12.1%), as net sales in constant currency grew 10.7% to $29.4B. Operating income grew 31.7% to $1.5B. Adjusted operating income grew 27.2% to $1.5B.

- Sam's Club US generated net sales of $21.4B (+4.6%), as net sales ex-fuel grew 5.3% to $18.7B, comp sales ex-fuel grew 4.4%, number of transactions grew 5.4% and average ticket size was down 1%. Operating income grew 34.3% to $0.6B. Adjusted operating income grew 9.6% to $5.5B.

Guidance

For the current quarter, Walmart is guiding net sales towards 3.5% to 4.5% growth, with 3% to 4.5% growth in operating income. The firm sees an adjusted EPS of $0.62 to $0.65. This is in line with the $0.64 that Wall Street had in mind.

For the full year, Walmart sees net sales growth at the high end or above the firm's previous guidance for growth of 3% to 4%. The firm sees adjusted operating income at the high end or above the previously given guidance for growth of 4% to 6%. The firm also sees full year adjusted EPS at the high end or above the original guidance of $2.23 to $2.27.

Fundies

For the period reported, Walmart generated operating cash flow of $4.249B. The firm spent $4.676B on Capital expenditures. This left free cash flow of $-427M. Hmm... In addition to that, the firm repurchased $1.059B in common stock and dished out $1.671B in cash dividends to shareholders. That's pretty imbalanced.

To put that in perspective, Walmart drove free cash flow of $15B+ for the calendar year ending January 2024, almost $12B for the calendar year ending January 2023, $11B+ for the calendar year ended January 2022, and almost $26B for the calendar year ended 2021, so the cash does tend to flow freely over the course of a full year, but there have been negative quarters sprinkled in throughout.

Looking at the balance sheet, which has been a fairly constant weakness for this firm as well as for others in this business, Walmart ended the quarter with a cash position of $9.405B and inventories of $55.382B. This puts current assets at $77.152B. Current liabilities add up to $96.1B including shorter-term debt of $7.322B. We can let the quick ratio slide with a large retailer like Walmart and we should. However, the current ratio of 0.80 is rather ugly, and is very difficult to overlook. So, is the shorter-term debt load that is 78% of the cash position.

Total assets amount to $254.054B, including goodwill of $27.999B. At 11% of total assets, this is not an issue. Total liabilities less equity comes to $165.981B. This includes another $35.928B in debt labeled as long-term. Not the prettiest balance sheet by a long shot. I will say this, the long-term debt-load is down 5.8% over the past twelve months.

My Thoughts

Not enough analysts have chimed in just yet, so we cannot do a "Wall Street" section. Guess I'll go first. Walmart had an excellent quarter. They are still champion to struggling consumers and there is a good chance that the conditions that require such a champion will not only continue on but could exacerbate going forward.

The guidance provided for the full year is excellent as well. I could harp on the free cash flow a bit, but going over recent years, I see that Q1 was an aberration as long as it's a one-off.

That said, the firm is going to have to get on its horse and better manage that free cash flow. It may have made sense to borrow at ultra-low interest rates and use that money to buy back stock and pay dividends. At these interest rates, that kind of activity is going to be a "no-go."

Walmart is going to have to both beef up its cash position and pay off much of its short-term debt without adding too much to its long-term debt through refinancing. Otherwise, it is clear that Walmart is running a tight ship. The balance sheet is what makes it so difficult to invest in his name, even as I root for them. I am a fan.

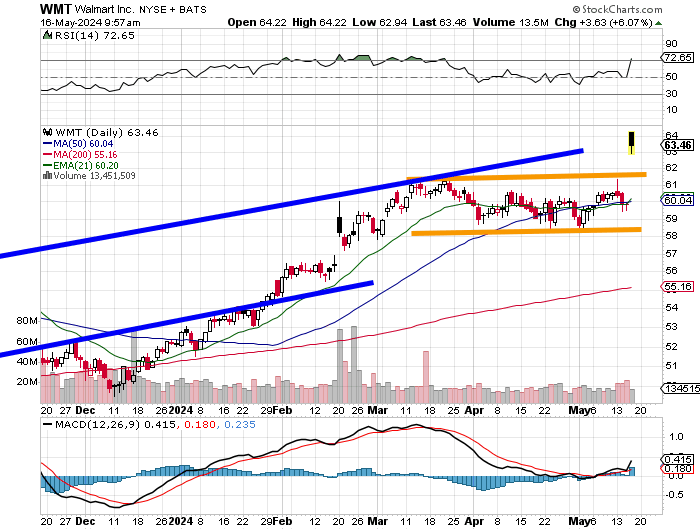

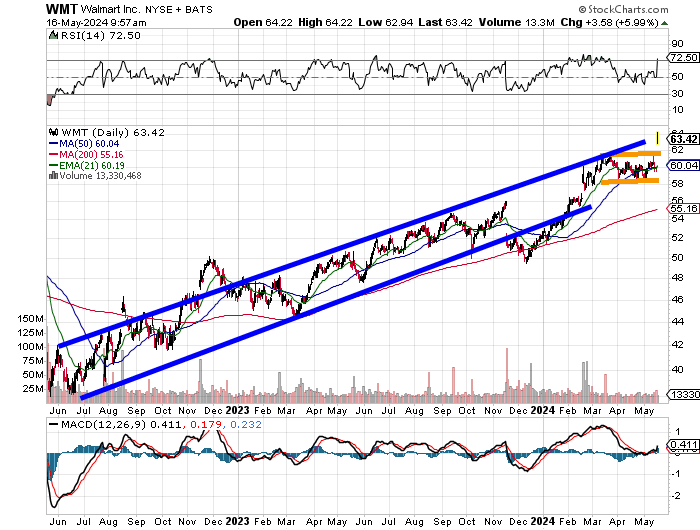

This morning, we see WMT breaking out of a flat base of consolidation with a $61 pivot. Relative Strength is suddenly greatly improved, while the daily MACD (moving average convergence divergence) has gone from "meh" to bullish in a few hours. We have to zoom out for me to show you more...

Thursday's morning pop puts WMT back on trend, a trend that has been in place for two years. The stock with a $63 handle is closing in on what should be a rising trendline of resistance. I, personally, though I like Walmart, would not initiate a long position this morning.

I think WMT is a short-term short for a trade and I may go that route. Longer-term, as long as the firm heeds my words, this is an investment. Should they fail to tackle the current state of the balance sheet through better cash flow management, then no, I cannot get long the name for an investment.

At the time of publication, Stephen Guilfoyle had no position in the securities mentioned.