Super Micro Computer Isn't So Super After All: Buy the Dip?

For those of you who bought the stock ahead of the secondary offering, don't you feel special?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

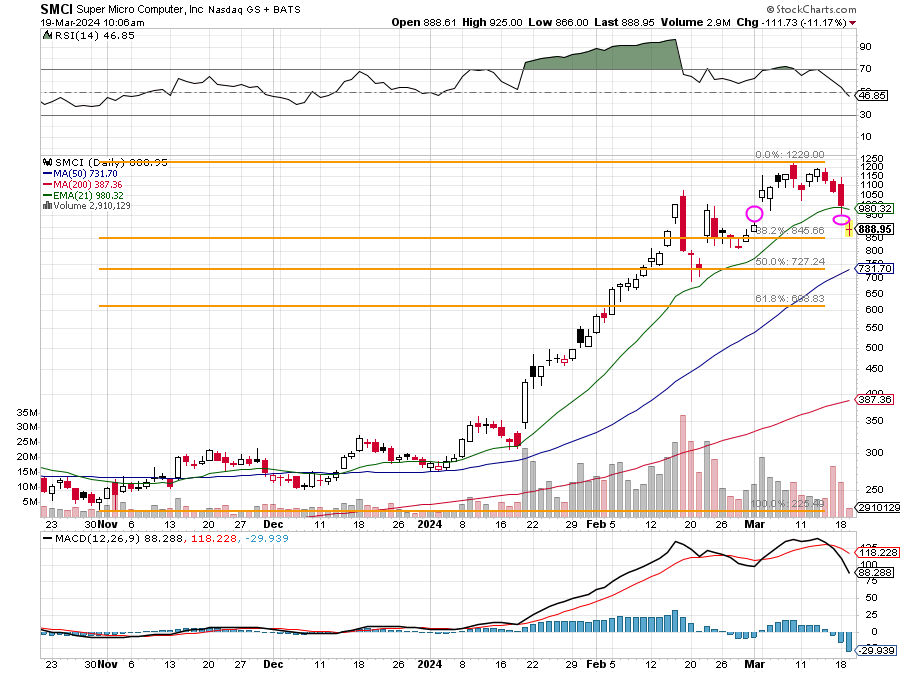

Super Micro Computer SMCI closed at $311.44 on January 18. The stock traded as high as $1,229 on March 8. That was a run of roughly 295% over the prior nearly seven weeks.

The stock was headed into the S&P 500. Party on, Garth. The stock would trade sideways to lower going into its March 18 (yesterday morning) admittance to the S&P 500, forcing a certain level of mandated capital to follow into the name that had not been forced to before.

What could possibly go wrong? Except, the stock gave up 6.4% on Monday to close at $1,000.68. As the opening bell has now rung on Tuesday morning, I see SMCI trading with an $880 handle, and was down another 12.3% overnight.

What gives?

Secondary Offering

On Tuesday morning, Super Micro Computer announced plans for a proposed underwritten registered public offering of $2M of common stock. Obviously, the firm had made a decision to allow for a piling in of public funds in anticipation of the stock's inclusion in the S&P 500 and had intended to announce the intent to raise a nice chunk of cash through a secondary offering of it's stock after having taken all of your money.

For those of you who bought the stock ahead of the event, don't you feel special? Don't you feel valued by the firm as an investor? That was a pretty brazen pick-off play. The old hidden ball trick?

The underwriter, Goldman Sachs GS will be granted a 30-day option to purchase up to an additional 300K shares. The proposed offering is subject to market conditions and there can be no assurance that the offering will even be completed. Maybe when they see how this news has hit the stock, management will shelf the registration for a while or piece it out over time.

Just an FYI, SMCI runs with 55.93M shares outstanding and a float of $447.54M shares, so this offering, if completed, would dilute the equity by 3.6% and increase the float by 4.2%, so it is enough shares added to leave a nasty mark. Oh, and this new offering comes just about a month after a $1.5B convertible senior note offering by the very same company.

Earnings

Super Micro Computer is set to report fiscal third quarter financial results in about a month. Estimates are for an adjusted EPS of $5.70 on revenue of about $3.9B. That would compare to $1.63 on revenue of $1.3B for the year ago comps.

Of the 10 analysts that I know of that follow this name, all 10 have increased their estimates since the start of the quarter. Sounds good, right? Check this out...

Fundamentals

Despite being profitable, the firm has generated operating cash flow over the trailing twelve months of -$135.7M. Tacking on Capex spending of $33.5M, and free cash flow over the past year comes to -$169.2M. Looking at the balance sheet, the firm ended the most recent quarter reported with a cash position of $725.8M and current assets of $4.842B, including inventories of $2.467B.

Current liabilities added up to $1.992B, including unearned revenue of $193.3M. This leaves the firm with a current ratio of 2.43 and a quick ratio of 1.18, both pass muster. The current ratio is very strong.

Total assets amounted to $5.405B including no entry for goodwill, which we appreciate. Total liabilities less equity came to $3.077B with just $99.3M in long term debt but remember that the firm did just lay out $1.5B in convertible notes last month so this is obviously dated, and the balance sheet is obviously not quite as strong as it was back in December.

The Future of AI?

Maybe? Buy on the dip? This is one heck of a dip.

Let's look at the chart:

Suddenly, relative strength is relatively neutral. Suddenly the daily MACD (moving average convergence divergence) is relatively bearish. The good news is that the gap created in early March has been filled.

Now there's an upside gap from this morning's action that will need a trade at $952 or higher to fill. The stock may get some help today from our favorite twelfth century mathematician if the 31.8% retracement level of the November through March rally holds. If not, it will be cross your fingers and cross your toes that the 50-day SMA (simple moving average) and "half-way" back point that are generally in the same neighborhood can mount a defense of the stock.

The $730 puts expire on April 19, after earnings are trading for about $30. That sure is tempting for a sale. This is one of those names where it would be crazy to sell naked puts, though, so a prudent trader would have to buy puts with lower strikes expiring the same day, which depending on how much risk one is willing to bear, could knock off more than two-thirds of that premium paid in net terms.

At the time of publication, Stephen Guilfoyle had no position in the securities mentioned.