SoFi at a Discount? I'm a Believer and Welcome the Opportunity

I'm not sitting on my hands with the stock trading at attractive levels.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

A long-time Sarge favorite went to the tape with its first-quarter financial results on Monday morning.

SoFi Technologies SOFI posted GAAP earnings per share of $0.02 on revenue of $644.995M for the three-month period ended March 31. While the earnings print beat Wall Street expectations by a penny, the revenue number was good for year-over-year growth of 37%.

SoFi also reported $59.2M in gains made on the extinguishment of debt. With that in mind and omitted along with about $5M in servicing rights that were not repeatable, the company also reported "adjusted" net revenue of $580.648M. This number still beat Street expectations and was still good enough for growth of 26.2%.

On the expense side, product development costs increased about 11%, as marketing expenses decreased almost 5%. Additionally, costs of operations grew 19%, while administrative costs rose almost 18%. Provisions for credit losses were actually down from the year-ago quarter.

After accounting for interest and taxes, net income crossed the tape at $88.043M, up from -$34.422M for the year-ago comparison. That resulted in EPS of $0.08 (basis) and $0.02 (once diluted) versus -$0.05 last year.

CEO Anthony Noto

CEO Anthony Noto commented in the press release “Our first quarter was an exceptionally strong start to 2024, demonstrating significant momentum as we responsibly grow revenue and diversify toward our Financial Services and Tech Platform segments, sustain profitability, reinforce our balance sheet, and grow our member base."

Segment Performance

Lending: Generated net interest income of $255.536M (+33%) and noninterest income of $63.94M (-53%). In aggregate, the segment posted revenue of $330.476M (-2%). For the quarter, segment contribution profit was $207.7M, -1% from the year-ago comp.

Technology Platform: Generated net interest income of $501K (up from zero) and noninterest income of $93.865M (+21%). In aggregate, the segment posted revenue of $94.624M (+21%). For the quarter, segment contribution profit was $30.742M, +107% from the year-ago comp.

Financial Services: Generated net interest income of $119.713M (+106%) and noninterest income of $30.838M (+34%). In aggregate, the segment posted revenue of $150.551M (+86%). For the quarter, segment contribution profit was $37.174M, up from the year ago comp of $-24.235M.

Guidance

SoFi informed that 2024 is expected to be a transitional year, as the Tech and Financial Services segments combined are seen driving growth and increasing from an aggregate 38% share of adjusted net revenue to something more like 50%.

For the full year, SoFi is now lifting net revenue guidance to $2.39B-$2.43B from $2.365B-$2.405B. Wall Street had been looking for $2.37B, so this was solid guidance.

Tech is seen growing 20%, while Financial Services is seen growing 75%. Additionally, the company increased its expectation for adjusted EBITDA to $590M-$600M from $580M-$590M.

Full-year net income is now seen at $165M-$175M, way up from prior guidance of $95M-$105M as full-year GAAP EPS guidance slides up to $0.08 $0.09 from $0.07-$0.08. The Street was at $0.08 coming in.

For the current quarter, SoFi now sees adjusted net revenues of $555M-$565M, which was a little shy of the $580M the Street had in mind. SoFi also sees adjusted EBITDA of $115M-$125M and net income of $5M-1$10M for the second quarter.

My Thoughts

A couple things are clear to me.

SoFi Technologies is a very well-run online bank/financial services company that seems to be steadily growing and doing so quite efficiently. The growth seems to be happening in the more desirable parts of the business.

The leadership at the CEO level is in my book, top notch. While the Q2 guidance is admittedly a little soft, the full-year guidance is excellent.

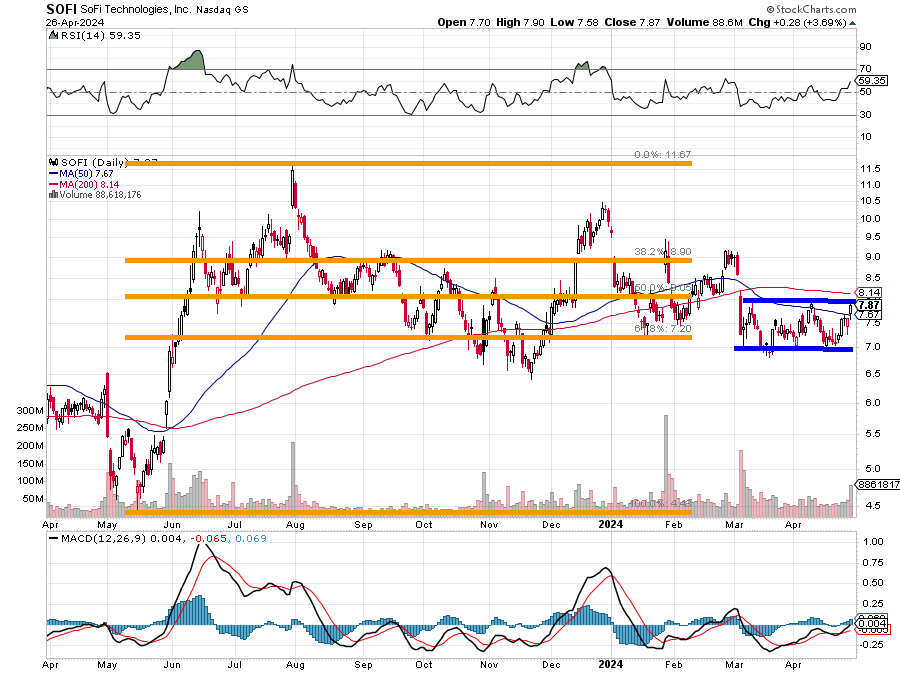

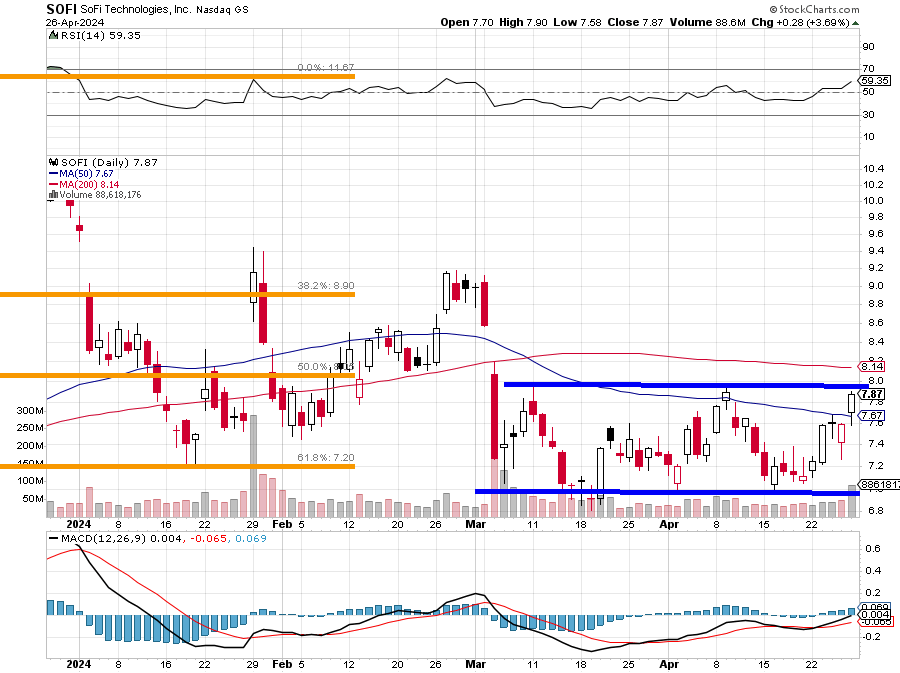

Readers will see that over the past two months or so, SOFI has developed a base of consolidation with a floor of roughly $7 and a ceiling of approximately $9. On the above chart, you can see that support for this base appeared close to a 38.2% Fibonacci retracement of the stock's May 2023 through August 2023 rally.

Let's zoom in on the right:

The stock has been wildly volatile Monday morning. Things had been looking up coming in with the 50-day simple moving average (SMA) having been taken on Friday and both relative strength and the daily Moving Average Convergence Divergence (MACD) appearing to be in better shape. At last glance, I see the stock trading around $7.10. The 50-day line stands at $7.67. The loss of this line could impact the stock significantly.

As many readers know, I am long this stock, and I would welcome the chance to get longer, as I believe in the concept, and I believe in Anthony Noto. SOFI is my seventh largest position.

I will not act in haste Monday. If the 50-day line is lost, and the stock comes in, I will be adding this afternoon at a discount. Should that line hold during the regular session, I will likely be adding on momentum.

I don't expect to sit on my hands.

At the time of publication, Guilfoyle was long SOFI equity.