Here's a Small-Cap Defense Name With Two-Way Potential

This aerospace and defense firm might offer a way to trade in a tough environment.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Looking for a small-cap aerospace/defense name with two-way potential? Look no further. I present Triumph Group TGI.

Who the heck are these guys? Triumph is a Radnor, Pennsylvania operation that designs, engineers, manufactures, repairs and overhauls a portfolio of aerospace and defense systems, subsystems, components and structures. The firm serves the global aviation industry to include both military and commercial operators through the lifecycle of the aircraft involved.

The firm works through two segments: Triumph Systems & Support and Triumph Interiors.

Systems & Support designs, develops and services proprietary parts and systems and produces complex assemblies for commercial, regional and military aircraft. Interiors supplies commercial, regional and military manufacturers with insulation, as well as interior and composite components largely related to environmental control ducting.

Triumph's customers include almost all major airlines, FedEx FDX, United Parcel Systems UPS, Boeing BA, Airbus EADSY, Lockheed Martin LMT, Northrop Grumman NOC, GE Aerospace GE, Rolls-Royce RYCEY, the Pratt & Whitney unit of RTX RTX and Honeywell HON.

Last Week

Triumph Group was downgraded two levels to "underperform," which we consider to be a sell-equivalent, from "buy" at Bank of America by Ronald Epstein who took his target price down to $12 from $17. Epstein is rated at five stars (out of five) by TipRanks and is considered a top-3% analyst at that service.

Epstein wrote, "Triumph is ramping production, and that inventory is being accepted by Boeing and Airbus (for now). However, we are concerned any further production cuts could lead to destocking."

Boeing has halted production of several models due to a labor strike. Airbus has been dealing with sporadic supply chain issues. Triumph was also downgraded by five-star analysts at JP Morgan and Truist Financial back in August.

Earnings and Fundamentals

Triumph is expected to report in about five weeks. Currently, Wall Street is looking for an adjusted EPS of $0.01 on revenue of $283 million. That would compare to an adjusted EPS of $-0.05 for the year-ago comp on revenue "growth" of -20%. Of the nine analysts who cover this name, all nine have reduced their estimates since the quarter began.

As of June, over the trailing 12 months, Triumph has "generated" an operating cash flow of $-31.4 million and free cash flow of $-55 million. Obviously the firm does not return cash to shareholders.

Moving on to the balance sheet, as of the end of June, the firm had a cash position of $152.6 million, and inventories of $358.7 million. That made for current assets of $749.8 million. Current liabilities added up to $303.2 million, which included no short-term debt. This puts the firm's current and quick ratios at 2.47 and 1.29, respectively. That's pretty darned decent. In fact, it's better than decent.

Total assets amount to $1.493 billion, which includes $573.5 million in goodwill and other intangibles. At 38% of total assets, that's on the high side, but not quite the end of the world. Total liabilities come to $1.612 billion, including long-term debt of $947 million. That's a bit much in my opinion for a firm with $152.6 million in cash and negative cash flow.

My Thoughts

The business has real potential. Of course, having Boeing for a customer makes for an uncertain future. The current situation clears the firm for the next 12 months, but long-term, unless those cash flows can be reversed, this firm will run into an unpleasant situation. The best hope for the bulls right now might be a short squeeze. I see that roughly 11.5% of the float is held in short positions. While that is enough to cause a squeeze, I don't feel that it is enough to sustain a squeeze.

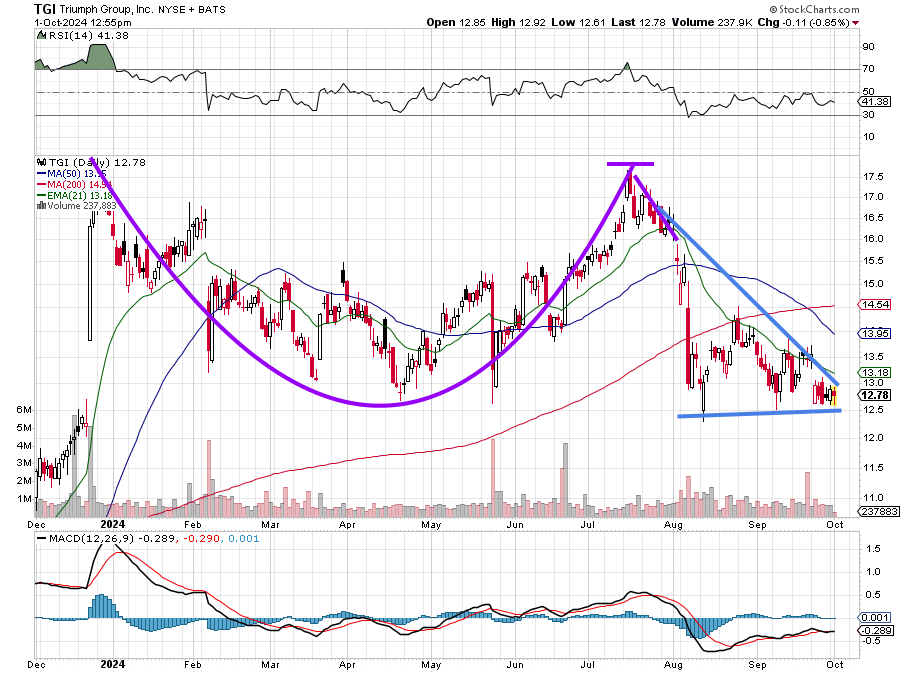

Readers will see the eight-month long cup that added a handle that then failed to produce an upside move. What became of that handle is that it developed into a descending triangle, which is a bearish pattern. Relative strength is on the weak side of neutral, while the daily MACD is postured rather bearishly. The stock also suffered a "death cross" in late September.

This name appears to me to be a candidate for a short position. We already spoke about the short interest. Rather than short the equity, if I were to get involved here, I would rather go out to the January 17 expiration and purchase $12.50 puts for about $1.15, meaning the stock would have to trade below $11.35 by January 17 for this options position to be profitable once exercised.

Note that the options market for this name is rather thin. A trader may have to wait a while to get his or her price on those puts. A market order will likely end up in a poor execution.

At the time of publication, Guilfoyle was long LMT, NOC, GE and RTX equity.