I'm Shorting Olive Garden's Parent Amid Weak Fundamentals

Darden Restaurants released its latest financial results and I cannot see myself investing in the corporation.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Thursday morning, Darden Restaurants DRI released the firm's fiscal first quarter (2025) financial results. For the three-month period ended August 25, 2024, Darden posted a GAAP EPS of $1.74 on revenue of $2.757 billion. The bottom-line print fell about a dime short of Wall Street's expectations, while the top-line print narrowly missed consensus view. That sales print was, however, good enough for year-over-year growth of 1.1%.

While total sales increased 1.1% driven by 42 new restaurants, company-wide same-store comp sales decreased 1.1%. Same-store sales cross the firm's segments/brands are as follows:

- Olive Garden -2.9%

- LongHorn Steakhouse +3.7%

- Fine Dining -6%

- Other -1.8%

The firm also owns three fine dining brands, The Capital Grille, Eddie V's and Ruth's Chris Steak House. Ruth's Chris is not included in the year-over-year comps and won't be until fiscal Q2 2025, which is the current quarter. Other businesses include Bahama Breeze, Seasons 52, The Capital Burger, Yard House and Cheddar's Scratch Kitchen.

Operations

As sales grew 1.1% to $2.757 billion, all costs and expenses to include the cost of sales and operating expenses increased slightly to $2.488 billion. This left an operating income of $269.2 million (+6.4%) as operating margin improved from 9.3% to 9.8%. After accounting for interest, taxes and losses from discontinued operations, net earnings printed at $207.2 million (+6.6%). This worked out to a GAAP EPS of $1.74 per diluted share.

Segment/Brand Performance

- Olive Garden generated sales of $1.209 billion (-1.5%), producing segment profit of $249 million (-5.1%)

- LongHorn Steakhouse generated sales of $713.5 million (+6.5%), producing segment profit of $117.6 million (+8.7%)

- Fine Dining generated sales of $278.9 million (+1.9%), producing segment profit of $37.6 million (-5.3%).

- Other generated sales of $555.5 (-0.6%), producing segment profit of $83.7 million (-0.7%)

CFO/Guidance

CFO Raj Vennam commented in the press release: "The significant step down in traffic during July, led to our first quarter earnings being lower than expected."

Vennam then added, "Following the softness in July, our sales trend has continued to improve. Considering this recovery as well as the planned initiatives to support the remainder of the fiscal year, we are reiterating our guidance for fiscal 2025."

For that reason, the firm is reiterating all aspects of its previously issued full-year guidance for fiscal year 2025. The firm still sees diluted full year, diluted earnings per share of $9.40 to $9.60. Consensus had been for about $9.48, so Wall Street took this reiteration quite well.

Wall Street Also Liked...

The announcement, unrelated to earnings, that Darden had entered into an exclusive multi-year delivery partnership with Uber Technologies UBER to begin as soon as late 2024 with the firm's flagship Olive Garden brand.

Fundamentals

For the quarter reported, Draden generated operating cash flow of $273.2 million. Out of that came capex spending of $145.2 million and purchases of capitalized software of $4.5 million.

This left free cash flow of $123.5 million, up more than $10 million from the year-ago comparison. Out of that number, the firm purchased $172.4 million worth of common stock and paid cash dividends of $166 million to shareholders. I know, that does not exactly add up. The firm does pay a handsome dividend (yield of 3.52%). I would rather the repurchases are pared back, rather than the firm change the dividend at some point.

Turning to the balance sheet, Darden ended the period with a cash position of $192.5 million and inventories of $297.7 million. This put current assets at $819.6 million. Current liabilities add up to $2.325 billion (not a misprint), including short-term debt of $293.9 million, but also unearned revenue of $554.7 million. We know that is not a true financial obligation.

This is a little messy. We won't do a quick ratio, as I don't think we can hold inventories against a restaurant chain. The current ratio, at the headline, is an awful looking 0.35. Even adjusting for those deferred revenues, the current ratio only rises to a still awful looking 0.46. Not pretty.

Total assets amount to $11.356 billion, which includes $1.391 billion in goodwill and $1.148 billion in trademarks. I do not see this as problematic. Total assets less equity comes to $9.212 billion, including long-term debt of $1.386 billion. This balance sheet is a tough one to look at. The current ratio is really sort of atrocious. Short-term debt seriously outweighs cash on hand, meaning the debt will have to be rolled over, likely at higher interest rates.

My Thoughts

The stock is up almost 7% on Thursday morning because the firm did not cut guidance and because they have reached a deal with Uber Eats. Oh boy. That may be an over-reaction.

Just one man's opinion, but the balance sheet is not in good shape. Positive cash flows could correct that problem. The only issue there is that cash flows are not that positive, and the firm spends more cash than it creates on share repurchases and cash dividends. At some point, I would speculate, the repurchases would have to stop and the dividend will have to be reduced. Either that, or the fundamentals remain messy (polite term) indefinitely.

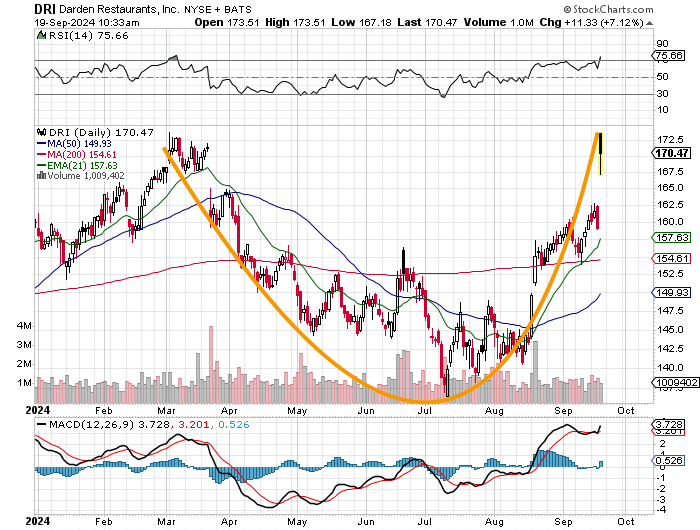

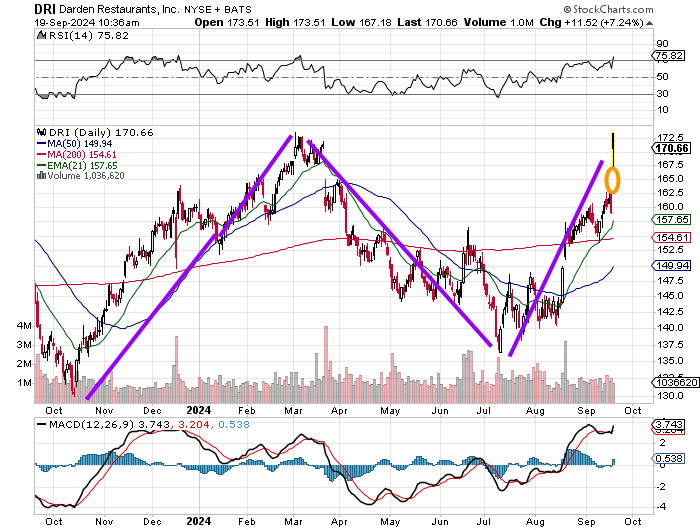

Both the RSI and daily MACD have suddenly become much more bullish looking as the share price has rallied off of its July lows. Cups with handle patterns are generally thought of as bullish, but the stock still has to add a handle. That makes DRI a short-term sell, but a longer-term buy. That is, if that is what you see.

However, if you see the development of a double-top reversal pattern with a $135 pivot, then you would be bearish at these levels. Don't forget, the stock just created a gap that may have to be filled. This is the camp that I am in.

I will be shorting DRI on strength once this article is public information. I cannot see myself investing in a corporation with such weakness in the fundamentals, but I can short such a corporation, especially when only 7% of the float is held in short positions.

At the time of publication, Guilfoyle had no positions in any securities mentioned.