Here's When Rocket Lab Could Be Ready for Launch

This is my plan for the low-priced space name, which is now my second largest position in terms of shares held.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It's been a while since I have updated my view on Sarge favorite Rocket Lab USA RKLB. I last featured this name post-earnings back on May 9. Yes, I am still long RKLB shares. In fact, I am longer as I have purchased more on weakness when possible.

Rocket Lab is not a top-10 or even top-15 allocation for me in terms of weighting, but due to the low share price, is my second largest position in terms of shares held.

Back in early May, Rocket Lab had just reported its first-quarter financial results. Earlier that week, for that quarter, the company had posted a GAAP loss of $0.09 per share on revenue of $92.767 million. The bottom-line print beat Wall Street consensus by a penny, while that top line number fell just a smidge short of expectations. Oh, and that top-line number was also good for year-over-year growth of 69%.

At that time, for the second quarter, Rocket Lab projected revenue of $105 million to $110 million, which at the midpoint, was above what Wall Street had been looking for. That would also reflect annual growth of roughly 74%. The company saw GAAP gross margin between 24% and 26%, and GAAP operating expenses of between $74 million and $76 million. Interest income was expected for the quarter to reach $1 million, while it foresaw an adjusted EBITDA loss of $23 million to $25 million.

With about five weeks to go until Rocket Lab releases its Q2 financial results, Wall Street expectations are for a GAAP loss of $0.10 per share (adjusted up to -$0.07) on revenue of about $107 million. This would be within the company's guidance offered in early May and very close to the midpoint of that range.

News in June

-- June 11... The U.S. Department of Commerce signed a non-binding preliminary memorandum of terms with Rocket Lab to receive up top $23.9 million in direct funding under the CHIPs and Science Act. The proposed investment would enable Rocket Lab to increase its production of compound semiconductors for satellites as part of a modernization of its facilities in Albuquerque, New Mexico. The hope is that Rocket Lab, which is one of only two U.S. companies specializing in space-grade solar cells requiring these compound semiconductors might be able to ramp production by 50% over three years.

-- Rocket Lab signed the largest Electron launch agreement in its history. The deal is for 10 launches with Japanese Earth observation company Synaspective. The agreement was made in Tokyo and attended by Rocket Lab CEO Peter Beck, Synaspective CEO Dr. Motoyuki Arai and New Zealand Prime Minister Christopher Luxon. Rocket Lab has extensive facilities in New Zealand and would likely launch from that location for this project.

Fundamentals

Just a reminder, Rocket Lab is still burning cash. Operating and free cash flows remain negative. Over the 12 months ending with the March quarter, the company generated operating cash flow of -$76.1 million and free cash flow of -$137.3 million. This is why it's a good thing that Rocket Lab has a strong balance sheet.

As of March 31, Rocket Lab had a cash position of $492.522 million and inventories of $99.901 million. This left it with current assets of $725.623 million. Current liabilities then added up to $232.462 million, including short-term debt of $10.996 million. Those numbers put its current ratio at a very healthy 3.12, and the quick ratio at a still strong 2.69.

Total assets amounted to $1.182 billion including $137.865 million worth of "goodwill" and other intangibles. At less than 12% of total assets, I did not consider this to be a problem. Total liabilities less equity came to $702.978 million, including $396.546 million in long-term debt.

This is a very strong balance sheet, as that debt-load could be paid off completely out of cash if need be. There is a catch, though. Most of that debt... $343.829 million, is in the form of convertible senior notes, so the company is at risk, if the stock price rises steadily, of some further dilution. These notes, for the most part, come due in 2029, and run with a conversion price of approximately $5.13 per share of common stock.

Wall Street

In June, two five-star rated (at TipRanks) analysts opined on Rocket Lab USA.

On June 11, in response to that news, Erik Rasmussen of Stifel Nicolaus reiterated both his "buy" rating and $9 price target for the shares, adding that in addition to the memorandum of terms with Commerce, that "The State of New Mexico has also committed $25.5M of additional incentives to help drive modernization and expansion of its manufacturing capacity of space-grade solar cells."

Then on June 18th, in response to that deal, Sujeeva De Silva of Roth MKM reiterated his "buy" rating on RKLB and his $7 target.

My Thoughts

The stock is down a chunk Monday. I haven't found the news as of yet if there is some.

It's still well above my net basis ($3.98), but I must consider opportunities like these when they arise as publicly traded space names don't grow on trees, and I already have the aerospace/defense industry well covered.

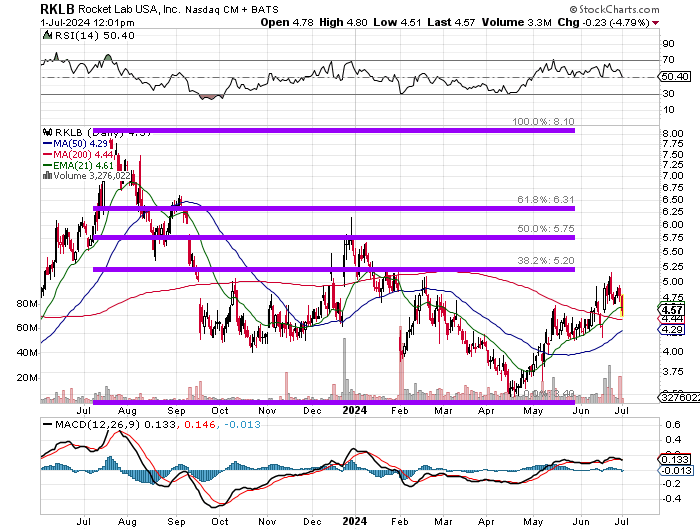

Readers will note that RKLB recovered nicely coming off of that mid-April low. That is until the shares hit the 38.2% Fibonacci retracement level of the July 2023 through April 2024 selloff.

Currently, Relative Strength is neutral, as for the most part is the daily Moving Average Convergence Divergence (MACD). However, the 50-day simple moving average (SMA) is rising and rapidly gaining on the 200-day SMA. This will create what we call a "golden cross" and could produce a positive algorithmic reaction.

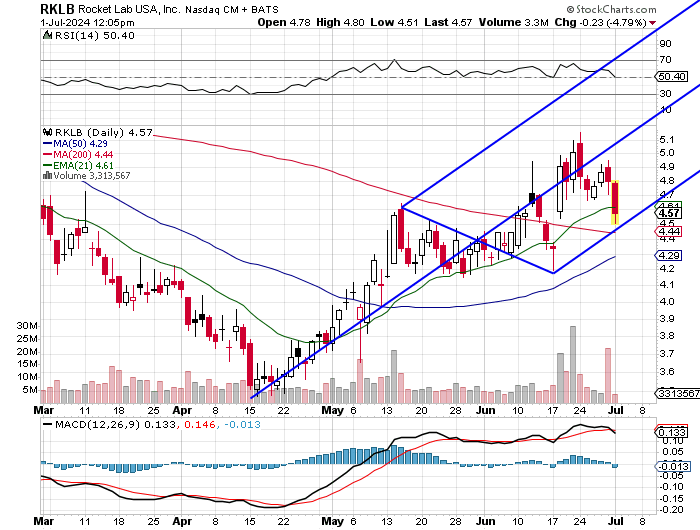

Let's take a different look:

Readers will see that RKLB has developed a "launching pad" for the stock that now fits neatly into this upward facing Andrews' Pitchfork model. The lower trendline could be tested soon and could also be running with the 50-day SMA when contact is made.

My Plan

Price Target: $7

Pivot: $5.16 (central trendline/high of June)

Add: Down to 50-day SMA (currently $4.29)

Panic: Break of June low ($4.20)

At the time of publication, Guilfoyle was long RKLB equity.