Peloton Has Popped, But it Faces a Big Problem

Peloton's convertible notes could eventually dilute its equity, but is there a trade to be made in the meantime?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

A little more than a week ago, I wrote to you and laid out my thoughts on Peloton Interactive PTON ahead of earnings. I mentioned that the stock was starting to move higher because the name had shown up on DME Capital's Form 13-F. Well known hedge fund veteran David Einhorn is the name behind DME Capital, and that fund had apparently acquired 6.8 million shares of the stock during the second quarter of this year. As of June 30, 2024, DME Capital was one of Peloton Interactive's 15 largest shareholders.

Regular readers might recall that I wrote that I did not think chasing the stock was a good idea and that I might consider the shares at a price closer to $2.90 for a trade. I did allow that, maybe, just maybe, Einhorn had more of a clue when it comes to Peloton than I did. That certainly turned out to be true.

I also pointed out that 22% of Peloton's float was held in short positions, so that if the shares got going, there could be something of a squeeze. Well, my "down" day never came. The shares had last traded at $3.12 when I submitted last week's piece to our editorial team here at TheStreet Pro. On Thursday, a week exactly after I had written that piece, Peloton reported, and the rest was history. The shares popped for a gain of 35.4%, closing at $4.55. On Friday morning, at least so far, the stock is hanging on to those gains.

The Quarter

For the firm's fiscal fourth quarter, Peloton posted a GAAP EPS of $-0.08 on revenue of $643.6 million. Though still a loss, the bottom-line number beat expectations decisively, while the top-line print reflected year-over-year growth of just 0.2%. That still, however, narrowly beat Wall Street. Within that number, subscription revenue grew 2% to $431.4 million, while connected fitness products revenue decreased by 4% to $212.1 million.

Subscription gross profit grew 4% to $294.4 million on a subscription gross margin of 68.2% up from 67.3%. Connected fitness products gross profit grew to a positive $11.6 million from $-82.6 million on a connected fitness products gross margin of 8.3%, up from -37.5%. Firm-wide gross profit grew 55% to $312 million from $201.1 million on a gross margin of 48.5% (up from 31.3%).

Operating expenses were down 12% to $375.3 million, leaving a net income/loss of $-30.5 million, which was up from the year ago comparison of $-241.8 million. Adjusted EBITDA improved to $70.3 million from $-34.7 million. The firm did post negative free cash flow for the year, but a positive free cash flow of $426 million for the quarter, which was a pleasant surprise for investors.

The Balance Sheet

As of June 30, 2024, Peloton Interactive had a cash balance of $697.6 million and current assets of $1.266 billion. That does include inventories of $329.7 million. While it is difficult to judge the value of those inventories, that number is down 37% from a year ago, so that albatross is showing improvement. Current liabilities add up to $685.2 million. This includes almost no short-term debt and deferred revenue of $163.7 million. At the headline that's a current and quick ratio of 1.85 and 1.37, respectively. Not bad at all. Once adjusted for those deferred revenues, Peloton's current and quick ratios rise to 2.43 and 1.80 in that order. Peloton's current situation is not weak.

Total assets amount to $2.185 billion, which includes very little in the way of goodwill or other intangibles. Total liabilities less equity comes to $2.704 billion, including $950.1 million in normal long-term debt, and another $540 million in convertible senior notes. That's a problem. Maybe not yet, but a problem at some point. Free cash flow is not yet great enough to pay off a significant portion of this debt and the convertible notes could, if the stock gained some upside traction, wind up diluting the equity.

Guidance

For the current quarter, Peloton projects revenue of $560 million to $580 million, with Wall Street looking for something close to $605 million. Gross margin is seen at 50%. Paid connected fitness subscribers are seen at 2.88 million to 2.89 million, while paid app subscribers are seen at 560,000 to 570,000. At the midpoints, those numbers would be down 3% and 26%, respectively.

For the full year, total revenue is projected at $2.4 billion to $2.5 billion, with Wall Street looking for something between $2.65 billion and $2.7 billion. Gross margin is seen at 49%. Year-end paid connected fitness subscribers are seen at 2.68 million to 2.75 million, while year-end paid app subscribers are seen at 570,000 to 620,000. At the midpoints this would be "growth" of -9% and -3%, respectively.

Lastly, the firm continues its search for a permanent CEO.

My Thoughts

It's really a shame. The balance sheet has really been managed as well as it could have been. Costs and expenses have been curbed severely. The business just continues to shrink. There is not the demand for online fitness classes and equipment that former management thought there would be. In addition, there is competition for the slice of the at-home fitness pie. The firm can survive for a bit. Perhaps at some point, a larger fitness firm would look to bring Peloton on board? I don't see this as a standalone business forever.

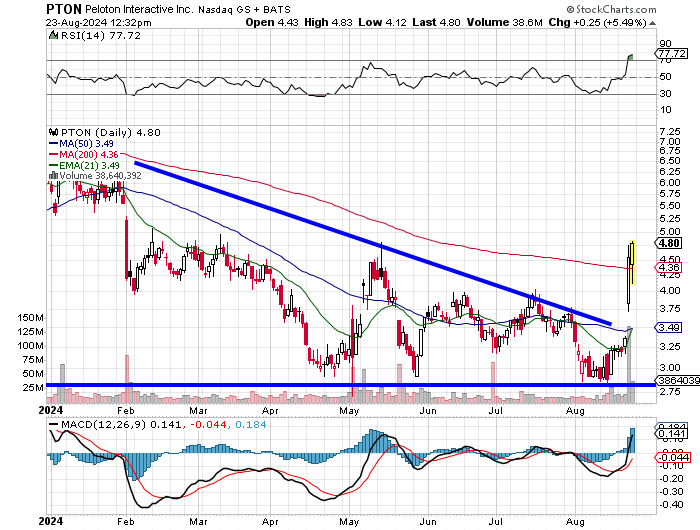

Readers might recognize this chart. It looks like the one that I drew up for you last week, but with a breakout attached. I think there is probably some short covering involved. Do you think the stock stays at $4.80? Me neither. Can it hold the 200-day SMA? I really don't know. Einhorn didn't buy it for no good reason. Will it come back in? If this mini short squeeze is done, it will.

What I am thinking of doing is going out to September 20, 2024 expirations and getting long a $5/$4.50 strangle for a net debit of $0.73 (or so). A stupid waste of money? Maybe. The stock will have to trade above $5.73 or below $3.77 by expiration to be profitable. Then again, we're only spending chump change to begin with.

One could just go out to October 18, 2024 expiration and get long $4 puts for $0.29. That trade would break even at $3.71 on the downside and offers no upside profitability. The stock has moved but will likely move again before too long. Missed the equity trade? There is always more than one way to skin a cat.

At the time of publication, Guilfoyle had no positions in any securities mentioned.