Palo Alto's Results Were Not Great, But Not Discouraging: How to Trade It

There's a lot to like here. Billings was the problem.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

"Best in class" (my opinion) cybersecurity provider Palo Alto Networks PANW released the firm's fiscal first quarter financial results on Wednesday evening.

For the three-month period ended October 31st, Palo Alto posted an adjusted EPS of $1.38 (GAAP EPS: $0.56) on revenue of $1.878B. Revenue generation just edged expectations and was good enough for year over year growth of 20.1%. Bottom line results easily beat Wall Street, adjusted or not. The lion's share of the adjustment that was made was for $287.8M worth of share-based compensation related expenses.

Remaining Performance obligation grew 26% to $10.4B, while billings increased roughly 16% to $2.02B. This billings number fell slightly short of both expectations and the firm's guidance. This along with slightly reduced guidance for billings for the full fiscal year are the primary reasons for the stock market's negative reaction to this release. That said, while not great, I don't see the data on billings as truly discouraging. I added to my long position on overnight weakness for that reason. Let's dig in.

Operations

As revenue grew 20.1%, the cost of that revenue increased 2.4% to $472.8M. That took gross profit up to $1.405B (+27.5%) on a gross margin of 74.8% (up from 70.5%). Operating expenses increased 9.6% to $1.19B, leaving the firm with GAAP operating income of $215.2M (up from $15.2M for the year ago comp). That took GAAP operating margin from 0.9% up to 11.5%. Once adjusted, operating margin hit 28%.

After accounting for interest and taxes, GAAP net income landed at $194.2M, up from $20M, or $0.56 per share. Once adjusted, net income increased 75% to $466.3M or $1.38 per share.

Guidance

This is where it gets a little dicey and I emphasize the word "little." Remember that very few firms get this granular in their guidance and that is to the credit of both CEO Nikesh Arora and CFO Dipak Golechha.

For the current (fiscal second) quarter, Palo Alto sees total billings in a range spanning from $2.335B to $2.385B, which would be good for y/y growth of 15% to 18%. The firm sees quarterly revenue of $1.96B to $1.97B. Wall Street was looking for $1.97B. Adjusted EPS are seen at $1.29 to $1.31, which is well ahead of the $1.25 that Wall Street had in mind.

For the full fiscal year, the firm sees total billings in between $10.7B and $10.8B, which would reflect year over year growth of 16% to 17%. Wall Street was looking for something close to $1.95B here, as the firm had previously guided this metric to a range of $10.9B to $11B. The firm's new guidance on billings runs about 1.8% shy of that guidance as well as Wall Street consensus.

Total revenue is seen at $8.15B to $8.2B, which is in line with prior guidance and would be good for growth of 18% to 19%. For the full year, the firm sees adjusted operating margin of 26% to 26.5% and adjusted EPS of $5.40 to $5.53. That, my friends, is an increase from the previously given range of $5.27 to 5.40 and well above the $5.33 that Wall Street had in mind. The firm also expects adjusted free cash flow margin of 37% to 38%, in line with prior guidance.

Fundamentals

For the quarter reported, Palo Alto generated operating cash flow of $1.526B. Out of that came CapEx spending of $36.8M, leaving free cash flow of $1.489B. The firm does not pay a cash dividend to shareholders and repurchased just $66.7M shares of common stock. Most of the rest moved into the firm's cash position.

Glancing at the balance sheet, Palo Alto ended the period with a cash position of $3.894B (+63% in three months) and current assets of $6.478B. Current liabilities add up to $7.513B, which doesn't look good on the surface until one realizes that of that number... $4.732B is entered as "deferred revenue" which as we know, is not a financial obligation, but one of in this case, services owed. Unadjusted, the firm's current ratio stands at a less than impressive 0.86. However, once adjusted for deferred revenue, the firm's current ratio soars to an absolutely robust 2.33.

Total assets amount to $14.809B including $3.217B in goodwill and other intangibles. At 21.7% of total assets, this is no cause for alarm. Total liabilities less equity comes to $12.638B. That includes another $4.711 in longer-term deferred revenue. What that means is that if deferred revenue is set aside, that total liabilities print of $12.638 becomes just $3.195B. That's impressive. Know what's even more impressive? The firm does have $1.947B worth of convertible senior notes coming due within the next twelve months. Other than that, no debt whatsoever. That's with a cash stash of almost $3.9B.

Wall Street

Since these earnings were released last night, I have come across 17 sell-side analysts that are rated at a minimum of four stars by TipRanks and have also opined on PANW. Among the 17 analysts are 16 "buy" or buy-equivalent ratings and one "neutral" rating, which is a "hold-equivalent." The hold, which was John DiFucci at Guggenheim, did not set a target price. The other 16 did.

Across the 16 "buys", the average target price is now $284.88 with a high of $310 (Ittai Kidron of Oppenheimer) and a low of $260 (Adam Tindle of Raymond James). Once omitting those two as potential outliers, the average target across the other 14 drops just two cents to $284.86.

My Thoughts

There's a lot to like here. Revenue beat. Gross profit beat. Subscriptions beat. Adjusted operating income and margin beat. Free cash flow beat as well. Billings was the problem. CEO Nikesh Arora wasted no time explaining the situation in his opening remarks last night. Arora said:

" The cost of money remained a constant discussion and customers' significant focus on this topic is becoming the new normal. The way it manifests itself in our business is that there's always a payment in duration discussions in final negotiations."

Arora went on...

"We can use a mix of strategies to navigate the environment. This includes annual billing plans, financing through PANFS, and partner financing. Whilst this does not impact our business demand or the impact to annual revenue or annual metrics, it does create variability on total billings more than before depending on financing used or the duration of contracts."

Then, finally....

"I'm not concerned about the demand for cyber security, for this quarter and upcoming quarters, though my concern about our ability to execute, the billings variability is a pure consequence of the payment conversation that we're having with our customers, and this is validated by the fact that we continue to see strong RPO and low churn suggesting this is a cosmetic impact to our business."

If Arora says there's no cause for concern in regard to future demand, then I believe that to probably be true until something impacting future profitability happens. We have not yet seen this. Is the stock too expensive at 48 times forward looking earnings? Perhaps, but CrowdStrike CRWD trades at 72 times and ZscalerZS at 82 times, so PANW is inexpensive relative to the other names that I see as elite in this business.

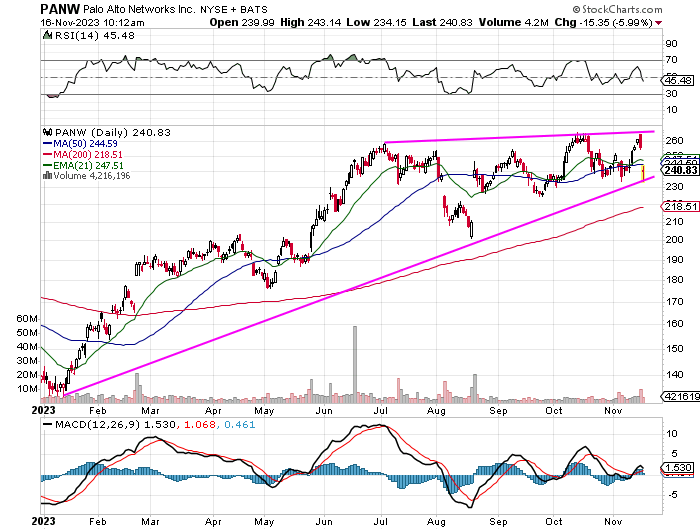

Readers will see here something very close to an ascending triangle. Granted the upper trendline is not flat, but it is close and if that rising lower trendline holds, this can be quite bullish. The stock gave up its 50-day SMA (simple moving average) this morning and needs to take back that line in short order to prevent resistance from settling in.

You know I added overnight. I see two upside pivots. One would be the 50-day line at $244, the second would be a break of the upper trendline. That's around $266 right now. $266 can give us $306. On the other hand, do we panic at the 200-day line or at the lower trendline? I have a cushion here. Even with last night's purchase, my net basis is just $189.51. If the 200-day line fails, I'll give PANW a chance to regroup at that thin red line. That said, lose the 200-day line, you lose me.

At the time of publication, Stephen Guilfoyle was long PANW, CRWD equity.