New Upside Target for Expeditors of Washington as Inside Ownership Rises

The logistics name offers several intriguing advantages for a short-term timeframe.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Here’s my third trading idea for TheStreet Pro readers, drawn from holdings in my Select Equity strategy that I like for shorter-term trader timeframes.

The company is Expeditors of Washington (EXPD), a leading global logistics company that provides integrated freight forwarding, custom brokerage and supply chain solutions. Here is my trade rationale based on the fundamental and technical setup.

Why Expeditors Is Profitable

- Flexibility: EXPD is flexible because it doesn’t own expensive transportation assets, so it can adapt quickly to shipping rate swings, disruptions or demand shifts

- Technological Edge: Internal systems with real-time tracking, compliance and optimization which leads to efficiency

- Diversification: It has a broad customer base across industries and geography which reduces risks

- Efficient Capital Allocation: Consistent cash flow, dividends and high return on capital, often averaging 30% to 40% with stable margins.

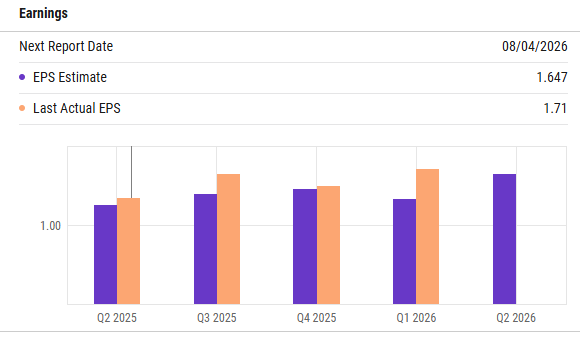

Trend of Beating Earnings and Lower Valuation Multiples

Earnings expectations have been beat fairly consistently. In November 2025, we had a 17.6% surprise. It appears that analysts are a little behind with growth expectations. If you look at the historical multiples evaluation, it averages 12.82% below the average historical valuation multiples.

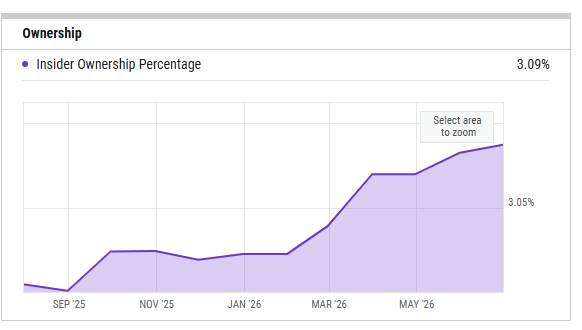

Inside Ownership Percentages Have Been Rising

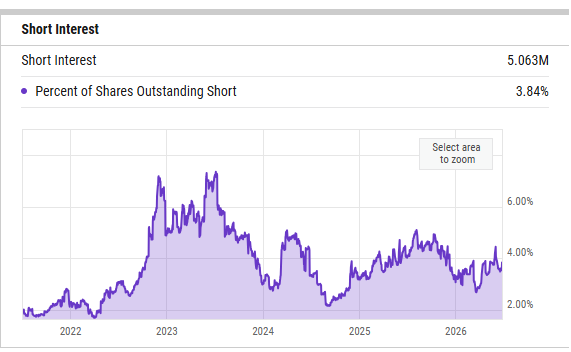

And short interest has been falling from the peak we saw in 2023…

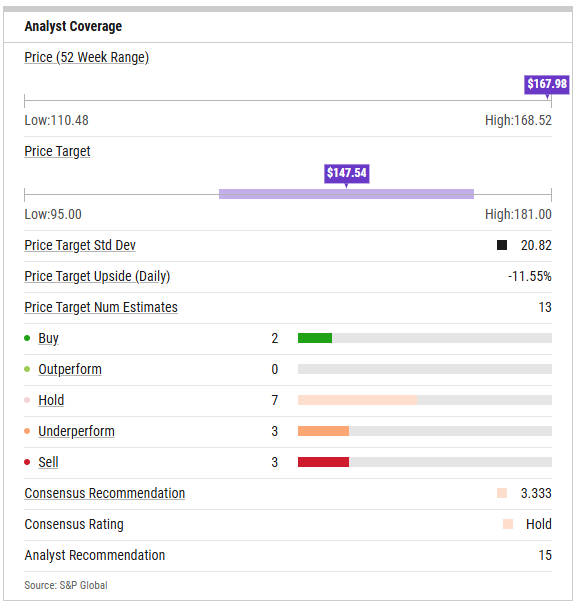

Analyst Views Are Mixed

Analysts ratings appear to be mixed — there’s a couple of buys, seven holds, three underperforms and three sells based on 15 analyst recommendations according to S&P Global. I expect a shift in expectations toward a bullish stance.

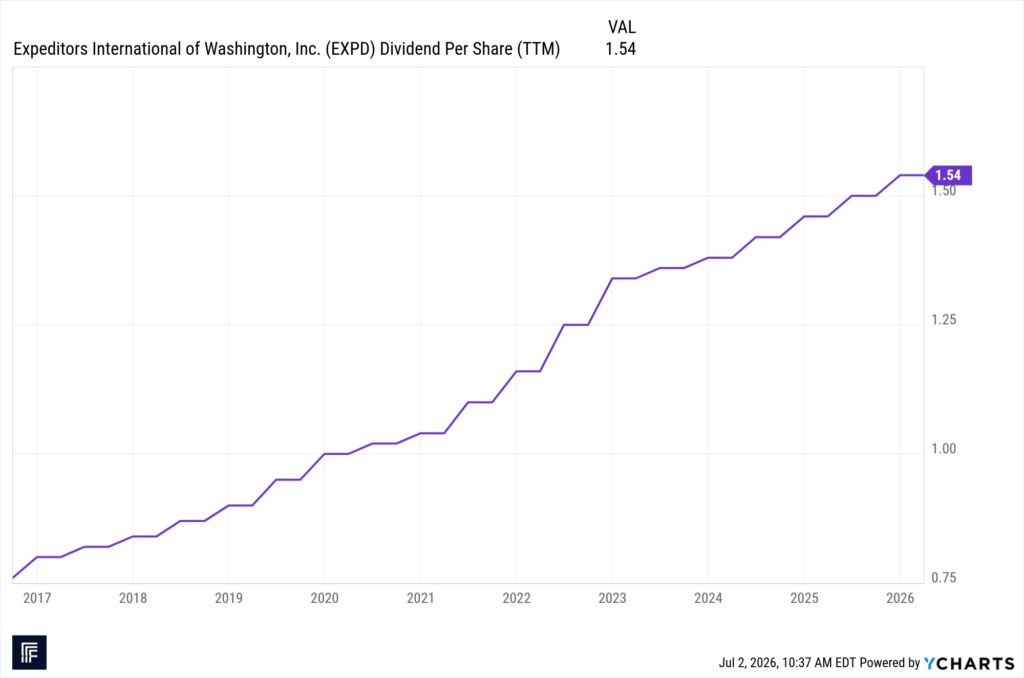

Steady Dividend and Cash Flows Are a Plus

Another good sign is that dividends per share have been steadily rising, initially with an accelerated pace in 2022, but we had consistent raises in dividends year by year. Although the yield is only 0.94%, which is slightly below the S&P 500 yield, their payout ratio is only 24.88% of the earnings, so they appear to be growing rewarding shareholders with dividends.

Promising Chart Pattern and Good Reward-to-Risk Ratio

And, in a market where the price action of many leading tech stocks appear to sluggish, this stock is a standout. The technical chart pattern completed a base and is near the upper end of the range, appearing to be ready to break out and is not extended.

This particular stock has a chart pattern that is conducive to using a measured move forecast of the upside potential. The peak of the base was approximately $167 per share and the low of the base was $129 per share. That’s about a 38-point upside potential from the $167 pivot, giving it an upside target of $205 per share.

The reward-risk ratio is reasonable on this. Place the stop loss below the minor low from the most recent right-hand side of the base, around $158 per share. To leave some room for its average volatility so you don’t get shaken out too quickly, I would subtract another couple of points and set the stop loss at $156 per share.

That’s a pretty decent reward-risk ratio. It’s roughly $11 risk per share and $38 reward per share — a 3.45 reward-to-risk ratio, which is reasonably good for a shorter-term trade.

Let me know your thoughts and happy trading!