New Trade Idea for Dell After Jaw-Dropping Report

On Thursday evening, Dell Technologies ($DELL) released the firm’s fiscal first quarter financial results and, wow, did the firm impress. For the period ended May 1, Dell posted an adjusted EPS of $4.86 (GAAP EPS: $5.24) on revenue of $43.842 billion. These results were quite simply “off the charts,” as the top-line print beat expectations …

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Thursday evening, Dell Technologies (DELL) released the firm’s fiscal first quarter financial results and, wow, did the firm impress.

For the period ended May 1, Dell posted an adjusted EPS of $4.86 (GAAP EPS: $5.24) on revenue of $43.842 billion. These results were quite simply “off the charts,” as the top-line print beat expectations by a rough $8.5 billion and the adjusted bottom-line number beat by almost $2. The GAAP bottom-line number was even juicier. The sales print, by the way, was good for year-over-year growth of 87.5%.

Adjustments were made for a number of items, most notably though, for changes in the fair value of the firm’s equity investments. Think the quarter was incredible? The guidance provided was just as incredible.

COO and vice chair Jeff Clarke commented in the press release:

“Our record Q1 performance reflects strong in-quarter demand, as well as our pace of innovation across the full stack of PCs, compute and storage. We booked $24.4 billion in AI orders and recognized $16.1 billion of AI server revenue. We’re increasing our AI server revenue expectations for FY27 to $60 billion, which only goes to show the AI opportunity shows no signs of slowing.”

Segment Performance

Infrastructure Solutions Group generated net revenue of $29.009 billion (+181%) producing an operating income of $3.055 billion (+206%). Within that group, sales of AI-optimized servers were up 757% to $16.132 billion.

Client Solutions Group generated net revenue of $14.609 billion (+17%) producing an operating income of $1.17 billion (+79%).

Guidance

For the current quarter, Dell sees revenue generation of $44 billion to $45 billion, producing an adjusted EPS of $4.80. Wall Street had been looking for revenue of about $36.6 billion and an adjusted EPS of roughly $2.73. The size of these beats cannot be overstated.

For the full fiscal year, Dell is projecting revenue of $165 billion to $169 billion, which would produce an adjusted EPS of $17.90. Consensus had been for an adjusted EPS of about $13.42 on revenue of slightly less than $145 billion. These beats are enormous.

Fundamentals

For the period reported, Dell generated operating cash flow of $4.081 billion (+46%). Out of this number came Capex spending and software development costs of $963 million. This left free cash flow of $3.118 billion (+40%). Out of that number, the firm repurchased $1.628 billion worth of common stock for its corporate treasury and paid out cash dividends of $464 million to shareholders.

Turning to the balance sheet, Dell ended the quarter with a cash position of $11.578 billion and inventories of $15.052 billion. That puts current assets at $70.607 billion. Current liabilities add up to $74.598 billion including short-term debt of $7.55 billion. On the surface, Dell’s current and quick ratios stand at 0.95 and 0.74. That would not pass muster. However, after adjusting for current deferred revenue of $13.193, those ratios rise to 1.15 and 0.90, respectively. Not great, but enough to get by.

Total assets amount to $114.913B. Goodwill and other intangibles account for less than 21% of that total which is not scary. Total liabilities less equity comes to $116.317B. This includes long-term debt of $23.611B, but also non-current deferred revenues of $14.259B. I don’t love this balance sheet, but the deferred revenue is impressive.

Opinion

The quarter is beyond impressive. So is the guidance. So are the cash flows. The balance sheet, not so much. That said, with cash flow like that, the balance sheet will correct itself. My jaw dropped at this quarter and at the sight of the outlook.

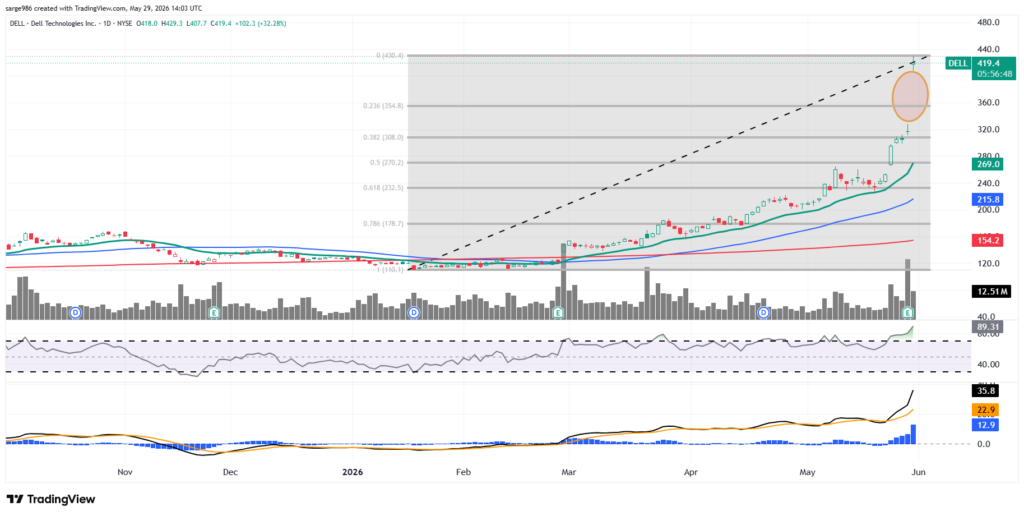

I don’t think that I am that interested in initiating DELL up more than $100 and almost 35% on the day. The gap-up opening is just too large for me. That said, I do see that a 23.6% Fibonacci retracement from Friday morning’s high would put the shares at $355, which gives me an idea. Relative strength and the daily MACD both look to suddenly be technically overbought, though that does not always mean a whole lot in the short term.

Personally, I would rather sell (write) one July 17 $360 put for about $17.25 than purchase 100 shares of DELL equity in the $420s. If shorting a put like that in the raw (naked) gets traders nervous, they can always turn it into a spread and purchase a July 17 $340 put for around $11.75.

At the time of publication, Guilfoyle had no positions in any securities mentioned.