Missing the Target Isn't the Most Alarming Thing Going On Here

There's no respite in sight for Target, as Walmart and Amazon continue their dominance.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Wednesday, Target TGT shares fell by over 21% as both earnings and revenue missed analysts’ forecasts. The Minneapolis-based retailer also forecast weak sales for the holiday season.

For Target shareholders, what is even more alarming than Wednesday’s news is the fact that this stock has been dead money for five years. These stats are damning:

Past month: -19%

Past six months: -22%

Year-to-date: -14%

Past year: -5.8%

Past five years: -4%

We’re all aware of the challenges faced by the retail sector, but this goes deeper. Compare the above stats to those of the SPDR S&P Retail Trust XRT, a bellwether for the retail industry:

Past month: +0.2%

Past six months: +2.1%

Year-to-date: +7%

One year: +21%

Five years: +76%

Here is a chart depicting XRT on the left, representing the overall retail sector, and Target on the right, covering the past year:

Target isn’t just underperforming, it’s getting trounced within its own sector.

Perhaps it’s time for changes at the top? Brian Cornell has served as Chair and CEO for over 10 years. If I were a Target shareholder, I’d be displeased at what could be perceived as a lack of accountability.

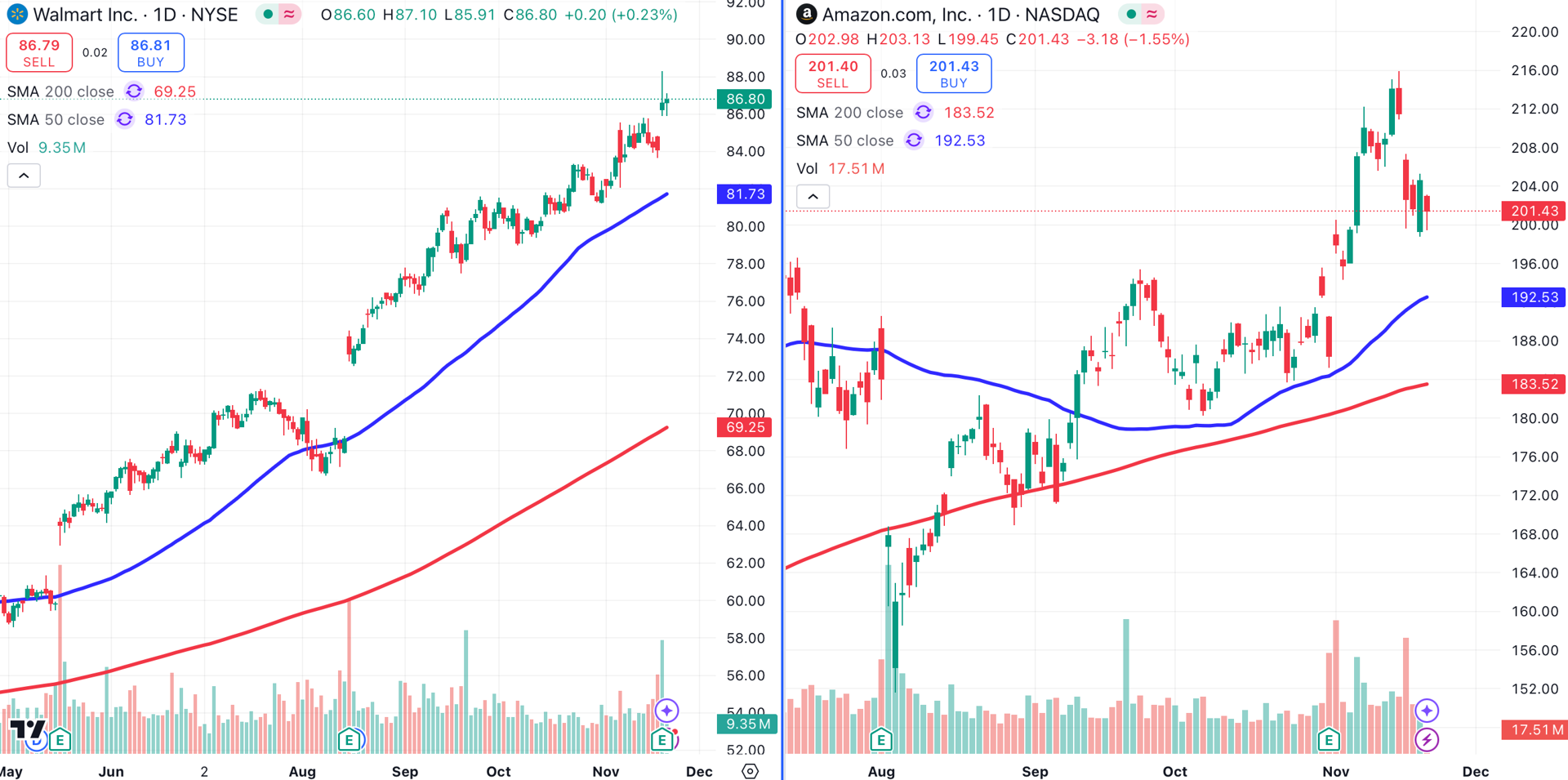

Meanwhile, competitors Walmart WMT and Amazon AMZN both reached all-time highs after reporting earnings earlier this month. Walmart’s chart (left) is particularly impressive.

While Target is sounding the alarm for soft holiday sales, Walmart raised guidance when it reported earnings on Tuesday. Walmart beat earnings expectations by 8.8%, and exceeded revenue projections by 1.1%. Unlike Target, Walmart sees its momentum continuing into the holiday season.

There were many solid metrics within Walmart’s results, but online sales were perhaps the most impressive. In the U.S., sales for Walmart’s e-commerce division popped by 22%, marking the third consecutive quarter of gains in excess of 20%.

Perhaps the biggest complaint about Walmart is the stock’s valuation. The Arkansas-based giant now trades at about 36x its trailing price earnings ratio.

Consider this — Walmart, the world’s biggest retailer, is the world’s second largest online retailer. Walmart now accounts for about 6.4% of all online sales, far behind leader Amazon’s 37%.

Think of Walmart’s online division as a separate company. It’s no mean feat to grow the world’s second largest online retailer at a clip in excess of 20%.

That kind of performance deserves special recognition, and the market is showing respect by granting Walmart a P/E ratio resembling that of a tech stock. Notably, Walmart’s 36 P/E ratio is still below Amazon’s, which is currently just under 43.

At the time of publication, Ponsi was long WMT.