Micron Offers Golden Opportunity to Enter Surging AI Growth

After reporting its third quarter financial results, elite memory chip maker Micron could be at the perfect entry point for traders.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Thursday, elite memory chip maker Micron Technology MU released the firm's fiscal third quarter financial results. For the three-month period ended May 30, 2024, Micron posted an adjusted EPS of $0.62 (GAAP EPS: $0.30) on revenue of $6.811 billion. These top- and bottom-line numbers both beat Wall Street's expectations, while the sales print was good enough for year-over-year growth of 81.5%. The $0.32 per share worth of adjustments all were made for the purposes of share-based compensation expense.

“Robust AI demand and strong execution enabled Micron to drive 17% sequential revenue growth, exceeding our guidance range in fiscal Q3," president and CEO Sanjay Mehrotra said in an accompanying press release. "We are gaining share in high-margin products like High Bandwidth Memory (HBM), and our data center SSD revenue hit a record high, demonstrating the strength of our AI product portfolio across DRAM and NAND. We are excited about the expanding AI-driven opportunities ahead and are well positioned to deliver a substantial revenue record in fiscal 2025.”

Certainly, this has my attention.

Operations

As Micron was driving revenue generation 81.6% higher to $6.811 billion, the cost of goods sold, printed at $4.979 billion (+12.7%), leaving a GAAP gross profit of $1.832 billion, up from the year ago comp of $-668 million. That took GAAP gross margin from -17.8% to +26.9%. The adjusted gross margin improved from -16.1% to +28.1%.

Operating expenses grew 1.8% to $1.113 billion, leaving a GAAP operating income of $719 million, up from $-1.896 billion as GAAP operating margin improved from -46.9% to +10.6%. Once adjusted for share-based compensation — which, in all honesty, a mature company should not be adjusting for (if you do it every quarter for decades, it's ordinary, duh) — operating expenses increased 12.7% to $976 million, leaving an operating income of $941 million, up from $-1.469 billion. Adjusted operating margin improved from -39.2% to +13.8%.

After accounting for interest, taxes and other income/losses, GAAP net income printed at $332 million, up from the year ago comparison of $-1.896 billion, which works out to $0.30 per diluted share. Adjusted, net income improved to $702 million from $-1.565 billion, which ends up looking like $0.62 per diluted share.

Guidance

For the current quarter, Micron guided toward revenue of $7.4 billion to $7.8 billion. At the midpoint, this is slightly above the $7.58 billion or so that Wall Street was looking for. Gross margin is seen at 32.5% to 34.5% GAAP, or 33.5% to 35.5% adjusted. EPS for the quarter is projected at a GAAP $0.53 to $0.69, or an adjusted $1.00 to $1.16. Wall Street was looking for a rough $1.05.

Traders found this in-line to slightly better than in-line guidance disappointing, which was the primary reason for the overnight weakness in the share price. I see this as a quite good outlook. Both revenue and profitability are seen at their midpoints above incoming consensus and the sales expectation would be good for annual growth of roughly 89%. That's impressive, if you ask me.

Fundamentals

For the quarter reported, Micron generated operating cash flow of $2.482 billion (up from $24 million, not a misprint). Out of that came $2.057 billion (+49.2%) in capital expenditures, leaving free cash flow of $425 million (up from $-1.355 billion). The firm did not repurchase any shares of common stock during the quarter, while paying out $384 million in cash dividends to shareholders. This shows the kind of discipline in cash flow management that we fundamental analysts crave seeing, by the way. On top of that, the firm paid off $1.816 billion in debt mostly out of cash, which is truly impressive.

Looking at the balance sheet, Micron had a cash position of $8.379 billion on the books along with $8.512 billion in inventories. That took current assets up to $23.319 billion (+9% over nine months) thanks to dramatic growth in accounts receivable. Current liabilities add up to $6.84 billion, which is mostly accounts payable. There is only a negligible amount of short-term debt. This puts the firm's current ratio at a more than muscular 3.41. Even sans inventories, the quick ratio of 2.16 is beyond healthy.

Total assets amount to $66.255 billion, which includes just $1.563 billion in goodwill and other intangibles. Total liabilities less equity comes to $22.03 billion. This does include $12.86 billion in long-term debt. If not for the size of that debt-load, this would be a fortress-like balance sheet. The firm sees that and is obviously addressing that. As is, this balance sheet is in good shape. Short-term, it's in outstanding shape.

Wall Street

It appears that Wall Street likes this release and I'm pretty sure that I do, too. Since these earnings hit the tape last night, I have come across 14 sell-side analysts that are both highly-rated (four-plus stars out of five) at TipRanks and have opined on MU. After allowing for changes, all 14 of these analysts rate MU at a "buy" or their firm's buy-equivalent rating.

The average target price across these 14 analysts is $161.29 with a high of $190 (Aaron Rakers of Wells Fargo) and a low of $13 (Toshiya Hari of Goldman Sachs). Once omitting those two as potential outliers, the average target across the remaining 12 analysts drops to $160.83.

During the Call...

Again, I quote Mehrotra. During his opening remarks last night, the CEO said, "Most data center customer inventories have normalized, and demand from customers continues to strengthen. PC and smartphone customers have built additional inventories due to the rising price trajectory, the anticipated growth in AI PCs and AI smartphones, as well as the expectation of tight supply as an increasing portion of DRAM and NAND output is dedicated to meeting growing data center demand. Due to expectations for continued leading-edge node tightness, we are seeing increased interest from many customers across market segments to secure 2025 long-term agreements ahead of their typical schedule."

That really says it all.

My Thoughts

The quarter was better than great. Balance sheet and cash flow management is impressive and shows discipline. The guidance is solid. The CEO is not only confident, but he is also talking about long-term agreements through 2025 with his clientele. Oh, and without memory, there is no AI, there are no AI-infrastructure providers like Nvidia NVDA, and there are no AI software developers and cloud providers like mega-cap tech.

Who competes with Micron? Western Digital WDC? Not much competition there. Seagate Technology STX? Even less there. Micron has a chance to build as much of a lead and as much of a moat in AI memory as Nvidia has built in AI-capable GPUs. Rock on.

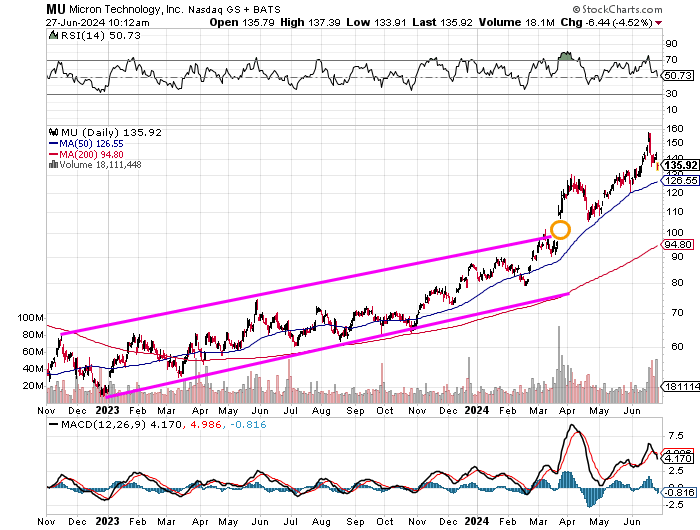

Readers will see that MU ran in a tight, ascending price channel from late 2022 through April 2024 when the stock broke out to the upside. Let's take a look at that breakout:

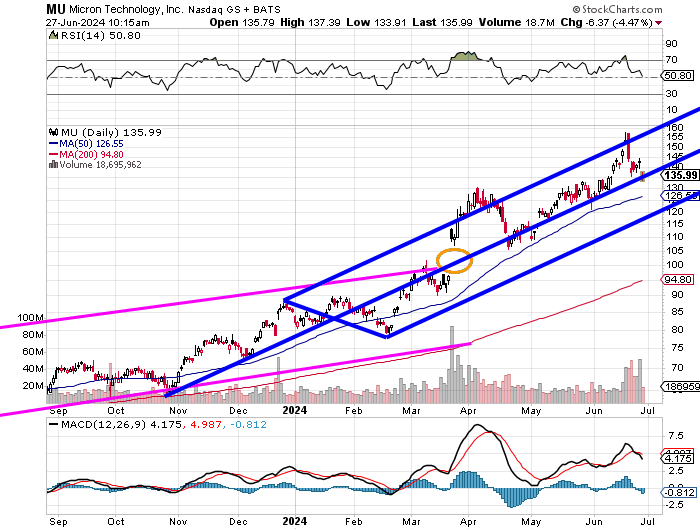

Readers will now see that the breakout of the rising price channel fits fairly nicely into an upward-sloping pitchfork model, with most of the action in the upper chamber of that model. There have been a couple of failed breakouts from the pitchfork, but now, the central trend line of the model is under pressure with his weakness.

Relative strength is neutral. The daily MACD is not in the greatest shape. The 12-day EMA has crossed below the 26-day EMA, and the nine-day EMA is already negative. Should the central trend line of the pitchfork fail to support MU through this weakness, the 50-day SMA is running parallel to that line and could do the job.

I came into these earnings short a $125/$115 bear put spread that paid me a net $1.70 that I will be able to subtract from my entry point in the formation of my net basis, but I will tell you this: I see this weakness in Micron as a golden opportunity to enter an AI-necessary name that I mostly missed, that has historically feasted and starved in cyclical fashion that may longer have to go through the cycle in that way as demand is apparently going to be inelastic for some time for this kind of chip. I will get long Micron equity on this weakness.

At the time of publication, Guilfoyle was long NVDA equity and MU puts and short MU puts.