Micron Report Is Greatest in Recent ‘Memory’. Here’s How I’m Responding

Micron’s quarterly report could be among the best in the history of corporate America. But will we see a Hynix hiccup?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Sarge-folio and “Memory/Storage Basket” core holding Micon Technology (MU) released fiscal third-quarter financial results last night, revealing adjusted earnings per share of $25.11 (unadjusted EPS: $24.67) on revenue of $41.456 billion. That top-line result was good enough for year-over-year growth of 345.8% (not a misprint), while the unadjusted and adjusted bottom-line number beat Wall Street by more than $4 per share. These numbers are simply put, incredible. Adjustments were made for stock-based compensation, which is ridiculous, and losses taken on debt repayments.

Did Micron Technology just report the greatest quarter in the history of corporate America? Maybe. Did Micron just post the best guidance ever? Maybe. Chairman and CEO Sanjay Mehrotra commented in the press release, “Micron’s record fiscal Q3 financial results and even stronger outlook for Q4 reflect the strategic value of memory in the AI era. Micron is investing at record levels in technology, products and supply to address our customers’ rapidly growing demand. We believe our multi-year Strategic Customer Agreements will significantly enhance the durability and predictability of Micron’s strong financial performance.”

Operations

As revenues generated grew 345.8% to $41.456 billion, the cost of those goods sold grew just 4.8% to $6.4 billion. That left a gross profit of $35.056 billion (+97.4%) as gross margin soared from 37.7% to a jaw-dropping 84.6%. Unadjusted operating expenses increased 29.8% to $1.738 billion. This left a unadjusted operating income of $33.318 billion, which was up 1,436% (again, not a misprint) as unadjusted operating margin improved from 23.3% to a stunning 80.4%. Adjusted operating margin improved from 26.8% to 81.2%.

After accounting for interest, other income & expenses and taxes, unadjusted net income printed at $28.243 billion (+1,398%). This works out to $24.67 per fully diluted share, up from the year ago comparison of $1.68. After adjustments, net income grew 1,223% and fully diluted EPS landed at $25.11, up from $1.91.

Guidance

For the current quarter, Micron is projecting revenue of $49 billion to $51 billion, which is well above Wall Street’s consensus view for a rough $43.5 billion. MU sees, for this quarter, an adjusted EPS of $30.00 to $32.00 vs. Wall Street’s expectations for something below $25.50. Gross margin is projected at a rough 86%, which is up even from the incredible quarter just reported.

Fundamentals

For the quarter reported, Micron generated operating cash flow of $25.388 billion (+451%). Out of that number came capital spending of $7.826 billion. Added to that sum are $733 million in government incentives and $9 million in proceeds from property sales. That left free cash flow of $18.304B, which was up 839% from the year ago comp.

Turning to the balance sheet, Micron ended the quarter with a cash position of $26.022 billion and inventories of $8.567 billion. That makes for current assets of $66.737 billion. Current liabilities add up to $19.488 billion. There is no short-term debt in this number. That puts the firm’s current and quick ratios at 3.42 and 2.98 respectively. That’s excellent, by the way.

Total assets amount to $134.112 billion. This includes only very small numbers for either “goodwill” or other intangibles. Total liabilities less equity comes to $33.388 billion, of which just $5.14 billion is labeled as long-term debt. Micron could take care of that five times over out of pocket. This balance sheet is absolutely pristine.

The CFO’s Call…

CFO Mark Murphy said, “Today, we indicated that we expected market tightness to continue beyond ’27. And part of that reason is we did see the HBM (high bandwidth) TAM (total addressable market) increase. We saw that. We had said previously that it would cross $100 billion in ’28. We see that now, the HBM TAM easily crossing $100 billion in ’27.”

Sarge Says… “Holy Moly, Batman!”

My Take

What’s not to be thrilled with? The quarter reported was beyond even what I thought were my possibly exaggerated expectations. I would have been happy with a revenue print of $36 billion to $37 billion. The guidance was even better. Cash flows are growing like weeds in August. The balance sheet? Simply one of the strongest and cleanest in the world. The one potential negative I see has nothing to do with anything you read here today.

There are basically two stories going on here. One… growing demand for high bandwidth memory as well as traditional Flash and DRAM. Two… surging prices for anything having to do with memory or storage.

The potential negative would be the listing in early July of SK Hynix ADRs on the Nasdaq in New York. SK Hynix is Micron’s very legitimate South Korean rival. Together, they dominate the market for memory and until now, very few U.S.-based investors could be in that name. Now, my “Memory / Storage Basket” will have to grow from four names to five. The decision is where to draw funds for SK Hynix from, not whether or not to be invested in SK Hynix.

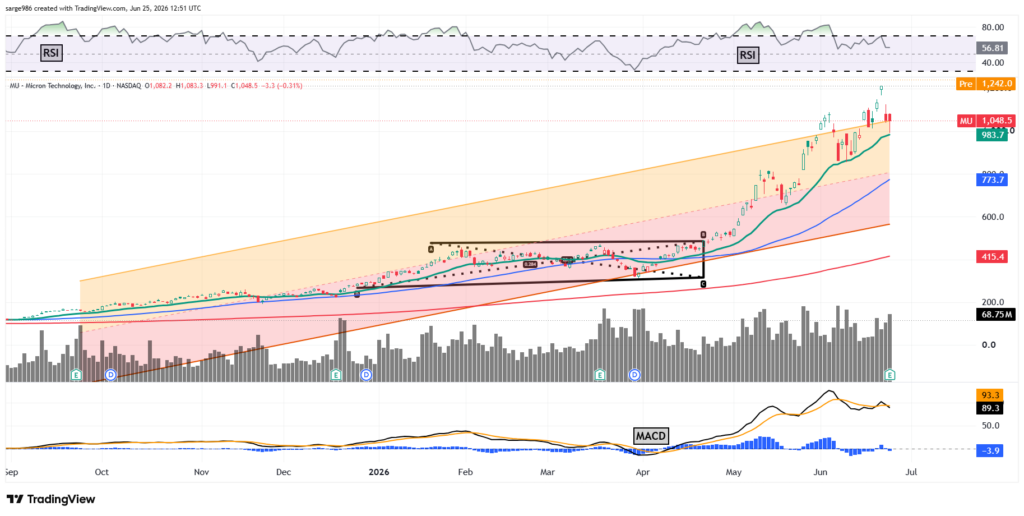

Readers will see that MU broke out of a basing period of consolidation in early April and continued its near-parabolic march higher. On Wednesday, the shares tested their 21-day EMA, where once again, traders and investors feasted on the dip. This allowed the stock to continue with its repetitive series of both higher highs and higher lows. The stock is now trying to break out of its lengthy up-trend that is illustrated here by my Raff Regression model.

Reviewing the key indicators, Relative Strength is solid and will surge on the open. Below the chart, the daily moving average convergence divergence is set to renew a much more bullish posture once the bell rings. I would expect the histogram of the 9-day exponential moving average to go positive and the 12-day EMA to cross above the 26-day EMA with both of those lines well above the zero-bound. These are all bullish in nature and in my opinion, trend re-affirming.

My Micron Strategy

Target Price: $1,600 (up from $1,375)

Add: Down to 21-day EMA (currently $984)

Pivot: Recent High (currently $1,213)

Panic: Loss of 50-day SMA (currently $773)

At the time of publication, Guilfoyle was long MU equity.