Meet the New Member of the Stocks Under $10 Club (That's Not a Good Thing)

Hopes were high going to earnings, but the stock is taking a pounding. Still, there's an interesting way to play this.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

There's a new member of the 'Stocks Under $10' Club. I'd like you to meet them.

Uber Technologies UBER rival, Lyft LYFT, released its second-quarter earnings on Wednesday morning. UBER had previously posted solid numbers, and the stock had done well in the wake of that release, so hopes were high for Lyft.

For the three-month period ended June 30, Lyft posted GAAP EPS of $0.01 (first time Lyft has been GAAP profitable) on revenue of $1.436 billion. These top and bottom-line numbers both beat Wall Street's expectations while the revenue print was good for year-over-year growth of 40.6%. Not bad at all.

Gross bookings were up 17% to $4 billion, while active riders increased 10% to 23.7 million. Total rides of 205 million were a company quarterly record, and also up 15% over the year-ago comp. In addition, driver hours hit an all-time high as the most new drivers joined the company in any one quarter since 2019.

The CFO

CFO Erin Brewer commented in the press release:

“Our platform is growing in a very healthy way as evidenced by the strength of our financial results, including strong cash flow generation and GAAP Net income. We had a strong second quarter with more than a hundred million dollars in Adjusted EBITDA, and we have solid momentum entering the second half of the year.”

Why the Stock Is Lower

LYFT shares have taken a pounding on Wednesday. I currently see that stock trading around $9.50, down almost 13.4% for the session. The financial results were good. The guidance was light.

For the current quarter, LYFT expects gross bookings to remain close to unchanged from Q2 (see above, was $4 billion). Wall Street was looking for something around $4.15 billion.

Adjusted EBITDA is expected to print within a range spanning from $90 million to $95 million, down sequentially from $102.9 million for the quarter reported. The Street was expecting a $103 million handle. Additionally, adjusted EBITDA margin is expected to decline to 2.3% from 2.6%.

For the full year, LYFT sees rides growing in the mid-teens year over year, and gross bookings growth that is "slightly faster than Rides" growth. Full-year EBITDA margin is seen at a rough 2.1%, up from 1.6% a year ago, but down from the reported Q2 and the expectations for Q3.

Fundamentals

For the quarter reported, LYFT generated operating cash flow of $276.2 million. Out of that number came capex spending of $19.8 million, leaving free cash flow of $256.2 million. That brought trailing 12-month free cash flow up to $368.4 million just to inform that this quarter was special.

Turning to the balance sheet, LYFT ran with a cash position (including restricted cash) of $2.014 billion and current assets of $2.68 billion. Current liabilities add up to $3.641 billion, including $389.3 million in shorter-term convertible notes. That makes for a fairly awful-looking current ratio of 0.74.

Total assets amount to $4.997 billion, which includes $306.6 million in goodwill and other intangibles. That's no problem at all. Total liabilities less equity comes to $4.419 billion, which includes another $578.3 million in longer-term debt.

This balance sheet looks kind of lousy. Largely that's because of a $1.603 billion item entered as a current liability that is quite simply labeled as "accrued and other current liabilities." Kind of hard to thoroughly analyze a balance sheet with a line item under current assets described so vaguely.

My Thoughts

The guidance is somewhat disappointing. The balance sheet does not do the shares any favor either.

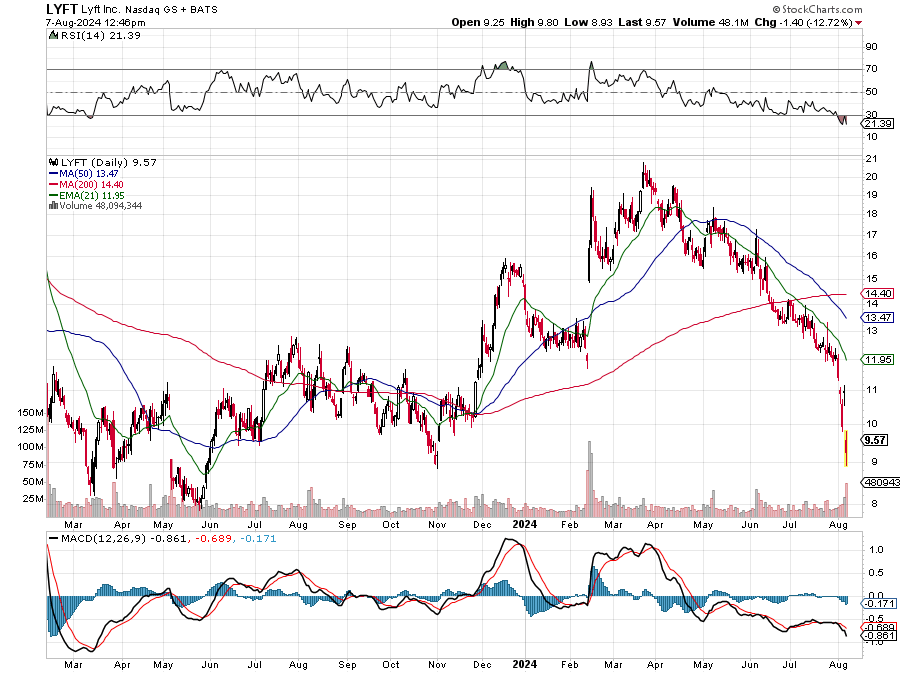

Take a look at the chart below. I really could not find a pattern that I thought might work here.

Relative strength is in a very bad place. The stock suffered a death cross just a few days ago and the stock is already trading more than $2 below its 50-day simple moving average (SMA). Lastly, look at that daily Moving Average Convergence Divergence (MACD). That's as ugly as ugly gets.

I don't need to buy LYFT on this dip, but if I were thinking of doing so, I think I'd wait to see if that low from May 2023 comes under fire. Instead of laying down the cash for some equity, I think the August 23 $8 calls trading at about $1.50 seem more interesting. Perhaps they would allow a speculative trader to cash in on an oversold bounce. Perhaps, if there is no bounce, they'll still have some value in a couple of weeks.

At the time of publication, Guilfoyle had no positions in any securities mentioned.