Lilly Is Expensive, But Priced for Explosive Growth: How to Trade It

The company is stingy with information, although sales growth and margins are going in the right direction.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

All hail, mighty Eli Lilly LLY !!

On Tuesday morning, pharmaceutical giant Eli Lilly released the firm's first quarter financial results.

For the three-month period ended March 31st, Lilly posted an adjusted EPS of $2.58 (GAAP EPS: $2.48) on revenue of $8.768B. The earnings print was good for a decisive beat, while the top line number, despite being good for annual growth of 26%, fell just short of consensus view.

The stock is trading sharply higher on Tuesday morning, thanks not just to the earnings beat and sales growth, but also due to the solid guidance that was increased from what had previously been provided.

Sales growth was largely driven by GLP drugs such as Mounjaro (diabetes), Zepbound (obesity), Verzenio (breast cancer), and Jardiance (diabetes). Domestically, revenue increased by 28%, driven by 16% growth in realized prices and 12% growth in volume sold. Ex-US, sales increased 22% driven by 23% volume growth, offset slightly by a 1% contraction in realized prices. Tyvyt (lung cancer) also improved sales growth outside the US.

Operations

As revenue grew 26% to $8.768B, the cost of those sales increased 3% to $1.674B. This left a gross profit of $7.094B (+33%) on a gross margin of 80.9%, up from 76.6%. Operating expenses such as research and development (+27%), market/administrative (+12%) and acquired IPR&D (+5%), left a GAAP operating income of $2.509B. That was good for year over year growth of 68% (not a misprint).

After accounting for other income, interest and taxes, GAAP net income popped for growth of 67% to $2.243B. That works out, after dilution, to earnings per share of $2.48.

Guidance

For the full year 2024, Lilly increased revenue guidance to $42.4B to $43.6B from the previously given $40.4B to $41.6B, a 4.9% increase at the midpoints. The firm sees a GAAP gross/operating margin of 32% to 34%, up from 30% to 32% and adjusted gross/operating margin at 33% to 35%, up from 31% to 33%.

Finally, Lilly is projecting a full year GAAP EPS of $13.05 to $13.35, and adjusted EPS of $13.50 to $14.00. This would be up from guidance already given of $11.80 to $12.30 and $12.20 to $12.70.

According to the press release, the sharply improved expectations will be "primarily driven by the strong performance of Mounjaro and Zepbound and greater visibility into the company's production expansion for the remainder of the year." For the first quarter, Mounjaro sales were up 218% from its year ago comp to $1.807B, while Zepbound sales were up from zero to $517.4M.

What Bugs Me

Now, I like Lilly. This stock has been great to me. It's up, what, like 7% this morning and I'm up 86% on the position. What Lilly does not do is release its balance sheet and statement of cash flows with its earnings release. That drives me crazy. I am sure that not that much has changed since February, but I want to know that. Things change.

In 2023, Lilly produced just $792M in free cash flow. In 2022, FCF came out to $5.732B. Is a timely release too much to ask for? The current ratio has fallen below the 1.0 level that many use as a barometer for balance sheet health. Has the solid quarter allowed the firm to get that balance sheet back into a better current condition? We may not know for two weeks. So, yes, I am annoyed.

My Thoughts

While we must wait patiently for more information, let's go to the charts. We know sales growth and margins are going in the right direction. The stock trades at 59 times forward looking earnings, which is expensive, but still priced for explosive growth. The firm pays shareholders $5.20 per share per year, which seems nice, but really only yields 0.7%.

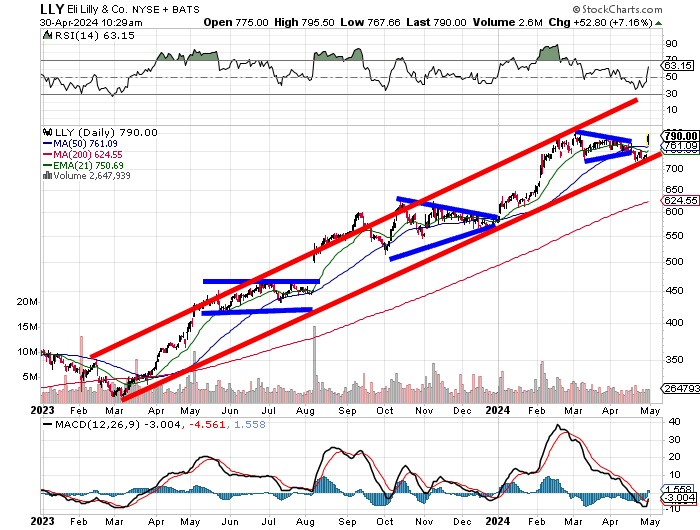

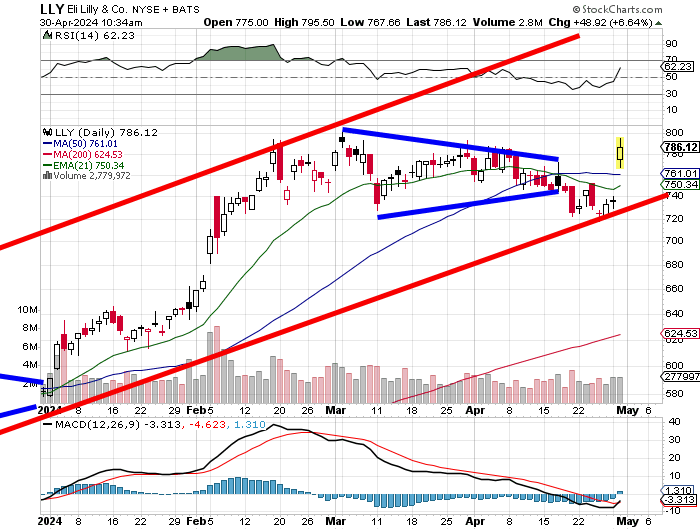

I showed readers the stepladder approach that LLY has taken as it has progressed since March 2022 creating a nice looking ascending price channel. Now, relative strength is up on today's move and the daily MACD (moving average convergence divergence) is turning for the better after what had been a couple of less than hot looking months. Let's zoom in.

The stock has retaken its 21-day EMA (exponential moving average) and 50-day SMA (simple moving average) on a gap. It will be key going into Fed Day and Jobs Day this week to see if the stock can hold that 50-day line.

Know what? Is this as good as it gets? Maybe, maybe not. This stock was one of my top 2023 performers, but I'll tell you this. I would expect profit takers to feast on this stock the next chance they get.

Instead of increasing my target price, I am inclined to make a sale myself if a new 2024 high cannot be made this week. It's easy, take the $800 level, and I sit tight with a $913 target. Fall back and fail at the 50-day line? I say "sold." It's one or the other.

At the time of publication, Stephen Guilfoyle was long LLY equity.