Just Do It? Or Is Nike Just Done?

The athletic brand giant has been disappointing shareholders and its latest financial reporting hasn't done anything to change that.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Athletic footwear, apparel and equipment maker Nike NKE released the firm's fiscal fourth quarter on Thursday evening. Yet again, Nike has disappointed its shareholders and the market, which has become a habit over the past few years.

FYI, CEO John Donohoe took this job in January 2020. I saw NKE trading with a $79 handle this morning. At that price, NKE would be down 21% since then and down 55.5% since the highs of December 2021. I do not know anything, but to think that Donohoe's job is completely safe is probably a bit naive. Shareholders may demand a change in the C-suite. We'll see.

For the three-month period ended May 31, 2024, Nike posted an adjusted EPS of $1.01 (GAAP EPS: $0.99) on revenue of $12.606 billion. The bottom-line print beat Wall Street quite decisively, but that top-line number not only fell short of expectations, but also showed a year-over-year contraction of 1.7%. I will warn readers that when I get to the fundamentals of the company, there was not a statement of cash flows included with last night's release. You know how much I love companies that do not release a complete financial package when they release earnings. Nike has made a habit in the past of including that cash flow information with their Form 10-Q about two weeks after the earnings release.

Operations

As revenue generation contracted 1.7%, the cost of sales decreased 4% to $6.972 billion. This permitted gross profit to increase 1% to $5.634 billion as gross margin improved from 43.6% to 44.7%. Selling and administrative expenses were down 7% to $4.088 billion. Prior to accounting for interest and taxes, income or EBIT increased a whopping 39% to $1.726 billion as EBIT margin improved from 9.5% to 13.3%. After accounting for interest and an effective tax rate that dropped from 17.3% to 13.1%, net income improved to $1.5 billion (+45%). This works out to $0.99 per diluted share.

Regional Performance

- North America: Sales decreased 1% to $5.278 billion, producing EBIT of $1.462 billion (+5%)

- Europe, Middle East and Africa: Sales decreased 2% to $3.292 billion, producing EBIT of $797 million (+2%)

- Greater China: Sales increased 3% to $1.863 billion, producing EBIT of $548 million (+4%)

- Asia, Pacific and Latin America: Sales increased 1% to $1.705 billion, producing EBIT of $479 million (+4%)

Brand Performance

- Nike: Sales decreased 1% to $12.149 billion, producing EBIT of $2.138 billion (+13%)

- Wholesale sales increased 5% to $7.1 billion

- NIKE Direct: Sales decreased 8% to $5.1 billion

- Converse: Sales decreased 18% to $480 million, producing EBIT of $94 million (-37%)

Product Line Performance

- Footwear: Sales decreased 4% to $8.237 billion

- Apparel: Sales increased 3% to $3.323 billion

- Equipment: Sales increased 35% to $578 million

Guidance

The firm alluded to updating its fiscal 2025 outlook in the press release (the current quarter is FQ1). CFO Matthew Friend covered that turf in the call and, wow, that's when things got ugly. I will let you read it in his words for the current quarter:

"Now turning to our first quarter, we expect first quarter revenue to be down approximately 10%. This reflects more aggressive actions in managing our classic footwear franchises, continuing challenges on NIKE Digital, muted wholesale order books with newness not yet at scale, a softer outlook in greater China, and a number of quarter-specific timing factors. We expect first quarter gross margins to be in line with the full year guidance."

And for the full fiscal year:

"We now expect fiscal 2025 reported revenue to be down mid-single digits, with the first half down high single digits. Foreign exchange headwinds have also worsened and will now have a one-point translational impact on revenue in fiscal 2025. Turning to gross margin, we expect full year expansion of approximately 10 basis points to 30 basis points on a reported basis. This reflects benefits from strategic pricing actions and lower product input costs, partially offset by supply chain deleverage, channel mix shifts, and net foreign exchange impact."

Balance Sheet

I would love to have access to the statement of cash flows, but some firms are just comfortable releasing incomplete information. Unfortunately, Nike is one of those companies. Looking at this balance sheet, as of May 31, 2024, Nike had a cash position of $11.582 billion (+8%) and inventories of $7.519 billion (-11%), putting current assets at $25.382 billion (+1%). Current liabilities add up to $10.593 billion, including $1 billion worth of short-term debt. This puts the firm's current ratio at a strong looking 2.39 and a quick ratio (ex-inventories) of 1.30, which for this kind of firm, is very solid.

Total assets amount to $38.11 billion, including just a negligible level of intangible assets. Total liabilities less equity comes to $23.68 billion, including $7.903 billion in longer-term debt. Though that seems like a hefty number, the firm does have the cash in reserve to more than take care of it if necessary. For all of Nike's problems, the balance sheet does not appear to be one of them. This is a healthy balance sheet.

Wall Street

Since these earnings were released, I have come across 15 highly-rated (four-plus stars at TipRanks) that have opined on NKE. After allowing for adjustments, across the 15, we have 10 "buy" or buy-equivalent ratings, four "hold" or hold-equivalent ratings and one outright "sell" rating. One of the "buys" and two of the "holds" did not set target prices, so we are working with just 12 of those.

The average target price across these 12 analysts is $97.75 with a high of $120 (Brian Nagel of Oppenheimer) and a low of $67 (Sam Poser of Williams Trading). Once omitting these two as potential outliers, the average target across the other 10 analysts rises to $98.60.

My Thoughts

This is a pretty tough report to look at. There are some positives. Margins are growing. The balance sheet is a strength. I really would like to look at the statement of cash flows when I look at everything else. I do look at not producing timely information as something lacking in corporate transparency. That may not be warranted, but why not produce all of your information in a timely fashion like almost every other publicly-traded firm does?

The gut punch here though is in the revenue for the quarter reported, and the revenue going forward both in the current quarter and full year guidance. Nike has problems and I am not sure they easily recover without making significant changes.

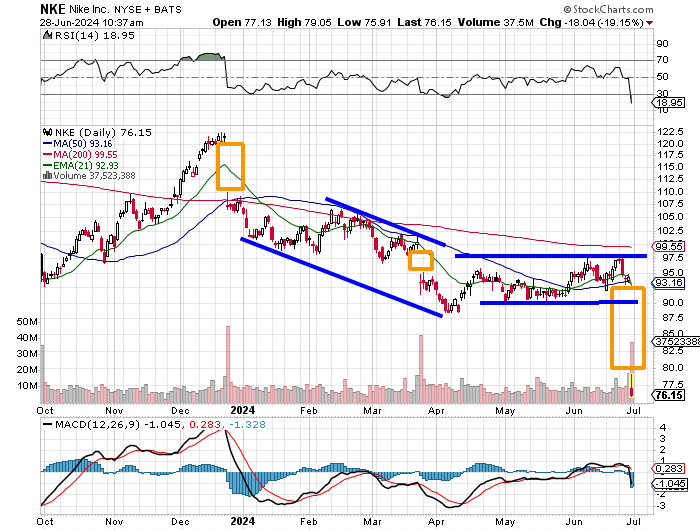

Readers will note that NKE has made a habit of gapping lower following the firm's earnings releases. These gaps are identified by the orange boxes above and, interestingly, none of these gaps has completely filled in the months after the report. The stock had been in a descending price channel from late December 2023 into April 2024 when the shares started to build a base. That base held into this morning when the floor fell out.

Relative strength is awful. The daily MACD is awful. The last sale is now 19% below its 50-day SMA and almost 17% below its 21-day EMA. That's fairly incredible. There is no technical support to speak of. The stock will have to build a base again and hopefully build some kind of positive breakout pattern from there. This will not be an easy or quick process in my opinion.

I will not be buying this show of weakness as I did yesterday with Micron MU. That was a much more upbeat, much more optimistic story. Instead of purchasing equity in NKE, if I were interested in the name, I might go out to August 16, 2024 expirations and sell $70 puts for about $0.55, while buying a like number of $65 puts for roughly $0.15 just for protection. The net credit would be $0.40. If the investor ends up being tagged with the shares in mid-August, the equity net basis would be $69.60.

At the time of publication, Guilfoyle was long MU equity and long MU puts.