Is This 'Perplexing' Low-Priced Stock Finally Dressed for Success?

Remember this one? Not too long ago the shares traded as high as $150.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Remember Stitch Fix SFIX?

The company was going to change the way we bought clothing. It was going to be everyone's online personal styling service.

The San Francisco-based online purveyor of personalized apparel with operations across the U.S. and at one time, the U.K. as well, offers merchandise at various price points from established brand names as well as from its own private labels.

Well, Stitch Fix still exists, but things haven't quite gone as planned.

The stock traded as high as $113.91 in late January 2021 after having traded below $150.90 in early 2020. The stock has not traded with a $10 handle since May 2022, and has not traded with anything above a $6 handle since August 2022.

Recent Earnings

On Tuesday evening, Stitch Fix released its fiscal fourth-quarter financial results. For the period ended August 3, Stitch Fix posted a GAAP loss per share of $0.30 on revenue of $319.550 million.

The earnings print missed estimates by more than a dime and compared to a $0.24 loss per share for the year-ago period. The revenue number actually beat consensus estimates, but still contracted 12.4% year over year.

n between the top line and the bottom line, the operating loss fell from $22.943 million to $41.888 million.

Guidance

For the current (fiscal first) quarter, Stitch Fix sees net revenue at $303 million to $310 million and adjusted EBITDA at $5 million to $9 million. That would work out to year-over-year revenue contraction of 17% to 15% and brings the high end of the range below the $319 million that Wall Street was looking for.

For the full fiscal year, Stitch Fix projects net revenue of $1.11 billion to $1.16 billion, which would be down between 17% and 13% year over year. Again, this brings the high end of the range well below the $1.31 billion that Wall Street had in mind. The company sees full-year adjusted EBITDA at $14 million to $28 million.

Fundamentals

For the period reported, Stitch Fix generated operating cash flow of $28.207 million, while spending $13.965 million on property and equipment. This left the company with free cash flow of $14.242 million, which was down from operating and free cash flows of $73.23 million and $54.367 million for the year-ago period. The company obviously cannot return capital to shareholders.

Turning to the balance sheet, Stitch Fix ended the quarter with a cash position of $246.968 million, and inventories of $97.903 million. That makes for current assets of $366.71 million (-14%). Current liabilities add up to $203.551 million, including a small amount ($9.217 million) in deferred revenue.

These numbers put the company's current and quick ratios at 1.80 and 1.32, respectively. Those ratios are nowhere near as poor as I had expected based on its recent business performance.

Total assets amount to $486.864 million, which includes no intangibles. We appreciate that. Total liabilities less equity comes to $299.842 million.

Other than lease liabilities and gift card liabilities, Stitch Fix has no "normal" debt on the books. No short-term debt, no long-term debt and certainly no revolving credit facilities that one might have expected to find.

My Thoughts

This stock is perplexing. Sales have contracted on a year-over-year basis for 10 consecutive quarters and once peaked at $581.24 million back in Q1 2022. Seems like a long time ago. The company still lost money that quarter.

Stitch Fix has not posted a positive EPS print since Q4 2021. Yet, free cash flow for the most recent quarter was above zero and the company has a deteriorating balance sheet over time, but still no debt in the traditional sense.

Still fairly new at his job, CEO Matt Baer commented early in the conference call:

"Since I joined Stitch Fix, we have been hard at work formalizing and executing our transformation strategy, which includes three distinct phases: a rationalization phase, a build phase, and a growth phase. Our rationalization phase, which took place over the past year, was a period of critical assessment. It was during this phase that we began to strengthen the foundation of our business and ensure we had the right priorities in place to improve our financial position and enable us to operate as a more nimble and efficient organization. As part of this, we exited the U.K., closed two fulfillment centers, right sized our corporate head-count and continued our cost discipline management. These actions, among others, resulted in over $100 million of SG&A savings in FY 2024."

So, there is a plan, and is it possible that this was the nadir? I cannot say I would buy this one for my own accounts just yet. I can say that it is worthy of being placed on my "Stocks Under $10" watchlist, or what we used to call the "bullpen."

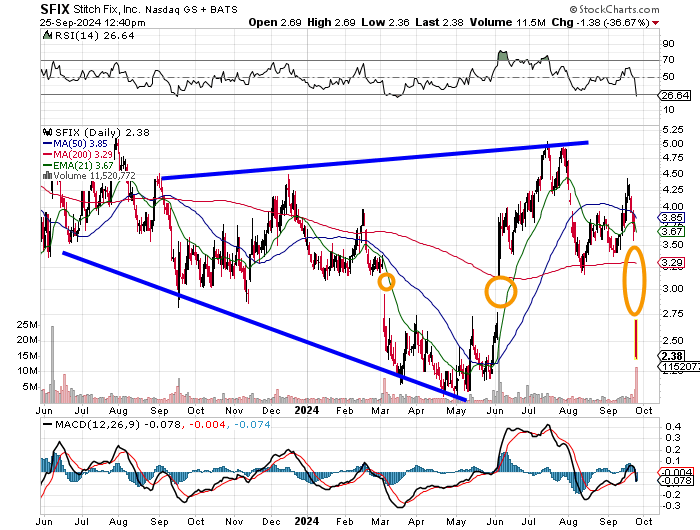

Readers can see in the chart that the above wedge is broadening and repeatedly leaving unfilled gaps in its wake. If see this stock trade closer to the $2 level I may just take the speculative plunge. It appears, even at these low-single-digits prices, the stock is only becoming more and more volatile in percentage terms.

At the time of publication, Guilfoyle had no positions in any securities mentioned.