Intel Is Losing Ground

There is technical reason for Intel stock to rebound from here but no strong case to put equity in its name.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Over the weekend, we heard from Nvidia NVDA and Advanced Micro Devices AMD to much fanfare from the Computex conference in Taiwan. The stock of Nvidia soared on Monday in response to the firm's roadmap for its elite-level businesses over the next two years. AMD rallied early and then sold off some 2% for the session after that early surge failed. I own both names.

Intel INTC has been busy making announcements, too. It certainly seems that fewer folks care. Is Intel in danger of losing its spot in the Dow 30? Anything at this point is speculation, but can you see the possibility of Intel ousted from that not-so-focused-upon-but-still-prestigious equity market index and being replaced by one of its peers? I sort of can. I think.

Intel Unveils New Innovations

On Monday, Intel revealed new processors designed to compete with the likes of what appear to be the firm's more advanced competitors.

First up are the Xeon 6 server processors that include both E-core and P-core versions. These are intended, in CEO Pat Gelsinger's words, to "deliver better performance and power efficiency for high-intensity data center workloads as compared to its predecessor."

I think we expected the newer products to outperform their predecessors. What we want to know is can they outperform their direct competition.

The E-cores enables rack-level consolidation of three to one, a performance gain of 4.2 times and a performance-per-watt gain of 2.6 times relative to second generation Xeon chips with media transcode workloads. The P-cores are designed for highly-demanding workloads and are expected to launch at some point in Q3 2024. The success of the Xeon 6 family of chips is paramount to the possibility of Intel regaining any lost ground to AMD for the PC/laptop market where AMD has simply stolen Intel's lunch.

Intel also unveiled its Lunar Lake architecture designed to grow the firm's profile in the AI PC category. Lunar Lake is expected to power more than 80 new AIPC designs from more than 20 PC manufacturing partners. Intel will also make available a Gaudi 3 accelerator kit, including eight AI-capable chips that will list at $125,000 or about two-thirds of what it claims competing platforms are going for.

JPMorgan Highlights Intel Competitors

On Tuesday morning, JPMorgan released a note explaining that the firm sees Broadcom AVGO and Marvell Technology MRVL dominating the high-end of the custom chip market, which is described as fast-growing. JPMorgan sees the "application-specific integrated circuit" market increasing to $25 billion to $30 billion and growing at a compound annual growth rate of 20% due to the rise in generative AI.

Intel Beat Expectations But Still Fell Short

Intel reported the firm's first quarter on April 25, so more than a month ago. We'll hear about Intel's second quarter in late July. For that first quarter, Intel beat expectations for adjusted earnings, but fell short of Wall Street's projections for revenue generation, while growing sales 8.5%. What was frightening in those results was, of course, not the 30% growth in client computing, but the 19.4% contraction in the data center and in AI as well as the 47.8% contraction in sales for Mobileye.

Perhaps most disturbing of all was the lack of performance in the Foundry, which is how the firm brought in federal capital related to the Chips Act and an area where, even if behind other designers on the elite side of the semiconductor coin, perhaps there was room for the firm to take share away from industry leader Taiwan Semiconductor TSM. Yet the firm operated the foundry at a loss in Q1 2024, a larger loss than in Q1 2023.

Additionally, Intel guided the current quarter towards revenue in a range spanning from $12.5 billion to $13.5 billion with Wall Street looking for something around $13.6 billion and an adjusted EPS of $0.10 with Wall Street looking for $0.25. Of course, Intel also projected a GAAP loss which has become their norm.

Intel Cannot Continue This Way

Readers might be surprised to know that Intel burned a lot of cash over the past four quarters. At the close of the firm's first quarter, Intel had generated $12.033 billion in operating cash flow over the trailing twelve months while spending $24.307 billion on capital expenditures. That's a pretty gnarly 12-month print for free cash flow of $-12.274 billion. The firm also paid out $2.195 billion in cash dividends. That's quite a cash burn.

The balance sheet is not in awful shape, but Intel cannot have a couple more years like the one just had. The firm ended Q1 with a cash position of $21.311 billion, which is down approximately 44% over two years. Short-term debt stood at $4.581 billion, which will have to be either paid off or refinanced at higher interest rates within a year. The firm has no current unearned revenues on the balance sheet, which may or may not be troubling. Then there's another $47.869 billion in long-term debt. (I'm doing the shoulder-shrug here.) This balance sheet is not even close to being in the same fine condition as are the balance sheets at Nvidia and AMD.

Top-Tier Analyst Rates Intel a Sell

Regular readers will remember the name Toshiya Hari of Goldman Sachs. He is the top-tier five star rated (by TipRanks) analyst that I wrote to you about earlier this week, who had placed a "conviction buy" on NVDA and had also rated AMD as a "buy."

Last week, Hari opined on Intel. He reiterated his outright "sell" rating on INTC with a $29 target price. Analysts who do not like a stock will often rate that stock as a "hold," but Hari has and has reiterated a sell on Intel. Wow.

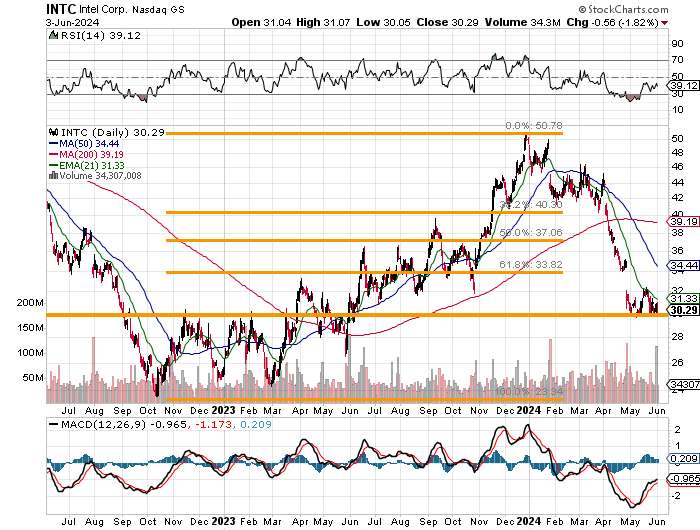

Readers will see that INTC has found, at least since late April, support at the 78.6% Fibonacci retracement level of the October 2022 through late December 2023 rally. Yes, 78.6% and 23.6% retracements are Fibonacci sequences, but my model here does not recognize them, so I have to draw them in when they matter. Here, they matter. If one was inclined to get long INTC, this is probably the spot to do so. I will not be joining you, however.

When it comes to Intel, I am from Missouri. They are going to have to show me. Yes, there is a technical reason for the stock to rebound from here, but that has failed once (in May) already. Should that Fibonacci door open here, the stock can indeed go lower. There is not a strong fundamental case to put equity into this name, and the fact is that Nvidia, Advanced Micro Devices, Broadcom, Marvell Technology and Taiwan Semiconductor are all better at doing different things than Intel, which is really a jack of all trades at this point.

At the time of publication, Guilfoyle was long NVDA and AMD equity.