Intel Falls Flat on Its Face Leaving Investors Rattled: How to Trade It

If readers have not been following the Intel story, the cash flow numbers might floor you, so sit down.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Dow component and semiconductor designer/foundry Intel INTC also until now, through Thursday as "the comeback kid", reported the firm's fourth quarter financial results last night. To say that the firm fell flat on its face would not be overstatement.

For the three month period ended December 30th, Intel actually did well. The firm posted an adjusted EPS of $0.54 (GAAP EPS: $0.63) on revenue generation of $15.4B. Intel did manage to beat Wall Street on both the top and bottom lines as that sales number was good for year over year growth of 10%. Adjustments were made primarily for stock based compensation that were more than offset by restructuring charges.

The fourth quarter was decent, and not the problem. The problem was the firm's outlook for the current quarter that badly missed consensus view.

Operations

As revenue was growing 10%, the cost of that revenue printed at $8.359B (-2.1%), leaving gross profit of $7.047B (+28.1%) on a gross margin of 45.7%, up from 39.2%. Operating Expenses dropped 32.7% to $4.462B, leaving operating income of $2.585B (up from $-1.132B) as operating margin improved from -8.1% to +16.8%.

After accounting for interest and taxes, net income attributable to Intel printed at $2.669B, up from $-664M. That's how we get to a GAAP EPS of $0.64, which was up from $-0.16 for the year ago comparison.

Segment Performance

Client Computing generated revenue of $8.844B (+33%), producing operating income of $2.888B (+451%) on an operating margin of 32.7%, up from 7.9%.

Data Center & AI generated revenue of $3.985B (-10%), producing operating income of $78M (-38%) on an operating margin of 1.9%, down from 2.9%.

Network & Edge generated revenue of $1.471B (-24%), producing operating income/loss of $-12M (down from $+126M) as operating margin fell into the negative from 6.5%.

Mobileye generated revenue of $637M (+13%), producing operating income/loss of $242M (down from $-34M) as operating margin improved to 38% from 37.2%.

Intel Foundry generated revenue of $291M (+63.5%), producing operating income of $-113M (down from $-34M ).

All other generated revenue of $178M (-42%), producing operating income/loss of $-498M (up from $-2.084B).

Guidance

For the current quarter, Intel is projecting revenue of $12.2B to $13.2B, which is well below the $14.2B or so that Wall Street had been expecting. For the quarter, the firm sees an adjusted gross margin of 44.5% down sequentially from 48.8% and a GAAP gross margin of 40.7% down sequentially from 45.7%. Lastly, the firm sees an adjusted EPS of $0.13 and a GAAP EPS of $-0.25. Wall Street had been looking for an adjusted EPS of roughly $0.40. That, my friends, is ugly.

Quite alarmingly, during the call last night, CFO David Zinsner said, "We expect Q1 data center revenue to decline double-digit percent sequentially before improving through the year. While the data center has seen some wallet share shift between CPU and accelerators over the last several quarters, we expect growth in CPU compute cores to return to more normal historical rates and our discrete accelerator portfolio with well over $2 billion in pipeline to gain traction as we move through 2024."

This is what rattled investors overnight.

Fundamentals

If readers have not been following the Intel story, the cash flow numbers might floor you, so sit down. For the full year 2023, Intel generated operating cash flow of $11.471B, down from $15.433B in 2022. In 2023, Intel spent $22.324B on capital expenditures, down from $24.069B in 2022. This left free cash flow at $-11.853B for 2023, down from $-4.075B in 2022. The last year that Intel generated positive free cash flow was 2021.

Checking out the balance sheet, Intel ended the quarter and year with a cash position of $34.945B and inventories of $11.127B. Both of those were down from 2022. Current assets totaled $43.269B (-14.2%). Current liabilities also decreased (-12.8%) to $28.053B including short-term debt of $8.578B. This puts Intel's current and quick ratios at 1.54 and 1.15, respectively. These ratios still pass muster, but we do have to trust the valuation for those inventories and that is a nice chunk of debt maturing this year that will either have to come out of cash or end up financed at higher interest rates.

Total assets amount to $191.572B including $32.18B in goodwill and other intangibles. At 16.8% of total assets, this is not a problem. Total liabilities less equity comes to $81.607B including $46.978B in longer-term debt. This balance sheet, while technically in decent shape for now, will lose that decent shape more quickly than one might think if the firm can not stop burning cash at the rate it has been.

Wall Street

Since these earnings were released last night, I have come across 25 highly rated sell-side (4+ stars at TipRanks) that have opined on INTC. After allowing for changes, across the 25, there are four "buy" or buy-equivalent ratings, 19 "holds" or hold-equivalent ratings, and two outright "sell" or sell-equivalent ratings. Three of our holds did not set target prices, so we are left working with 22 of those.

The average target price across the 22 analysts is $44.11 with a high of $68 (Gus Richard of Northland Securities) and a low of $31 (Chris Caso of Wolfe Research). Once omitting those two as potential outliers, the average target across the other 20 drops to $43.58.

Out of interest, the average target among the buys is $59.25, the average "hold" target is $41.59, and the average "sell" target is an even $34.

My Thoughts

Make no mistake. This is a troubled firm. The cloud and AI battles have already been lost to Nvidia NVDA, with Advanced Micro Devices AMD and maybe Marvell Technology MRVL the only competitors that seem to have an edge toward taking some market share. Automotive is high margin, but small business for the firm. The PC business is still the bread and butter of the firm, providing the lion's share of revenue generation, but AMD has been taking share there for years and I don't know if that can change. AMD reports next week and we'll learn more about that.

The one part of the business that I actually have fairly high hopes for is the foundry. Still a money loser, there is probably plenty of room for competition in the space.

The balance sheet is not great, but good enough, as long as the firm can find a way to bring down CapEx spending versus operating cash flow. To do anything else will be to watch the quality of the balance sheet continue to deteriorate.

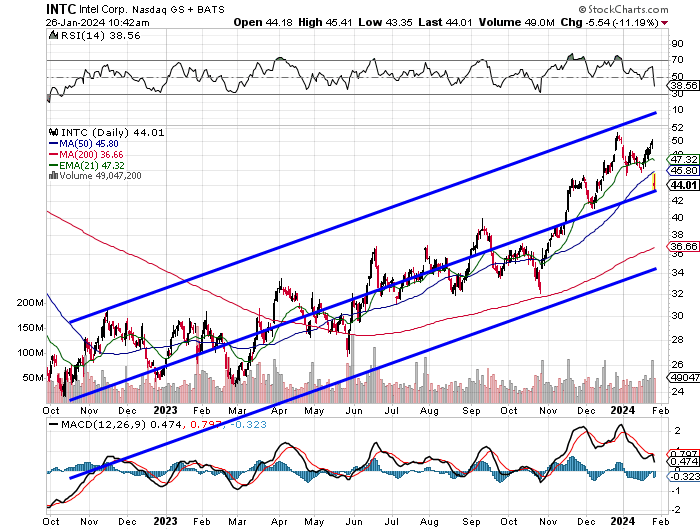

Readers will see that the shares remain neatly tucked inside of this Raff Regression model, so despite the overnight selloff, the trend is not necessarily broken. The shares gave up both the 21 day EMA (exponential moving average) and 50 day SMA (simple moving average) overnight as Relative Strength rolled off of a table and the daily MACD (moving average convergence/divergence), took a turn for the worse.

Is the 200 day SMA worth an investment? If it gets there. Waiting for the stock to test the lower trendline of the model might take a while. It never has. No, in short, I am not buying this dip, deep as it is. That said, I think that Intel does eventually get itself back in this game.

I would not pay more than the 200 day SMA (currently $36.66) for the equity. Write April 19th INTC $37 puts for about $0.50? That's an idea. Found money if it never sells off that far. A $36.50 net basis if the investor does end up having the shares put to him or her. That's for a stock trading above $44 today. Like I said. It's an idea.

(Marvell is a holding in the Action Alerts PLUS member club. Want to be alerted before AAP buys or sells MRVL? Learn more now.)

At the time of publication, Stephen Guilfoyle was long NVDA, AMD equity.