I'm Not Going to Disney... Until This Happens

The House of Mouse reports — and it ain't so hot. Here's what I'm looking for to get long the stock.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I had some doubts coming in. Disney DIS has often released their quarterly earnings after the closing bell when they think they have good news to report. I did not want to read too much into a pre-opening release, but that did cross my mind.

The quarter reported was pretty good. The outlook? I'm not so sure. Let's dig in.

Readers should note that I am not a shareholder at the moment, nor have I been for quite some time. That said, I'll probably always be a Disney fan and have tended in the past to look for ways to be optimistic on the stock.

For the fiscal third quarter, which ended June 29, Disney posted adjusted EPS of $1.39 (GAAP EPS: $1.43) on revenue of $23.155 billion. These top-line and bottom-line results all beat Wall Street expecations, the EPS prints quite handily, while the revenue print reflected year-over-year growth of 3.7%. Adjustments were made for income tax reserve changes offset to a great degree by the amortization of the acquired Fox and Hulu assets and a fair value step up on film and TV costs.

Operations

As revenue increased 3.7% to $23.155 billion, costs and operating expenses rose 0.5% to $19.801 billion. After accounting for other income/losses, interest and impairment charges (for the year-ago quarter), EBIT (earnings before taxes) improved to $3.093 billion (up from -$134 million).

After taxes, net income attributable to shareholders improved to $2.621 billion (up from -$460 million). This works out to a GAAP EPS of $1.43, up from a loss of $0.25 per share for the year-ago comparison.

Segment Performance

- Entertainment... generated revenue of $10.58B (+4%), producing operating income of $1.201B (up from $408M).

1) Linear Networks... generated revenue of $2.663B (-7%), producing operating income of $966M (-6%).

- Domestic... generated revenue of $2.145B (-7%), producing operating income of $682M (-1%).

- International... generated revenue of $518M (-9%), producing operating income of $157M (flat).

2) Direct to Consumer... generated revenue of $5.805B (+15%), producing operating income/ loss of $-19M (up from $-505M).

- Disney+ (US & Canada) grew paid subs 1% to $54.8M, as monthly ARPU dropped 3% to $7.74.

- Disney+ (Int, ex-Hotstar) saw a small decrease in paid subs to 63.5M as monthly ARPU grew 2% to $6.78.

- Disney+ Core grew paid subs 1% to 118.3M as monthly ARPU dropped 1% to $7.22

- Disney+ Hotstar saw paid subs contract 1% to 35.5M as monthly ARPU grew 50% to $1.05.

- Hulu (SVOD) grew paid subs 2% to 46.7M as monthly ARPU grew 8% to $12.73.

- Hulu (Live TV & SVOD) saw paid subs contract 2% to 4.4M as ARPU grew 1% to $96.11.

3) Content Sales / Licensing... generated revenue of $2.112B (+4%), producing operating income of $254M (up from $-112M).

- Sports... generated revenue of $4.558B (+5%), producing operating income of $802M (-6%).

1) ESPN (Domestic)... generated revenue of $3.908B (+5%), producing operating income of $1.085B (+1%).

2) ESPN (International)... generated revenue of $371M (+6%), producing operating income of $5M (up from $-27M)).

3) Star India... generated revenue of $279M (+1%), producing operating income/loss of $-314M (down from $-216M).

- Experiences... generated revenue of $8.386B (+2%), producing operating income of $2.222B (-3%).

1) Parks (Domestic)... generated revenue of $5.82B (+3%), producing operating income of $1.347B (-6%).

2) Parks (International)... generated revenue of $1.602B (+5%), producing operating income of $435M (+2%).

3) Consumer Products... generated revenue of $964M (-5%), producing operating income of $440M (+2%).

The CEO Comments

CEO Bob Iger commented in the press release: “This was a strong quarter for Disney, driven by excellent results in our Entertainment segment both at the box office and in DTC, as we achieved profitability across our combined streaming businesses for the first time and a quarter ahead of our previous guidance."

However, Iger added: "Despite softer third quarter performance in our Experiences segment, adjusted EPS for the company was up 35%, and with our complementary and balanced portfolio of businesses, we are confident in our ability to continue driving earnings growth through our collection of unique and powerful assets.”

Guidance

For the current quarter, Disney sees Disney+ Core subscribers growing modestly. The Content Sales & Licensing business is expected to remain profitable and post profitability for the full year. However, despite seeing "strong demand" for the Cruise Line, the company expects that for Experiences, "the demand moderation we saw in our domestic businesses in Q3 could impact the next few quarters" The company adding, "We expect Q4 Experiences segment operating income to decline by mid-single digits versus the prior year."

For the full year, Disney is targeting adjusted EPS growth of 30%, while focusing on cost cutting beyond previously stated targets. The combined streaming services are expected to continue to improve during the quarter, providing profitability across Disney+, Hulu and ESPN+.

Fundamentals

For the first nine months of the fiscal year, Disney has generated operating cash flow of $8.453 billion. Out of that number, came capex spending of $3.923 billion, leaving free cash flow of $4.53 billion. Out of that number, the company has repurchased $2.523 billion in common stock for the company treasury, while also paying shareholders $549 million in cash dividends.

Turning to the balance sheet, Disney ended the period with a cash position of $5.954 billion and inventories of $1.984 billion. This has left current assets at $25.493 billion. Current liabilities add up to $35.612 billion, including deferred revenue of $7.336 billion, which is not a true financial obligation, but also $8.06 billion in shorter-term debt. The level of debt maturing within 12 months is problematic, as it outweighs the cash on hand and will have to be refinanced possibly in its entirety and probably at higher interest rates.

Disney's current and quick ratios at the headline level come to 0.72 and 0.66, respectively, which is below what I would call acceptable. Once adjusted for those deferred revenues, these ratios climb to 0.90 and 0.83, respectively. That really does not cut the mustard, in my opinion.

Total assets amount to $197.772 billion, including $85.021 billion in goodwill and other intangibles. At 43% of total assets, this is enough to watch and almost enough to be concerned about. Total liabilities less equity comes to $92.469 billion, including another $39.524 billion in longer-term debt. To call this one of the higher quality balance sheets that I have analyzed would be dishonest.

My Thoughts

The positive takeaway is that the streaming services are becoming profitable. Additionally, Disney just announced increased pricing across all three services.

The negative takeaway? That the company is concerned enough about the state of the parks that they warned in the guidance. The parks have been a constant winner since the pandemic, but households are significantly poorer on average than they were a few years ago and a trip to a Disney park is very expensive.

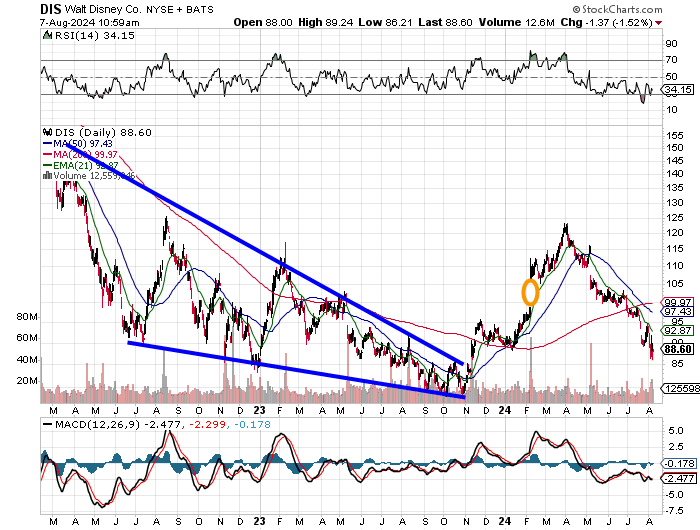

Notice the falling wedge pattern, above, which is a pattern of bullish reversal that stretched from March 2022 into late 2023. This produced the breakout that Disney shares enjoyed into this past spring.

Let's zoom in:

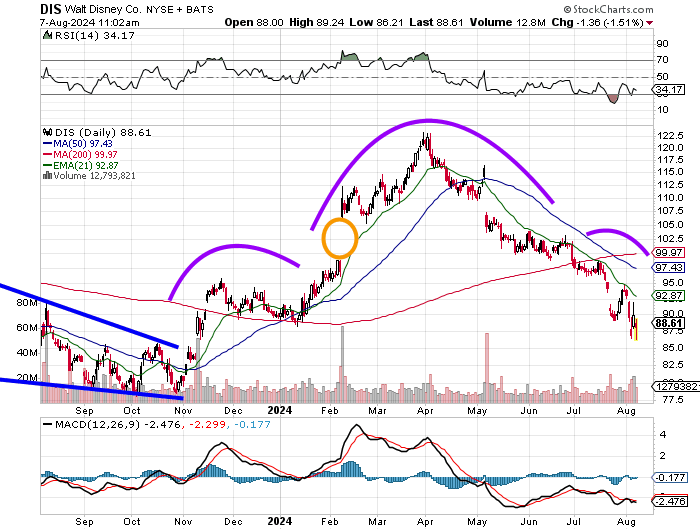

Disney stock has produced a head-and-shoulders pattern that has seen the stock retrace the gains of late 2023 into 2024 almost in their entirety. Relative strength is weakish, the daily Moving Average Convergence Divergence (MACD) is postured quite bearishly, and the stock has just suffered a death cross in July.

My opinion is that this stock could trade even lower and test the lows of last October/November. I'd love to get long some, but not until it takes and holds its 21-day exponential average (EMA) and shows at least a little momentum towards its 50-day simple moving average (SMA).

Right now, due to the slowing parks business, the lower quality balance sheet and the lousy chart, Disney is a "no-go" for me.

More Trading Basics:

- The Most Important Thing I've Learned in 25 Years of Trading

- Day Trading Is Very Difficult: Here Are 6 Tips for Long-Term Success

- Everything You Ever Wanted to Know About the CNN Fear & Greed Index

At the time of publication, Guilfoyle had no positions in any securities mentioned.