How to Handle Honeywell as Its Aerospace Business Could Take Off (Literally)

The aerospace technology segment posted sales growth of 10% in Q3 and now the company is eyeing separating it from the rest of HON.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We've been long Honeywell International HON for some time now. The shares are trading higher since this past autumn, but hid a lofty peak in mid-November and have traded sideways or lower ever since. The reason for our investment? We felt that the stock was undervalued and that the gem of the company, the aerospace business, was worth investing in all by itself. Apparently, the company feels the same way. Huzzah!

News broke early on Monday morning that the Honeywell board of directors has continued its comprehensive evaluation of the business portfolio launched earlier this year by chair and CEO Vimal Kapur. The goal had been to unlock shareholder value, and what is under consideration apparently includes the separation of the aerospace business.

Readers may recall that as Honeywell posted sales growth of 6% for the third quarter, the aerospace technology business posted sales growth of 10%. For the entire company, 6% growth equaled the strongest quarter it had since the second quarter of 2021, while for the aerospace unit, that was a ninth consecutive quarter of double-digit growth.

Behind The News

Readers will recall that activist investor Elliott Investment Management had gotten involved, taken down a $5 billion stake in the firm and called for such a split back in November. That was the reason behind the spike in the share price about five weeks ago. Honeywell, for that matter, has already announced the sale of its personal protective equipment business to Protective Industrial Products, which is an Odyssey Investment Partners Business for $1.325 billion in cash since Elliott Management started throwing its weight around.

At that time, Honeywell made a statement that this sale enabled it to "further simplify and optimize its business in alignment with three powerful megatrends: automation, the futures of aviation, and energy transition." Elliott, by the way, has not only called for the separation of the aerospace unit, but also the separation of that automation unit.

Earnings

Honeywell will not report the fourth quarter financial results until Feb. 6. Current consensus view is for an adjusted earnings per share of $2.31, and an unadjusted EPS of $2.21 on revenue of $9.87 billion. That would compare to an adjusted EPS of $2.60 for the year-ago period, while reflecting sales growth of just 4.6%. The company remains a cash flow beast, generating operating cash flow of $6.771 billion and free cash flow of $5.636 billion over the trailing twelve months as of the end of the third quarter.

Wall Street

Just last week, two five-star rated sell-side analysts opined on the stock. On Monday, Andrew Kaplowitz of Citigroup reiterated his "buy" rating while increasing his target price from $244 to $268. On Thursday, Joe Ritchie of Goldman Sachs reiterated his "buy" rating while taking his target price up to $256 from $227.

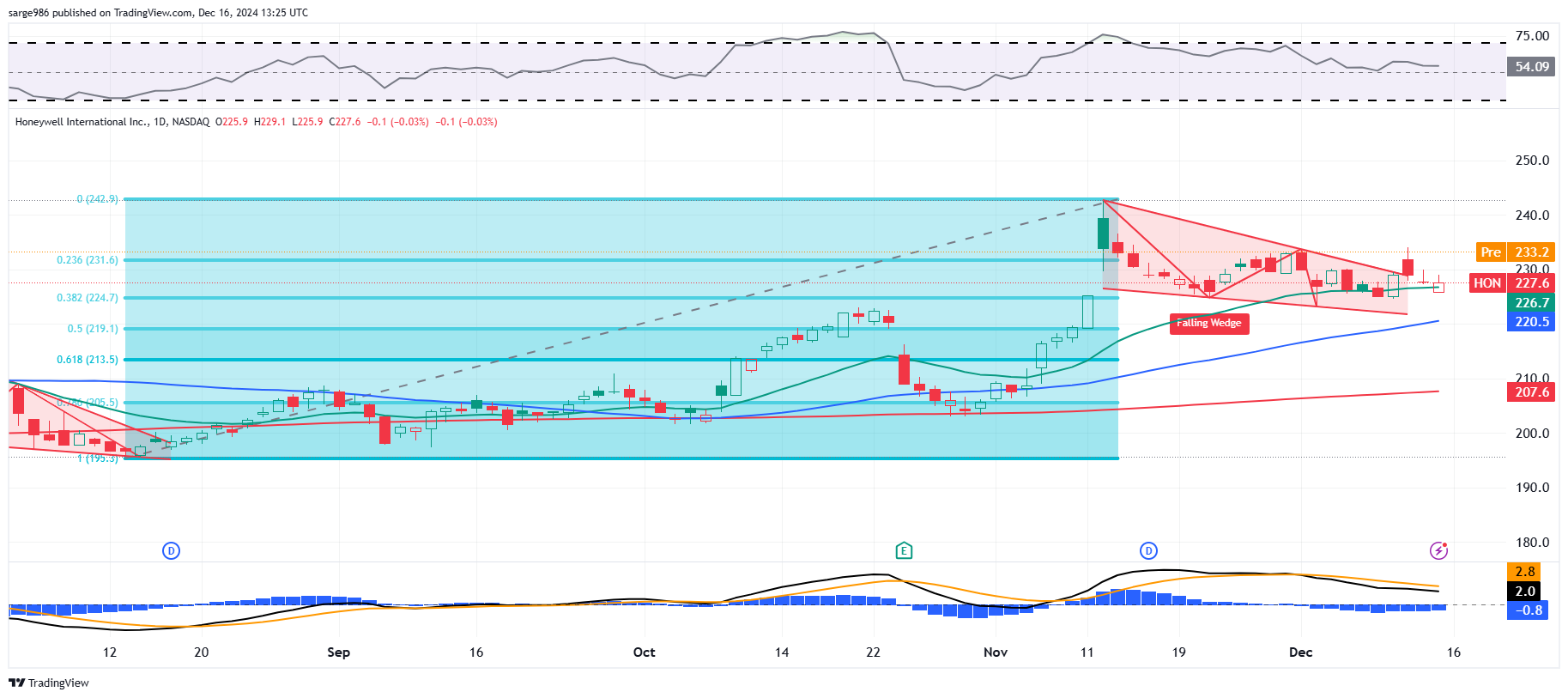

The Chart

Readers will see that HON slowly worked its way higher, out of a Falling Wedge pattern that bottomed this past October. The shares spiked in November on the Elliott news and thus began the creation of a new Falling Wedge, which for the new kids, is considered to be a pattern of bullish reversal. The first bit of support for the lower trendline of the wedge came at the 38.2% Fibonacci retracement level of the August into November run.

This morning, Honeywell more or less announced that it will likely have something to say on the matter, or at least some results of its internal study by fourth-quarter earnings release and that has the shares higher ahead of the U.S. open. My thoughts are that as long as Elliott forces the company to take steps that unlock shareholder value, this stock can sit in my most active portfolio.

Honeywell is a small to medium-sized position for me, my 20th largest long position in a book holding 34 long positions in either stocks or ETFs. My allocation toward HON is currently about 1.4% of the book. My median allocation is 1.9%. As my readers well know, some of my more successful names have run wild this year, so my book is currently top heavy despite having taken some profits at target prices along the way.

Honeywell International Trade Strategy

Target Price: $260

Pivot: $226 (current upper trendline of wedge pattern)

Add: down to 50-day simple moving average (currently $220)

Panic: break of 200-day SMA (currently $207)

At the time of publication, Guilfoyle was long HON equity.