Have the JetBlue Blues? I've Got Your Boarding Pass

This is not a screaming 'buy' by any chance. But there's a good way to play it.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Tuesday morning, just about a week after making a decision to back off from its efforts to acquire Spirit Airlines SAVE, former Stocks Under $10 bullpen member JetBlue Airways JBLU released a Form 8-K update concerning the company's expected first-quarter performance. Though no longer burdened by the economics of the Spirit deal that would have been daunting, this update is still not exactly pretty.

It was just about six weeks ago that JetBlue posted a fourth-quarter adjusted loss per share of $0.19 per share on revenue of $2.33B. Though the revenue print was only good for a year-over-year contraction of 3.7%, both the top and adjusted bottom lines did beat expectations.

At that time, JetBlue saw Q1 revenue down between 5% and 9% year over year and flat for the full-year 2024. The company also saw CASM (cost per average seat mile), ex-fuel to be up between 9% to 11% for the current quarter and up mid-to-high single digits for the full year.

With the new filing, JetBlue now expects revenue generation for the current quarter to be down just 4.5% to 7.5%, an improvement from previous guidance of down 5% to 9%. The company also sees CASM, ex-fuel up 8.5% to 9.5%, which is an improvement over the previously given (9% to 11% growth. However, JetBlue currently sees fuel price per gallon for the quarter at $2.93 to $3.03, which is up from the $2.87 to $3.02 it had previously been projecting. Available seat miles are now expected to drop 3% to 4% as opposed to 3% to 6% for Q1. That's positive.

Fundamentals

As of that last earnings release, which covered the three-month period ended December 31, JetBlue generated operating cash flow of -$86M. Tack on Capex spending of $433M and free cash flow came to -$519M.

For the trailing 12 months (full year), JetBlue generated operating cash flow of $400M, out of which came Capex spending of $1.206B, leaving free cash flow of -$806M. Obviously, the company did not return capital to shareholders.

Turning to the balance sheet, JetBlue ended the quarter with a cash position of $1.567B and inventories of $109M. This left current assets of $2.16B. Current liabilities added up to $3.628B, including short-term debt of $307M, but unearned revenue (which is not a true financial obligation) of $1.463B.

On the surface, the company's current ratio is an awful looking 0.59. However, once adjusted for unearned revenue, this ratio rises to a nearly acceptable 0.99.

Total assets amount to $13.853B, with no entry for goodwill or any other intangible asset. We appreciate that. Total liabilities less equity comes to $10.516B, including long-term debt of $2.76B, which is indeed a chunk, but is also less than twice cash on hand. There's another $740M in unearned revenue on the balance sheet too that is not considered current.

What Do I Think?

I think it could have been a lot worse.

Cash flows have to get turned around. Then, JetBlue can get started on profitability. At least, it had the good sense to walk away from the Spirit deal.

This is not a screaming "buy" by any chance. That said, I thought the balance sheet (which is not golden) was going to be a lot worse when I started doing the numbers.

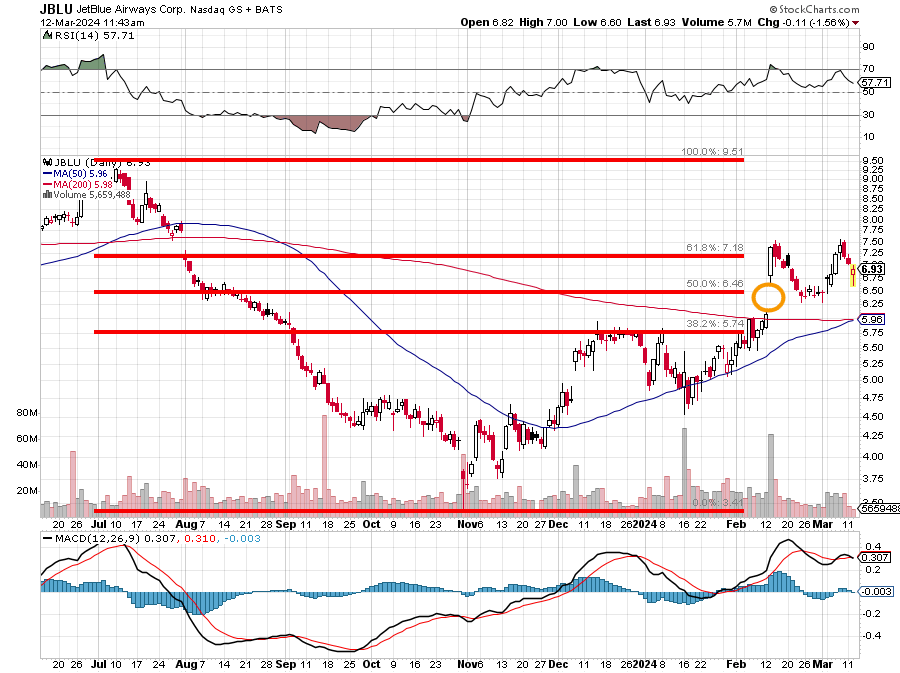

Readers will see in the above table that JBLU developed a double top reversal in February into March after retracing just a tad more than 61.8% of the entire July into November selloff. Does this set up a fill of the gap created about a month ago? I think it does.

JBLU needs to trade at $6.14 or lower to fill that gap. That makes selling June 21 $6 puts for about $0.44 seem fairly attractive if one is open to owning the shares at such a discount.

Just be cautious, the stock is near a "golden cross" as the 50-day simple moving average closes in on the 200-day SMA. That could provide a short-term rally.

At the time of publication, Guilfoyle had no positions in any securities mentioned.