Cisco Disappoints But There Is Hope: Here's the Trade

Guidance for both the quarter and the year is nothing short of dramatically disappointing on every single important metric.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Is this Groundhog Day?

Does it not seem like Cisco Systems CSCO on a semi-regular basis gets investor hopes up and then eventually disappoints eventually disappoints? I'm just glad that I did not come in long CSCO. This time.

For the firm's fiscal second quarter that ended January 27th, on Wednesday evening, Cisco posted an adjusted EPS of $0.87 (GAAP EPS: $0.65) on revenue of $12.791B. The non-GAAP EPS print beat Wall Street by a few pennies, while the revenue generation number did also beat Wall Street despite contracting 5,9% on a year over year basis.

Adjustments were made more for share-based compensation than anything else, which is ridiculous for a mature company such as Cisco. That's for start-ups. Once you've been around for decades and have been putting capital aside for share based compensation, it's part of your normal operating expenses.

I'm sorry, but I am so sick of established businesses finding ways to exclude their routine quarterly expenses from their adjusted earnings result.

Total software revenue was flat year over year, while software subscription revenue was up 5%. Total annualized recurring revenue (ARR) printed at $24.7B, which was up 6%. Product ARR was up 9%. Remaining Performance Obligation (RPO) now stands at $35.7B, up 12%, while Product RPO was also up 12%.

Operations

As revenue contracted 5.9% for the quarter to $12.791B, product-driven revenue contracted 9.1% to $9.232B. Service-driven revenue increased 3.5% to $3.559B. Cost of sales came in 11.4% to $4.574B, leaving a gross profit of $8.217B (-2.5%) on a gross margin of 64.2% (up from 62%). Service gross margin printed at 68.2%, as Product gross margin hit the tape at 62.7%.

Operating expenses including the whole kit and kaboodle came to $5.121B (-0.03%), leaving an operating income of $3.096B (-5.9%) on an operating margin of 24.2%, which was flat from the year ago comparison.

After accounting for interest and taxes, net income printed at $2.634B (-5%). This is how we get to earnings of $0.65 per diluted share. That, by the way, was in line with GAP expectations. The share based compensation adjustment was worth $0.20 per share by the way.

Geographic Performance

- Americas suffered a sales contraction of 4% to $7.51B, producing a gross margin of 65.7%

- EMEA suffered a sales contraction of 7% to $3.484B, producing a gross margin of 68.1%.

- APJC suffered a sales contraction of 12% to $1.798B, producing a gross margin of 68.2%.

Business Sales Performance

- Networking suffered a sales contraction of 12% to $7.081B.

- Security produced sales growth of 3% to $973M.

- Collaboration produced sales growth of 3% to $989M.

- Observability produced sales growth of 16% to $188M.

- Services produced sales growth of 4% to $3.559B.

Guidance

For the current (fiscal third) quarter, Cisco sees revenue of $12.1B to $12.3B, which was well below the $13.1B or so that Wall Street had in mind. Adjusted gross margin is seen at 66% to 67% as adjusted operating margin is projected at 33.5% to 34.5%. That puts the adjusted EPS for the quarter at $0.84 to $0.86. Wall Street was up around $0.92 on that one, so another nasty miss.

For the full fiscal year, the firm is projecting revenue generation of $51.5B to $52.25B. This drags the entire range below well below the $54.25B that Wall Street was looking for. Full year AAP EPS is seen at $2.61 to $2.73, while the adjusted EPS is now seen at $3.68B to $3.74B. Wall Street was up at $3.86 on this metric. Basically, this guidance for both the quarter and the year is nothing short of dramatically disappointing on every single important metric.

Fundamentals

Cisco generated operating cash flow of $3.179B (-63.5%) over the past six months. Out of this number, the firm spent $304M on capital expenditures, leaving free cash flow of $2.875B (-65.7%). Out of that number, Cisco repurchased $2.504B worth of common stock for the firm's treasury and paid out $3.163B in cash dividends to shareholders. Obviously, free cash flow of $2.875B over six months can not produce returns to shareholders of $5.667B for very long without becoming a problem.

Looking at the balance sheet, the firm ended the quarter with a cash position of $25.671B and inventories of $3.209B. This puts current assets at $42.127B. Current liabilities add up to $30.851B, including $4.936B in short-term debt and $14.011B in deferred revenue. On the surface, this leaves the firm with a current ratio of 1.37 and a quick ratio of 1.26. Once adjusted for current deferred revenue, those ratios rise to 2.5 and 2.31 respectively, so the current situation is healthy.

Total assets amount to $101.174B, including $40.765B in goodwill and other intangibles. At 40% of total assets, that is a little more than I am comfortable with. Total liabilities less equity comes to $54.923B, including $6.669B in long-term debt and another $11.76B in deferred revenue.

Bottom-line? Cisco has enough cash on hand to pay off all of its debt twice over, so while I do not love everything about this balance sheet, there is no problem here. This balance sheet can withstand a couple more quarters as sloppy as was this last one in terms of creating cash flows and then returning capital to stakeholders.

Wall Street

Since Cisco released these earnings last night, I have come across just nine sell-side analysts that have both opined on CSCO and are rated at a minimum of four stars by TipRanks. Among the nine, there are two "buy" or buy-equivalent ratings and seven "hold" or hold-equivalent ratings. Three of our "holds" did not set a target price so we are working with just six of those.

Across the six remaining analysts, the average target price is $51.83 with a high of $55 (Amit Daryanani of Evercore ISI and Tal Liani of Bank of America) twice and a low of $47 (James Fish of Piper Sandler). Once mitting one of those highs and that low, the average target price across the remaining four rises slightly to $52.25.

My Thoughts

The balance sheet is strong enough. Cash flows are strong, but unless they recover, returns to shareholders will have to be reduced significantly. That's not what the firm is doing. Cisco announced last night that the quarterly dividend would be increased by a penny to $0.40, good for a forward yield of 3.19%.

Obviously, the firm's business is not doing as well as Wall Street had thought as the guidance across both the current quarter and full year did not even come close to consensus view. This was the second consecutive quarter that Cisco reduced its full year outlook. The firm did announce layoffs that will amount to 4,000 individual positions or 5% of the firm's labor force being eliminated.

Need good news? Cisco did announce, according to CEO Chuck Robbins a "partnership with Nvidia NVDA during the quarter to offer enterprises simplified, cloud-based and on-prem AI infrastructure." Robbins added that this collaboration will include both networking hardware and software to support advanced AI workloads.

Additionally, Robbins addressed the pending acquisition of Splunk SPLK that Cisco announced last September. Robbins said, "The combination of Splunk's complementary capabilities with ours and AI, security and observability will create an end-to-end data platform to enhance our customers' digital resiliency."

On timing, Robbins added, "While the closing of the acquisition of Splunk remains subject to regulatory approvals and other customary closing conditions, given the positive progress to date on the required regulatory approvals, we now expect to close the transaction late in the first quarter or early in the second quarter of calendar year 2024, which is in our fiscal third quarter."

So, there is hope. It may come from the acquisition of Splunk and the collaboration with Nvidia, but there is hope.

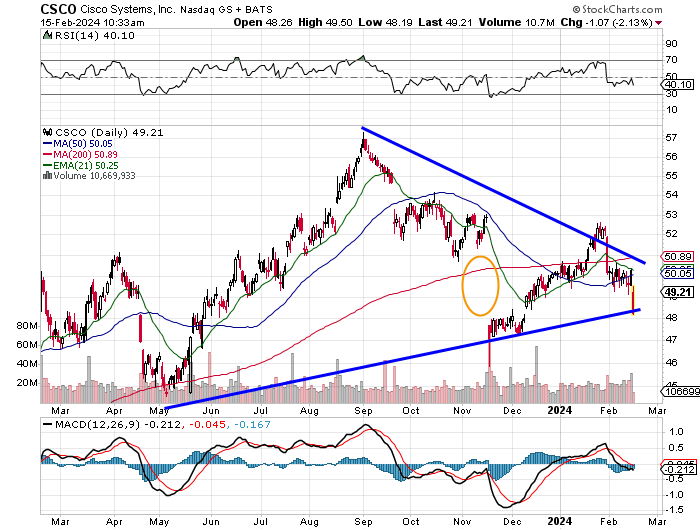

Readers will see that the symmetrical triangle that CSCO has been existing in since last May is closing. Upon that event, one would think that there will be a violent move of some sort. Right now, it feels like that move would be down, with a weaning reading for relative strength and a soft looking daily MACD (moving average convergence divergence). A break of that lower trendline could lead to prices as low mid-November or even last May.

I do not think I would risk a long side equity position at this time in this name.

If interested in a long side posturing in case there is good news regarding Splunk or the partnership with Nvidia, instead of purchasing equity above $49, I would rather write April 19th $47.50 puts for about $0.75 and purchase a like number of April 19th $45 puts for roughly $0.30 just as insurance.

This would leave the trader with a net credit of $0.45, or a net basis of $47.05 if that trader ends up having to eat the shares.

At the time of publication, Stephen Guilfoyle was long NVDA equity.